Case (continued)

2. The spending variances are computed as follows:

The Little Theatre

Spending Variances

For the Year Ended December 31

Actual

Results

Spending

Variances

Flexible

Budget

Number of productions (q1) ……..

7

7

Number of performances (q2) …..

168

168

Actors’ and directors’ wages

($2,000q2) ………………………….

$341,800

$5,800

U

$336,000

Stagehands’ wages ($300q2) …….

49,700

700

F

50,400

Ticket booth personnel and

ushers’ wages ($150q2) …………

25,900

700

U

25,200

Scenery, costumes, and props

($18,000q1) ………………………..

130,600

4,600

U

126,000

Theater hall rent ($500q2) ……….

78,000

6,000

F

84,000

Printed programs ($250q2) ……….

38,300

3,700

F

42,000

Publicity ($2,000q1) ………………..

15,100

1,100

U

14,000

Administrative expenses

($32,400 + $1,080q1 +$40q2) ..

47,500

820

U

46,680

Total expense ……………………….

$726,900

$2,620

U

$724,280

Case (continued)

3. The overall unfavorable spending variance is a very small percentage of

the total cost, less than 0.4%. This suggests that costs are under

control. In addition, the pattern of the variances may reflect good

4. Average costs may not be very good indicators of the additional costs of

any particular production or performance. The averages gloss over

considerable variations in costs. For example, a production of Peter

Rabbit may require only half a dozen actors and actresses and fairly

Chapter 8

Take Two Solutions

Exercise 8-1 (10 minutes)

Puget Sound Divers

Flexible Budget

For the Month Ended May 31

Actual diving-hours ……………………………….

110

Revenue ($365.00q) ……………………………..

$40,150

Expenses:

Wages and salaries ($8,000 + $125.00q) …

21,750

Supplies ($3.00q) ……………………………….

330

Equipment rental ($1,800 + $32.00q) …….

5,320

Insurance ($3,400) ……………………………..

3,400

Miscellaneous ($630 + $1.80q) ……………..

828

Total expense ………………………………………

31,628

Net operating income …………………………….

$ 8,522

Exercise 8-2 (15 minutes)

Quilcene Oysteria

Revenue and Spending Variances

For the Month Ended August 31

Actual

Results

Flexible

Budget

Revenue

and

Spending

Variances

Pounds …………………………………

8,000

8,000

Revenue ($4.00q) ……………………

$30,000

$32,000

$2,000

U

Expenses:

Packing supplies ($0.50q) ……….

4,200

4,000

200

U

Oyster bed maintenance

($3,200) …………………………..

3,100

3,200

100

F

Wages and salaries ($2,900 +

$0.30q) …………………………….

5,640

5,300

340

U

Shipping ($0.80q) …………………

6,950

6,400

550

U

Utilities ($830) ……………………..

810

830

20

F

Other ($450 + $0.05q) …………..

980

850

130

U

Total expense …………………………

21,680

20,580

1,100

U

Net operating income ………………

$8,320

$11,420

$3,100

U

Exercise 8-3 (15 minutes)

Alyeski Tours

Planning Budget

For the Month Ended July 31

Budgeted cruises (q1) ………………………………………………….

24

Budgeted passengers (q2) ……………………………………………

1,500

Revenue ($25.00q2) ……………………………………………………

$37,500

Expenses:

Vessel operating costs ($5,200 + $480.00q1 +$2.00q2) ……

19,720

Advertising ($1,700) …………………………………………………

1,700

Administrative costs ($4,300 + $24.00q1 +$1.00q2) ………..

6,376

Insurance ($2,900) …………………………………………………..

2,900

Total expense ……………………………………………………………

30,696

Net operating income ………………………………………………….

$ 6,804

Exercise 8-4 (20 minutes)

1.

Number of helmets …………………………………….

35,000

Standard kilograms of plastic per helmet …………

× 0.75

Total standard kilograms allowed …………………..

26,250

Standard cost per kilogram …………………………..

× $8

Total standard cost …………………………………….

