Problem 5-20A (continued)

c. This problem illustrates the difficulty faced by some companies. When

Problem 5-21A (30 minutes)

1.

Product

White

Fragrant

Loonzain

Total

Percentage of total

sales …………………

40%

24%

36%

100%

Sales …………………..

$300,000

100%

$180,000

100%

$270,000

100%

$750,000

100%

Variable expenses …..

216,000

72%

36,000

20%

108,000

40%

360,000

48%

Contribution margin ..

$ 84,000

28%

$144,000

80%

$162,000

60%

390,000

52%

*

Fixed expenses ………

449,280

Net operating

income (loss) ………

$ (59,280)

2. Break-even sales would be:

Fixed expenses

Dollar sales to =

break even CM ratio

Problem 5-21A (continued)

3. Memo to the president:

Although the company met its sales budget of $750,000 for the month,

the mix of products changed substantially from that budgeted. This is

the reason the budgeted net operating income was not met, and the

Problem 5-22A (60 minutes)

1. The CM ratio is 30%:

Total

Per Unit

Percent of Sales

Sales (19,500 units) ………

$585,000

$30.00

100%

Variable expenses …………

409,500

21.00

70%

Contribution margin ………

$175,500

$ 9.00

30%

= ($30 − $21) × Q − $180,000

= ($9) × Q − $180,000

= $180,000

Incremental contribution margin:

Problem 5-22A (continued)

3.

Sales (39,000 units @ $27.00 per unit*) ………

$1,053,000

Variable expenses

(39,000 units @ $21.00 per unit) ……………..

819,000

Contribution margin …………………………………

234,000

Fixed expenses ($180,000 + $60,000) …………

240,000

Net operating loss …………………………………..

$ (6,000)

*$30.00 – ($30.00 × 0.10) = $27.00

4.

Profit

= Unit CM × Q − Fixed expenses

$9,750

= ($30.00 − $21.75*) × Q − $180,000

$9,750

= ($8.25) × Q − $180,000

$8.25Q

= $189,750

Q

= $189,750 ÷ $8.25

Q

= 23,000 units

Target profit + Fixed expenses

Unit sales to attain =

target profit CM per unit

$9,750 + $180,000

=

$8.25**

= 23,000 units

5. a. The new CM ratio would be:

Per Unit

Percent of Sales

Sales ……………………….

$30.00

100%

Variable expenses ………

18.00

60%

Contribution margin ……

$12.00

40%

Problem 5-22A (continued)

The new break-even point would be:

