2-12 Introduction to Managerial Accounting, 6th edition

Problem 2-25B (continued)

Rent Expense

Cost of Goods Sold

(h)

17,000

(l)

530,000

Sales

(l)

1,100,000

3.

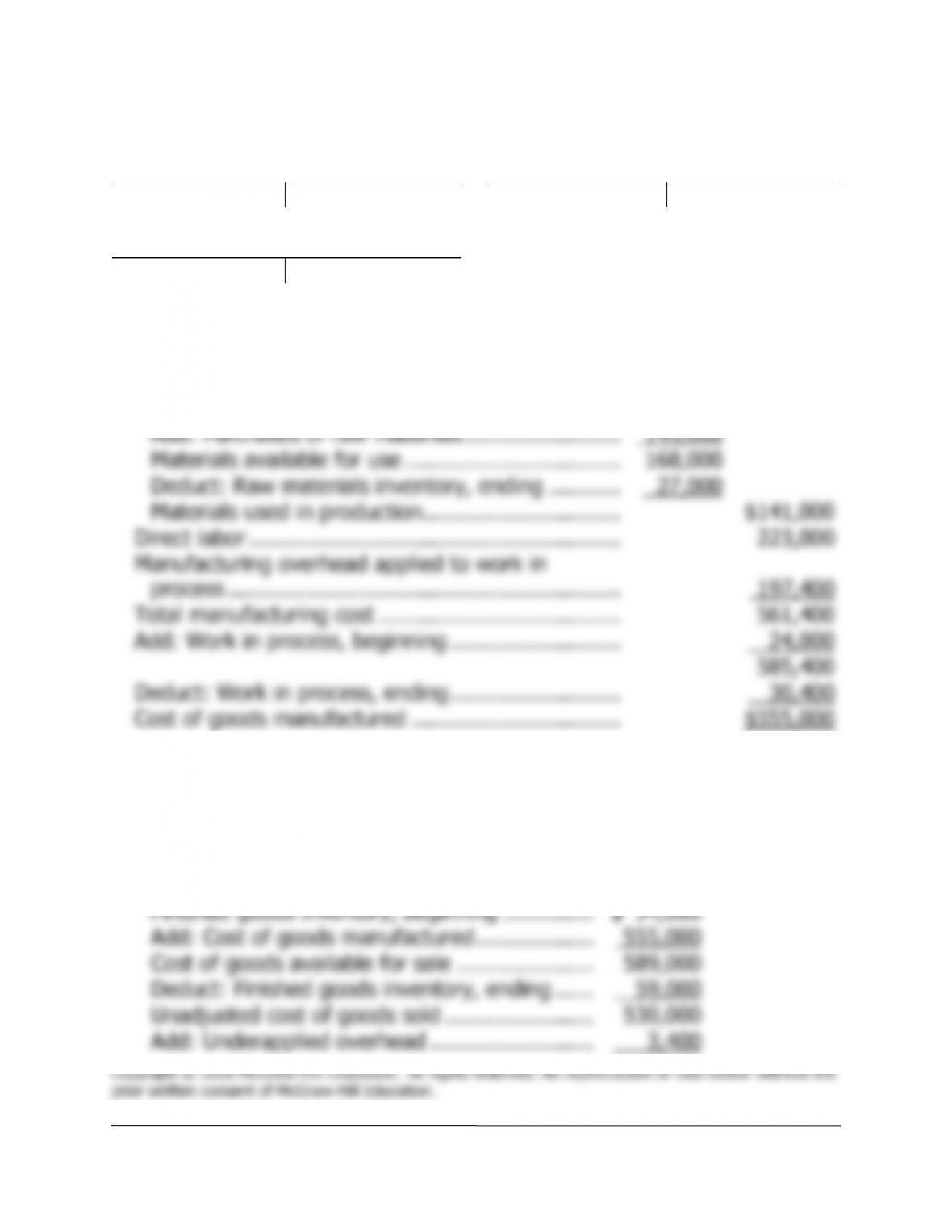

Mariya Company

Schedule of Cost of Goods Manufactured

Direct materials:

Raw materials inventory, beginning ……………….

