Chapter 7

Master Budgeting

Solutions to Questions

7-1 A budget is a detailed quantitative plan

for the acquisition and use of financial and other

7-2

1. Budgets communicate management’s

2. Budgets force managers to think about

and plan for the future. In the absence of the

3. The budgeting process provides a means

4. The budgeting process can uncover

5. Budgets coordinate the activities of the

entire organization by integrating the plans of its

6. Budgets define goals and objectives that

7-3 Responsibility accounting is a system in

which a manager is held responsible for those

items of revenues and costs—and only those

7-4 A master budget represents a summary

of all of management’s plans and goals for the

future, and outlines the way in which these

plans are to be accomplished. The master

income statement, budgeted balance sheet, and

cash budget.

7-5 The level of sales impacts virtually every

other aspect of the firm’s activities. It

cash budget and budgeted income statement

although related, concepts. Planning involves

achieve those goals. Control, by contrast,

involves the means by which management

7-7 Creating a “budgeting assumptions” tab

the projected financial statements.

7-8 A self-imposed budget is one in which

views and judgments are valued. (2) Budget

estimates prepared by front-line managers are

often more accurate and reliable than estimates

prepared by top managers who have less

7-9 The direct labor budget and other

budgets can be used to forecast workforce

The Foundational 15

1. The budgeted sales for July are computed as follows:

Unit sales (a) ………………………..

10,000

Selling price per unit (b) ………….

$70

Total sales (a) × (b) ……………….

$700,000

2. The expected cash collections for July are computed as follows:

July

June sales:

$588,000 × 60% ……………….

$352,800

July sales:

$700,000 × 40% ……………….

280,000

Total cash collections …………….

$632,800

3. The accounts receivable balance at the end of July is:

July sales (a) ………………………..

$700,000

Percent uncollected (b) ……………

60%

Accounts receivable (a) × (b) ……

$420,000

4. The required production for July is computed as follows:

July

Budgeted sales in units ………………

10,000

Add desired ending inventory* …….

2,400

Total needs ……………………………..

12,400

Less beginning inventory** …………

2,000

Required production ………………….

10,400

*August sales of 12,000 units × 20% = 2,400 units.

**July sales of 10,000 units × 20% = 2,000 units.

The Foundational 15 (continued)

5. The raw material purchases for July are computed as follows:

July

Required production in units of finished goods ……………..

10,400

Units of raw materials needed per unit of finished goods ..

5

Units of raw materials needed to meet production …………

52,000

Add desired units of ending raw materials inventory* …….

6,100

Total units of raw materials needed …………………………...

58,100

Less units of beginning raw materials inventory** …………

5,200

Units of raw materials to be purchased ……………………….

52,900

6. The cost of raw material purchases for July is computed as follows:

Units of raw materials to be purchased (a)………

52,900

Unit cost of raw materials (b) ……………………….

$2.00

Cost of raw materials to be purchased (a) × (b) .

$105,800

7. The estimated cash disbursements for materials purchases in July is

computed as follows:

July

June purchases:

$88,880 × 70% ………………….

$62,216

July purchases:

$105,800 × 30% ………………..

31,740

Total cash disbursements ………..

$93,956

8. The accounts payable balance at the end of July is:

July purchases (a) ………………….

$105,800

Percent unpaid (b) …………………

70%

Accounts payable (a) × (b) ………

$74,060

The Foundational 15 (continued)

9. The estimated raw materials inventory balance at the end of July is

computed as follows:

Ending raw materials inventory (pounds) (a) ……

6,100

Cost per pound (b) …………………………………….

$2.00

Raw material inventory balance (a) × (b) ……….

$12,200

10. The estimated direct labor cost for July is computed as follows:

July

Required production in units …………..

10,400

Direct labor hours per unit ……………..

× 2.0

Total direct labor-hours needed (a)…..

20,800

Direct labor cost per hour (b) ………….

$15

Total direct labor cost (a) × (b) ……….

$312,000

11. The estimated unit product cost is computed as follows:

Quantity

Cost

Total

Direct materials …………………..

5 pounds

$2 per pound

$10.00

Direct labor ………………………..

2 hours

$15 per hour

30.00

Manufacturing overhead ……….

2 hours

$10 per hour

20.00

Unit product cost …………………

$60.00

12. The estimated finished goods inventory balance at the end of July is

computed as follows:

Ending finished goods inventory in units (a) …….

2,400

Unit product cost (b) ………………………………….

$60.00

Ending finished goods inventory (a) × (b) ……….