Fixed expenses

Unit sales to =

break even Unit contribution margin

$180,000 + $72,000

=

$12.00

= 21,000 units

Fixed expenses

Dollar sales to =

break even CM ratio

$180,000 + $72,000

=

0.40

= $630,000

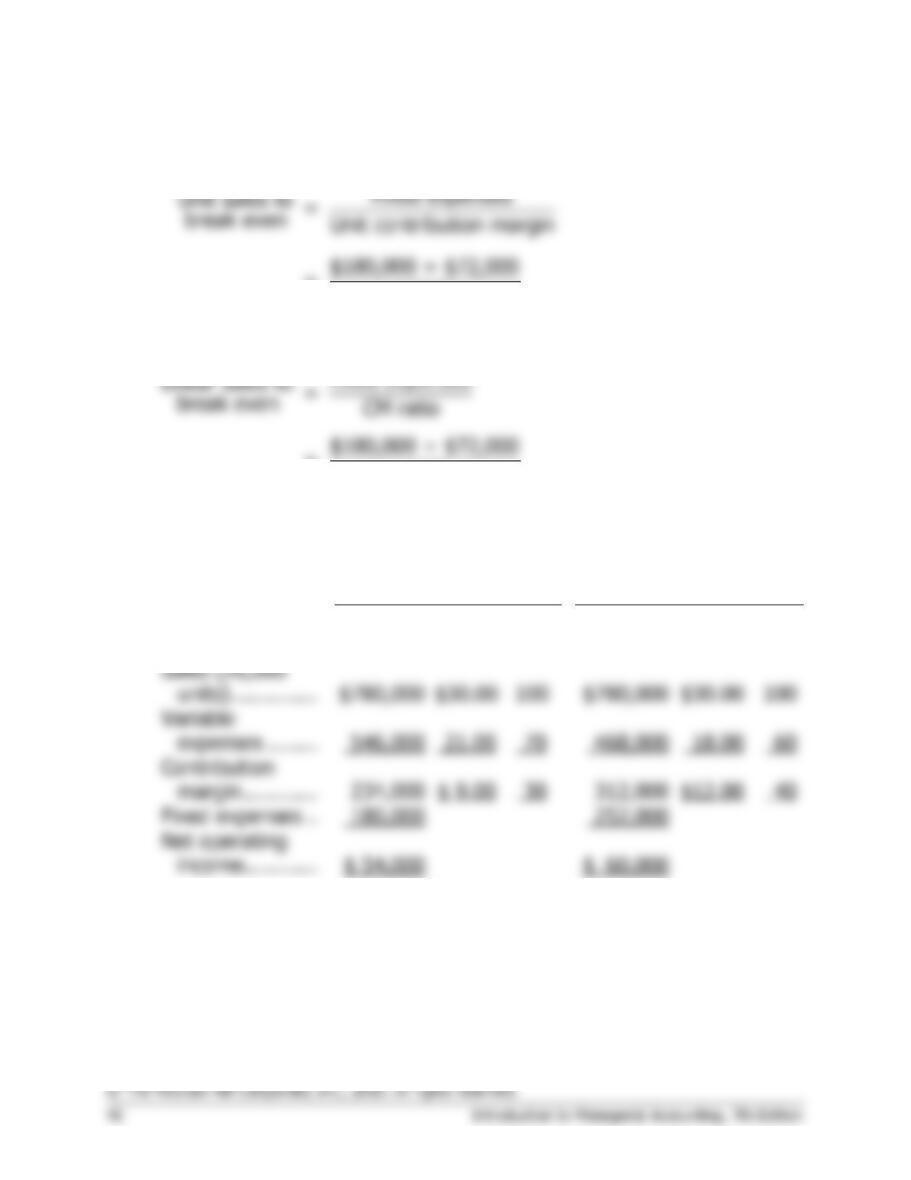

b. Comparative income statements follow:

Not Automated

Automated

Total

Per

Unit

%

Total

Per

Unit

%

Sales (26,000

units) …………..

$780,000

$30.00

100

$780,000

$30.00

100

Variable

expenses ……..

546,000

21.00

70

468,000

18.00

60

Contribution

margin …………

234,000

$ 9.00

30

312,000

$12.00

40

Fixed expenses ..

180,000

252,000

Net operating

$ 54,000

$ 60,000

Problem 5-22A (continued)

c. Whether or not the company should automate its operations depends

on how much risk the company is willing to take and on prospects for

future sales. The proposed changes would increase the company’s

fixed costs and its break-even point. However, the changes would

Problem 5-23A (60 minutes)

1. The CM ratio is 60%:

Sales price ………………….

$20.00

100%

Variable expenses ………..

8.00

40%

Contribution margin ………

$12.00

60%

2.

Fixed expenses

Dollar sales to =

break even CM ratio

$180,000

=

0.60

= $300,000

3. $75,000 increased sales × 0.60 CM ratio = $45,000 increased

4.

a.

Contribution margin

Degree of

=

operating leverage Net operating income

$240,000

=

$60,000

= 4

b. 4 × 20% = 80% increase in net operating income. In dollars, this

increase would be 80% × $60,000 = $48,000.

Problem 5-23A (continued)

5.

Last Year:

18,000 units

Proposed:

24,000 units*

Amount

Per Unit

Amount

Per Unit

Sales ………………………

$360,000

$20.00

$432,000

$18.00

**

Variable expenses ………

144,000

8.00

192,000

8.00

Contribution margin ……

216,000

$12.00

240,000

$10.00

Fixed expenses …………

180,000

210,000

Net operating income …

$ 36,000

$ 30,000

6.

