Problem 9-14B (30 minutes)

1.

Present

New Line

Total

(1)

Sales …………………….

$22,000,000

$10,290,000

$32,290,000

(2)

Net operating income .

1,826,000

730,590

*

2,556,590

(3)

Operating assets ……..

5,500,000

3,430,000

8,930,000

(4)

Margin (2) ÷ (1) ………

8.30%

7.10%

7.92 %

(5)

Turnover (1) ÷ (3) ……

4.00

3.00

3.62

(6)

ROI (4) × (5) ………….

33.20%

21.30%

28.63 %

*

Sales …………………………………………………….

$10,290,000

Variable expenses (65% × $10,290,000)………

6,688,500

Contribution margin …………………………………

3,601,500

Fixed expenses ……………………………………….

2,870,910

Net operating income ……………………………….

$ 730,590

2. Brian Stettler will be inclined to reject the new product line because

accepting it would reduce his division’s overall rate of return.

4.

a.

Present

New Line

Total

Operating assets …………………

$5,500,000

$3,430,000

$8,930,000

Minimum required return ………

×15 %

×15 %

×15 %

Minimum net operating income

$825,000

$514,500

$1,339,500

Actual net operating income ….

$1,826,000

$ 730,590

$ 2,556,590

Minimum net operating income

(above) …………………………..

825,000

514,500

1,339,500

Residual income ………………….

$1,001,000

$ 216,090

$1,217,090

b. Under the residual income approach, Brian Stettler would be inclined

Problem 9-15B (30 minutes)

1. Breaking the ROI computation into two separate elements helps the

manager to see important relationships that might remain hidden. First,

the importance of turnover of assets as a key element to overall

profitability is emphasized. Prior to use of the ROI formula, managers

2.

Companies in the Same Industry

X

Y

Z

Sales …………………………….

$3,910,000

*

$1,390,000

*

$6,336,000

Net operating income ……….

$664,700

*

$180,700

*

$316,800

Average operating assets …..

$1,700,000

*

$2,780,000

$2,640,000

*

Margin …………………………..

17%

13%

5 %

*

Turnover ………………………..

2.3

0.5

2.4

*

Return on investment (ROI) .

39.1%

6.50%

*

12%

Problem 9-15B (continued)

NAA Report No. 35

states (p. 35): “Introducing sales to measure level of

operations helps to disclose specific areas for more intensive

investigation.”

Company Y’s margin is somewhat lower than that of Company X. Why

Process time ÷ Throughput time …..

Delivery cycle time in days:

Wait time ………………………………..

Total throughput time …………………

Total delivery cycle time ……………..

Problem 9-16B (30 minutes)

1. a., b., and c.

Month

1

2

3

4

Throughput time in days:

Process time …………………………....

0.5

0.8

0.7

0.6

Inspection time …………………………

0.6

0.7

0.5

0.5

Move time ……………………………….

0.5

0.7

0.5

0.3

Queue time ……………………………..

3.0

3.0

2.0

1.0

Total throughput time …………………

4.6

5.2

3.7

2.4

Problem 9-16B (continued)

3. a. and b.

Month

5

6

Throughput time in days:

Process time …………………………..……..

0.6

0.6

Inspection time ………………………………

0.5

Move time …………………………………….

0.3

0.3

Queue time …………………………………..

Total throughput time ………………………

1.4

0.9

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time ………..

42.9%

66.7%

As a company pares away non-value-added activities, the manufacturing

cycle efficiency improves. The goal, of course, is to have an efficiency of

100%. This will be achieved when all non-value-added activities have

been eliminated and process time equals throughput time.

