Problem 5-28A (continued)

2. The sales mix has shifted over the last year from Standard sets to

3. Sales commissions could be based on contribution margin rather than

on sales price. A flat rate on total contribution margin, as the text

suggests, might encourage the salespersons to emphasize the product

Problem 5-29A (60 minutes)

1. The income statements would be:

Present

Amount

Per Unit

%

Sales …………………….

$450,000

$30

100%

Variable expenses ……

315,000

21

70%

Contribution margin …

135,000

$ 9

30%

Fixed expenses ……….

90,000

Net operating income .

$ 45,000

Proposed

Amount

Per Unit

%

Sales …………………….

$450,000

$30

100%

Variable expenses* ….

180,000

12

40%

Contribution margin …

270,000

$18

60%

Fixed expenses ……….

225,000

Net operating income .

$ 45,000

*$21 – $9 = $12

2. a. Degree of operating leverage:

Present:

Contribution margin

Degree of

=

operating leverage Net operating income

$270,000

= = 6

$45,000

Problem 5-29A (continued)

b. Dollar sales to break even:

Problem 5-29A (continued)

3. The major factor would be the sensitivity of the company’s operations to

cyclical movements in the economy. Because the new equipment will

increase the CM ratio, in years of strong economic activity, the company

4. No information is given in the problem concerning the new variable

expenses or the new contribution margin ratio. Both of these items must

be determined before the new break-even point can be computed. The

computations are:

break even CM ratio 0.40

Problem 5-29A (continued)

The greatest risk is that the increases in sales and net operating income

predicted by the marketing manager will not happen and that sales will

remain at their present level. Note that the present level of sales is

Target profit + Fixed expenses

Dollar sales to =

attain target profit CM ratio

$45,000 + $180,000

= 0.40

= $562,500 in sales each month

Thus, sales would have to increase by at least 25% ($562,500 is 25%

Problem 5-30A (60 minutes)

1.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($40 − $16) × Q − $60,000

$0

= ($24) × Q − $60,000

$24Q

= $60,000

Q

= $60,000 ÷ $24

Q

= 2,500 pairs, or at $40 per pair, $100,000 in sales

Alternative solution:

Fixed expenses $60,000

Unit sales to = = = 2,500 pairs

break even CM per unit $24.00

Fixed expenses $60,000

Dollar sales to = = = $100,000

break even CM ratio 0.600

2. See the graphs at the end of this solution.

3.

Profit

= Unit CM × Q − Fixed expenses

$18,000

= $24 × Q − $60,000

$24Q

= $18,000 + $60,000

Q

= $78,000 ÷ $24

Q

= 3,250 pairs

Alternative solution:

Target profit + Fixed expenses

Unit sales to attain =

target profit Unit contribution margin

$18,000 + $60,000

= = 3,250 pairs

$24.00

4.

Incremental contribution margin:

$25,000 increased sales × 60% CM ratio …..

$15,000

Incremental fixed salary cost …………………….

8,000

Increased net income ………………………………

$ 7,000

Yes, the position should be converted to a full-time basis.

Problem 5-30A (continued)

5.

a.

Contribution margin $72,000

Degree of = = = 6

operating leverage Net operating income $12,000

b. 6.00 × 50% sales increase = 300%

increase

in net operating income.

Thus, net operating income next year would be: $12,000 + ($12,000

× 300%) = $48,000.

