Problem 5-19B (60 minutes)

1.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

(($58 − $37.60) × Q) − $401,880

$0

=

($20.40 × Q) − $401,880

$20.40Q

=

$401,880

Q

=

$401,880 ÷ $20.40 per shirt

Q

=

19,700 shirts

Break-even sales ……………..

Actual sales …………………….

Sales short of break-even ….

Sales (18,200 shirts × $58.00 per shirt) …………………

Variable expenses (18,200 shirts × $37.60 per shirt) ..

Contribution margin …………………………………………..

Fixed expenses …………………………………………………

Net operating loss …………………………………………….

$(30,600)

Problem 5-19B (continued)

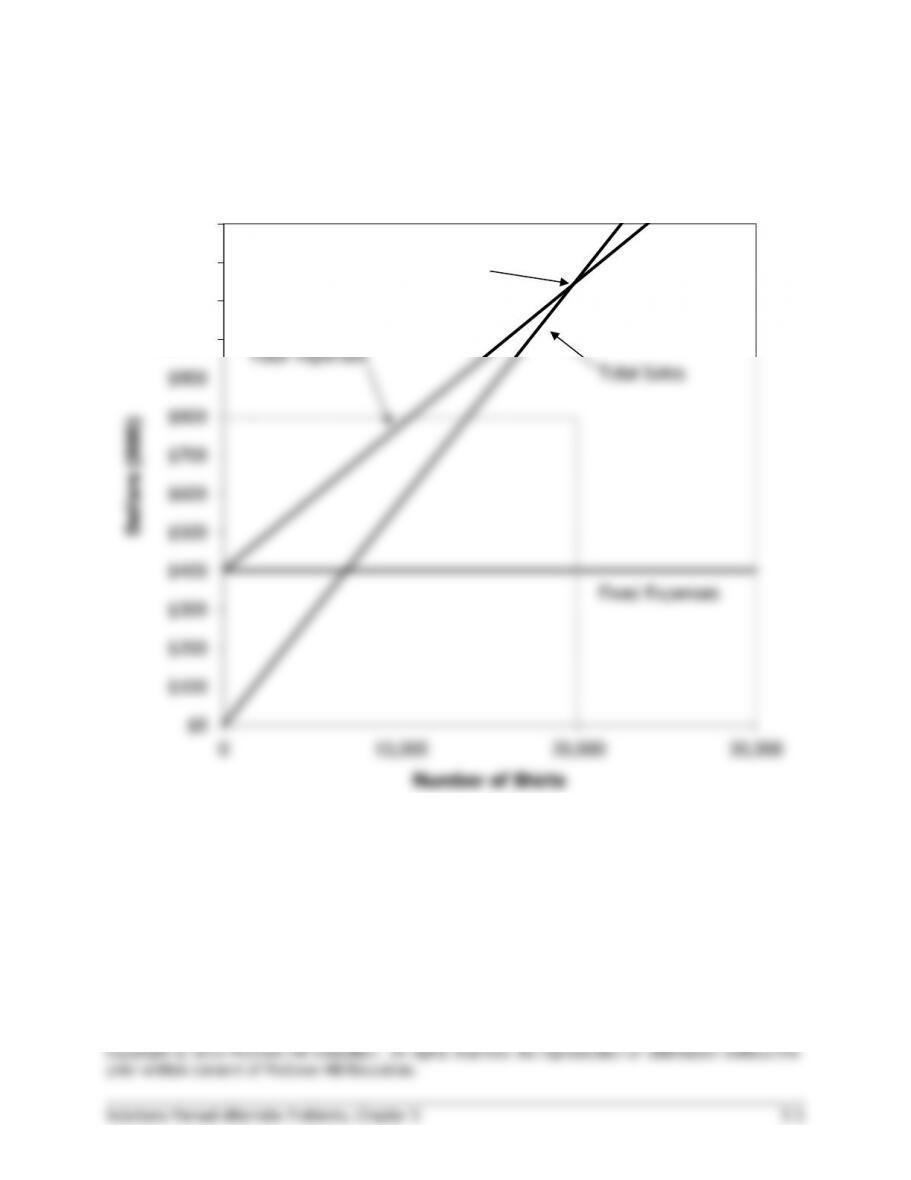

2. Cost-volume-profit graph:

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

0 10,000 20,000 30,000

Dollars (000)

Number of Shirts

Break-even point: 19,700 shirts,

or $1,142,600 in sales

Fixed Expenses

Total Expenses

Total Sales

Actual sales …………………………….

Excess over break-even sales ……..

Problem 5-19B (continued)

4. The variable expenses will now be $38.30 ($37.60 + $0.70) per shirt,

and the contribution margin will be $19.70 ($58.00 – $38.30) per shirt.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

(($58.00 − $38.30) × Q) − $401,880

$0

=

($19.70 × Q) − $401,880

$19.70Q

=

$401,880

Q

=

$401,880 ÷ $19.70 per shirt

Q

=

20,400 shirts

Problem 5-19B (continued)

Alternative solution:

Sales (23,140 shirts × $58 per shirt) ………………..

