Problem 12-13A (continued)

The decrease in the long-term investments account ($20,000) equals

the cost of the long-term investment sold; therefore, Rusco did not

purchase any long-term investments during the year. The proceeds from

the sale of the long-term investment ($30,000) should be recorded as a

Problem 12-13A (continued)

Rusco Company

Statement of Cash Flows

For the Year Ended July 31, 2015

Operating activities:

Net income ………………………………………………

$ 30,000

Adjustments to convert net income to cash basis:

Depreciation …………………………………………..

$ 20,000

Increase in accounts receivable ………………….

(40,000)

Increase in inventory ……………………………….

(50,000)

Decrease in prepaid expenses ……………………

4,000

Increase in accounts payable ……………………..

63,000

Decrease in accrued liabilities …………………….

(9,000)

Increase in income taxes payable ……………….

8,000

Loss on sale of equipment …………………………

2,000

Gain on sale of investments……………………….

(10,000)

(12,000)

Net cash provided by operating activities ………..

18,000

Investing activities:

Proceeds from sale of long-term investments …..

30,000

Proceeds from sale of equipment ………………….

8,000

Additions to plant and equipment ………………….

(150,000)

Net cash used in investing activities ………………

(112,000)

Financing activities:

Issuance of bonds payable …………………………..

70,000

Issuance of common stock …………………………..

20,000

Cash dividends ………………………………………….

(9,000)

Net cash provided by financing activities …………

81,000

Net decrease in cash ………………………………….

(13,000)

Beginning cash and cash equivalents ……………..

21,000

Ending cash and cash equivalents …………………

$ 8,000

Problem 12-13A (continued)

3. Free cash flow computation:

Net cash provided by operating activities ……………..

$ 18,000

Capital expenditures ……………………………………..

$150,000

Dividends ……………………………………………………

9,000

159,000

Free cash flow ………………………………………………..

$(141,000)

4. Although the company reported $30,000 of net income for the year, a

smaller amount of cash was provided by operating activities ($18,000)

due to increases in accounts receivable and inventory. The cash

Problem 12-14A (45 minutes)

1. Prepare a statement of cash flows.

Operating activities:

Step 1: The following equation can be applied to the Accumulated

Depreciation account to compute the depreciation to add back to net

income:

Beginning balance – Debits + Credits = Ending balance

income.

Problem 12-14A (continued)

The net cash provided by operating activities can now be calculated as

follows:

Net income …………………………..…………..

$170,000

Adjustments to convert net income to cash basis:

Depreciation ……………………………………

$ 95,000

Increase in accounts receivable …………..

(180,000)

Decrease in inventory ……………………….

12,000

Increase in prepaid expenses ……………..

(5,000)

Increase in accounts payable ………………

300,000

Decrease in accrued liabilities ……………..

(17,000)

Increase in income taxes payable ………..

15,000

Loss on sale of equipment ………………….

20,000

Gain on sale of investments ………………..

(60,000)

180,000

Net cash provided by operating activities …

$350,000

Investing and Financing activities:

The guidelines from Exhibit 12-3 can be used to analyze the changes in

noncash balance sheet accounts that impact investing and financing

cash flows as follows:

Increase in

Account

Balance

Decrease in

Account

Balance

Noncurrent Assets

Property, plant, and equipment ……………

– 570,000

Long-term investments ………………………

+ 50,000

Long-term loans to subsidiaries ……………

– 44,000

Liabilities and Stockholders’ Equity

Bonds payable …………………………………

+ 220,000

Common stock …………………………………

+ 90,000

Problem 12-14A (continued)

Lomax’s subsidiaries did not repay any loans during the year, therefore,

the amount in the table on the prior page (– 44,000) represents a cash

outflow pertaining to a new loan. The company did not repurchase any

of its own stock, so the amount on the prior page represents a $90,000

Problem 12-14A (continued)

Lomax Company

Statement of Cash Flows

Operating activities:

Net income …………………………………………………

$170,000

Adjustments to convert net income to cash basis:

Depreciation ……………………………………………..

$ 95,000

Increase in accounts receivable …………………….

(180,000)

Decrease in inventory …………………………..……..

12,000

Increase in prepaid expenses ………………………..

(5,000)

Increase in accounts payable ………………………..

300,000

Decrease in accrued liabilities ……………………….

(17,000)

Increase in income taxes payable …………………..

15,000

Loss on sale of equipment …………………………...

20,000

Gain on sale of investments ………………………….

(60,000)

180,000

Net cash provided by operating activities …………..