Expected total contribution margin:

18,000 units × 1.25 × $11.00 per unit* ……………………

$247,500

Present total contribution margin:

18,000 units × $12.00 per unit ……………………………….

216,000

Incremental contribution margin, and the amount by

which advertising can be increased with net operating

income remaining unchanged …………………………………

$ 31,500

*$20.00 – ($8.00 + $1.00) = $11.00

Problem 5-24A (30 minutes)

1. The contribution margin per sweatshirt would be:

Selling price ………………………………………

$13.50

Variable expenses:

Purchase cost of the sweatshirts ………….

$8.00

Commission to the student salespersons .

1.50

9.50

Contribution margin …………………………….

$ 4.00

300 sweatshirts × $13.50 per sweatshirt = $4,050 in total sales

2. Since an order has been placed, there is now a “fixed” cost associated

with the purchase price of the sweatshirts (i.e., the sweatshirts can’t be

returned). For example, an order of 75 sweatshirts requires a “fixed”

cost (investment) of $600 (=75 sweatshirts × $8.00 per sweatshirt).

Selling price …………………………………..

$13.50

Variable expenses (commissions only) …

1.50

Contribution margin …………………………

$12.00

Since the “fixed” cost of $600 must be recovered before Mr. Hooper

shows any profit, the break-even computation would be:

Fixed expenses

Unit sales to =

break even Unit CM

$600

= = 50 sweatshirts

$12.00

50 sweatshirts × $13.50 per sweatshirt = $675 in total sales

Problem 5-25A (45 minutes)

1. The contribution margin per unit on the first 16,000 units is:

Per Unit

Sales price ……………………..

$3.00

Variable expenses …………….

1.25

Contribution margin ………….

$1.75

The contribution margin per unit on anything over 16,000 units is:

Per Unit

Sales price ……………………..

$3.00

Variable expenses …………….

1.40

Contribution margin ………….

$1.60

Thus, for the first 16,000 units sold, the total amount of contribution

margin generated would be:

16,000 units × $1.75 per unit = $28,000

Since the fixed costs on the first 16,000 units total $35,000, the $28,000

contribution margin above is not enough to permit the company to

break even. Therefore, in order to break even, more than 16,000 units

would have to be sold. The fixed costs that will have to be covered by

the additional sales are:

Fixed costs on the first 16,000 units …………………..

$35,000

Less contribution margin from the first 16,000 units

28,000

Remaining unrecovered fixed costs …………………….

7,000

Add monthly rental cost of the additional space

needed to produce more than 16,000 units ……….

1,000

Total fixed costs to be covered by remaining sales …

$ 8,000

Problem 5-25A (continued)

The additional sales of units required to cover these fixed costs would

be:

Total remaining fixed costs $8,000

= = 5,000 units

Unit CM on added units $1.60

Therefore, a total of 21,000 units (16,000 + 5,000) must be sold in

order for the company to break even. This number of units would equal

total sales of:

21,000 units × $3.00 per unit = $63,000 in total sales

2.

Target profit $12,000

= = 7,500 units

Unit CM $1.60

3. If a bonus of $0.10 per unit is paid for each unit sold in excess of the

break-even point, then the contribution margin on these units would

drop from $1.60 to $1.50 per unit.

Problem 5-26A (60 minutes)

1.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($30 − $18) × Q − $150,000

$0

= ($12) × Q − $150,000

$12Q

= $150,000

Q

= $150,000 ÷ $12

Q

= 12,500 pairs

12,500 pairs × $30 per pair = $375,000 in sales

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit CM

$150,000

= = 12,500 pairs

$12.00

Fixed expenses

Dollar sales to =

break even CM ratio

$150,000

= = $375,000 in sales

0.40

2. See the graph on the following page.

3. The simplest approach is:

Break-even sales ……………………

12,500 pairs

Actual sales ………………………….

12,000 pairs

Sales short of break-even ………..