$ 23,000

Add: Purchases of raw materials ……………………

145,000

Materials available for use …………………………...

168,000

Deduct: Raw materials inventory, ending ………..

27,000

Materials used in production …………………………

$141,000

Direct labor …………………………………………………

223,000

Manufacturing overhead applied to work in

process ……………………………………………………

197,400

Total manufacturing cost ……………………………….

561,400

Add: Work in process, beginning ……………………..

24,000

585,400

Deduct: Work in process, ending ……………………..

30,400

Cost of goods manufactured …………………………..

$555,000

4.

Cost of Goods Sold ……………………………………

3,400

Manufacturing Overhead………………………..

3,400

Schedule of cost of goods sold:

Finished goods inventory, beginning …………..

$ 34,000

Add: Cost of goods manufactured ………………

555,000

Cost of goods available for sale …………………

589,000

Deduct: Finished goods inventory, ending ……

59,000

Unadjusted cost of goods sold …………………..

530,000

Add: Underapplied overhead …………………….

3,400

Adjusted cost of goods sold ………………………

$533,400

2-14 Introduction to Managerial Accounting, 6th edition

Problem 2-25B (continued)

5.

Mariya Company

Income Statement

Sales ………………………………………………….

$1,100,000

Cost of goods sold …………………………………

533,400

Gross margin ……………………………………….

566,600

Selling and administrative expenses:

Salaries expense …………………………………

$143,000

Advertising expense …………………………….

128,000

Depreciation expense …………………………..

12,900

Rent expense …………………………………….

17,000

Miscellaneous expense …………………………

11,000

311,900

Net operating income …………………………….

$ 254,700

6.

Direct materials …………………………………………………….

$ 3,900

Direct labor (400 hours × $14 per hour) …………………….

5,600

Manufacturing overhead cost applied (140% × $3,900) …

5,460

Total manufacturing cost ………………………………………..

14,960

Add markup (65% × $14,960) …………………………………

9,724

Total billed price of Job 521 …………………………………….

$24,684

Problem 2-26B (30 minutes)

1. Preparation Department:

The estimated total manufacturing overhead cost in the Preparation

Estimated fixed manufacturing overhead ………………

$207,500

Estimated variable manufacturing overhead:

$3.00 per MH × 83,000 MHs …………………………...

249,000

Estimated total manufacturing overhead cost …………

$456,500

The predetermined overhead rate is computed as follows:

Estimated total manufacturing overhead ……

$456,500

÷ Estimated total machine-hours …………….

83,000

MHs

= Predetermined overhead rate ………………

$5.50

per MH

Estimated fixed manufacturing overhead ………………

$518,700

Estimated variable manufacturing overhead:

$5.00 per DLH × 57,000 DLHs ………………………….

285,000

Estimated total manufacturing overhead cost …………

$803,700

Estimated total manufacturing overhead ……

÷ Estimated total machine-hours …………….

DLHs

= Predetermined overhead rate ………………

per DLH

units

per unit

Preparation

Manufacturing overhead cost incurred …..

Manufacturing overhead cost applied:

Underapplied (or overapplied) overhead ..

$(35,900)

Problem 2-26B (continued)

2.

Preparation Department overhead applied:

360 machine-hours × $5.50 per machine-hour …..

$1,980

Fabrication Department overhead applied:

133 direct labor-hours × $14.10 per labor-hour ….

1,875

Total overhead cost ………………………………………..

$3,855

3. Total cost of Job 135:

Preparation

Fabrication

Total

Direct materials …………….

$ 940

$1,120

$2,060

Direct labor ………………….

690

970

1,660

Manufacturing overhead …

1,980

1,875

3,855

Total cost ……………………

$3,610

$3,965

$7,575

Problem 2-27B (45 minutes)

1.

