Ethics Challenge (90 minutes)

1. The original cost of the facilities at Clayton is a sunk cost and should be

ignored in any decision. The decision being considered here is whether to

continue operations at Clayton. The only relevant costs are the future

facility costs that would be affected by this decision. If the facility were

shut down, the Clayton facility has no resale value. In addition, if the

Increase in rent at Billings and Great Falls ……………..

$600,000

Decrease in local administrative expenses ………………

(90,000)

Net increase in costs …………………………………………

$510,000

In addition, there would be costs of moving the equipment from Clayton

and there might be some loss of sales due to disruption of services. In

Ethics Challenge (continued)

Financial Performance

After Shutting Down the Clayton Facility

Rocky Mountain Region

Total

Sales …………………………………………………….

$50,000,000

Selling and administrative expenses:

Direct labor ………………………………………….

32,000,000

Variable overhead………………………………….

850,000

Equipment depreciation ………………………….

3,900,000

Facility expense* …………………………………..

2,300,000

Local administrative expense** ………………..

360,000

Regional administrative expense ……………….

1,500,000

Corporate administrative expense ……………..

4,750,000

Total operating expense …………………………...

45,660,000

Net operating income ……………………………….

$ 4,340,000

* $2,800,000 – $1,100,000 + $600,000 = $2,300,000

** $450,000 – $90,000 = $360,000

2. If the Clayton facility is shut down, BSC’s profits will decline, employees

will lose their jobs, and customers will at least temporarily suffer some

decline in service. Therefore, Romeros is willing to sacrifice the interests

of the company, its employees, and its customers just to make her

performance report look better.

Ethics Challenge (continued)

It should be noted that the performance report required by corporate

3. Prices should be set ignoring the depreciation on the Clayton facility. As

argued in part (1) above, the real cost of using the Clayton facility is

Analytical Thinking (120 minutes)

1. The product margins computed by the accounting department for the

drums and bike frames should not be used in the decision of which

product to make. The product margins are lower than they should be

2. Students may have answered this question assuming that direct labor is

a variable cost, even though the case strongly hints that direct labor is a

Solution assuming direct labor is fixed

Manufactured

Purchased

WVD

Drums

WVD

Drums

Bike

Frames

Selling price ……………………………….

$149.00

$149.00

$239.00

Variable costs:

Direct materials ………………………..

138.00

52.10

99.40

Variable manufacturing overhead ….

0.00

1.35

1.90

Variable selling and administrative ..

0.75

0.75

1.30

Total variable cost ……………………….

138.75

54.20

102.60

Contribution margin ……………………..

$ 10.25

$ 94.80

$136.40

Analytical Thinking (continued)

3. Because the demand for the welding machine exceeds the 2,000 hours

that are available, products that use the machine should be prioritized

Solution assuming direct labor is fixed

Manufactured

WVD

Drums

Bike

Frames

Contribution margin per unit (above) (a) …………

$94.80

$136.40

Welding hours per unit (b) …………………………...

0.4 hour

0.5 hour

Contribution margin per welding hour (a) ÷ (b) ..

$237.00

per hour

$272.80

per hour

Analytical Thinking (continued)

Because the contribution margin per unit of the constrained resource (i.e., welding time) is larger for the

bike frames than for the WVD drums, the frames make the most profitable use of the welding machine.

Analysis assuming direct labor is a fixed cost

(a)

(b)

(c)

(a) × (c)

(a) × (b)

Quantity

Unit

Contri-

bution

Margin

Welding

Time

per Unit

Total

Welding

Time

Balance

of

Welding

Time

Total

Contri-

bution

Total hours available ……………….

2,000

Bike frames produced ……………..

1,600

$136.40

0.5

800

1,200

$218,240

WVD Drums—make ………………..

3,000

$94.80

0.4

1,200

0

284,400

WVD Drums—buy ………………….

3,000

$10.25

30,750

Total contribution margin …………

533,390

Less: Contribution margin from

present operations: 5,000

drums × $94.80 CM per drum ..

474,000

Increased contribution margin

and net operating income ……..

$ 59,390

Analytical Thinking (continued)

4. The computation of the contribution margins and the analysis of the

best product mix are repeated here under the assumption that direct

labor costs are variable.