$210,000

Actual cost incurred (given) ………………………….

$171,000

Total standard cost (above) ………………………….

210,000

Total material variance—favorable …………………

$ 39,000

2.

Actual Quantity

of Input, at

Actual Price

Actual Quantity of Input,

at Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

22,500 kilograms ×

26,250 kilograms* ×

$8 per kilogram

$8 per kilogram

$171,000

= $180,000

= $210,000

Price Variance =

$9,000 F

Quantity Variance =

$30,000 F

Spending Variance = $39,000 F

*35,000 helmets × 0.75 kilograms per helmet = 26,250 kilograms

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

22,500 kilograms ($7.60 per kilogram* – $8.00 per kilogram)

= $9,000 F

* $171,000 ÷ 22,500 kilograms = $7.60 per kilogram

Materials quantity variance = SP (AQ – SQ)

$8 per kilogram (22,500 kilograms – 26,250 kilograms)

= $30,000 F

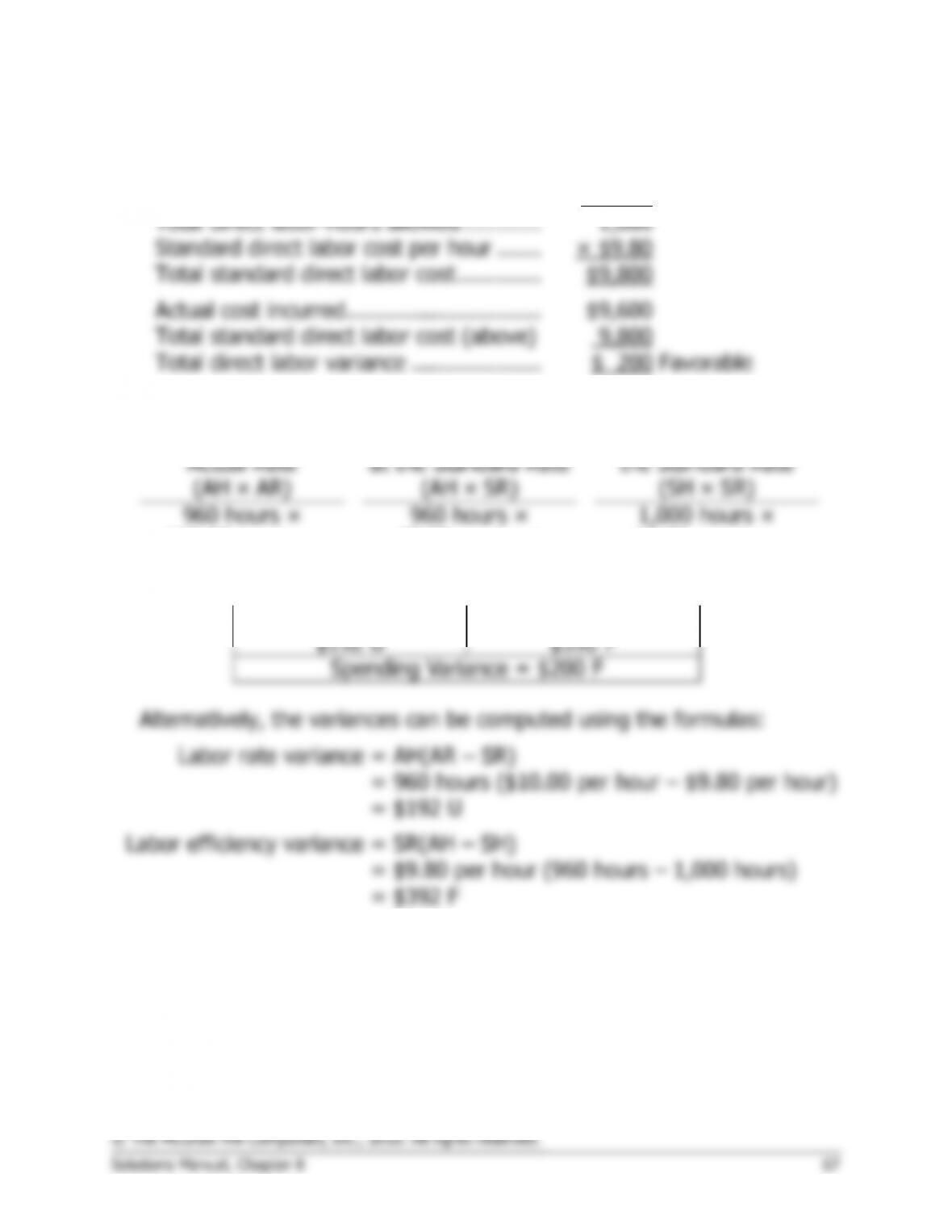

Exercise 8-5 (20 minutes)

1.

Number of meals prepared ……………….

4,000

Standard direct labor-hours per meal ….

× 0.25

Total direct labor-hours allowed …………

1,000

Standard direct labor cost per hour …….

× $9.80

Total standard direct labor cost ………….

$9,800

Actual cost incurred …………………………

$9,600

Total standard direct labor cost (above)

9,800

Total direct labor variance ………………..

$ 200

Favorable

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

960 hours ×

$10.00 per hour

960 hours ×

$9.80 per hour

1,000 hours ×

$9.80 per hour

= $9,600

= $9,408

= $9,800

Rate Variance =

$192 U

Efficiency Variance =

$392 F

Spending Variance = $200 F

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH(AR – SR)

= 960 hours ($10.00 per hour – $9.80 per hour)

= $192 U

Labor efficiency variance = SR(AH – SH)

= $9.80 per hour (960 hours – 1,000 hours)

= $392 F

Exercise 8-7 (15 minutes)

Lavage Rapide

Planning Budget

For the Month Ended August 31

Budgeted cars washed (q) ………………………..

8,200