500 pairs

500 pairs × $12 contribution margin per pair = $6,000 loss

Alternative solution:

Sales (12,000 pairs × $30.00 per pair) ….

$360,000

Variable expenses

(12,000 pairs × $18.00 per pair) ……….

216,000

Contribution margin ………………………….

Fixed expenses ………………………………..

Net operating loss …………………………….

Problem 5-26A (continued)

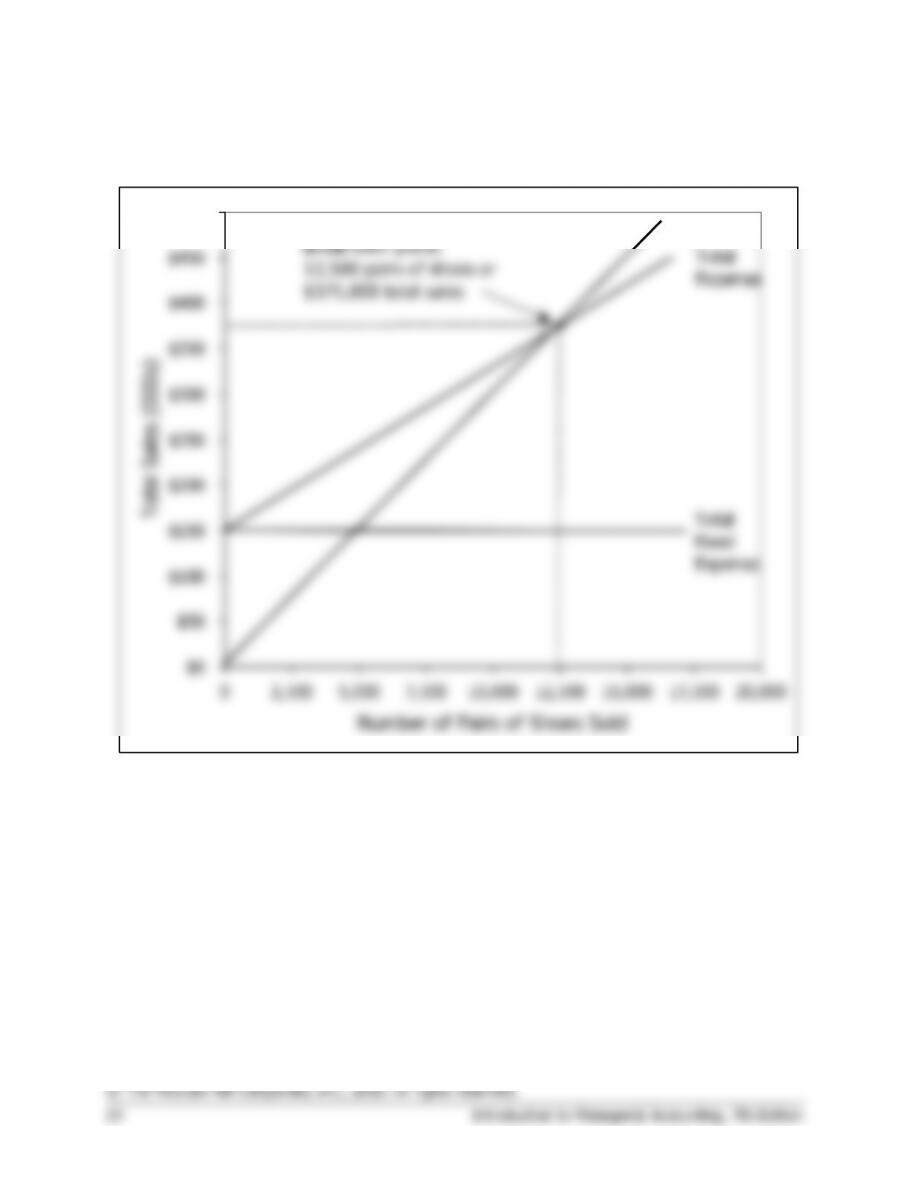

2. Cost-volume-profit graph:

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

0 2,500 5,000 7,500 10,000 12,500 15,000 17,500 20,000

Number of Pairs of Shoes Sold

Total Sales (000s)