Solution assuming direct labor is a variable cost

Manufactured

Purchased

WVD

Drums

WVD

Drums

Bike

Frames

Selling price ……………………………..

$149.00

$149.00

$239.00

Variable costs:

Direct materials ………………………

138.00

52.10

99.40

Direct labor …………………………...

0.00

3.60

28.80

Variable manufacturing overhead ..

0.00

1.35

1.90

Variable selling and administrative

0.75

0.75

1.30

Total variable cost ……………………..

138.75

57.80

131.40

Contribution margin ……………………

$ 10.25

$ 91.20

$107.60

Solution assuming direct labor is a variable cost

Manufactured

WVD

Drums

Bike

Frames

Contribution margin per unit (above) (a) ……….

$91.20

$107.60

Welding hours per unit (b) ………………………….

0.4 hour

0.5 hour

Contribution margin per welding hour (a) ÷ (b)

$228.00

per hour

$215.20

per hour

When direct labor is assumed to be a variable cost, the conclusion is

reversed from the case in which direct labor is assumed to be a fixed

cost—the WVD drums appear to be a better use of the constraint than

the bike frames. The assumption about the behavior of direct labor

really does matter.

Analytical Thinking (continued)

Solution assuming direct labor is a variable cost

(a)

(b)

(c)

(a) × (c)

(a) × (b)

Quantity

Unit

Contri-

bution

Margin

Welding

Time

per Unit

Total

Welding

Time

Balance

of

Welding

Time

Total

Contri-

bution

Total hours available ………………..

2,000

WVD Drums—make …………………

5,000

$91.20

0.4

2,000

0

$456,000

Bike frames produced ………………

0

$107.60

0.5

0

0

0

WVD Drums—buy …………………..

1,000

$10.25

10,250

Total contribution margin ………….

466,250

Less: Contribution margin from

present operations: 5,000

drums × $91.20 CM per drum …

456,000

Increased contribution margin

and net operating income ………

$ 10,250

Analytical Thinking (continued)

5. The case strongly suggests that direct labor is fixed: “The bike frames

could be produced with existing equipment and personnel.”

Nevertheless, it would be a good idea to examine how much labor time

is really needed under the two opposing plans.

Production

Direct Labor-

Hours Per Unit

Total Direct

Labor-Hours

Plan 1:

Bike frames ……………..

1,600

1.6*

2,560

WVD drums …………….

3,000

0.2**

600

3,160

Plan 2:

WVD drums …………….

5,000

0.2**

1,000

* $28.80 ÷ $18.00 per hour = 1.6 hour

** $3.60 ÷ $18.00 per hour = 0.2 hour

Some caution is advised. Plan 1 assumes that direct labor is a fixed cost.

However, this plan requires 2,160 more direct labor-hours than Plan 2

and the present situation. At 40 hours per week a typical full-time

Analytical Thinking (continued)

Contribution margin from Plan 1:

Bike frames produced (1,600 × $136.40) …………

218,240

WVD Drums—make (3,000 × $94.80) ……………..

284,400

WVD Drums—buy (3,000 × $10.25) ……………….

30,750

Total contribution margin ……………………………..

533,390

Less: Additional fixed labor costs ……………………..

34,200

Net effect of Plan 1 on net operating income ………

$499,190

Contribution margin from Plan 2: ……………………..

WVD Drums—make (5,000 × $94.80) ……………..

$474,000

WVD Drums—buy (1,000 × $10.25) ……………….

10,250

Net effect of Plan 2 on net operating income ………

$484,250

If an additional direct labor employee would have to be hired, Plan 1 is

still optimal.

Chapter 10

Take Two Solutions

Exercise 10-4 (15 minutes)

Only the incremental costs and benefits are relevant. In particular, only the

variable manufacturing overhead and the cost of the special tool are

relevant overhead costs in this situation. The other manufacturing

overhead costs are fixed and are not affected by the decision.

Per Unit

Total

for 20

Bracelets

Incremental revenue ………………………..

$139.95

$2,799.00

Incremental costs:

Variable costs:

Direct materials ………………………….

$ 84.00

1,680.00

Direct labor ……………………………….

45.00

900.00

Variable manufacturing overhead …..

4.00

80.00

Special filigree …………………………...

2.00

40.00

Total variable cost …………………………

$135.00

2,700.00

Fixed costs:

Purchase of special tool ………………..