$144,000

The Foundational 15 (continued)

13. The estimated cost of goods sold for July is computed as follows:

Unit sales (a) ……………………………………………

10,000

Unit product cost (b) ………………………………….

$60.00

Estimated cost of goods sold (a) × (b) …………..

$600,000

The estimated gross margin for July is computed as follows:

Total sales (a) …………………………………………..

$700,000

Cost of goods sold (b) ………………………………..

600,000

Estimated gross margin (a) – (b) …………………..

$100,000

14. The estimated selling and administrative expense for July is computed

as follows:

July

Budgeted unit sales ……………………………..

10,000

Variable selling and administrative …………..

expense per unit …………………………..…..

× $1.80

Total variable expense ………………………….

$18,000

Fixed selling and administrative expenses …

60,000

Total selling and administrative expenses …

$78,000

15. The estimated net operating income for July is computed as follows:

Gross margin (a) ……………………………………….

$100,000

Selling and administrative expenses (b) ………….

78,000

Net operating income (a) – (b) ……………………..

$ 22,000

Exercise 7-1 (20 minutes)

1.

April

May

June

Total

February sales:

$230,000 × 10% …….

$ 23,000

$ 23,000

March sales: $260,000

× 70%, 10% ………….

182,000

$ 26,000

208,000

April sales: $300,000 ×

20%, 70%, 10% …….

60,000

210,000

$ 30,000

300,000

May sales: $500,000 ×

20%, 70% …………….

100,000

350,000

450,000

June sales: $200,000 ×

20% …………………….

40,000

40,000

Total cash collections ….

$265,000

$336,000

$420,000

$1,021,000

Notice that even though sales peak in May, cash collections peak in

June. This occurs because the bulk of the company’s customers pay in

the month following sale. The lag in collections that this creates is even

more pronounced in some companies. Indeed, it is not unusual for a

company to have the least cash available in the months when sales are

greatest.

2. Accounts receivable at June 30:

From May sales: $500,000 × 10% ……………………

$ 50,000

From June sales: $200,000 × (70% + 10%) ………

160,000

Total accounts receivable at June 30 …………………

$210,000

Exercise 7-2 (10 minutes)

April

May

June

Quarter

Budgeted unit sales ……………..

50,000

75,000

90,000

215,000

Add desired units of ending

finished goods inventory* ……

7,500

9,000

8,000

8,000

Total needs ………………………..

57,500

84,000

98,000

223,000

Less units of beginning finished

goods inventory ………………..

5,000

7,500

9,000

5,000

Required production in units …..

52,500

76,500

89,000

218,000

*10% of the following month’s sales in units.

Exercise 7-3 (15 minutes)

Quarter—Year 2

First

Second

Third

Fourth

Year

Required production in units of finished

goods ………………………………………………

60,000

90,000

150,000

100,000

400,000

Units of raw materials needed per unit of

finished goods …………………………………..

× 3

× 3

× 3

× 3

× 3

Units of raw materials needed to meet

production ………………………………………..

180,000

270,000

450,000

300,000

1,200,000

Add desired units of ending raw materials

inventory ………………………………………….

54,000

90,000

60,000

42,000

42,000

Total units of raw materials needed ………….

234,000

360,000

510,000

342,000

1,242,000

Less units of beginning raw materials

inventory ………………………………………….

36,000

54,000

90,000

60,000

36,000

Units of raw materials to be purchased ……..

198,000

306,000

420,000

282,000

1,206,000

Unit cost of raw materials ……………………….

× $1.50

× $1.50

× $1.50

× $1.50

× $1.50

Cost of raw materials to purchased …………..

$297,000

$459,000

$630,000

$423,000

$1,809,000

Exercise 7-4 (20 minutes)

1. Assuming that the direct labor workforce is adjusted each quarter, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ……………………….

8,000

6,500

7,000

7,500

29,000

Direct labor time per unit (hours) …………………

× 0.35

× 0.35

× 0.35

× 0.35

× 0.35

Total direct labor-hours needed……………………

2,800

2,275

2,450

2,625

10,150

Direct labor cost per hour …………………………..

× $12.00

× $12.00

× $12.00

× $12.00

× $12.00

Total direct labor cost ………………………………..

$ 33,600

$ 27,300

$ 29,400

$ 31,500

$121,800

2. Assuming that the direct labor workforce is not adjusted each quarter and that overtime wages are

paid, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ………………………

8,000

6,500

7,000

7,500

Direct labor time per unit (hours) ………………..