350,000

Investing activities:

Proceeds from sale of long-term investments ……

110,000

Proceeds from sale of equipment ……………………

70,000

Loans to subsidiaries …………………………………..

(44,000)

Additions to plant and equipment …………………..

(700,000)

Net cash used in investing activities ………………..

(564,000)

Financing activities:

Issuance of bonds payable …………………………...

570,000

Issuance of common stock …………………………...

90,000

Retirement of bonds payable …………………………

(350,000)

Cash dividends to stockholders ………………………

(75,000)

Net cash provided by financing activities ………….

235,000

Net increase in cash and cash equivalents ………..

21,000

Beginning cash and cash equivalents ………………

40,000

Ending cash and cash equivalents…………………..

$ 61,000

Problem 12-14A (continued)

2. The large amount of cash provided by operating activities is traceable

for the most part to the $300,000 increase in accounts payable. If the

accounts payable had remained basically unchanged, the same as

inventory, then operating activities would have provided very little cash

and the company might have experienced serious cash problems.

Appendix 12A

The Direct Method of Determining the Net Cash

Provided by Operating Activities

Exercise 12A-1 (15 minutes)

Sales ………………………………………………….

$700

Adjustments to a cash basis:

Increase in accounts receivable …………..

– 110

$590

Cost of goods sold ………………………………..

400

Adjustments to a cash basis:

Decrease in inventory ……………………….

– 70

Increase in accounts payable ………………

– 35

295

Selling and administrative expenses ………….

184

Adjustments to a cash basis:

Increase in prepaid expenses ……………..

+ 9

Decrease in accrued liabilities ……………..

+ 4

Depreciation charges ………………………..

– 60

137

Income tax expense ………………………………

36

Adjustments to a cash basis:

Increase in income taxes payable ………..

– 8

28

Net cash provided by operating activities ……

$130

Note that the $130 “net cash provided” figure agrees with the indirect

method presented in Exercise 12-4.