250.00

Total incremental cost ………………………

2,950.00

Incremental net operating income ………

$ (151.00)

The special order would not add to the company’s net operating income

and should be rejected.

Exercise 10-7 (10 minutes)

A

B

C

Selling price after further processing ….

$20

$13

$32

Selling price at the split-off point ………

16

8

25

Incremental revenue per pound or

gallon ……………………………………….

$ 4

$ 5

$ 7

Total quarterly output in pounds or

gallons ……………………………………..

×15,000

×20,000

×4,000

Total incremental revenue ……………….

$60,000

$100,000

$28,000

Total incremental processing costs …….

57,000

102,000

36,000

Total incremental profit or loss …………

$ 3,000

$ (2,000)

$(8,000)

Therefore, only product A should be processed further.

Exercise 10-8 (30 minutes)

1.

A

B

C

(1)

Contribution margin per unit ………………………

$54

$108

$76

(2)

Direct material cost per unit ………………………

$24

$72

$16

(3)

Direct material cost per pound ……………………

$8

$8

$8

(4)

Pounds of material required per unit (2) ÷ (3) .

3

9

2

(5)

Contribution margin per pound (1) ÷ (4) ………

$18

$12

$38

2. The company should concentrate its available material on product C:

A

B

C

Contribution margin per pound (above) .

$ 18

$ 12

$ 38

Pounds of material available ………………

× 5,000

× 5,000

× 5,000

Total contribution margin ………………….

$90,000

$60,000

$190,000

3. The price Barlow Company would be willing to pay per pound for

additional raw materials depends on how the materials would be used.

If there are unfilled orders for all of the products, Barlow would

presumably use the additional raw materials to make more of product C.

Exercise 10-11 (20 minutes)

The costs that can be avoided as a result of purchasing from the outside

are relevant in a make-or-buy decision. The analysis is:

Per Unit

Differential

Costs

30,000 Units

Make

Buy

Make

Buy

Cost of purchasing ……………….

$21.00

$630,000

Cost of making:

Direct materials …………………

$ 3.60

$108,000

Direct labor ………………………

10.00

300,000

Variable overhead ……………..

2.40

72,000

Fixed overhead …………………

3.00

*

90,000

Total cost …………………………..

$19.00

$21.00

$570,000

$630,000

Make

Buy

Total cost, as above ………………………………….

$570,000

$630,000

Rental value of the space (opportunity cost) …..

50,000

Total cost, including opportunity cost ……………

$620,000

$630,000

Net advantage in favor of making ………………..

$10,000

Profits would be $10,000 higher if the outside supplier’s offer is rejected.

Exercise 10-12 (15 minutes)

The company should accept orders first for Product A, second for Product

B, and third for Product C. The computations are:

Product

A

Product

B

Product

C

(1)

Direct materials required per unit ……

$24

$15

$18

(2)

Cost per pound …………………………..

$3

$3

$3

(3)

Pounds required per unit (1) ÷ (2) ….

8

5

6

(4)

Contribution margin per unit ………….

$32

$14

$12

(5)

Contribution margin per pound of

materials used (4) ÷ (3) …………….

$4.00

$2.80

$2.00

Exercise 10-13 (10 minutes)

Sales value after further processing

(7,000 units × $12 per unit) ……………………..

$84,000

Sales value at the split-off point

(7,000 units × $9 per unit) ………………………

63,000

Incremental revenue from further processing …

21,000

Cost of further processing ………………………….

22,000

Loss from further processing ………………………

$(1,000)

The $60,000 cost incurred up to the split-off point is not relevant in a

decision of what to do after the split-off point.