× 0.35

× 0.35

× 0.35

× 0.35

Total direct labor-hours needed ………………….

2,800

2,275

2,450

2,625

Regular hours paid …………………………..………

2,600

2,600

2,600

2,600

Overtime hours paid …………………………………

200

0

0

25

Wages for regular hours (@ $12.00 per hour) ..

$31,200

$31,200

$31,200

$31,200

$124,800

Overtime wages (@ 1.5 × $12.00 per hour) ….

3,600

0

0

450

4,050

Total direct labor cost ……………………………….

$34,800

$31,200

$31,200

$31,650

$128,850

Exercise 7-5 (15 minutes)

1.

Yuvwell Corporation

Manufacturing Overhead Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted direct labor-hours …………………………..

8,000

8,200

8,500

7,800

32,500

Variable manufacturing overhead rate ……………..

× $3.25

× $3.25

× $3.25

× $3.25

× $3.25

Variable manufacturing overhead ……………………

$26,000

$26,650

$27,625

$25,350

$105,625

Fixed manufacturing overhead ……………………….

48,000

48,000

48,000

48,000

192,000

Total manufacturing overhead ……………………….

74,000

74,650

75,625

73,350

297,625

Less depreciation ………………………………………..

16,000

16,000

16,000

16,000

64,000

Cash disbursements for manufacturing overhead .

$58,000

$58,650

$59,625

$57,350

$233,625

2.

Total budgeted manufacturing overhead for the year (a) …

$297,625

Budgeted direct labor-hours for the year (b) …………………

32,500

Predetermined overhead rate for the year (a) ÷ (b) ……….

$9.16

Exercise 7-6 (15 minutes)

Weller Company

Selling and Administrative Expense Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales …………………………..………..

15,000

16,000

14,000

13,000

58,000

Variable selling and administrative expense per

unit ……………………………………………………….

× $2.50

× $2.50

× $2.50

× $2.50

× $2.50

Variable selling and administrative expense ………

$ 37,500

$ 40,000

$ 35,000

$ 32,500

$145,000

Fixed selling and administrative expenses:

Advertising………………………………………………

8,000

8,000

8,000

8,000

32,000

Executive salaries ……………………………………..

35,000

35,000

35,000

35,000

140,000

Insurance ……………………………………………….

5,000

5,000

10,000

Property taxes ………………………………………….

8,000

8,000

Depreciation ……………………………………………

20,000

20,000

20,000

20,000

80,000

Total fixed selling and administrative expenses ….

68,000

71,000

68,000

63,000

270,000

Total selling and administrative expenses …………

105,500

111,000

103,000

95,500

415,000

Less depreciation ………………………………………..

20,000

20,000

20,000

20,000

80,000

Cash disbursements for selling and

administrative expenses ……………………………..

$ 85,500

$ 91,000

$ 83,000

$ 75,500

$335,000

Exercise 7-7 (15 minutes)