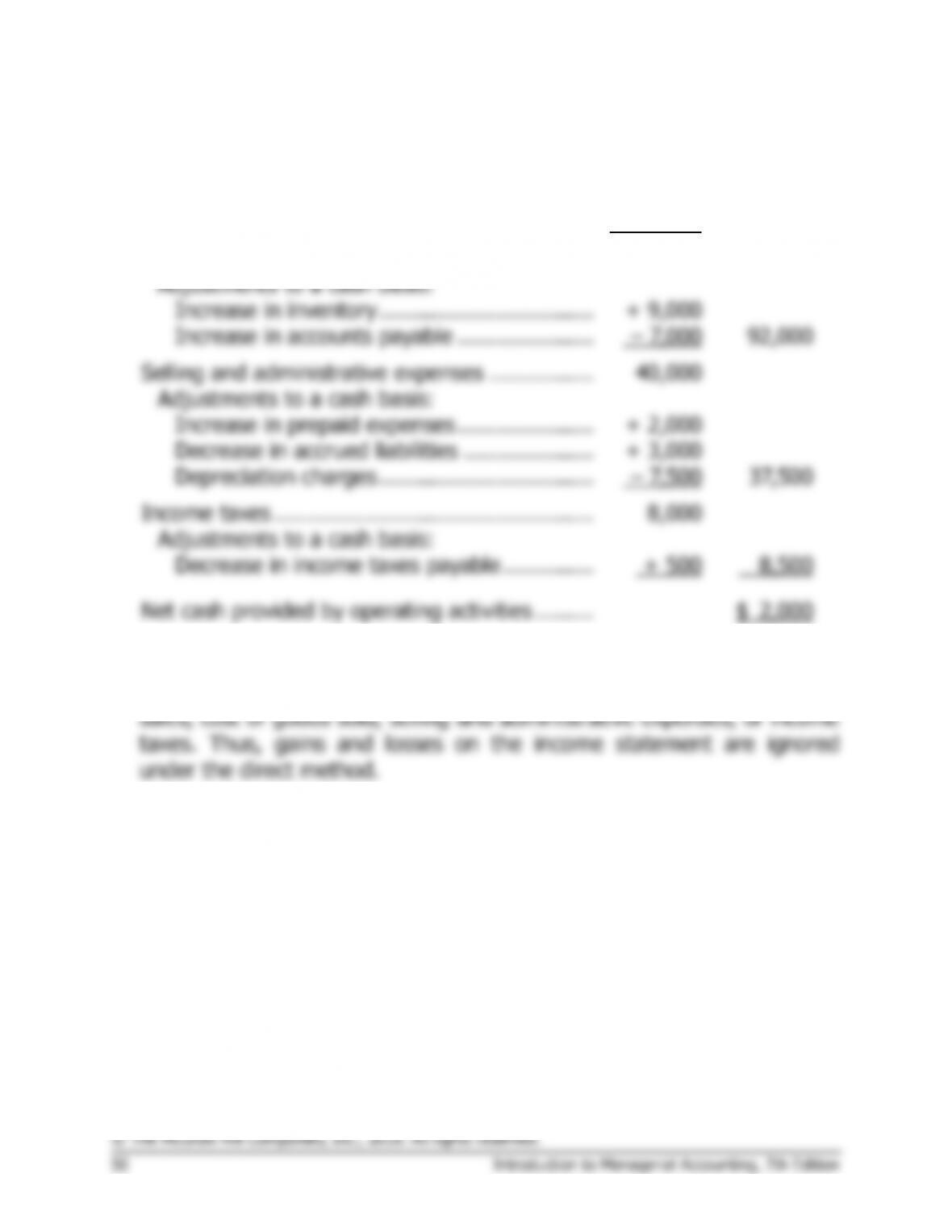

Exercise 12A-2 (15 minutes)

1.

Sales …………………………………………………….

$150,000

Adjustments to a cash basis:

Increase in accounts receivable ………………

– 10,000

$140,000

Cost of goods sold ……………………………………

90,000

Adjustments to a cash basis:

Increase in inventory …………………………...

+ 9,000

Increase in accounts payable …………………

– 7,000

92,000

Selling and administrative expenses …………….

40,000

Adjustments to a cash basis:

Increase in prepaid expenses …………………

+ 2,000

Decrease in accrued liabilities ………………..

+ 3,000

Depreciation charges …………………………...

– 7,500

37,500

Income taxes ………………………………………….

8,000

Adjustments to a cash basis:

Decrease in income taxes payable …………..

+ 500

8,500

Net cash provided by operating activities ………

$ 2,000

2. Gains and losses on the sale of assets would have no effect on the

computations in part (1). The reason is that these items are not part of

Exercise 12A-3 (15 minutes)

Sales …………………………………………………

$275

Adjustments to a cash basis:

Decrease in accounts receivable …………

+ 2

$277

Cost of goods sold ……………………………….

150

Adjustments to a cash basis:

Increase in inventory ……………………….

+ 10

Increase in accounts payable ……………..

– 4

156

Selling and administrative expenses …………

90

Adjustments to a cash basis:

Depreciation charges ……………………….

– 15

75

Net cash provided by operating activities …..

$ 46

Exercise 12A-4 (15 minutes)

Sales …………………………………………………….

$ 350,000

Adjustments to a cash basis:

Less increase in accounts receivable ……….

– 19,000

$331,000

Cost of goods sold …………………………………..

140,000

Adjustments to a cash basis:

Plus increase in inventory ……………………..

+ 33,000

Less increase in accounts payable …………..

– 15,000

158,000

Selling and administrative expenses …………….

160,000

Adjustments to a cash basis:

Less decrease in prepaid expenses …………

– 1,000

Plus decrease in accrued liabilities ………….

+ 2,000

Less depreciation charges …………………….

– 20,000

141,000

Income taxes ………………………………………….

15,000

Adjustments to a cash basis:

Less increase in income taxes payable …….

– 4,000

11,000

Net cash provided by operating activities ………

$ 21,000

Problem 12A-5A (45 minutes)

1.

The income statement adjusted to a cash basis:

Sales …………………………………………………

$500,000

Adjustments to a cash basis:

Increase in accounts receivable …………..

– 40,000

$460,000

Cost of goods sold ………………………………..

300,000

Adjustments to a cash basis:

Increase in inventory ………………………..

+ 50,000

Increase in accounts payable ……………..

– 63,000

287,000

Selling and administrative expenses ………….

158,000

Adjustments to a cash basis:

Decrease in prepaid expenses …………….

– 4,000

Decrease in accrued liabilities ……………..

+ 9,000

Depreciation charges ………………………..

– 20,000

143,000

Income taxes ………………………………………

20,000

Adjustments to a cash basis:

Increase in income taxes payable ………..

– 8,000

12,000

Net cash provided by operating activities …..

$ 18,000

Problem 12A-5A (continued)

2.

Rusco Company

Statement of Cash Flows

For the Year Ended July 31, 2015

Operating activities:

Cash received from customers …………………….

$460,000

Less cash disbursements for:

Cost of merchandise purchased …………………

$287,000

Selling and administrative expenses ……………

143,000

Income taxes ………………………………………..

12,000

Total cash disbursements …………………………...

442,000

Net cash provided by operating activities ……….

