Problem 13-18A (continued)

b.

Sabin Electronics

Common-Size Income Statements

This Year

Last Year

Sales ……………………………………………..

100.0

%

100.0

%

Cost of goods sold …………………………….

77.5

79.3

Gross margin …………………………………..

22.5

20.7

Selling and administrative expenses ……..

13.1

12.6

Net operating income ………………………..

9.4

8.1

Interest expense ………………………………

1.4

1.7

Net income before taxes …………………….

8.0

6.4

Income taxes …………………………………..

2.4

1.9

Net income ……………………………………..

5.6

%

4.5

%

3. The following points can be made from the analytical work in parts (1)

and (2) above:

a. The company’s current position has deteriorated significantly since

last year. Both the current ratio and the acid-test ratio are well below

the industry average and are trending downward. At the present rate,

Problem 13-18A (continued)

c. The inventory turned only five times this year as compared to over six

times last year. It takes nearly two weeks longer for the company to

turn its inventory than the average for the industry (73 days as

Problem 13-19A (45 minutes)

This Year

Last Year

1.

a.

Net income (a) ……………………………….

$280,000

$196,000

Average number of common shares (b) .

50,000

50,000

Earnings per share (a) ÷ (b) ……………..

$5.60

$3.92

b.

Dividends per share (a) ……………………

$2.20

$1.90

Market price per share (b) ………………..

$40.00

$36.00

Dividend yield ratio (a) ÷ (b)……………..

5.5%

5.3%

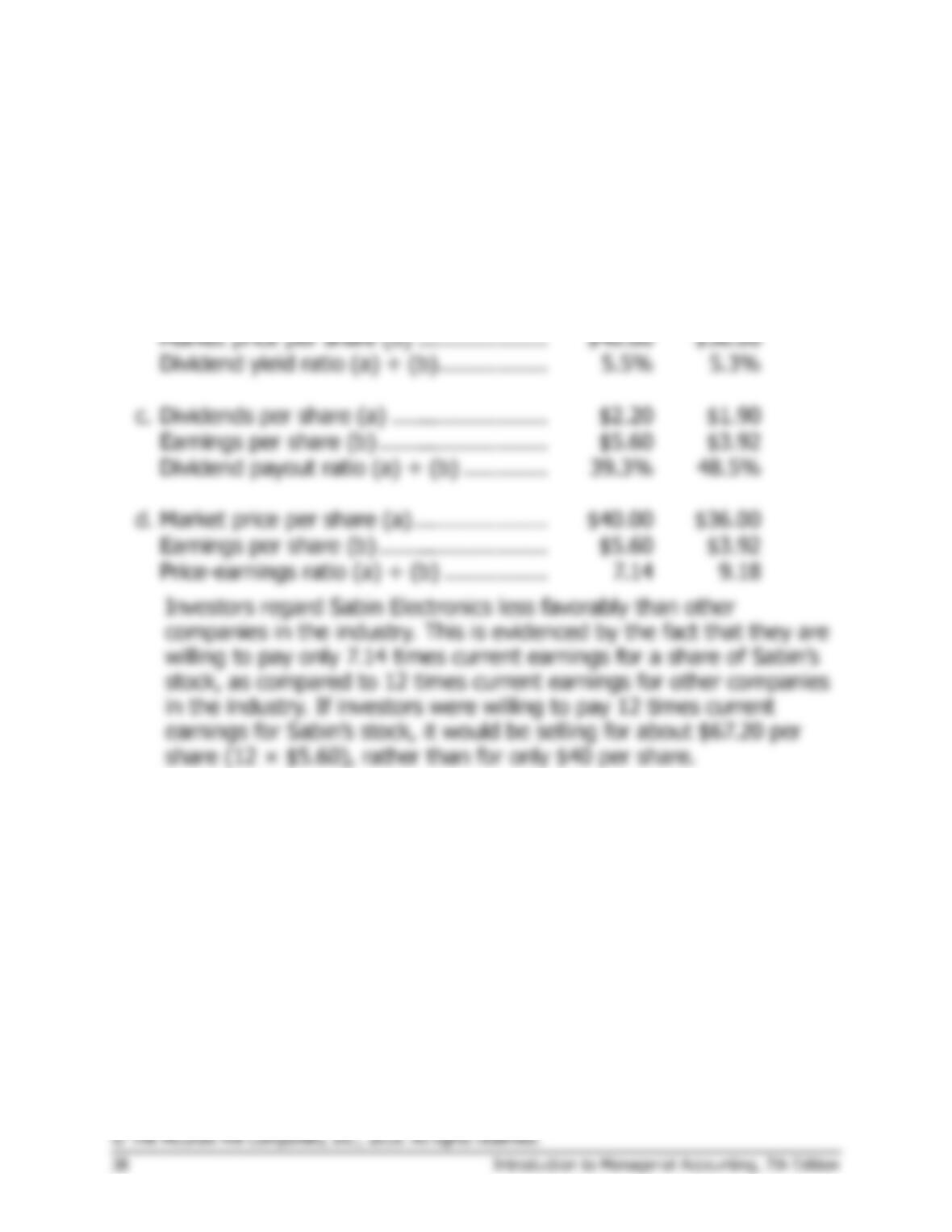

c.

