Ethics Challenge (continued)

It would take tremendous courage for Keri to take the problem all the

way up to Stokes himself—particularly in view of his less-than-humane

treatment of subordinates. And going to the Board of Directors is

unlikely to work either because Stokes and his venture capital firm

Analytical Thinking (45 minutes)

1. The budgetary control system has several important shortcomings that

reduce its effectiveness and may cause it to interfere with good

performance. Some of the shortcomings are explained below.

a.

Lack of Coordinated Goals.

Emory had been led to believe high-

quality output is the goal; it now appears low cost is the goal.

2. The improvements in the budgetary control system should correct the

deficiencies described above. The system should:

a. more clearly define the company’s objectives.

Case (120 minutes)

1.

a.

Sales budget:

April

May

June

Quarter

Budgeted unit sales ……

65,000

100,000

50,000

215,000

Selling price per unit ….

× $10

× $10

× $10

× $10

Total sales ……………….

$650,000

$1,000,000

$500,000

$2,150,000

b.

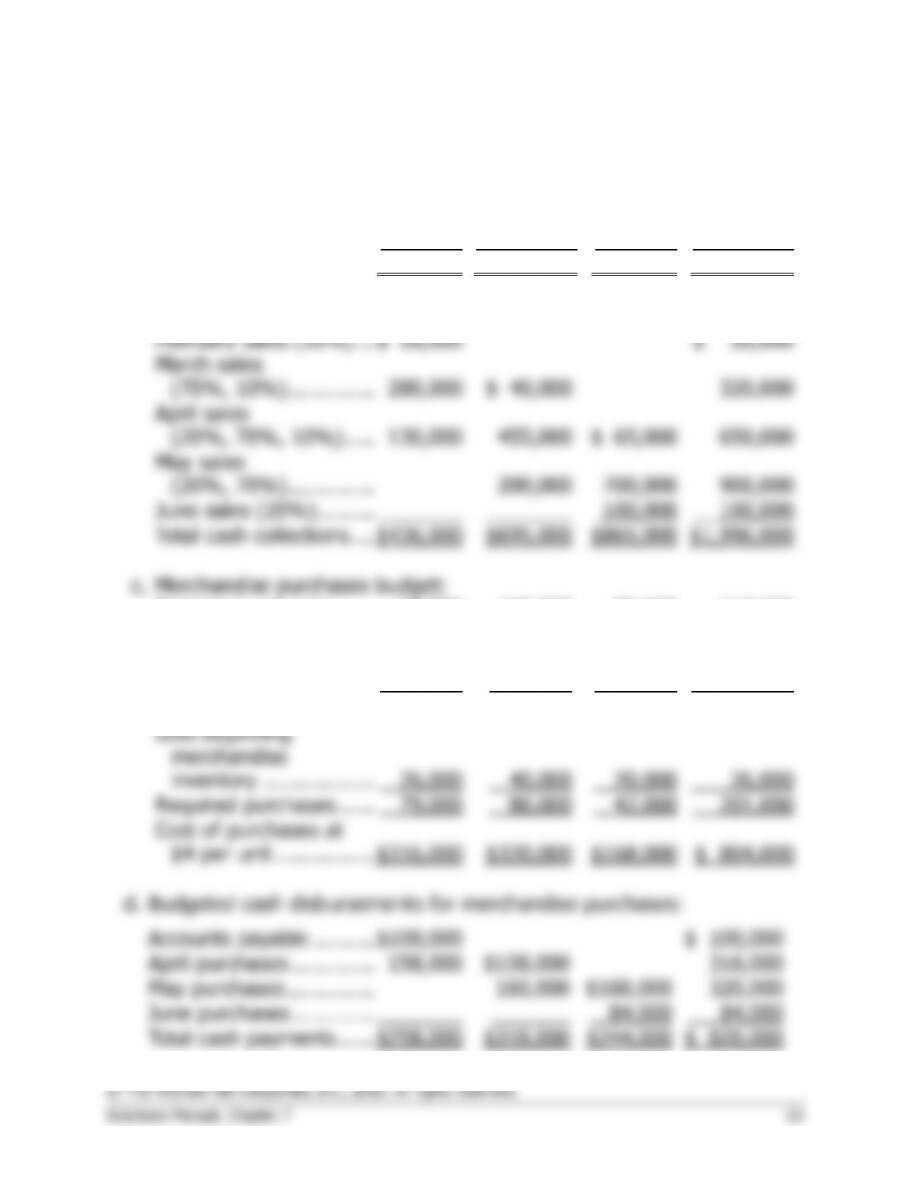

Schedule of expected cash collections:

February sales (10%) …

$ 26,000

$ 26,000

March sales

(70%, 10%) …………..

280,000

$ 40,000

320,000

April sales

(20%, 70%, 10%) …..