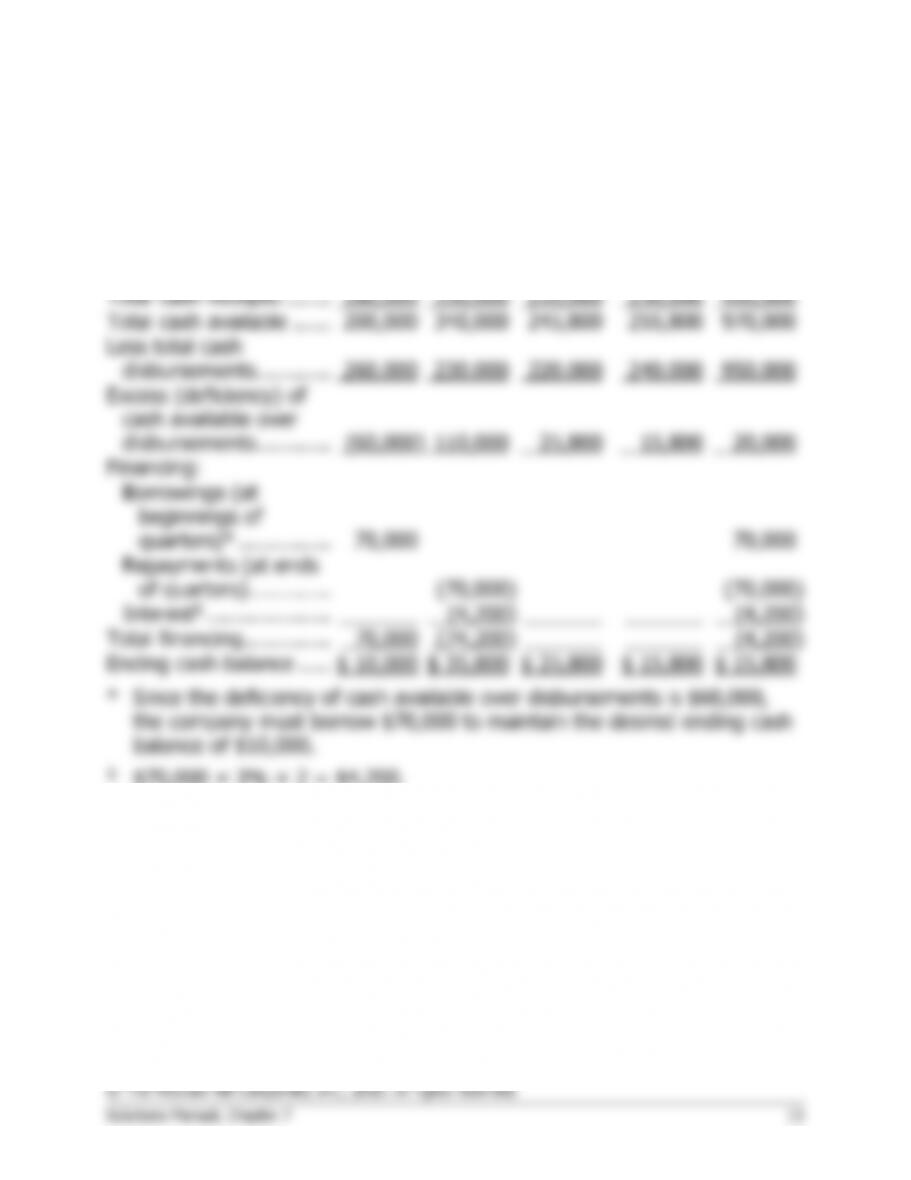

Garden Depot

Cash Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Beginning cash balance .

$ 20,000

$ 10,000

$ 35,800

$ 25,800

$ 20,000

Total cash receipts ……..

180,000

330,000

210,000

230,000

950,000

Total cash available ……

200,000

340,000

245,800

255,800

970,000

Less total cash

disbursements …………

260,000

230,000

220,000

240,000

950,000

Excess (deficiency) of

cash available over

disbursements …………

(60,000)

110,000

25,800

15,800

20,000

Financing:

Borrowings (at

beginnings of

quarters)* ……………

70,000

70,000

Repayments (at ends

of quarters) ………….

(70,000)

(70,000)

Interest§ ………………..

(4,200)

(4,200)

Total financing …………..

70,000

(74,200)

(4,200)

Ending cash balance …..

$ 10,000

$ 35,800

$ 25,800

$ 15,800

$ 15,800

* Since the deficiency of cash available over disbursements is $60,000,

the company must borrow $70,000 to maintain the desired ending cash

balance of $10,000.

§ $70,000 × 3% × 2 = $4,200.

Exercise 7-8 (10 minutes)

Gig Harbor Boating

Budgeted Income Statement

Sales (460 units × $1,950 per unit) ………………….

$897,000

Cost of goods sold (460 units × $1,575 per unit) …

724,500

Gross margin ……………………………………………….

172,500

Selling and administrative expenses* ………………..

139,500

Net operating income …………………………………….

33,000

Interest expense …………………………………………..

14,000

Net income ………………………………………………….

$ 19,000

*(460 units × $75 per unit) + $105,000 = $139,500.

Exercise 7-9 (15 minutes)

Mecca Copy

Budgeted Balance Sheet

Assets

Current assets:

Cash* …………………………………………

$12,200

Accounts receivable ……………………….

8,100

Supplies inventory …………………………

3,200

Total current assets …………………………

$23,500

Plant and equipment:

Equipment …………………………………..

34,000

Accumulated depreciation ……………….

(16,000)

Plant and equipment, net ………………….

18,000

Total assets …………………………..……….

$41,500

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable ………………………….

$ 1,800

Stockholders’ equity:

Common stock ……………………………..

$ 5,000

Retained earnings# ……………………….

34,700

Total stockholders’ equity ………………….

39,700

Total liabilities and stockholders’ equity ..

$41,500

*Plug figure.

#

Retained earnings, beginning balance ..

$28,000

Add net income …………………………….

11,500

39,500

Deduct dividends …………………………..