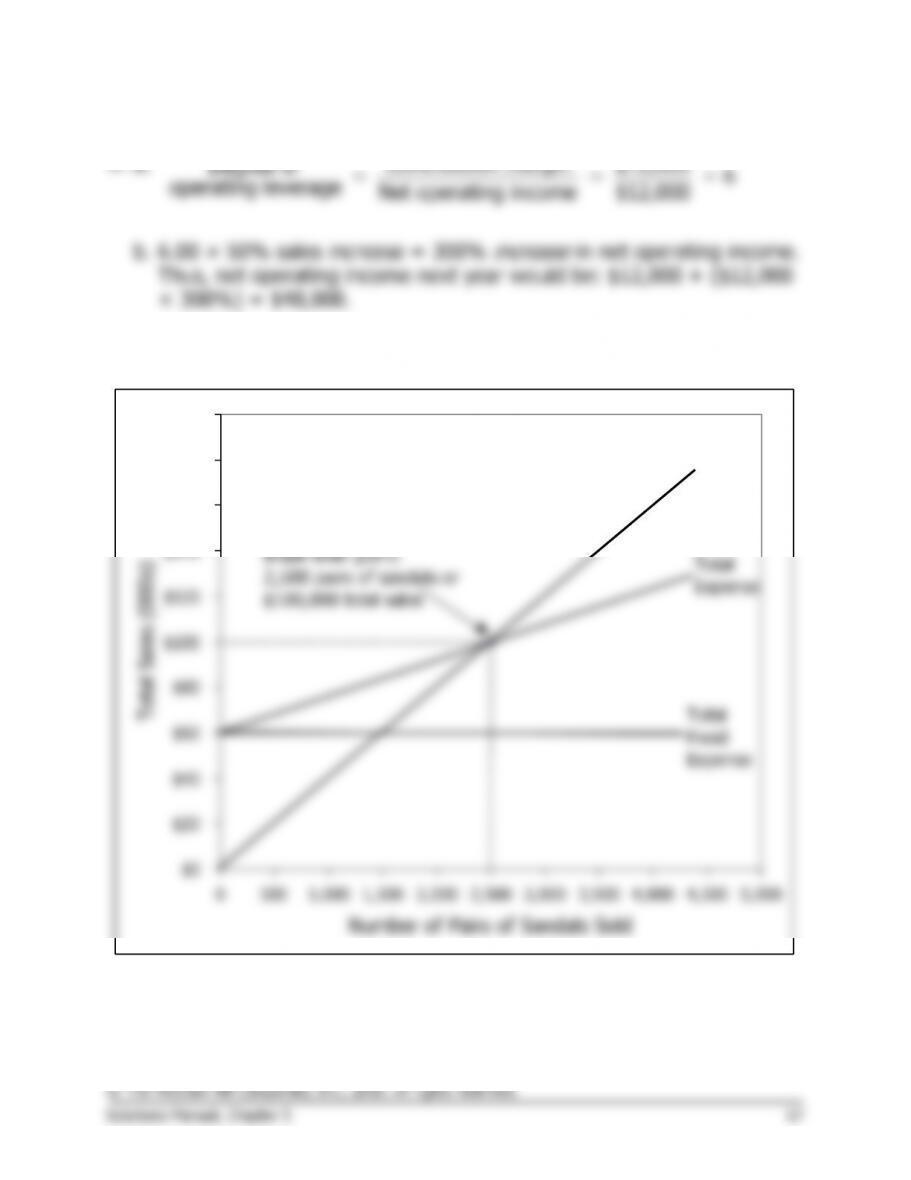

2. Cost-volume-profit graph:

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

0500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000

Number of Pairs of Sandals Sold

Total Sales (000s)

Break-even point:

2,500 pairs of sandals or

$100,000 total sales

Total Sales

Total

Expense

Total

Fixed

Expense

Problem 5-30A (continued)