Break-even point:

12,500 pairs of shoes or

$375,000 total sales

Total Sales

Total

Expense

Total

Fixed

Expense

Problem 5-26A (continued)

4. The variable expenses will now be $18.75 ($18.00 + $0.75) per pair,

and the contribution margin will be $11.25 ($30.00 – $18.75) per pair.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($30.00 − $18.75) × Q − $150,000

$0

= ($11.25) × Q − $150,000

$11.25Q

= $150,000

Q

= $150,000 ÷ $11.25

Q

= 13,333 pairs (rounded)

Fixed expenses

Unit sales to =

break even CM per unit

$150,000

= = 13,333 pairs

$11.25

Fixed expenses

Dollar sales to =

break even CM ratio

$150,000

= = $400,000 in sales

0.375

5. The simplest approach is:

Actual sales …………………………..

15,000 pairs

Break-even sales …………………….

12,500 pairs

Excess over break-even sales ……

2,500 pairs

2,500 pairs × $11.50 per pair* = $28,750 profit

*$12.00 present contribution margin – $0.50 commission = $11.50

Alternative solution:

Sales (15,000 pairs × $30.00 per pair) …………..

Contribution margin …………………………………..

Fixed expenses …………………………………………

150,000

Net operating income …………………………………

$ 28,750

Problem 5-26A (continued)

6. The new variable expenses will be $13.50 per pair.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($30.00 − $13.50) × Q − $181,500

$0

= ($16.50) × Q − $181,500

$16.50Q

= $181,500

Q

= $181,500 ÷ $16.50

Q

= 11,000 pairs

11,000 pairs × $30.00 per pair = $330,000 in sales

Problem 5-27A (45 minutes)

1.

a.

Hawaiian

Fantasy

Tahitian

Joy

Total

Amount

%

Amount

%

Amount

%

Sales ……………………..

$300,000

100%

$500,000

100%

$800,000

100%

Variable expenses …….

180,000

60%

100,000

20%

280,000

35%

Contribution margin ….

$120,000

40%

$400,000

80%

520,000

65%

Fixed expenses ………..

475,800

Net operating income ..