=

12% × 2.80 = 33.60%

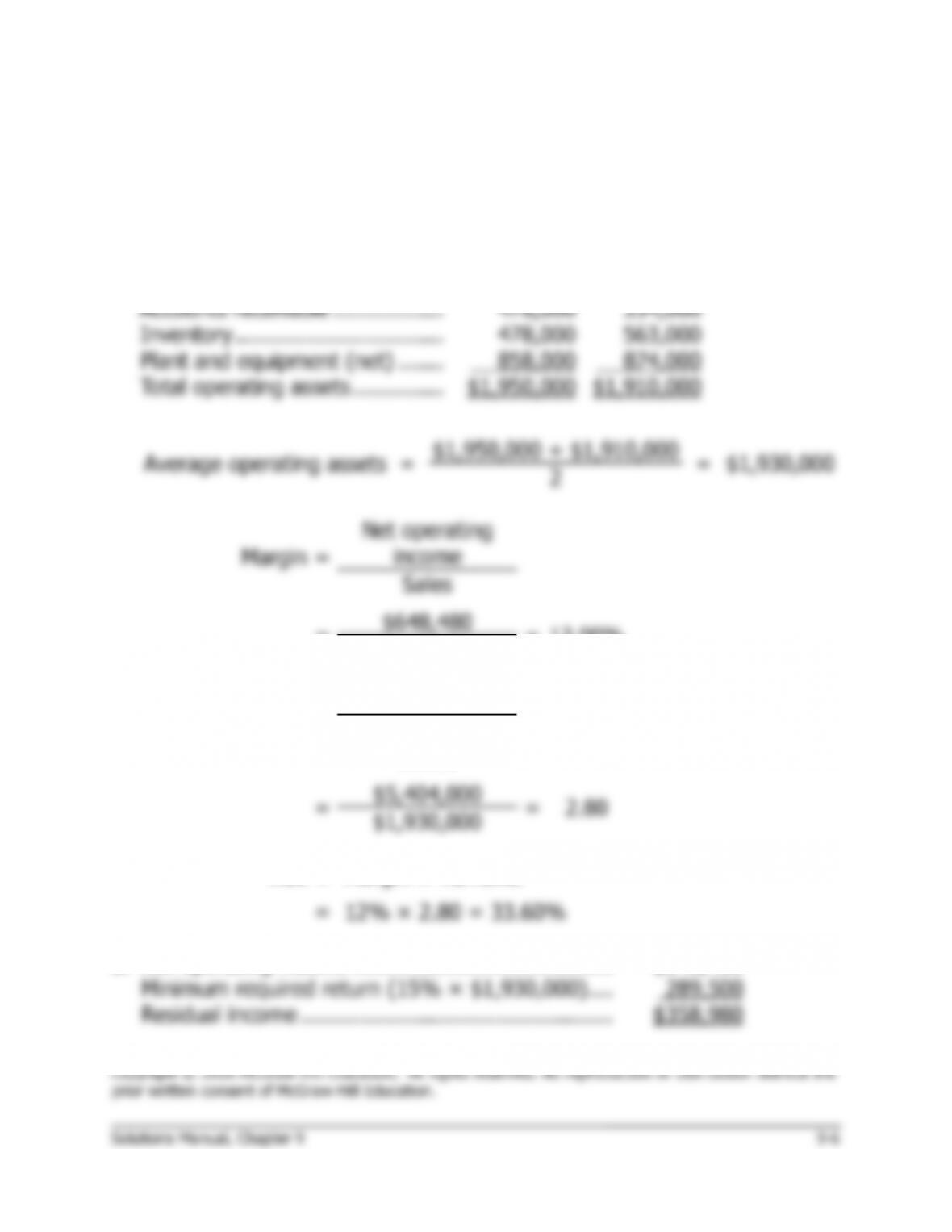

Net operating income ………………………………….

Minimum required return (15% × $1,930,000) ….

Residual income …………………………………………

Problem 9-17B (20 minutes)

1. Operating assets do not include investments in other companies or in

undeveloped land.

Ending

Balances

Beginning

Balances

Cash …………………………………

$ 136,000

$ 139,000

Accounts receivable ……………..

478,000

334,000

Inventory …………………………..

478,000

563,000

Plant and equipment (net) …….

858,000

874,000

Total operating assets …………..