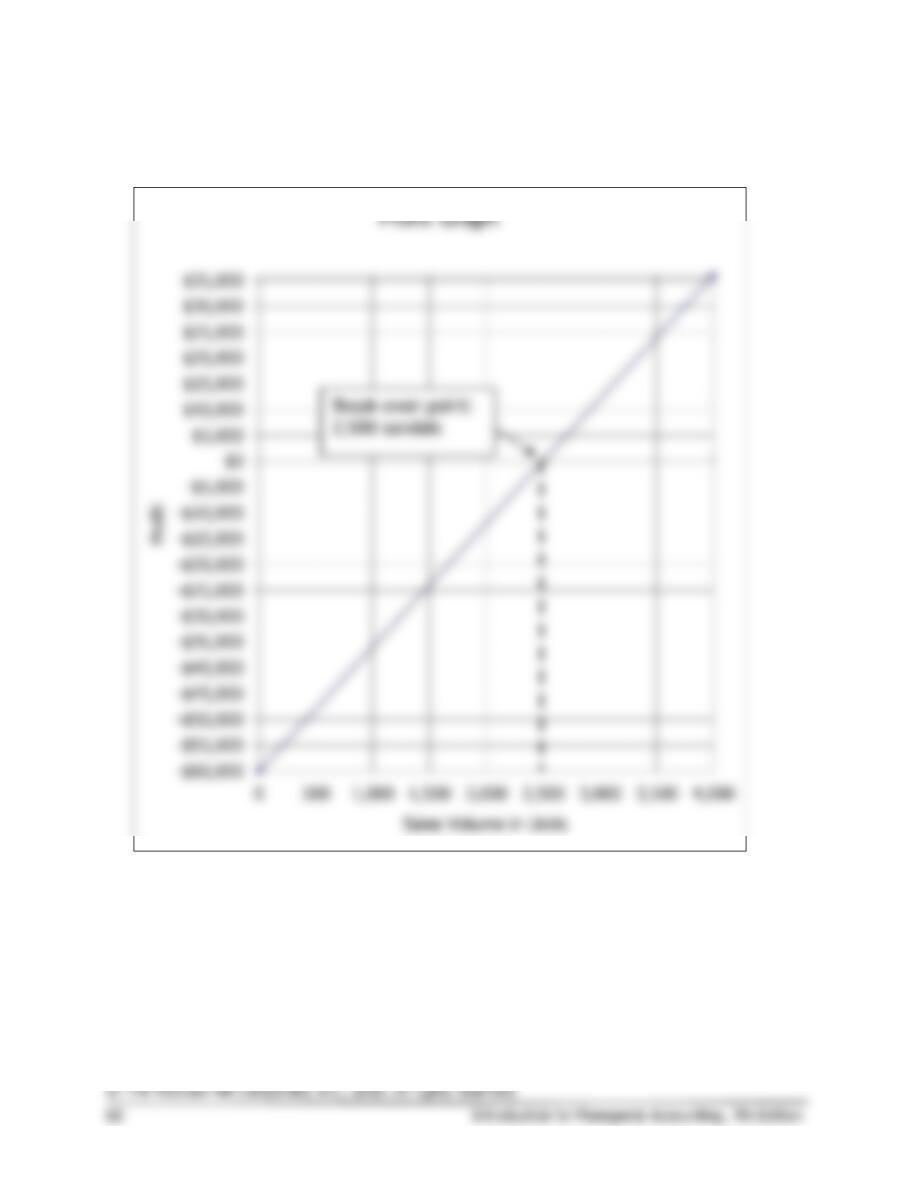

Profit graph:

-$60,000

-$55,000

-$50,000

-$45,000

-$40,000

-$35,000

-$30,000

-$25,000

-$20,000

-$15,000

-$10,000

-$5,000

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Profit

Sales Volume in Units

Profit Graph

Break-even point:

2,500 sandals

Problem 5-31A (30 minutes)

1.

(1)

Dollars

(2)

Volume of output, expressed in units, % of capacity, sales,

or some other measure

(3)

Total expense line

(4)

Variable expense area

(5)

Fixed expense area

(6)

Break-even point

(7)

Loss area

(8)

Profit area

(9)

Sales line

Problem 5-31A (continued)

2.

a.

Line 3:

Remain unchanged.

Line 9:

Have a steeper slope.

Break-even point:

Decrease.

b.

Line 3:

Have a flatter slope.

Line 9:

Remain unchanged.

Break-even point:

Decrease.

c.

Line 3:

Shift upward.

Line 9:

Remain unchanged.

Break-even point:

Increase.

d.

Line 3:

Remain unchanged.

Line 9:

Remain unchanged.

Break-even point:

Remain unchanged.

e.

Line 3:

Shift downward and have a steeper slope.

Line 9:

Remain unchanged.

Break-even point:

Probably change, but the direction is uncertain.

f.

Line 3:

Have a steeper slope.

Line 9:

Have a steeper slope.

Break-even point:

Remain unchanged in terms of units; increase

in terms of total dollars of sales.

g.

Line 3:

Shift upward.

Line 9:

Remain unchanged.

Break-even point:

Increase.

h.

Line 3:

Shift upward and have a flatter slope.

Line 9:

Remain unchanged.

Break-even point:

Probably change, but the direction is uncertain.

