Problem 12-7B (30 minutes)

1. Net cash provided by operating activities:

Step 1: The following equation can be applied to the Accumulated

Depreciation account to compute the depreciation to add back to net

income:

Beginning balance – Debits + Credits = Ending balance

$71 – $10 + Credits = $85

income.

Problem 12-7B (continued)

The net cash provided by operating activities is computed as follows:

Net income …………………………………………………

$ 65

Adjustments to convert net income to cash basis:

Depreciation …………………………………………..

24

Increase in accounts receivable …………………..

(77)

Decrease in inventory ……………………………….

38

Increase in prepaid expenses ……………………..

(2)

Increase in accounts payable ……………………..

76

Decrease in accrued liabilities …………………….

(10)

Increase in income taxes payable ………………..

9

Gain on sale of investments ……………………….

(6)

Loss on sale of equipment …………………………

2

54

Net cash provided by operating activities …………..

$119

2. Prepare a statement of cash flows.

Investing and Financing activities:

The guidelines from Exhibit 12-3 can be used to analyze the changes in

Problem 12-7B (continued)

The decrease in the long-term investments account ($7) equals the cost

of the long-term investment sold; therefore, the company did not

purchase any long-term investments during the year. The proceeds from

the sale of a long-term investment ($13) should be recorded as a cash

Problem 12-7B (continued)

Groton Company

Statement of Cash Flows

For the Year Ended December 31, 2011

Operating activities:

Net income ………………………………………………….

$ 65

Adjustments to convert net income to cash basis:

Depreciation ……………………………………………

$ 24

Increase in accounts receivable …………………..

(77)

Decrease in inventory ……………………………….

38

Increase in prepaid expenses ……………………..

(2)

Increase in accounts payable ………………………

76

Decrease in accrued liabilities ……………………..

(10)

Increase in income taxes payable ………………..

9

Gain on sale of investments ……………………….

(6)

Loss on sale of equipment ………………………….

2

54

Net cash provided by operating activities …………..

119

Investing activities:

Proceeds from sale of long-term investments ……..

13

Proceeds from sale of equipment ……………………..

19

Additions to plant and equipment …………………….

(110)

Net cash used in investing activities ………………….

(78)

Financing activities:

Issuance of bonds payable ……………………………..

26

Decrease in common stock ……………………………..

(39)

Cash dividends …………………………………………….

(39)

Net cash used in financing activities ………………….

(52)

Net decrease in cash ……………………………………..

(11)

Cash balance, January 1, 2011 ………………………..

12

Cash balance, December 31, 2011 ……………………

$ 1

Problem 12-8B (45 minutes)

1. Net cash provided by operating activities:

Step 1: The following equation can be applied to the Accumulated

Depreciation account to compute the depreciation to add back to net

income:

Beginning balance – Debits + Credits = Ending balance

$130,900 – $11,100 + Credits = $166,300

income.

Problem 12-8B (continued)

The net cash provided by operating activities is computed as follows:

Net income …………………………..………………………

$114,000

Adjustments to convert net income to cash basis:

Depreciation ……………………………………………….

$ 46,500

Increase in accounts receivable ………………………

(157,000)

Increase in inventory ……………………………………

(45,000)

Decrease in prepaid expenses …………………………

8,500

Increase in accounts payable ………………………….

65,000

Decrease in accrued liabilities …………………………

(7,000)

Increase in income taxes payable ……………………

3,900

Gain on sale of equipment ……………………………..

(6,000)

(91,100)

Net cash provided by operating activities …………….

$22,900

2. Prepare a statement of cash flows.

Investing and Financing activities:

The guidelines from Exhibit 12-3 can be used to analyze the changes in

noncash balance sheet accounts that impact investing and financing

Problem 12-8B (continued)

The loan to Puffington ($44,000) is recorded as a cash outflow in the

investing activities section of the statement. Because Pillsberry did not

retire any bonds during the year, the corresponding amount in the table

on the prior page (+101,000) represents a cash inflow pertaining to a

© The McGraw-Hill Companies, Inc., 2002. All rights reserved.

12-8 Introduction to Managerial Accounting, 1st Edition

Problem 12-8B (continued)

Pillsberry Company

Statement of Cash Flows

For Year 2

Operating activities:

Net income ……………………………………………….

$114,000

Adjustments to convert net income to cash basis:

Depreciation ……………………………………………

$ 46,500

Increase in accounts receivable …………………..

(157,000)

Increase in inventory ………………………………..