$ 44,200

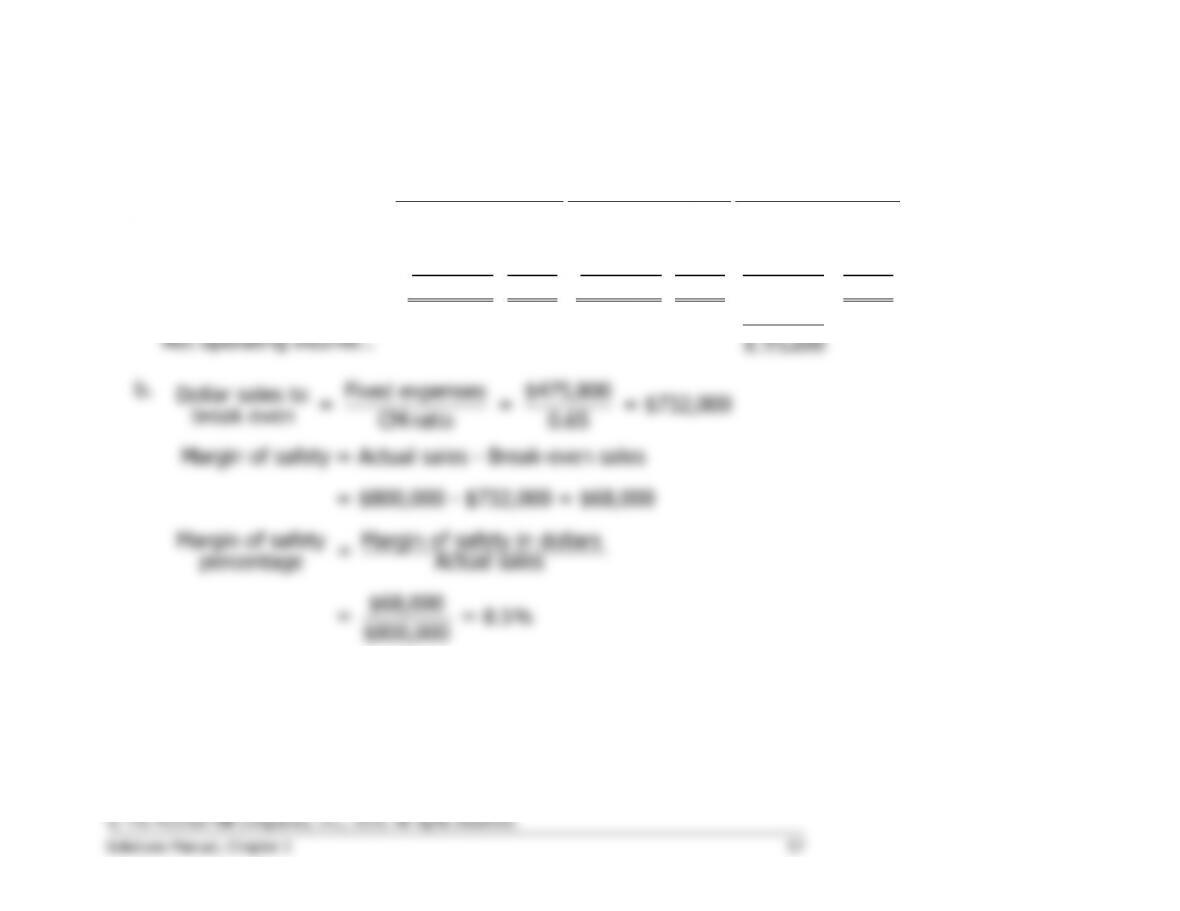

b.

Fixed expenses $475,800

Dollar sales to = = = $732,000

break even CM ratio 0.65

Margin of safety = Actual sales – Break-even sales

= $800,000 – $732,000 = $68,000

Margin of safety Margin of safety in dollars

=

percentage Actual sales

$68,000

= = 8.5%

$800,000

Problem 5-27A (continued)