4,800

Retained earnings, ending balance ……

$34,700

Exercise 7-10 (45 minutes)

1. Production budget:

July

August

Septem-

ber

October

Budgeted unit sales ……………

35,000

40,000

50,000

30,000

Add desired units of ending

finished goods inventory …..

11,000

13,000

9,000

7,000

Total needs ………………………

46,000

53,000

59,000

37,000

Less units of beginning

finished goods inventory ….

10,000

11,000

13,000

9,000

Required production in units ..

36,000

42,000

46,000

28,000

2. During July and August the company is building inventories in

anticipation of peak sales in September. Therefore, production exceeds

Exercise 7-10 (continued)

3. Direct materials budget:

July

August

Septem-

ber

Third

Quarter

Required production in units of finished goods …….

36,000

42,000

46,000

124,000

Units of raw materials needed per unit of finished

goods ………………………………………………………

× 3 cc

× 3 cc

× 3 cc

× 3 cc

Units of raw materials needed to meet production ..

108,000

126,000

138,000

372,000

Add desired units of ending raw materials

inventory …………………………………………………..

63,000

69,000

42,000

*

42,000

Total units of raw materials needed …………………..

171,000

195,000

180,000

414,000

Less units of beginning raw materials inventory …..

54,000

63,000

69,000

54,000

Units of raw materials to be purchased ………………

117,000

132,000

111,000

360,000

* 28,000 units (October production) × 3 cc per unit = 84,000 cc;

84,000 cc × 1/2 = 42,000 cc.

As shown in part (1), production is greatest in September; however, as shown in the raw material

purchases budget, purchases of materials are greatest a month earlier—in August. The reason for the

large purchases of materials in August is that the materials must be on hand to support the heavy

production scheduled for September.