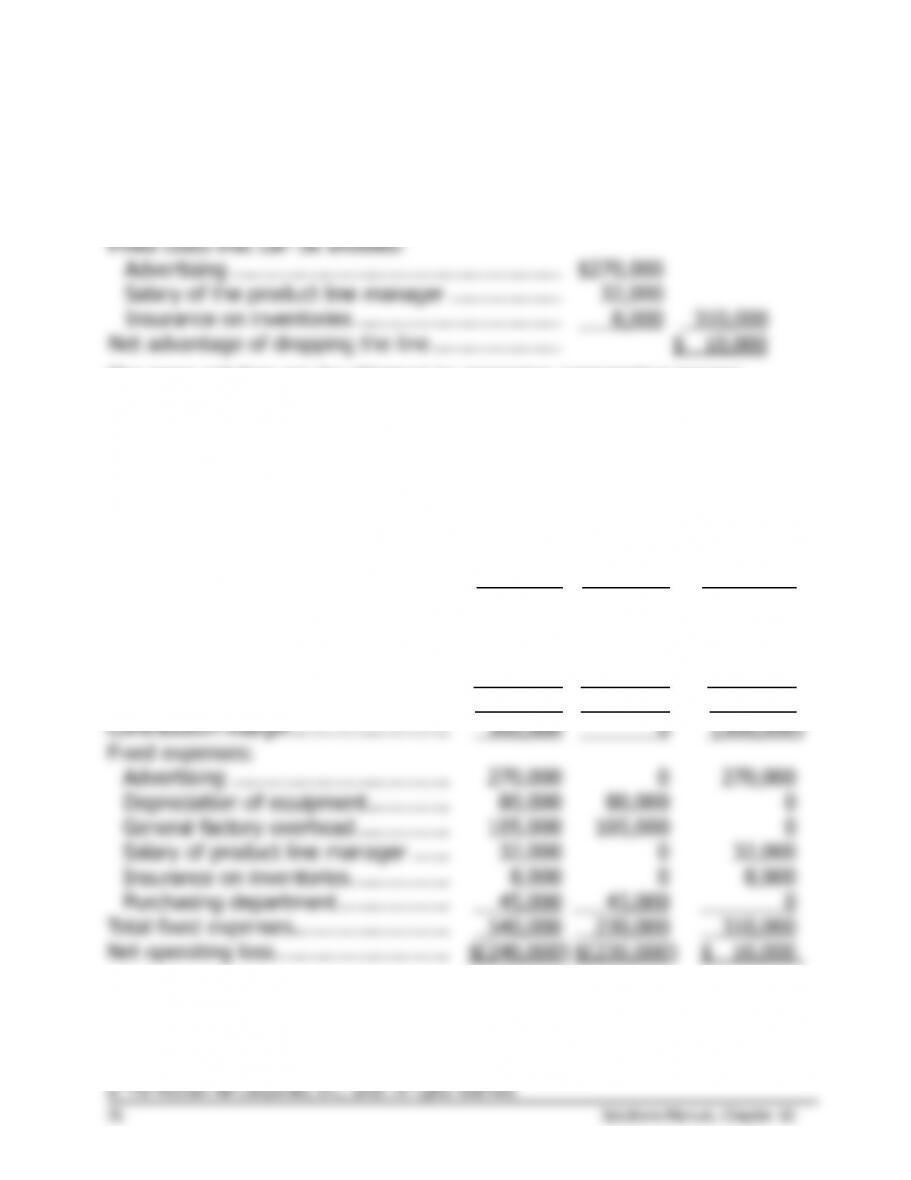

Exercise 10-15 (30 minutes)

No, the bilge pump product line should not be discontinued. The

computations are:

Contribution margin lost if the line is dropped …..

$(300,000)

Fixed costs that can be avoided:

Advertising ……………………………………………..

$270,000

Salary of the product line manager ………………

32,000

Insurance on inventories …………………………...

8,000

310,000

Net advantage of dropping the line …………………

$ 10,000

The same solution can be obtained by preparing comparative income

statements:

Keep

Product

Line

Drop

Product

Line

Difference:

Net

Operating

Income

Increase or

(Decrease)

Sales …………………………..……………

$690,000

$ 0

$(690,000)

Variable expenses:

Variable manufacturing expenses …

330,000

0

330,000

Sales commissions ……………………

42,000

0

42,000

Shipping …………………………………

18,000

0

18,000

Total variable expenses ………………..

390,000

0

390,000

Contribution margin …………………….

300,000

0

(300,000)

Fixed expenses:

Advertising ……………………………..

270,000

0

270,000

Depreciation of equipment ………….

80,000

80,000

0

General factory overhead ……………

105,000

105,000

0

Salary of product line manager ……

32,000

0

32,000

Insurance on inventories…………….

8,000

0

8,000

Purchasing department ………………

45,000

45,000

0

Total fixed expenses …………………….

540,000

230,000

310,000

Net operating loss ……………………….

$(240,000)

$(230,000)

$ 10,000