130,000

455,000

$ 65,000

650,000

May sales

(20%, 70%) …………..

200,000

700,000

900,000

June sales (20%) ………

100,000

100,000

Total cash collections ….

$436,000

$695,000

$865,000

$1,996,000

c.

Merchandise purchases budget:

Budgeted unit sales ……

65,000

100,000

50,000

215,000

Add desired ending

merchandise

inventory ………………

40,000

20,000

12,000

12,000

Total needs ………………

105,000

120,000

62,000

227,000

Less beginning

merchandise

inventory ………………

26,000

40,000

20,000

26,000

Required purchases ……

79,000

80,000

42,000

201,000

Cost of purchases at

$4 per unit …………….

$316,000

$320,000

$168,000

$ 804,000

d.

Budgeted cash disbursements for merchandise purchases:

Accounts payable ……….

$100,000

$ 100,000

April purchases ………….

158,000

$158,000

316,000

May purchases …………..

160,000

$160,000

320,000

June purchases ………….

84,000

84,000

Total cash payments ……

$258,000

$318,000

$244,000

$ 820,000

© The McGraw-Hill Companies, Inc., 2016. All rights reserved.

64 Introduction to Managerial Accounting, 7th Edition

Case (continued)

2.

Earrings Unlimited

Cash Budget

For the Three Months Ending June 30

April

May

June

Quarter

Beginning cash balance …..

$ 74,000

$ 50,000

$ 50,000

$ 74,000

Add collections from

customers ………………….

436,000

695,000

865,000

1,996,000

Total cash available ………..

510,000

745,000

915,000

2,070,000

Less cash disbursements:

Merchandise purchases …

258,000

318,000

244,000

820,000

Advertising ………………..

200,000

200,000

200,000

600,000

Rent …………………………

18,000

18,000

18,000

54,000

Salaries …………………….

106,000

106,000

106,000

318,000

Commissions (4% of

sales) ……………………..

26,000

40,000

20,000

86,000

Utilities ……………………..

7,000

7,000

7,000

21,000

Equipment purchases …..

0

16,000

40,000

56,000

Dividends paid ……………

15,000

0

0

15,000

Total cash disbursements ..

630,000

705,000

635,000

1,970,000

Excess (deficiency) of cash

available over

disbursements ……………

(120,000)

40,000

280,000

100,000

Financing:

Borrowings ………………..

170,000

10,000

0

180,000

Repayments ……………….

0

0

(180,000)

(180,000)

Interest

($170,000 × 1% × 3 +

$10,000 × 1% × 2) …..

0

0

(5,300)

(5,300)

Total financing ………………

170,000

10,000

(185,300)

(5,300)

Ending cash balance ………

$ 50,000

$ 50,000

$ 94,700

$ 94,700

© The McGraw-Hill Companies, Inc., 2016. All rights reserved.

Solutions Manual, Chapter 7 65

Case (continued)

3.

Earrings Unlimited

Budgeted Income Statement

For the Three Months Ended June 30

Sales (Part 1 a.) …………………………………

$2,150,000

Variable expenses:

Cost of goods sold @ $4 per unit …………

$860,000

Commissions @ 4% of sales ……………….

86,000

946,000

Contribution margin …………………………….

1,204,000

Fixed expenses:

Advertising ($200,000 × 3) ………………..

600,000

Rent ($18,000 × 3) …………………………..

54,000

Salaries ($106,000 × 3) …………………….

318,000

Utilities ($7,000 × 3) …………………………

21,000

Insurance ($3,000 × 3) ……………………..

9,000

Depreciation ($14,000 × 3) ………………..

42,000

1,044,000

Net operating income ………………………….

160,000

Interest expense (Part 2) ……………………..

5,300

Net income ……………………………………….

$ 154,700

Case (continued)

4.

Earrings Unlimited

Budgeted Balance Sheet

June 30

Assets

Cash ……………………………………………………………………

$ 94,700

Accounts receivable (see below) ………………………………..

500,000

Inventory (12,000 units @ $4 per unit) ……………………….

48,000

Prepaid insurance ($21,000 – $9,000) ………………………..

12,000

Property and equipment, net

($950,000 + $56,000 – $42,000) …………………………….

964,000

Total assets …………………………………………………………..

$1,618,700

Liabilities and Stockholders’ Equity

Accounts payable, purchases (50% × $168,000) …………..

$ 84,000

Dividends payable ………………………………………………….

15,000

Common stock ………………………………………………………

800,000

Retained earnings (see below) ………………………………….

719,700

Total liabilities and stockholders’ equity ……………………….

$1,618,700

Accounts receivable at June 30:

10% × May sales of $1,000,000 …………

$100,000

80% × June sales of $500,000 …………..

400,000

Total …………………………………………….