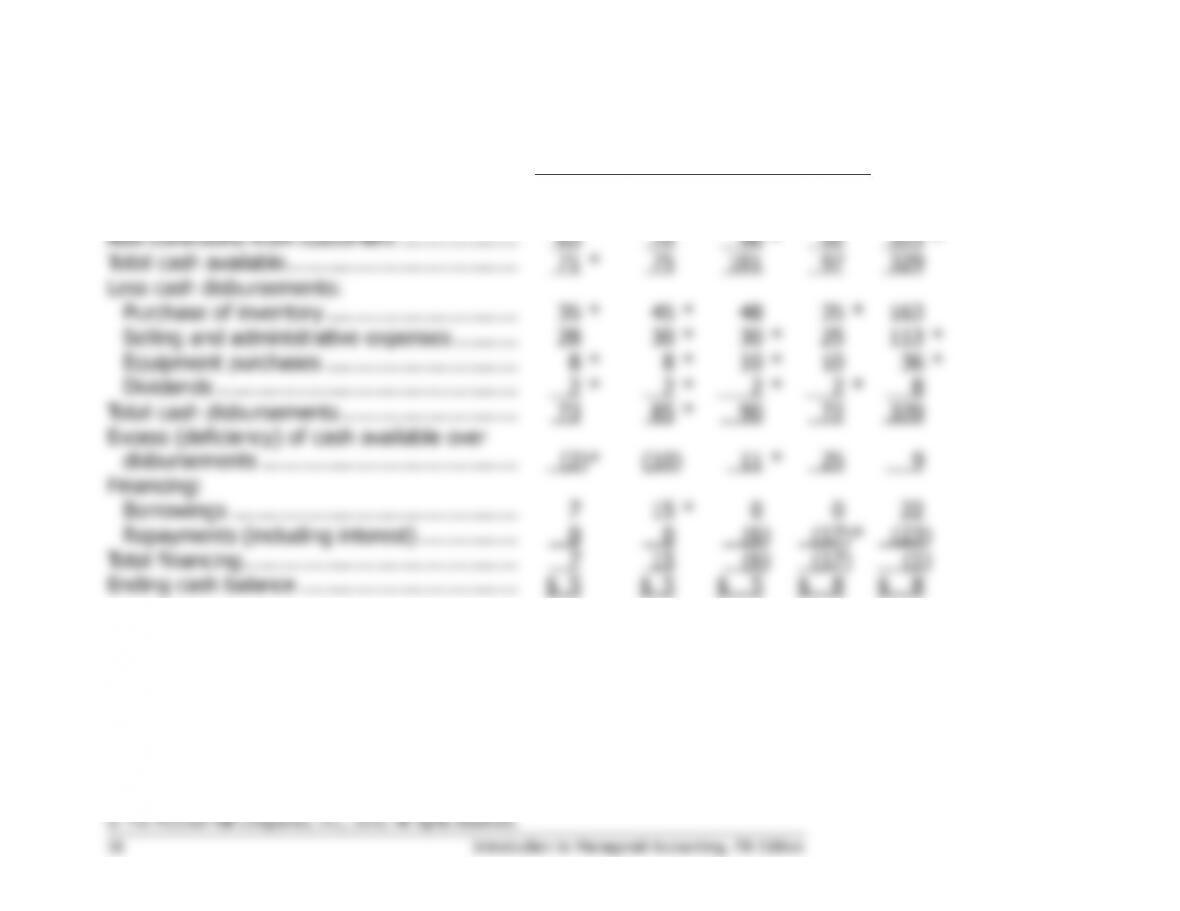

Exercise 7-11 (20 minutes)

Quarter (000 omitted)

1

2

3

4

Year

Beginning cash balance ………………………….

$ 6

*

$ 5

$ 5

$ 5

$ 6

Add collections from customers ……………….

65

70

96

*

92

323

*

Total cash available ……………………………….

71

*

75

101

97

329

Less cash disbursements:

Purchase of inventory ………………………….

35

*

45

*

48

35

*

163

Selling and administrative expenses ……….

28

30

*

30

*

25

113

*

Equipment purchases ………………………….

8

*

8

*

10

*

10

36

*

Dividends …………………………………………

2

*

2

*

2

*

2

*

8

Total cash disbursements ……………………….

73

85

*

90

72

320

Excess (deficiency) of cash available over

disbursements …………………………………..

(2)

*

(10)

11

*

25

9

Financing:

Borrowings ……………………………………….

7

15

*

0

0

22

Repayments (including interest) …………….

0

0

(6)

(17)

*

(23)

Total financing ……………………………………..

7

15

(6)

(17)

(1)

Ending cash balance ……………………………..

$ 5

$ 5

$ 5

$ 8

$ 8

* Given.

Exercise 7-12 (30 minutes)

1. Schedule of expected cash collections:

Month

July

August

Sept.

Quarter

From accounts receivable .

$136,000

$136,000

From July sales:

35% × 210,000 …………

73,500

73,500

65% × 210,000 …………

$136,500

136,500

From August sales:

35% × 230,000 …………

80,500

80,500

65% × 230,000 …………

$149,500

149,500

From September sales:

35% × 220,000 …………

77,000

77,000

Total cash collections …….

$209,500

$217,000

$226,500

$653,000

2. a. Merchandise purchases budget:

July

August

Sept.

Total

Budgeted cost of goods sold

(60% of sales)………………….

$126,000

$138,000

$132,000

$396,000

Add desired ending

merchandise inventory* ……..

41,400

39,600

43,200

43,200

Total needs ………………………..

167,400

177,600

175,200

439,200

Less beginning merchandise

inventory …………………………

62,000

41,400

39,600

62,000

Required purchases ……………..

$105,400

$136,200

$135,600

$377,200

July

August

Sept.

Total

From accounts payable ……….

$ 71,100

$ 71,100

For July purchases ……………..

42,160

$ 63,240

105,400

For August purchases …………

54,480

$ 81,720

136,200

For September purchases ……

54,240

54,240

Total cash disbursements …….

$113,260

$117,720

$135,960

$366,940

Exercise 7-12 (continued)

3.

Beech Corporation

Income Statement

For the Quarter Ended September 30

Sales ($210,000 + $230,000 + $220,000) ..

$660,000

Cost of goods sold (Part 2a) …………………

396,000

Gross margin ……………………………………..

264,000

Selling and administrative expenses

($60,000 × 3 months) ………………………

180,000

Net operating income…………………………..

84,000

Interest expense ………………………………..

0

Net income ……………………………………….

$ 84,000

4.

Beech Corporation

Balance Sheet

September 30

Assets

Cash ($90,000 + $653,000 – $366,940 – ($55,000 ×

3)) ……………………………………………………………

$211,060

Accounts receivable ($220,000 × 65%) …………………

143,000

Inventory (Part 2a) ……………………………………………

43,200

Plant and equipment, net ($210,000 – ($5,000 ×3)) …

195,000

Total assets …………………………..…………………………

$592,260

Accounts payable ($135,600 × 60%) …………………….

Common stock (Given) ………………………………………

Retained earnings ($99,900 + $84,000) …………………

Total liabilities and stockholders’ equity ………………….

$592,260