$1,950,000

$1,910,000

Average operating assets

=

$1,950,000 + $1,910,000

=

$1,930,000

2

Margin

=

Net operating

income

Sales

=

$648,480

=

12.00%

$5,404,000

Turnover

=

Sales

Average operating

assets

=

$5,404,000

=

2.80

$1,930,000

ROI

=

Margin × Turnover

16.71%

18.91%

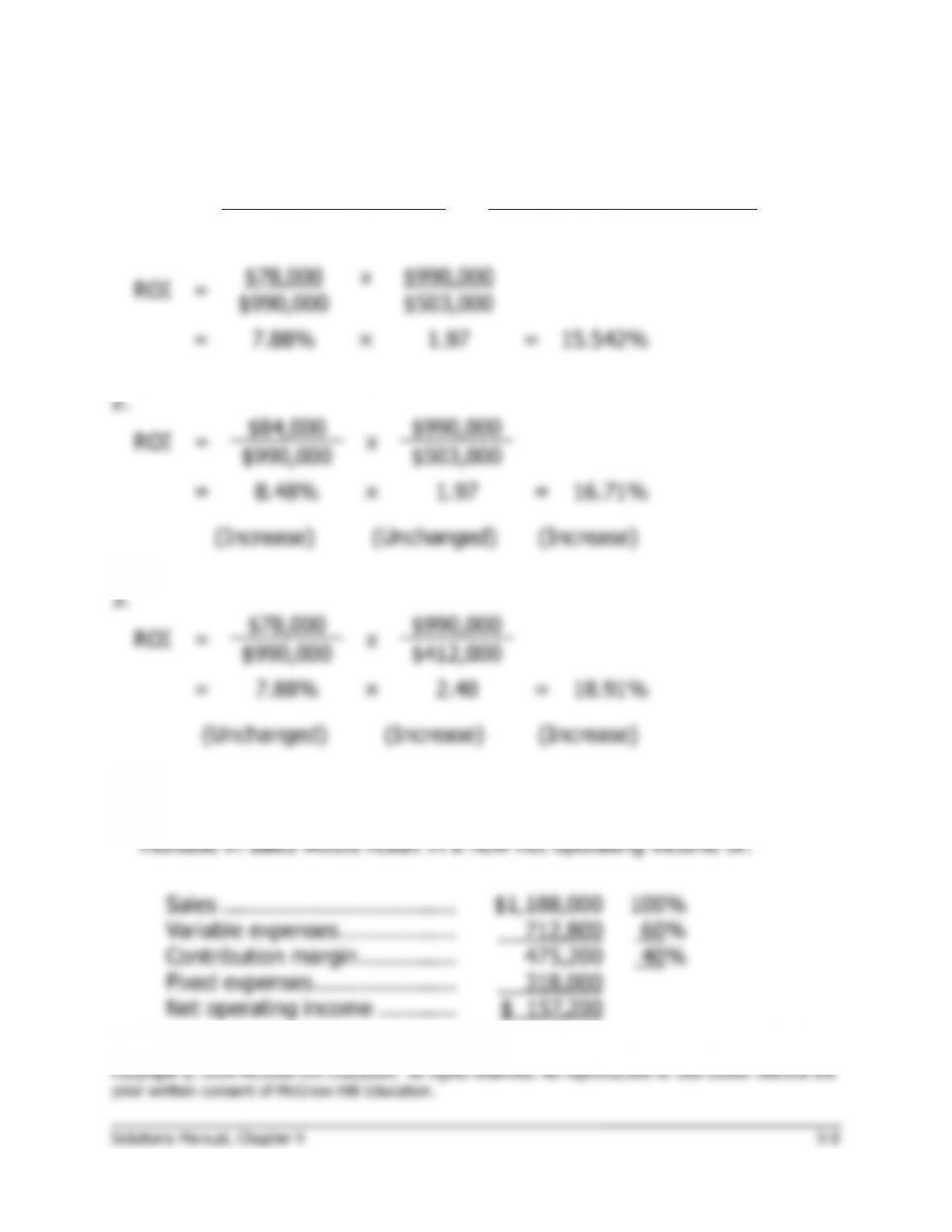

Problem 9-18B (30 minutes)

1.

ROI

=

Net operating income

x

Sales

Sales

Average operating assets

ROI

=

$78,000

x

$990,000

$990,000

$503,000

=

7.88%

×

1.97

=

15.542%

Problem 9-18B (continued)

ROI

=

$157,200

x

$1,188,000

$1,188,000

$503,000

=

13.23%

×

2.36

=

31.22%

(Increase)

(Increase)

(Increase)