$1,342,120

Variable expenses [(19,700 shirts × $37.60 per

shirt) + (3,440 shirts × $38.30 per shirt)] ……….

872,472

Contribution margin ………………………………………

469,648

Fixed expenses …………………………………………….

401,880

Net operating income ……………………………………

$ 67,768

6. a. The new variable expense will be $27 per shirt (the invoice price).

Profit

=

Unit CM × Q − Fixed expenses

$0

=

(($58.00 − $27.00) × Q) − $564,200

$0

=

($31.00 × Q) − $564,200

$31Q

=

$564,200

Q

=

$564,200 ÷ $31.00 per shirt

Q

=

18,200 shirts

18,200 shirts × $58.00 shirt = $1,055,600 in sales

b. Although the change will lower the break-even point from 19,700

shirts to 18,200 shirts, the company must consider whether this

reduction in the break-even point is more than offset by the possible

loss in sales arising from having the sales staff on a salaried basis.

Under a salary arrangement, the sales staff may have far less

incentive to sell than under the present commission arrangement,

resulting in a loss of sales and a reduction in profits. Although it

generally is desirable to lower the break-even point, management

must consider the other effects of a change in the cost structure. The

break-even point could be reduced dramatically by doubling the

selling price per shirt, but it does not necessarily follow that this

would increase the company’s profit.

$120,000

$120,000 ÷ $8 per unit

15,000 units

Unit contribution margin

Incremental contribution margin:

Less increased fixed costs:

Increase in monthly net operating income …………

Problem 5-20B (60 minutes)

1. The CM ratio is 30%.

Total

Per Unit

Percentage

Sales (13,500 units) ………

$270,000

$20

100%

Variable expenses …………

162,000

12

60%

Contribution margin ………

$108,000

$ 8

40%

Problem 5-20B (continued)

Since the company presently has a loss of $12,000 per month, if the

changes are adopted, the loss will turn into a profit of $16,000 per

month.

3.

Sales (27,000 units × $18 per unit*) …………..

$486,000

Variable expenses

(27,000 units × $12 per unit) ………………….

324,000

Contribution margin …………………………………

162,000

Fixed expenses ($120,000 + $30,000) …………

150,000

Net operating income (loss) ………………………

$ 12,000)

*$20 – ($20 × 0.10) = $18

4.

Profit

=

Unit CM × Q − Fixed expenses

$4,400

=

(($20.00 − $12.40*) × Q) − $120,000

$4,400

=

($7.60 × Q) − $120,000

$7.60Q

=

$124,400

Q

=

$124,400 ÷ $7.60 per unit

Q

=

16,368 units

$7.60** per unit

Sales (20,300 units) ….

Variable expenses …….

Contribution margin ….

Fixed expenses ………..

Problem 5-20B (continued)

5. a. The new CM ratio would be:

Per Unit

Percentage

Sales ……………………………………

$20

100%

Variable expenses……………………

6

30%

Contribution margin …………………

$14

70%

Problem 5-20B (continued)

c. Whether or not one would recommend that the company automate

its operations depends on how much risk he or she is willing to take,

and depends heavily on prospects for future sales. The proposed

Problem 5-21B (60 minutes)

1. The CM ratio is 50%:

Selling price ………………….

$80

100%

Variable expenses …………..

40

50%

Contribution margin ………..

$40

50%

2.

Dollar sales to

break even

=

Fixed expenses

CM ratio

=

$180,000

=

$360,000 in sales

0.5

3. $53,000 increased sales × 50% CM ratio = $26,500 increase in

4. a.

Degree of operating leverage

=

Contribution margin

Net operating income

=

$1,080,000

=

1.20

$900,000

b. 1.20 × 14% = 16.80% increase in net operating income. In dollars,

Problem 5-21B (continued)

5.

Last Year:

37,500 units

Proposed:

56,250 units*

Total

Per Unit

Total

Per Unit

Sales ………………………

$3,000,000

$80.00

$4,005,000

$71.20

**

Variable expenses ……..

1,500,000

40.00

2,250,000

40.00

Contribution margin ……

1,500,000

$40.00

1,755,000

$31.20

Fixed expenses …………

180,000

243,000

Net operating income …

$1,320,000

$1,512,000

*

37,500 units × 1.5 = 56,250 units

**

$80 per unit × .89 = $71.20 per unit

No, the changes should not be made.

6.

Expected total contribution margin:

37,500 units × 200% × $37.50 per unit* ………..

$2,812,000

Present total contribution margin:

37,500 units × $40.00 per unit ……………………..

1,500,000

Incremental contribution margin, and the amount

by which advertising can be increased with net

operating income remaining unchanged ………….

$1,312,000

*$80.00 – ($40.00 + $2.50) = $37.50

Problem 5-22B (30 minutes)

1.