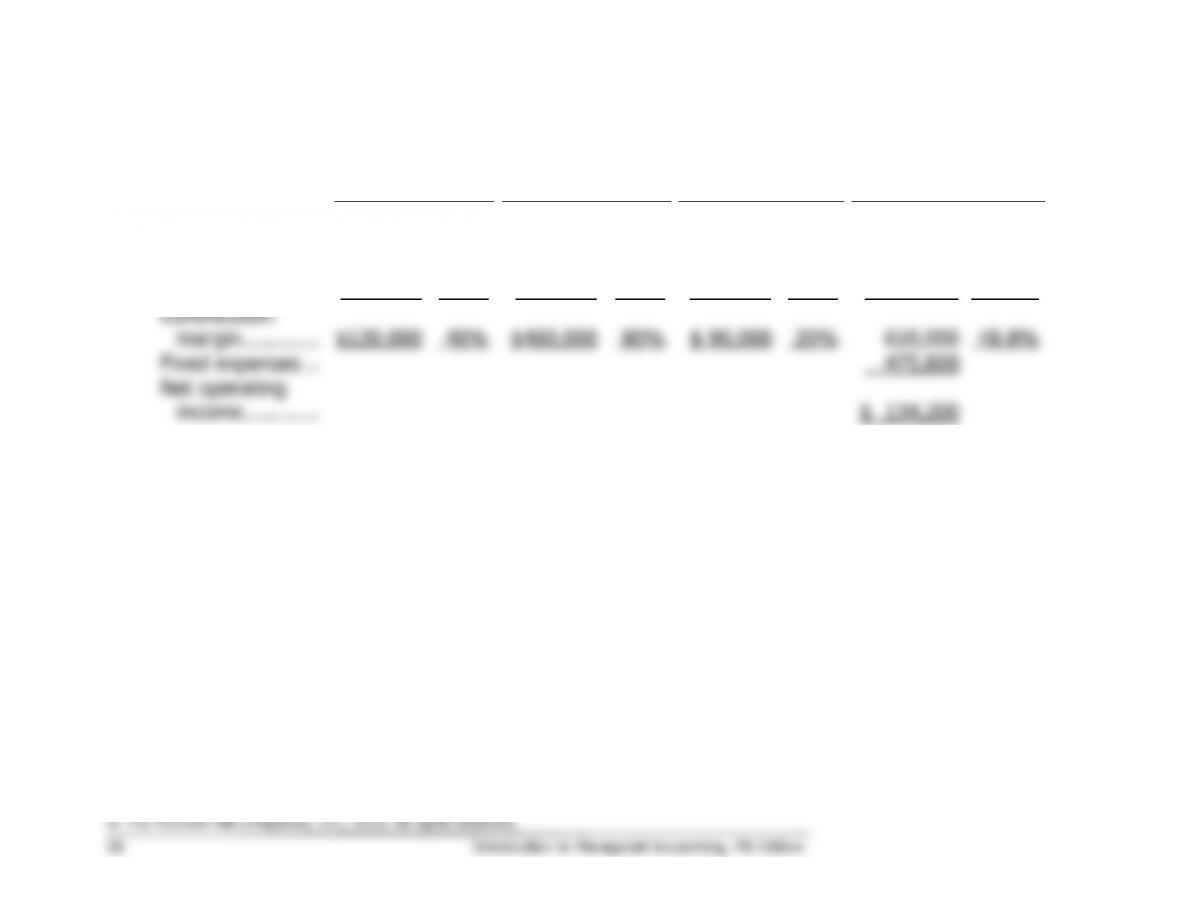

2.

a.

Hawaiian

Fantasy

Tahitian

Joy

Samoan

Delight

Total

Amount

%

Amount

%

Amount

%

Amount

%

Sales ……………..

$300,000

100%

$500,000

100%

$450,000

100%

$1,250,000

100.0%

Variable

expenses ………

180,000

60%

100,000

20%

360,000

80%

640,000

51.2%

Contribution

margin …………

$120,000

40%

$400,000

80%

$ 90,000

20%

610,000

48.8%

Fixed expenses ..

475,800

Net operating

income …………

$ 134,200

Problem 5-27A (continued)

b.

Fixed expenses $475,800

Dollar sales to = = = $975,000

break even CM ratio 0.488

Margin of safety = Actual sales – Break-even sales

= $1,250,000 – $975,000 = $275,000

Margin of safety Margin of safety in dollars

=

percentage Actual sales

$275,000

= = 22%

$1,250,000

3. The reason for the increase in the break-even point can be traced to the

decrease in the company’s overall contribution margin ratio when the

third product is added. Note from the income statements above that this

ratio drops from 65% to 48.8% with the addition of the third product.

Problem 5-28A (60 minutes)

1.

Carbex, Inc.

Income Statement For April

Standard

Deluxe

Total

Amount

%

Amount

%

Amount

%

Sales ……………………….

$240,000

100

$150,000

100

$390,000

100.0

Variable expenses:

Production ……………..

60,000

25

60,000

40

120,000

30.8

Sales commission …….

36,000

15

22,500

15

58,500

15.0

Total variable expenses .

96,000

40

82,500

55

178,500

45.8

Contribution margin ……

$144,000

60

$ 67,500

45

$211,500

54.2

Fixed expenses:

Advertising …………….

105,000

Depreciation …………..

21,700

Administrative …………

63,000

Total fixed expenses ……

189,700

Net operating income ….