5. Interest is a financing expense and thus is not used to compute net

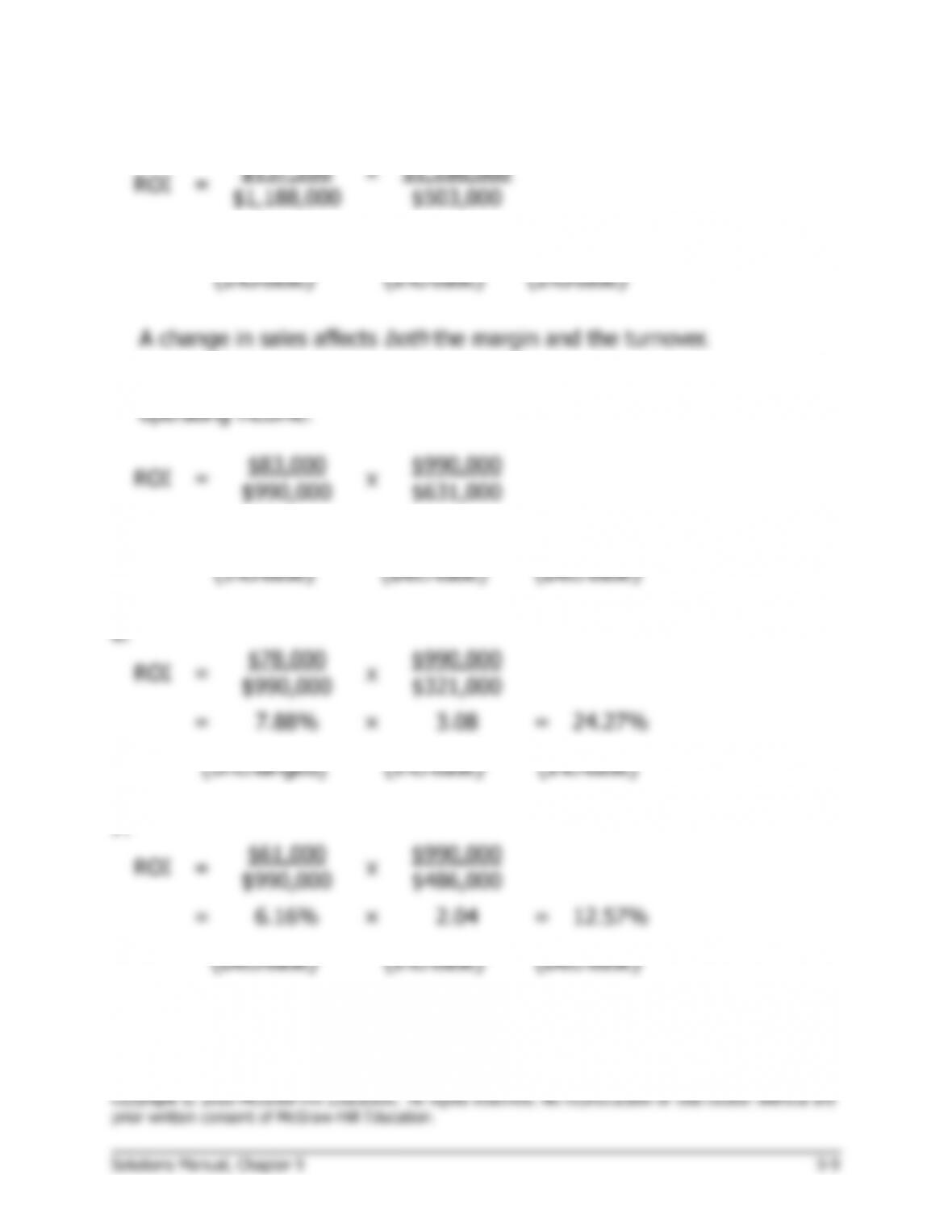

ROI

=

=

×

1.57

=

13.15%

(Increase)

=

×

3.08

=

24.27%

(Increase)

ROI

=

=

×

2.04

=

12.57%

(Increase)

Problem 9-19B (30 minutes)

1. a., b., and c.

Month

1

2

3

4

Throughput time in days:

Process time …………………………..….

0.5

0.5

0.5

0.5

Inspection time …………………………..

0.1

0.1

0.5

0.6

Move time …………………………………

1.4

1.3

1.3

1.4

Queue time ……………………………….

5.6

5.7

5.6

5.7

Total throughput time …………………..

7.6

7.6

7.9

8.2

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time …….

6.6%

6.6%

6.3%

6.1%

Delivery cycle time in days:

Wait time ………………………………….

15.6

14.5

11.8

9.0

Total throughput time …………………..

7.6

7.6

7.9

8.2

Total delivery cycle time ……………….

23.2

22.1

19.7

17.2

2. a. The company seems to be improving mainly in the areas of quality

control, material control, on-time delivery, and total delivery cycle

time. Customer complaints, warranty claims, defects, and scrap are

Problem 9-19B (continued)

c. While it is difficult to draw any definitive conclusions, it appears that

the company has concentrated first on those areas of performance

3. a. and b.

Month

5

6

Throughput time in days:

Process time …………………………..……….

0.5

0.5

Inspection time ………………………………..

0.6

0.0

Move time ………………………………………

1.4

1.4

Queue time …………………………………….

0.0

0.0

Total throughput time ………………………..

2.5

1.9

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time ………….

20.0%

26.3%

As non-value-added activities are eliminated, the manufacturing cycle

efficiency improves. The goal, of course, is to have an efficiency of

100%. This is achieved when all non-value-added activities have been

eliminated and process time equals throughput time.