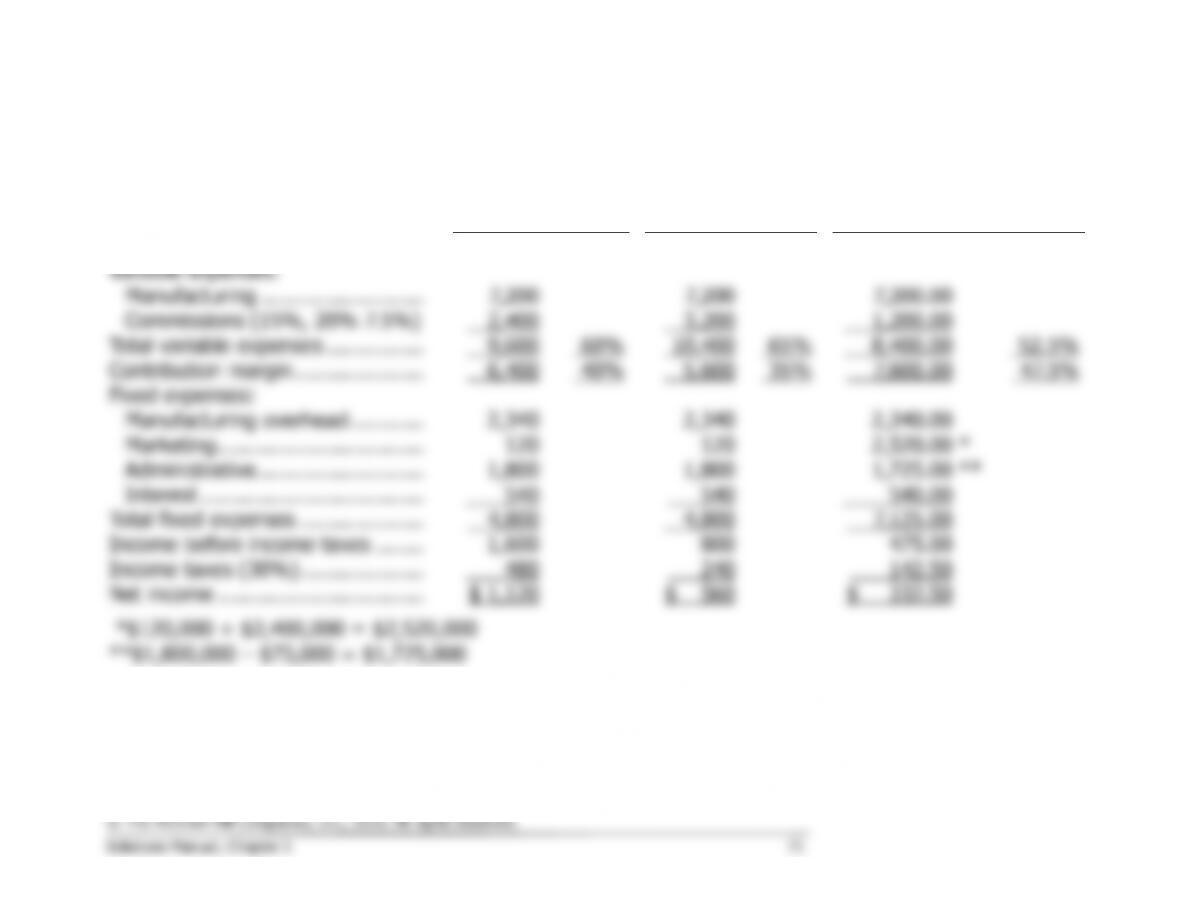

Case (75 minutes)

Before proceeding with the solution, it is helpful first to restructure the data into contribution format for

each of the three alternatives. (The data in the statements below are in thousands.)

15% Commission

20% Commission

Own Sales Force

Sales ……………………………………

$16,000

100%

$16,000

100%

$16,000.00

100.0%

Variable expenses:

Manufacturing ……………………..

7,200

7,200

7,200.00

Commissions (15%, 20% 7.5%)

2,400

3,200

1,200.00

Total variable expenses …………….

9,600

60%

10,400

65%

8,400.00

52.5%

Contribution margin …………………

6,400

40%

5,600

35%

7,600.00

47.5%

Fixed expenses:

Manufacturing overhead …………

2,340

2,340

2,340.00

Marketing …………………………...

120

120

2,520.00

*

Administrative ………………………

1,800

1,800

1,725.00

**

Interest ………………………………

540

540

540.00

Total fixed expenses ………………..

4,800

4,800

7,125.00

Income before income taxes ……..

1,600

800

475.00

Income taxes (30%) ………………..

480

240

142.50

Net income …………………………...