(45,000)

Decrease in prepaid expenses …………………….

8,500

Increase in accounts payable ………………………

65,000

Decrease in accrued liabilities ……………………..

(7,000)

Increase in income taxes payable ………………..

3,900

Gain on sale of equipment …………………………

(6,000)

(91,100)

Net cash provided by operating activities …………

22,900

Investing activities:

Proceeds from sale of equipment …………………..

26,200

Loan to Puffington Company …………………………

(44,000)

Additions to plant and equipment …………………..

(160,300)

Net cash used in investing activities ……………….

(178,100)

Financing activities:

Issuance of bonds payable …………………………...

101,000

Issuance of common stock…………………………...

46,000

Cash dividends …………………………………………..

(32,900)

Net cash provided by financing activities ………….

114,100

Net decrease in cash …………………………………..

(41,100)

Cash balance, beginning of year …………………….

88,500

Cash balance, end of year …………………………...

$ 47,400

Problem 12-8B (continued)

3. Free cash flow computation:

Net cash provided by operating activities ……………..

$ 22,900

Capital expenditures ……………………………………..

$160,300

Dividends ……………………………………………………

32,900

193,200

Free cash flow ………………………………………………..

$(170,300)

4. The relatively small amount of net cash provided by operating activities

during the year was largely the result of a large increase in accounts

© The McGraw-Hill Companies, Inc., 2013. All rights reserved.

12–10 Introduction to Managerial Accounting, 1st Edition

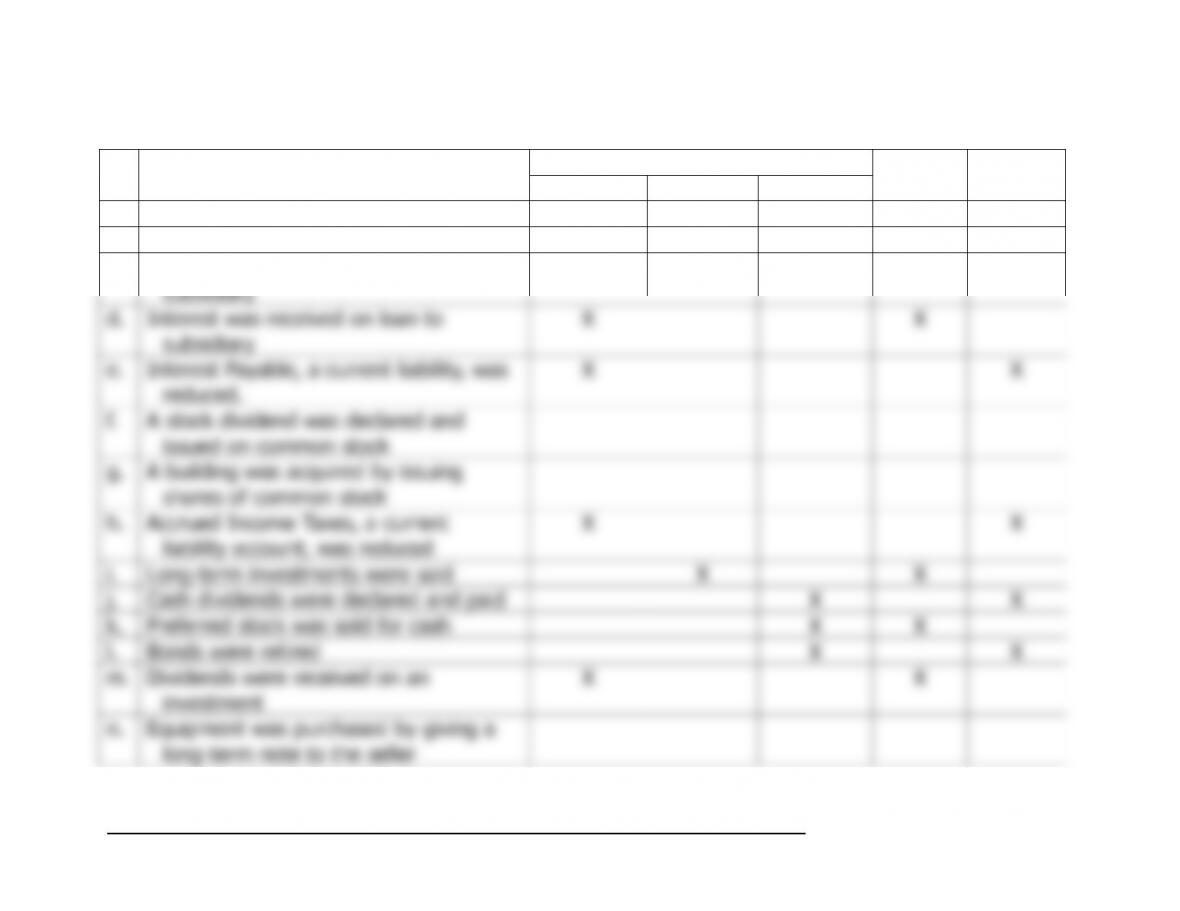

Problem 12-9B (30 minutes)