$ 21,800

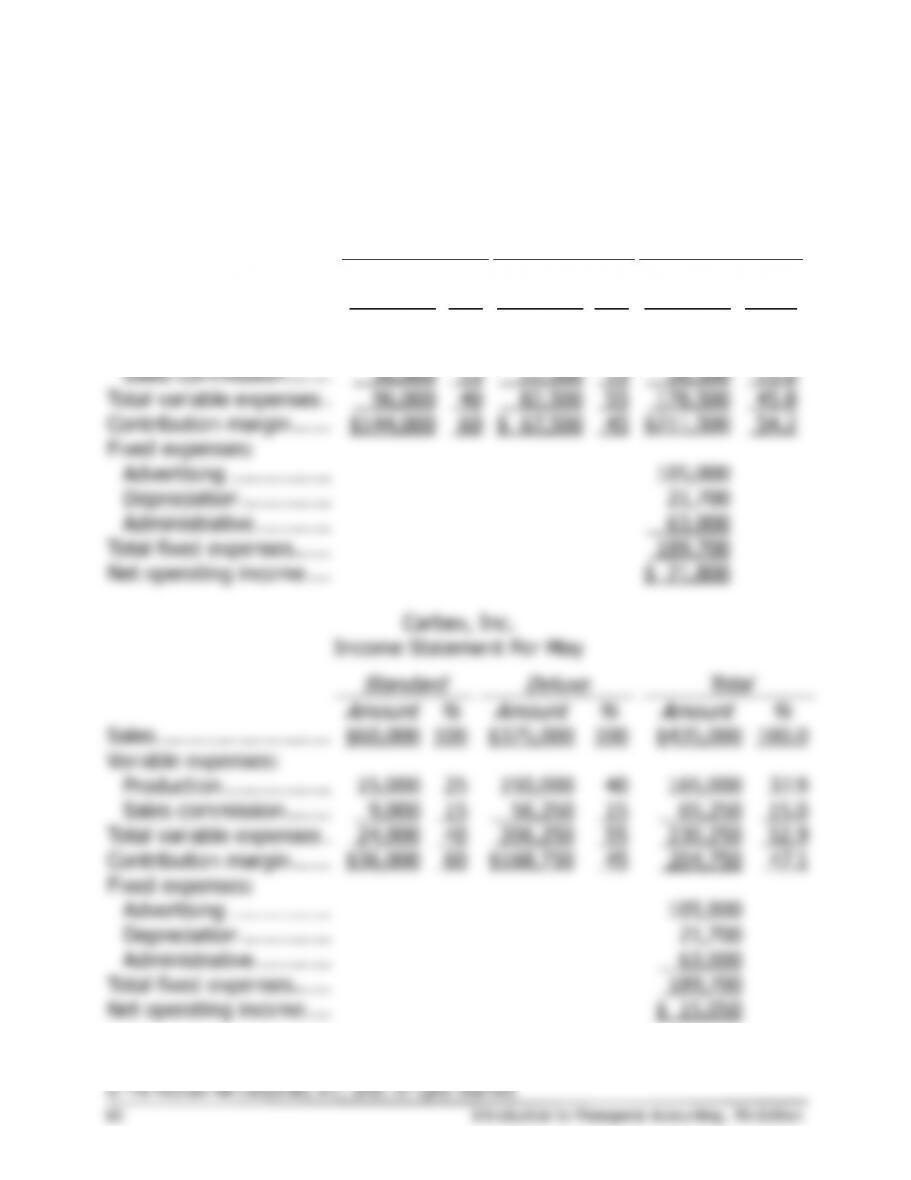

Carbex, Inc.

Income Statement For May

Standard

Deluxe

Total

Amount

%

Amount

%

Amount

%

Sales ……………………….

$60,000

100

$375,000

100

$435,000

100.0

Variable expenses:

Production ……………..

15,000

25

150,000

40

165,000

37.9

Sales commission …….

9,000

15

56,250

15

65,250

15.0

Total variable expenses .

24,000

40

206,250

55

230,250

52.9

Contribution margin ……

$36,000

60

$168,750

45

204,750

47.1

Fixed expenses:

Advertising …………….

105,000

Depreciation …………..

21,700

Administrative …………

63,000

Total fixed expenses ……

189,700

Net operating income ….

$ 15,050