$ 1,120

$ 560

$ 332.50

*$120,000 + $2,400,000 = $2,520,000

**$1,800,000 – $75,000 = $1,725,000

Case (continued)

1. When the income before taxes is zero, income taxes will also be zero

and net income will be zero. Therefore, the break-even calculations can

be based on the income before taxes.

a. Break–even point in dollar sales if the commission remains 15%:

Fixed expenses $4,800,000

Dollar sales to = = = $12,000,000

break even CM ratio 0.40

b. Break-even point in dollar sales if the commission increases to 20%:

Fixed expenses $4,800,000

Dollar sales to = = = $13,714,286

break even CM ratio 0.35

c. Break–even point in dollar sales if the company employs its own sales

force:

Fixed expenses $7,125,000

Dollar sales to = = = $15,000,000

break even CM ratio 0.475

2. In order to generate a $1,120,000 net income, the company must

generate $1,600,000 in income before taxes. Therefore,

Target income before taxes + Fixed expenses

Dollar sales to =

attain target CM ratio

$1,600,000 + $4,800,000

=

0.35

$6,400,000

= = $18,285,714

0.35

3. To determine the volume of sales at which net income would be equal

under either the 20% commission plan or the company sales force plan,

Case (continued)

X =

Total sales revenue

0.65X + $4,800,000 =

0.525X + $7,125,000

0.125X =

$2,325,000

X =

$2,325,000 ÷ 0.125

X =

$18,600,000

Thus, at a sales level of $18,600,000 either plan would yield the same

income before taxes and net income. Below this sales level, the

commission plan would yield the largest net income; above this sales

level, the sales force plan would yield the largest net income.

4. a., b., and c.

15%

Commission

20%

Commission

Own

Sales Force

Contribution margin (Part 1) (a) ….

$6,400,000

$5,600,000

$7,600,000

Income before taxes (Part 1) (b) …

$1,600,000

$800,000

$475,000

Degree of operating leverage:

(a) ÷ (b) ……………………………..

4

7

16

5. We would continue to use the sales agents for at least one more year,

and possibly for two more years. The reasons are as follows:

First, use of the sales agents would have a less dramatic effect on

net income.

Second, use of the sales agents for at least one more year would

Analytical Thinking (60 minutes)

Note: This is a problem that will challenge the very best students’ conceptual

and analytical skills. However, working through this case will yield substantial

dividends in terms of a much deeper understanding of critical management

accounting concepts.

1. The overall break-even sales can be determined using the CM ratio.

Velcro

Metal

Nylon

Total

Sales ……………………….

$165,000

$300,000

$340,000

$805,000

Variable expenses ………

125,000

140,000

100,000

365,000

Contribution margin …….

$ 40,000

$160,000

$240,000

440,000

Fixed expenses…………..

400,000

Net operating income ….

$ 40,000

Contribution margin $440,000

CM ratio = = = 0.5466

Sales $805,000

Fixed expenses $400,000

Dollar sales to = = = $732,000 (rounded)

break even CM ratio 0.5466

2. The issue is what to do with the common fixed cost when computing

the break-evens for the individual products. The correct approach is to

ignore the common fixed costs. If the common fixed costs are included

in the computations, the break-even points will be overstated for

individual products and managers may drop products that in fact are

Velcro

Metal

Nylon

Unit selling price ……………………………..

$1.65

$1.50

$0.85

Variable cost per unit ……………………….

1.25

0.70

0.25

Unit contribution margin (a) ………………

$0.40

$0.80

$0.60

Product fixed expenses (b)………………..

$20,000

$80,000

$60,000

Unit sales to break even (b) ÷ (a) ………

50,000

100,000

100,000

Analytical Thinking (continued)

b. If the company were to sell exactly the break-even quantities

computed above, the company would lose $240,000—the amount of

the common fixed cost. This can be verified as follows:

Velcro

Metal

Nylon

Total

Unit sales ……………….

50,000

100,000

100,000

Sales ……………………..

$82,500

$150,000

$85,000

$317,500

Variable expenses …….

62,500

70,000

25,000

157,500

Contribution margin ….

$20,000

$ 80,000

$60,000

160,000

Fixed expenses ………..

400,000

Net operating loss …….

$(240,000)

At this point, many students conclude that something is wrong with

their answer to part (a) because a result in which the company loses

money operating at the break-evens for the individual products does not

seem to make sense. They also worry that managers may be lulled into

a false sense of security if they are given the break-evens computed in

part (a). Total sales at the individual product break-evens is only

$317,500, whereas the total sales at the overall break-even computed in

part (1) is $732,000.

Many students (and managers, for that matter) attempt to resolve this

apparent paradox by allocating the common fixed costs among the

products prior to computing the break-evens for individual products. Any

of a number of allocation bases could be used for this purpose—sales,