Activity

Cash

Cash

Transaction

Operating

Investing

Financing

Inflow

Outflow

a.

Common stock was sold for cash

X

X

b.

Equipment was sold for cash

X

X

c.

A long-term loan was made to a

subsidiary

X

X

d.

Interest was received on loan to

subsidiary

X

X

e.

Interest Payable, a current liability, was

reduced.

X

X

f.

A stock dividend was declared and

issued on common stock

g.

A building was acquired by issuing

shares of common stock

h.

Accrued Income Taxes, a current

liability account, was reduced

X

X

i.

Long-term investments were sold

X

X

j.

Cash dividends were declared and paid

X

X

k.

Preferred stock was sold for cash

X

X

l.

Bonds were retired

X

X

m.

Dividends were received on an

investment

X

X

n.

Equipment was purchased by giving a

long-term note to the seller

Problem 12-10B (45 minutes)

1 Prepare a statement of cash flows (all numbers in millions).

Operating activities:

Step 1: The following equation can be applied to the Accumulated

Depreciation account to compute the depreciation to add back to net

income:

income.

© The McGraw-Hill Companies, Inc., 2013. All rights reserved.

12–12 Introduction to Managerial Accounting, 1st Edition

Problem 12-10B (continued)

As an intermediate step, the net cash provided by operating activities

can now be calculated as follows:

Net income ……………………………………………….

$206

Adjustments to convert net income to cash basis:

Depreciation ……………………………………………

$150

Increase in accounts receivable …………………..

(58)

Increase in inventory ………………………………..

(46)

Increase in accounts payable ………………………

106

Increase in accrued liabilities ………………………

22

Increase in income taxes payable ………………..

11

Gain on sale of equipment …………………………

(2)

183

Net cash provided by operating activities …………

$389

Investing and Financing activities:

The guidelines from Exhibit 12-3 can be used to analyze the changes in

noncash balance sheet accounts that impact investing and financing

cash flows as follows:

Increase

in Account

Balance

Decrease

in Account

Balance

Noncurrent Assets

Property, plant, and equipment ………………

– 27

Liabilities and Stockholders’ Equity

Bonds payable ……………………………………

– 215

Problem 12-10B (continued)

Kars did not issue any bonds during the year; therefore, the amount in

the table on the prior page (–215) represents a cash outflow pertaining

to a bond retirement. Property, plant, and equipment and retained

earnings require further analysis as follows:

© The McGraw-Hill Companies, Inc., 2013. All rights reserved.

12–14 Introduction to Managerial Accounting, 1st Edition

Problem 12-10B (continued)

Kars Company

Statement of Cash Flows

Operating activities:

Net income ……………………………………………….

$ 206

Adjustments to convert net income to cash basis:

Depreciation ……………………………………………

$150

Increase in accounts receivable …………………..

(58)

Increase in inventory ………………………………..

(46)

Increase in accounts payable ………………………

106

Increase in accrued liabilities ………………………

22

Increase in income taxes payable ………………..

11

Gain on sale of equipment …………………………

(2)

183

Net cash provided by operating activities …………

389

Investing activities:

Proceeds from sale of equipment …………………..

13

Additions to plant and equipment …………………..

(51)

Net cash used in investing activities ……………….

(38)

Financing activities:

Retirement of bonds payable ………………………..

(215)

Cash dividends …………………………………………..

(184)

Net cash used in financing activities ……………….

(399)

Net decrease in cash …………………………………..

(48)

Cash balance, beginning of year …………………….

93

Cash balance, end of year …………………………...

$ 45

Problem 12-10B (continued)

2. Kars’ net income decreased by $16 million (= $206 million – $190

million); however, its net cash provided by operating activities increased

by $229 million (= $389 million – $160 million) over the prior year.

When net income and net cash provided by operating activities move in

opposite directions, it warrants further inquiry. It appears that Kars has