Product

Sinks

Mirrors

Vanities

Total

Percentage of total

sales …………………….

32%

40%

28%

100%

Sales ………………………

$204,800

100

%

$256,000

100

%

$179,200

100

%

$640,000

100

%

Variable expenses ……..

61,440

30

%

204,800

80

%

98,560

55

%

364,800

57

%

Contribution margin ……

$143,360

70

%

$ 51,200

20

%

$ 80,640

45

%

275,200

43

%*

Fixed expenses …………

224,120

Net operating income ..

$51,080)

*$275,200 ÷ $640,000 = 43%.

Problem 5-22B (continued)

2.

Break-even sales

=

Fixed expenses

CM ratio

=

$224,120

=

$521,209 in sales

0.43

3. Memo to the president:

Although the company met its sales budget of $640,000 for the month,

the mix of products sold changed substantially from that budgeted. This

is the reason the budgeted net operating income was not met, and the

Problem 5-23B (45 minutes)

1. a.

Alvaro

Bazan

Total

%

%

%

Sales …………………….

€1,350

100

€810

100

€2,160

100

Variable expenses

810

60

162

20

972

45

Contribution margin ….

€ 540

40

€648

80

1,188

55

Fixed expenses ………..

560

Net operating income .

€ 628

b.

Break-even sales

=

Fixed expenses

CM ratio

=

€560

=

€1,018.18 in sales

0.55

Margin of safety

=

Actual sales – Break-even sales

€2,160.00 – €1,018.18 = €1,141.82

Margin of safety percentage

=

Margin of safety

Actual sales

=

€1,141.82

=

52.86%

€2,160.00

Problem 5-23B (continued)

2. a.

Alvaro

Bazan

Cano

Total

%

%

%

%

Sales ………………………..

€1,350

100

€810

100

€540

100

€2,700

100

Variable expenses ………..

810

60

162

20

405

75

1,377

51

Contribution margin ……..

€ 540

40

€648

80

€135

25

1,323

49

Fixed expenses ……………

560

Net operating income …..

€ 763

b.

Break-even sales

=

Fixed expenses

CM ratio

=

€560

=

€1,142.86 in sales

0.49

Margin of safety

=

Actual sales – Break-even sales

€2,700.00 – €1,142.86 = €1,557.14

Margin of safety percentage

=

Margin of safety

Actual sales

=

€1,557.14

=

57.67%

€2,700.00

Solutions Manual Alternate Problems, Chapter 5 5-16

Problem 5-23B (continued)

3. The reason for the increase in the break-even point can be traced to the

decrease in the company’s average contribution margin ratio when the

third product is added. Note from the income statements above that this

ratio drops from 55% to 49% with the addition of the third product.

57.67%. Thus, the addition of the new product shifts the company

Problem 5-24B (60 minutes)

1. a. April’s Income Statement:

Standard

Deluxe

Pro

Total

Amount

%

Amount

%

Amount

%

Amount

%

Sales ………………………

$141,000

100

$130,000

100

$516,000

100

$787,000

100

Variable expenses:

Production ……………..

56,400

40

45,500

35

154,800

30

256,700

32.6

Selling …………………..

7,050

5

6,500

5

25,800

5

39,350

5.0

Total variable expenses .

63,450

45

52,000

40

180,600

35

296,050

37.6

Contribution margin ……

$77,550

55

$78,000

60

$335,400

65

490,950

62.4

Fixed expenses:

Production ………………

107,000

Advertising ……………..

106,000

Administrative ………….

57,000

Total fixed expenses ……

270,000

Net operating income …..

$220,950

Problem 5-24B (continued)

1. b. May’s Income Statement:

Standard

Deluxe

Pro

Total

Amount

%

Amount

%

Amount

%

Amount

%

Sales ……………………….

$376,000

100

$130,000

100

$258,000

100

$764,000

100.0

Variable expenses:

Production ……………..

150,400

40

45,500

35

77,400

30

273,300

35.8

Selling …………………..

18,800

5

6,500

5

12,900

5

38,200

5.0

Total variable expenses .

169,200

45

52,000

40

90,300

35

311,500

40.8

Contribution margin ……

$206,800

55

$78,000

60

$167,700

65

452,500

59.2

Fixed expenses:

Production ……………..

107,000

Advertising …………….

106,000

Administrative …………

57,000

Total fixed expenses …..

270,000

Net operating income ….

$182,500

Problem 5-24B (continued)

2. The sales mix has shifted over the last month from a greater

concentration of Pro rackets to a greater concentration of Standard

3. The break-even in dollar sales can be computed as follows:

Unit sales to break even

=

Fixed expenses

CM ratio

=

$270,000

=

$432,692 (rounded)

.624

4. May’s break–even point has gone up. The reason is that the division’s

5.

Standard

Pro

Increase in sales …………………………….

$27,000

$27,000

Multiply by the CM ratio ……………………

× 55%

× 65%

Increase in net operating income* ………

$14,850

$17,550

*Assuming that fixed costs do not change.