$500,000

Retained earnings at June 30:

Balance, March 31 …………………………..

$580,000

Add net income (part 3) …………………..

154,700

Total …………………………………………….

734,700

Less dividends declared ……………………

15,000

Balance, June 30 …………………………….

$719,700

Communicating in Practice (60 minutes)

1. Across-the-board cuts may be politically palatable and may be perceived

students.

2. When determining which programs should receive greater or smaller

3. If cuts are likely to continue, administrators should be particularly

4. To increase understanding and cooperation, the decision-making

5. By allowing individuals to participate in the budgeting process and by

attempting to build consensus, the animosity that may be felt by those

affected by cuts may be reduced. However, this is a two-edged sword.

Chapter 7

Take Two Solutions

Exercise 7-1 (20 minutes)

1.

April

May

June

Total

February sales:

$230,000 × 10% …….

$ 23,000

$ 23,000

March sales: $260,000

× 70%, 10% ………….

182,000

$ 26,000

208,000

April sales: $300,000 ×

20%, 70%, 10% …….

60,000

210,000

$ 30,000

300,000

May sales: $500,000 ×

20%, 70% …………….

100,000

350,000

450,000

June sales: $250,000 ×

20% …………………….

50,000

50,000

Total cash collections ….

$265,000

$336,000

$430,000

$1,031,000

Notice that even though sales peak in May, cash collections peak in

June. This occurs because the bulk of the company’s customers pay in

the month following sale. The lag in collections that this creates is even

more pronounced in some companies. Indeed, it is not unusual for a

company to have the least cash available in the months when sales are

greatest.

2. Accounts receivable at June 30:

From May sales: $500,000 × 10% ……………………

$ 50,000

From June sales: $250,000 × (70% + 10%) ………

200,000

Total accounts receivable at June 30 …………………

$250,000

Exercise 7-2 (10 minutes)

April

May

June

Quarter

Budgeted unit sales ……………..

50,000

75,000

90,000

215,000

Add desired units of ending

finished goods inventory* ……

15,000

18,000

16,000

16,000

Total needs ………………………..

65,000

93,000

106,000

231,000

Less units of beginning finished

goods inventory ………………..

10,000

15,000

18,000

10,000

Required production in units …..

55,000

78,000

88,000

221,000

*20% of the following month’s sales in units.

Exercise 7-3 (15 minutes)

Quarter—Year 2

First

Second

Third

Fourth

Year

Required production in units of finished

goods ………………………………………………

60,000

90,000

150,000

100,000

400,000

Units of raw materials needed per unit of

finished goods …………………………………..

× 4

× 4

× 4

× 4

× 4

Units of raw materials needed to meet

production ………………………………………..

240,000

360,000

600,000

400,000

1,600,000

Add desired units of ending raw materials

inventory ………………………………………….

72,000

120,000

80,000

56,000

56,000

Total units of raw materials needed ………….

312,000

480,000

680,000

456,000

1,656,000

Less units of beginning raw materials

inventory ………………………………………….

48,000

72,000

120,000

80,000

48,000

Units of raw materials to be purchased ……..

264,000

408,000

560,000

376,000

1,608,000

Unit cost of raw materials ……………………….

× $1.50

× $1.50

× $1.50

× $1.50

× $1.50

Cost of raw materials to purchased …………..

$396,000

$612,000

$840,000

$564,000

$2,412,000

Exercise 7-4 (20 minutes)

1. Assuming that the direct labor workforce is adjusted each quarter, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ……………………….

8,000

6,500

7,000

7,500

29,000

Direct labor time per unit (hours) …………………

× 0.30

× 0.30

× 0.30

× 0.30

× 0.30

Total direct labor-hours needed……………………

2,400

1,950

2,100

2,250

8,700

Direct labor cost per hour …………………………..

× $12.00

× $12.00

× $12.00

× $12.00

× $12.00

Total direct labor cost ………………………………..

$ 28,800

$ 23,400

$ 25,200

$ 27,000

$104,400

2. Assuming that the direct labor workforce is not adjusted each quarter and that overtime wages are

paid, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ………………………

8,000

6,500

7,000

7,500

Direct labor time per unit (hours) ………………..

× 0.30

× 0.30

× 0.30

× 0.30

Total direct labor-hours needed ………………….

2,400

1,950

2,100

2,250

Regular hours paid …………………………………..

2,600

2,600

2,600

2,600

Overtime hours paid …………………………………

0

0

0

0

Wages for regular hours (@ $12.00 per hour) ..

$31,200

$31,200

$31,200

$31,200

$124,800

Overtime wages (@ 1.5 × $12.00 per hour) ….

0

0

0

0

0

Total direct labor cost …………………………..…..

$31,200

$31,200

$31,200

$31,200

$124,800