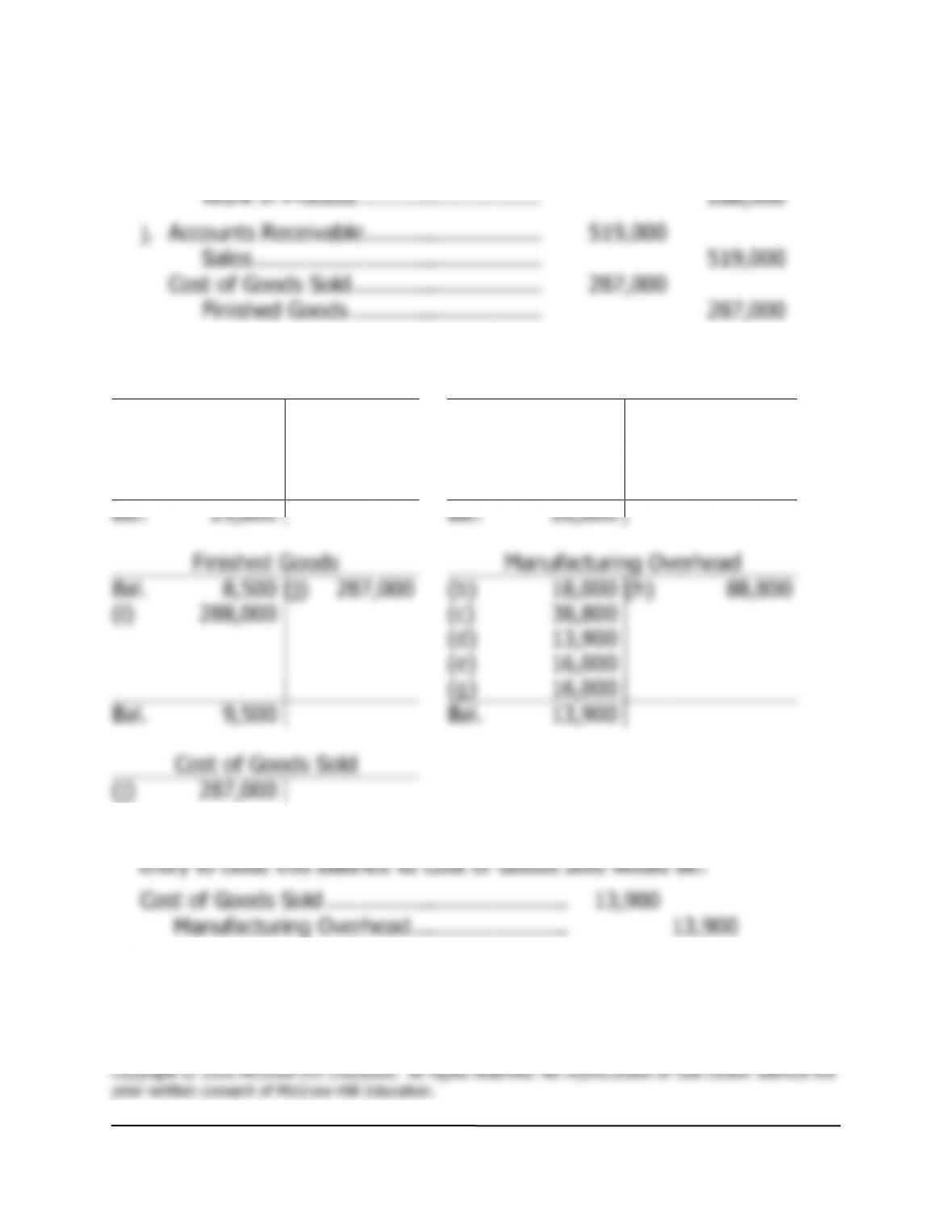

a.

Raw Materials ………………………………….

164,000

Accounts Payable …………………………

164,000

b.

Work in Process …………………………..…..

127,000

Manufacturing Overhead ……………………

18,000

Raw Materials ……………………………..

145,000

c.

Work in Process …………………………..…..

94,000

Manufacturing Overhead ……………………

38,800

Sales Commissions Expense ……………….