Revenue ($4.90q) …………………………………..

$40,180

Expenses:

Cleaning supplies ($0.80q) ……………………..

6,560

Electricity ($1,200 + $0.15q) ………………….

2,430

Maintenance ($0.20q)…………………………...

1,640

Wages and salaries ($5,000 + $0.30q) ……..

7,460

Depreciation ($6,000) …………………………...

6,000

Rent ($8,000) ……………………………………..

8,000

Administrative expenses ($4,000 + $0.10q) .

4,820

Total expense ………………………………………..

36,910

Net operating income ………………………………

$ 3,270

Appendix 8A

Predetermined Overhead Rates and

Overhead Analysis in a Standard Costing

System

Exercise 8A-1 (15 minutes)

1.

Fixed overhead

Fixed portion of the =

predetermined overhead rate Denominator level of activity

$250,000

= 25,000 DLHs

= $10.00 per DLH

2.

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $254,000 – $250,000

= $4,000 U

( )

Fixed portion of

Volume Denominator Standard hours

= the predetermined × –

variance hours allowed

overhead rate

= $10.00 per DLH × (25,000 DLHs – 26,000 DLHs)

= $10,000 F

Exercise 8A–2 (20 minutes)

1.

$3 per MH × 60,000 MHs + $300,000

Predetermined =

overhead rate 60,000 MHs

$480,000

= 60,000 MHs

= $8 per MH

Variable portion of $3 per MH × 60,000 MHs

the predetermined = 60,000 MHs

overhead rate

$180,000

= 60,000 MHs

= $3 per MH

Fixed portion of $300,000

the predetermined = 60,000 MHs

overhead rate

= $5 per MH

2. The standard hours per unit of product are:

Exercise 8A–2 (continued)

3. Variable overhead rate variance:

Variable overhead rate variance = (AH × AR) – (AH × SR)

($185,600) – (64,000 hours × $3 per hour) = $6,400 F

Variable overhead efficiency variance:

Variable overhead efficiency variance = SR (AH – SH)

= $15,000 F

Exercise 8A-3 (15 minutes)

1. The total overhead cost at the denominator level of activity must be

determined before the predetermined overhead rate can be computed.

Total fixed overhead cost per year …………………………...