Dividends per share (a) ……………………

$2.20

$1.90

Earnings per share (b) ……………………..

$5.60

$3.92

Dividend payout ratio (a) ÷ (b) ………….

39.3%

48.5%

d.

Market price per share (a)…………………

$40.00

$36.00

Earnings per share (b) ……………………..

$5.60

$3.92

Price-earnings ratio (a) ÷ (b) …………….

7.14

9.18

Investors regard Sabin Electronics less favorably than other

companies in the industry. This is evidenced by the fact that they are

willing to pay only 7.14 times current earnings for a share of Sabin’s

stock, as compared to 12 times current earnings for other companies

in the industry. If investors were willing to pay 12 times current

earnings for Sabin’s stock, it would be selling for about $67.20 per

share (12 × $5.60), rather than for only $40 per share.

Problem 13-19A (continued)

This Year

Last Year

e.

Total stockholders’ equity (a) ………………..

$1,600,000

$1,430,000

Number of common shares outstanding

(b) ………………………………………………..

50,000

50,000

Book value per share (a) ÷ (b) ………………

$32.00

$28.60

The market value is above book value for both years. However, this

does not necessarily indicate that the stock is overpriced. Market

value reflects investors’ perceptions of future earnings, whereas book

value is a result of already completed transactions.

This Year

Last Year

2.

a.

Gross margin (a) ……………………………..

$1,125,000

$900,000

Sales (b) ………………………………………..

$5,000,000

$4,350,000

Gross margin percentage (a) ÷ (b) ………

22.5%

20.7%

b.

Net income (a) ………………………………..

$280,000

$196,000

Sales (b) ………………………………………..

$5,000,000

$4,350,000

Net profit margin percentage (a) ÷ (b) …

5.6%

4.5%

c.

Net income …………………………………….

$ 280,000

$ 196,000

Add after-tax cost of interest paid:

[$72,000 × (1 – 0.30)] ……………………

50,400

50,400

Total (a) …………………………………………

$ 330,400

$ 246,400

Average total assets (b) …………………….

$2,730,000

$2,440,000

Return on total assets (a) ÷ (b) …………..

12.1%

10.1%

d.

Net income (a) ………………………………..

$ 280,000

$ 196,000

Average stockholders’ equity (b) ………….

$1,515,000

$1,425,000

Return on equity (a) ÷ (b) …………………

18.5%

13.8%

Problem 13-19A (continued)

e. Financial leverage is positive in both years because the return on

3. All profitability measures and the earnings per share are trending

upwards, which is a good sign. However, the price-earnings ratio has

dropped from 9.18 to 7.14. This decline indicates investor concerns

growth.

Ethics Challenge (45 minutes)

1. The loan officer stipulated that the current ratio prior to obtaining the

loan must be higher than 2.0, the acid-test ratio must be higher than

1.0, and the interest on the loan must be less than four times net

operating income. These ratios are computed below:

Current assets

Current ratio =

Current liabilities

$290,000

= = 1.8 (rounded)

$164,000

Acid-test ratio = Cash + Marketable securities + Current receivables

Current liabilities

$70,000 + $0 + $50,000

= = 0.7 (rounded)

$164,000

Net operating income $20,000

= = 5.0

Interest on the loan $80,000 × 0.10 × (6/12)

The company would fail to qualify for the loan because both its current

ratio and its acid-test ratio are too low.

Ethics Challenge (continued)

2. By reclassifying the $45 thousand net book value of the old machine as

inventory, the current ratio would improve, but the acid-test ratio would

be unaffected. Inventory is considered a current asset for purposes of

computing the current ratio, but is not included in the numerator when

computing the acid-test ratio.

Current assets

Current ratio =

Current liabilities

we strongly advise against it. Inventories are assets the company has

Ethics Challenge (continued)

Nevertheless, the old machine is an asset that could be turned into

cash. If this were done, the company would immediately qualify for the

loan because the $45 thousand in cash would be included in the

numerator in both the current ratio and in the acid-test ratio.