18,000

Investing activities:

Proceeds from sale of investments ……………….

30,000

Proceeds from sale of equipment …………………

8,000

Additions to plant and equipment …………………

(150,000)

Net cash used for investing activities …………….

(112,000)

Financing activities:

Increase in bonds payable ………………………….

70,000

Increase in common stock ………………………….

20,000

Cash dividends …………………………………………

(9,000)

Net cash provided by financing activities ………..

81,000

Net decrease in cash …………………………………

(13,000)

Beginning cash and cash equivalents …………….

21,000

Ending cash and cash equivalents ………………..

$ 8,000

Problem 12A-5A (continued)

3. There are two reasons for the sharp decline in cash. First, note that a

relatively small amount of cash was provided by operations during the

year. This is due to a build-up in accounts receivable and inventory,

Problem 12A-6A (30 minutes)

1.

Sales …………………………………………………………..

$800

Adjustments to a cash basis:

Increase in accounts receivable …………………….

– 100

$700

Cost of goods sold ………………………………………….

500

Adjustments to a cash basis:

Decrease in inventory …………………………………

– 50

Increase in accounts payable ……………………….

– 80

370

Selling and administrative expenses …………………..

213

Adjustments to a cash basis:

Increase in prepaid expenses ……………………….

+ 4

Decrease in accrued liabilities ………………………

+ 12

Depreciation charges ………………………………….

– 24

205

Income taxes ………………………………………………..

27

Adjustments to a cash basis:

Increase in income taxes payable ………………….

– 6

21

Net cash provided by operating activities …………….

$104

Problem 12A-6A (continued)

2.

Weaver Company

Statement of Cash Flows

For the Year Ended December 31, 2015

Operating activities:

Cash received from customers ……………………………..

$700

Less cash disbursements for:

Cost of merchandise purchased ………………………….

$370

Selling and administrative expenses …………………….

205

Income taxes …………………………………………………

21

Total cash disbursements …………………………………….

596

Net cash provided by operating activities ………………..

104

Investing activities:

Proceeds from sale of long-term investments …………..

10

Proceeds from sale of equipment ………………………….

20

Additions to plant and equipment ………………………….

(180)

Net cash used for investing activities ……………………..

(150)

Financing activities:

Increase in bonds payable …………………………………..

110

Decrease in common stock ………………………………….

(40)

Cash dividends ………………………………………………….

(30)

Net cash provided by financing activities …………………

40

Net decrease in cash ………………………………………….

(6)

Beginning cash and cash equivalents ……………………..

15

Ending cash and cash equivalents …………………………

$ 9

Problem 12A-7A (45 minutes)

1.

Sales …………………………………………………….

$900,000

Adjustments to a cash basis:

Increase in accounts receivable ………………

– 80,000

$820,000

Cost of goods sold ……………………………………

500,000

Adjustments to a cash basis:

Increase in inventory …………………………...

+ 50,000

Increase in accounts payable …………………

– 60,000

490,000

Selling and administrative expenses …………….

328,000

Adjustments to a cash basis:

Decrease in prepaid expenses ………………..

– 7,000

Decrease in accrued liabilities ………………..

+ 10,000

Depreciation charges …………………………...

– 42,000

289,000

Income taxes ………………………………………….

24,000

Adjustments to a cash basis:

Increase in income taxes payable ……………

– 3,000

21,000

Net cash provided by operating activities ………

$ 20,000

Problem 12A-7A (continued)

2.

Joyner Company

Statement of Cash Flows

For Year 2

Operating activities:

Cash received from customers ……………………..

$820,000

Less cash disbursements for:

Cost of merchandise purchased ………………….

$490,000

Selling and administrative expenses …………….

289,000

Income taxes …………………………………………

21,000

Total cash disbursements …………………………….

800,000

Net cash provided by operating activities ………..

20,000

Investing activities:

Proceeds from sale of equipment ………………….

18,000

Loan to Hymans Company …………………………..

(40,000)

Additions to plant and equipment ………………….

(150,000)

Net cash used for investing activities ……………..

(172,000)

Financing activities:

Increase in bonds payable …………………………..

120,000

Increase in common stock …………………………..

30,000

Cash dividends ………………………………………….

(15,000)

Net cash provided by financing activities …………

135,000

Net decrease in cash ………………………………….

(17,000)

Beginning cash and cash equivalents ……………..

21,000

Ending cash and cash equivalents …………………

$ 4,000

3. The decline in cash is explainable largely by the company’s inability to

generate a significant amount of cash from operating activities. Note

that the company generated only $20,000 from operating activities,