$250,000

Total variable overhead cost

($2 per DLH × 40,000 DLHs) ………………………………..

80,000

Total overhead cost at the denominator level of activity ..

$330,000

$330,000

= = $8.25 per DLH

40,000 DLHs

2.

Standard direct labor-hours allowed for

the actual output (a) ………………………

38,000

DLHs

Predetermined overhead rate (b) ………..

$8.25

per DLH

Overhead applied (a) × (b) ………………..

$313,500

Exercise 8A–4 (10 minutes)

Company A:

This company has a favorable volume variance because the

standard hours allowed for the actual production are greater

than the denominator hours.

Company B:

This company has an unfavorable volume variance because

the standard hours allowed for the actual production are less

than the denominator hours.

Company C:

This company has no volume variance because the standard

hours allowed for the actual production and the denominator

hours are the same.

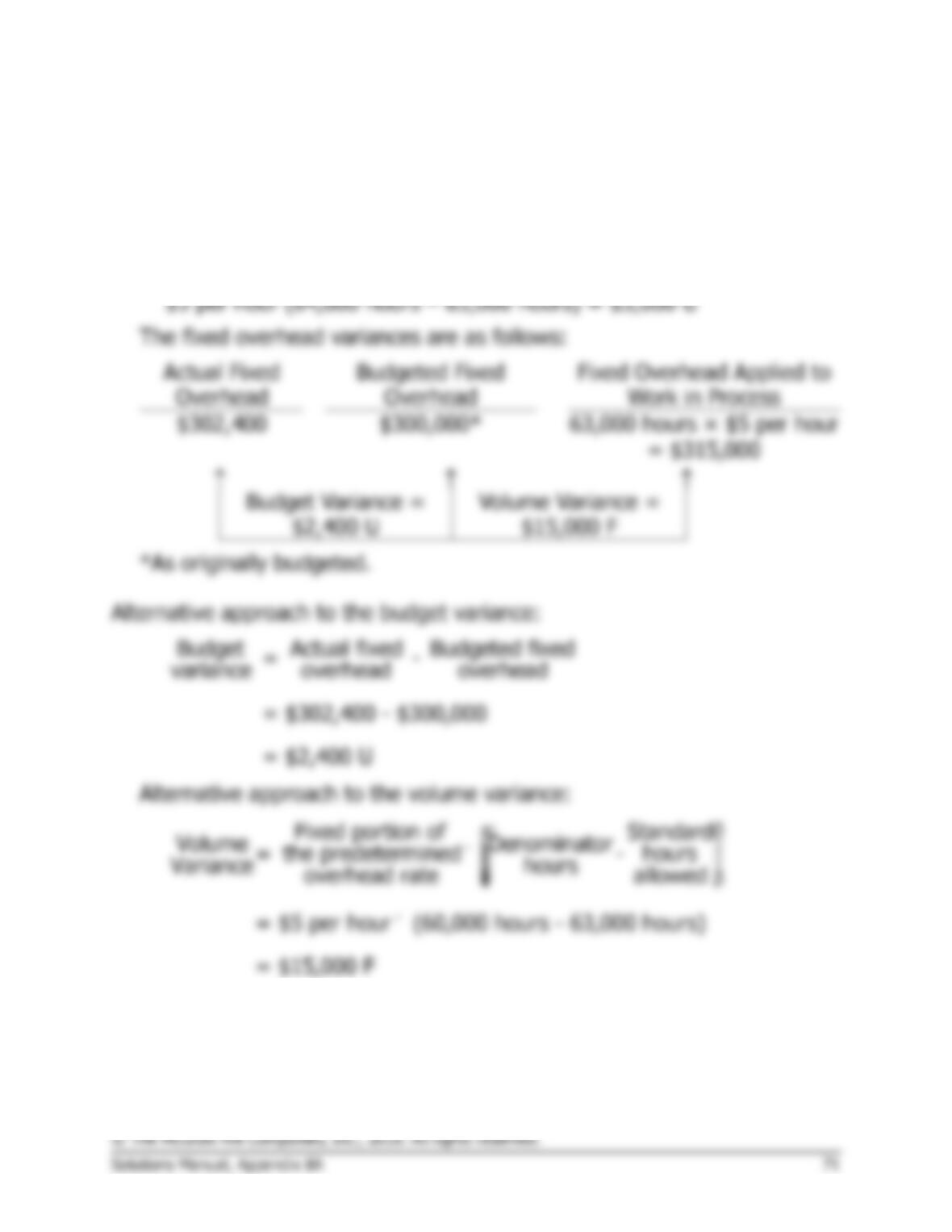

Exercise 8A–5 (15 minutes)

1. 9,500 units × 4 hours per unit = 38,000 hours.

2. and 3.

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead Applied to

Work in Process

$198,700*

$200,000

38,000 hours × $5 per hour*

= $190,000

Budget Variance =

$1,300 F

Volume Variance =

$10,000 U*

*Given.

4.

$200,000

= Denominator activity

= $5 per hour

Budgeted fixed overhead

Fixed element of the =

predetermined overhead rate Denominator activity

Therefore, the denominator activity is: $200,000 ÷ $5 per hour =

40,000 hours.

Exercise 8A-6 (15 minutes)

1.

Total overhead at the

denominator activity

Predetermined =

overhead rate Denominator activity

$1.90 per DLH × 30,000 per DLH + $168,000

= 30,000 DLHs

$225,000

= 30,000 DLHs

= $7.50 per DLH

2.

Direct materials, 2.5 yards × $8.60 per yard ………………….

$21.50

Direct labor, 3 DLHs* × $12.00 per DLH ……………………….

36.00

Variable manufacturing overhead, 3 DLHs × $1.90 per DLH

5.70

Fixed manufacturing overhead, 3 DLHs × $5.60 per DLH ….

16.80

Total standard cost per unit …………………………..…………..