Current assets

Current ratio =

Current liabilities

$290,000 + $45,000

= = 2.0 (rounded)

$164,000

Acid-test ratio = Cash + Marketable securities + Current receivables

Current liabilities

$70,000 + $0 + $50,000 + $45,000

= = 1.0 (rounded)

$164,000

the loan.

Analytical Thinking (60 minutes or longer)

Pepper Industries

Income Statement

For the Year Ended March 31

Key to

Computation

Sales …………………………………………

$4,200,000

Cost of goods sold ……………………….

2,730,000

(h)

Gross margin …………………………..….

1,470,000

(i)

Selling and administrative expenses …

930,000

(j)

Net operating income ……………………

540,000

(a)

Interest expense ………………………….

80,000

Net income before taxes ……………….

460,000

(b)

Income taxes (30%) …………………….

138,000

(c)

Net income …………………………………

$ 322,000

(d)

Pepper Industries

Balance Sheet

March 31

Current assets:

Cash ……………………………………….

$ 70,000

(f)

Accounts receivable, net ……………..

330,000

(e)

Inventory …………………………………

480,000

(g)

Total current assets ………………………

880,000

(g)

Plant and equipment …………………….

1,520,000

(q)

Total assets …………………………..……

$2,400,000

(p)

Current liabilities ………………………….

$ 320,000

Bonds payable, 10% …………………….

800,000

(k)

Total liabilities ……………………………..

1,120,000

(l)

Stockholders’ equity:

Common stock, $5 par value ………..

700,000

(m)

Retained earnings ……………………..

580,000

(o)

Total stockholders’ equity ………………

1,280,000

(n)

Total liabilities and equity ………………

$2,400,000

(p)

Analytical Thinking (continued)

Computation of missing amounts:

a.

Earnings before interest and taxes

Times interest earned = Interest expense

Earnings before interest and taxes

= $80,000

= 6.75

Therefore, the earnings before interest and taxes for the year must be

$540,000.

b. Net income before taxes = $540,000 – $80,000 = $460,000

f.

Cash + Marketable securities + Current receivables

Acid-test ratio= Current liabilities

Cash + Marketable securities + Current receivables

= $320,000

= 1.25

Analytical Thinking (continued)

Therefore, the total quick assets must be $400,000. Because there are

no marketable securities and the accounts receivable are $330,000, the

cash must be $70,000.

g.

Current assets

Current ratio = Current liabilities

Current assets

= $320,000

= 2.75

Therefore, the current assets must total $880,000. Because the quick

assets (cash and accounts receivable) total $400,000 of this amount, the

inventory must be $480,000.

h.

Cost of goods sold

Inventory turnover = Average inventory

Cost of goods sold

= ($360,000 + $480,000)/2

Cost of goods sold

= $420,000

= 6.5

Therefore, the cost of goods sold for the year must be $2,730,000.

i. Gross margin = $4,200,000 – $2,730,000 = $1,470,000.

j.

Net operating income = Gross margin – Operating expenses

Operating expenses = Gross margin – Net operating income

= $1,470,000 – $540,000

= $930,000

Analytical Thinking (continued)

k. The interest expense for the year was $80,000 and the interest rate was

10%, the bonds payable must total $800,000.

m.

Net income – Preferred dividends

Earnings per share = Average number of common shares outstanding

$322,000

=

Average number of common shares outstanding

= $2.30

The stock is $5 par value per share, so the total common stock must be

$700,000 ($5 × 140,000 shares).

n.

Total liabilities

Debt-to-equity ratio = Stockholders’ equity

$1,120,000

= Stockholders’ equity

= 0.875

Therefore, the total stockholders’ equity must be $1,280,000.

o.

Total stockholders’ equity = Common stock + Retained earnings

Retained earnings = Total stockholders’ equity – Common Stock

= $1,280,000 – $700,000 = $580,000

Analytical Thinking (continued)

p.

Total assets = Liabilities + Stockholders’ equity

= $1,120,000 + $1,280,000 = $2,400,000

This answer can also be obtained using the return on total assets:

Net income + [Interest expense × (1 – Tax rate)]

Return on =

total assets Average total assets

$322,000 + [$80,000 × (1 – 0.30)]

= Average total assets

$378,000

= Average total assets

= 18.0%

Therefore the average total assets must be $2,100,000. Since the total

q.

Total assets = Current assets + Plant and equipment

$2,400,000 = $880,000 + Plant and equipment

Plant and equipment = $2,400,000 – $880,000

= $1,520,000

Teamwork in Action

The answer to this question will depend on the company that the students

analyze.