25,000

Salaries Expense ………………………………

44,000

Salaries and Wages Payable …………..

201,800

d.

Manufacturing Overhead ……………………

13,900

Insurance Expense…………………………...

4,600

Prepaid Insurance ………………………..

18,500

e.

Manufacturing Overhead ……………………

16,000

Accounts Payable …………………………

16,000

f.

Advertising Expense ………………………….

11,000

Accounts Payable …………………………

11,000

g.

Manufacturing Overhead ……………………

16,000

Depreciation Expense ………………………..

4,000

Accumulated Depreciation ……………..

20,000

h.

Work in Process …………………………..…..

88,800

Manufacturing Overhead ……………….

88,800

Predetermined

overhead rate

=

Estimated total manufacturing overhead cost

Estimated amount of the allocation base

Predetermined

overhead rate

=

$108,000

=

$2.40 per MH

45,000 MHs

37,000 actual MHs × $2.40 per MH= $88,800 applied.

Bal.

(j)

287,000

(b)

(h)

(i)

288,000

(c)

38,800

(d)

13,900

(e)

(g)

Bal.

Bal.

13,900

(j)

287,000

Cost of Goods Sold ……………………………….

Manufacturing Overhead ……………………

Problem 2-27B (continued)

i.

Finished Goods …………………………….

288,000

Work in Process ……………………….

288,000

j.

Accounts Receivable ………………………

519,000

Sales ……………………………………..

519,000

Cost of Goods Sold ………………………..

287,000

Finished Goods ………………………..

287,000

2.

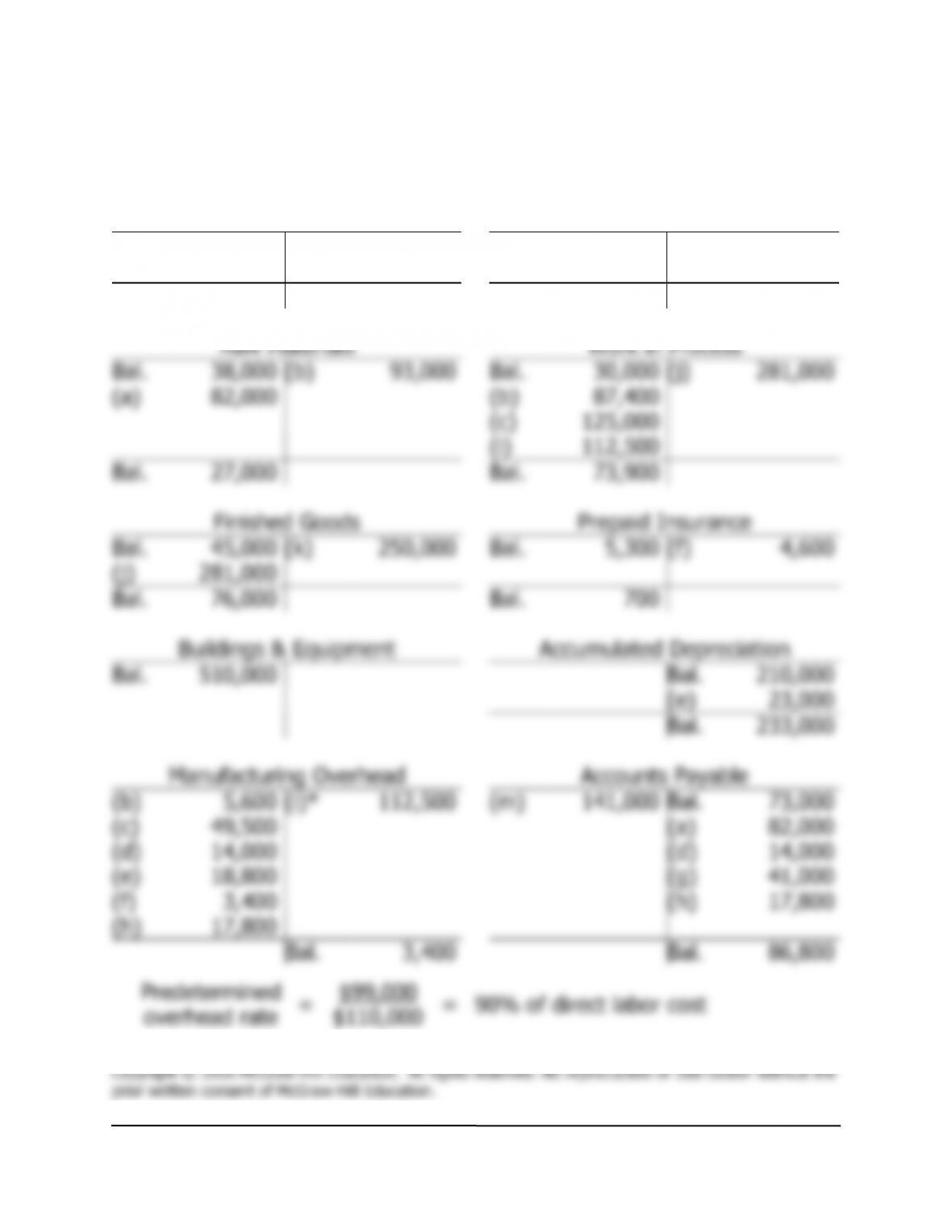

Raw Materials

Work in Process

Bal.

10,800

(b)

145,000

Bal.

4,800

(i)

288,000

(a)

164,000

(b)

127,000

(c)

94,000

(h)

88,800

Bal.

29,800

Bal.

26,600

Problem 2-27B (continued)

4.

Carpenter Cornices, Ltd.

Income Statement

For the Year Ended June 30

Sales ……………………………………………………..

$519,000

Cost of goods sold ($287,000 + $13,900) ………

300,900

Gross margin ……………………………………………

218,100

Selling and administrative expenses:

Sales commissions ………………………………….

$25,000

Administrative salaries ……………………………..

44,000

Insurance expense ………………………………….

4,600

Advertising expenses……………………………….

11,000

Depreciation expense ………………………………

4,000

88,600

Net operating income ………………………………..

$129,500

Bal.

(k)

250,000

Bal.

(f)

(j)

Bal.

76,000

Bal.

Bal.

510,000

Bal.

(e)

Bal.

233,000

(b)

(i)*

112,500

(m)

141,000

Bal.

(c)

(a)

82,000

(d)

(d)

14,000

(e)

(g)

(f)

(h)

(h)

17,800

Bal.

Bal.

86,800

Problem 2-28B (60 minutes)

1. and 2.

Cash

Accounts Receivable

Bal.

13,000

(c)

245,500

Bal.

45,000

(l)

415,000

(l)

415,000

(m)

141,000

(k)

530,000

Bal.

41,500

Bal.

160,000

Raw Materials

Work in Process

Bal.

38,000

(b)

93,000

Bal.

30,000

(j)

281,000

(a)

82,000

(b)

87,400

(c)

125,000

(i)

112,500

Bal.

27,000

Bal.

73,900

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the

prior written consent of McGraw-Hill Education.

Solutions Manual, Problems Set B 2-21

$125,000 actual direct labor cost × 0.90 = $112,500 applied.

2-22 Introduction to Managerial Accounting, 6th edition

Problem 2-28B (continued)

Retained Earnings

Capital Stock

Bal.

173,300

Bal.

230,000

Salaries Expense

Depreciation Expense

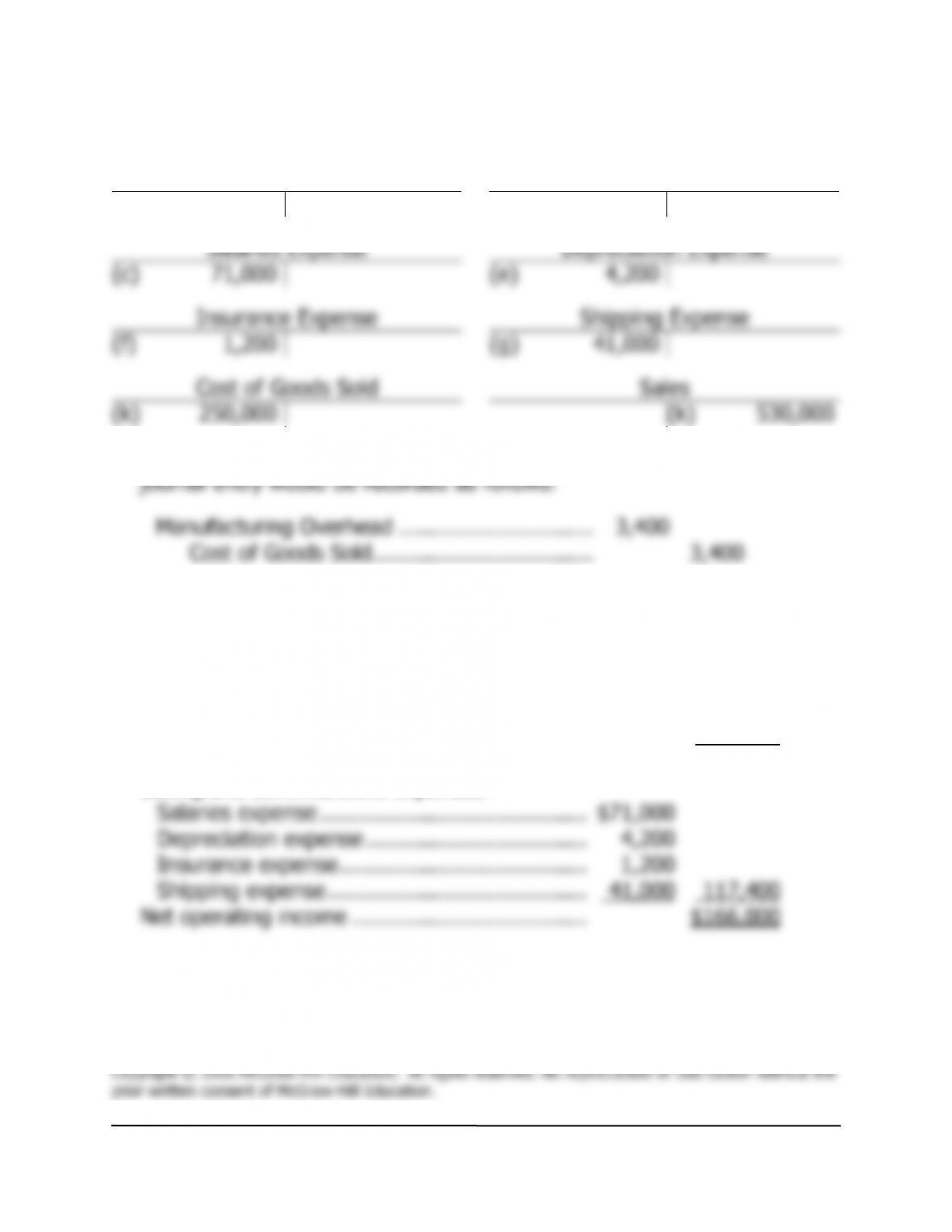

(c)

71,000

(e)

4,200

Insurance Expense

Shipping Expense

(f)

1,200

(g)

41,000

Cost of Goods Sold

Sales

(k)

250,000

(k)

530,000

3. Manufacturing overhead was overapplied by $3,400 for the year. The

Manufacturing Overhead …………………………

3,400

Cost of Goods Sold …………………………….

3,400

4.

Brinkerhoff, Inc.

Income Statement

For the Year Ended December 31

Sales ……………………………………………………

$530,000

Cost of goods sold ($250,000 – $3,400) ……….

246,600

Gross margin ………………………………………….

283,400

Selling and administrative expenses:

Salaries expense …………………………………..

$71,000

Depreciation expense …………………………….

4,200

Insurance expense ………………………………..

1,200

Shipping expense ………………………………….

41,000

117,400

Net operating income ………………………………

$166,000