$80.00

*30,000 DLHs ÷ 10,000 units = 3 DLHs per unit

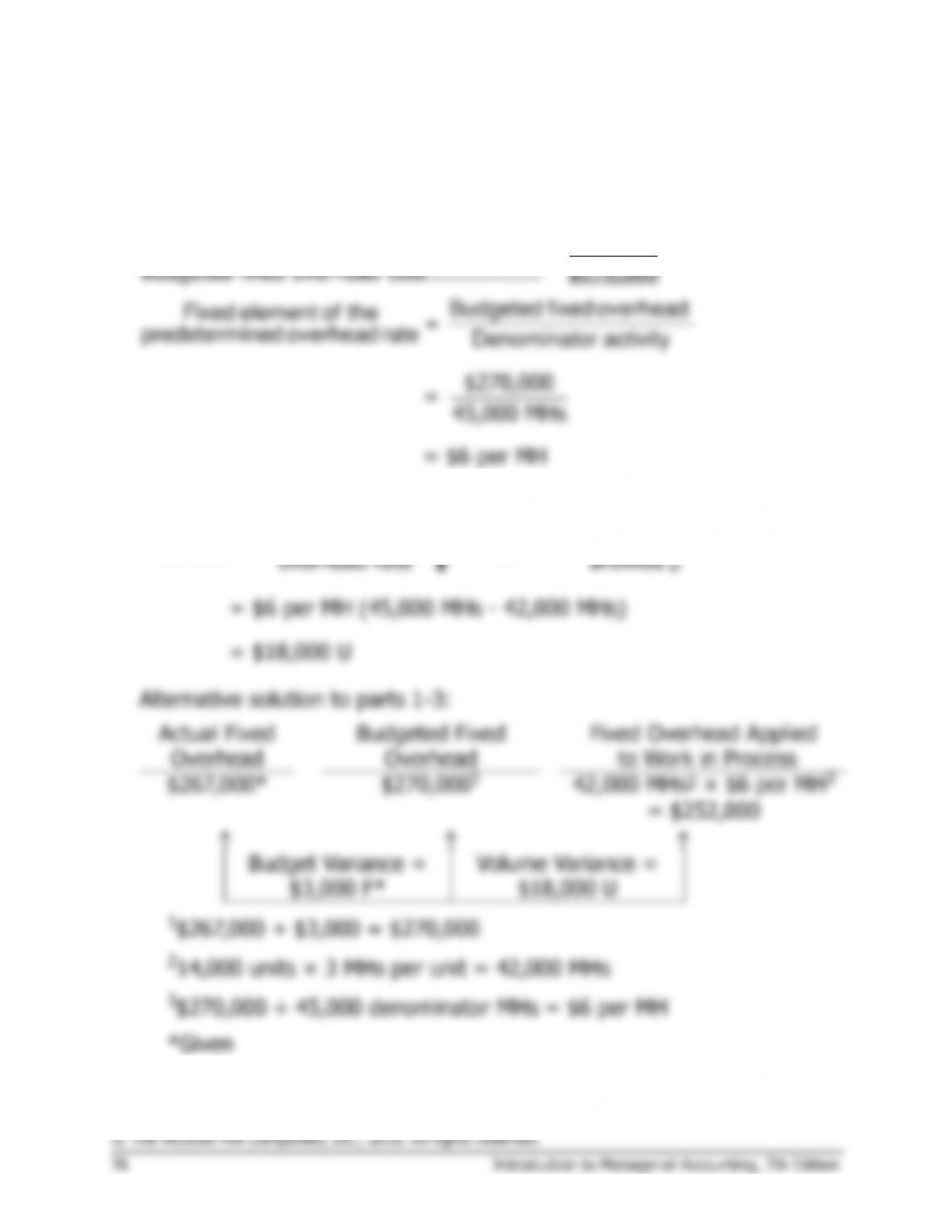

Exercise 8A–7 (15 minutes)

1. 14,000 units produced × 3 MHs per unit = 42,000 MHs

2.

Actual fixed overhead incurred …………….

$267,000

Add: Favorable budget variance …………..

3,000

Budgeted fixed overhead cost ……………..

$270,000

$270,000

= 45,000 MHs

= $6 per MH

Budgeted fixed overhead

Fixed element of the =

predetermined overhead rate Denominator activity

3.

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $6 per MH (45,000 MHs – 42,000 MHs)

= $18,000 U

æö

÷

ç÷

ç÷

ç÷

ç÷

ç

èø

Alternative solution to parts 1-3:

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead Applied

to Work in Process

$267,000*

$270,0001

42,000 MHs2 × $6 per MH3

= $252,000

Budget Variance =

$3,000 F*

Volume Variance =

$18,000 U

1$267,000 + $3,000 = $270,000

214,000 units × 3 MHs per unit = 42,000 MHs

3$270,000 ÷ 45,000 denominator MHs = $6 per MH

*Given

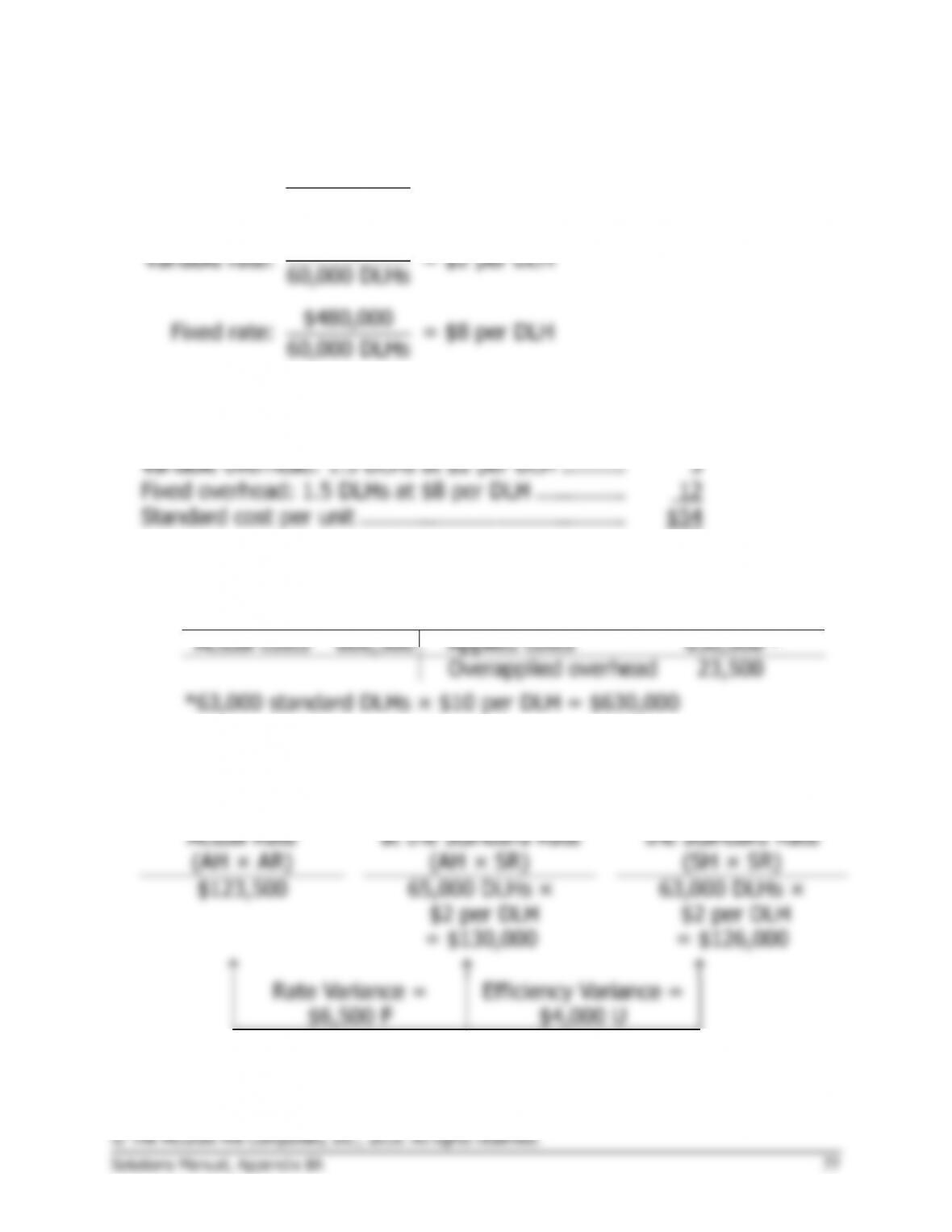

Problem 8A-8A (45 minutes)

1.

$600,000

Total rate: = $10 per DLH

60,000 DLHs

$120,000

Variable rate: = $2 per DLH

60,000 DLHs

$480,000

Fixed rate: = $8 per DLH

60,000 DLHs

2.

Direct materials: 3 pounds at $7 per pound ……….

$21

Direct labor: 1.5 DLHs at $12 per DLH ………………

18

Variable overhead: 1.5 DLHs at $2 per DLH ……….

3

Fixed overhead: 1.5 DLHs at $8 per DLH …………..

12

Standard cost per unit …………………………………..

$54

3. a. 42,000 units × 1.5 DLHs per unit = 63,000 standard DLHs.

b.

Manufacturing Overhead

Actual costs

606,500

Applied costs

630,000

*

Overapplied overhead

23,500

*63,000 standard DLHs × $10 per DLH = $630,000

4. Variable overhead variances:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$123,500

65,000 DLHs ×

$2 per DLH

63,000 DLHs ×

$2 per DLH

= $130,000

= $126,000

Rate Variance =

$6,500 F

Efficiency Variance =

$4,000 U

Problem 8A-8A (continued)

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

($123,500) – (65,000 DLHs × $2 per DLH) = $6,500 F

Variable overhead efficiency variance = SR (AH – SH)

= $24,000 F

Problem 8A–8A (continued)

The company’s overhead variances can be summarized as follows:

Variable overhead:

Rate variance …………………………...

$ 6,500

F

Efficiency variance ……………………..

4,000

U

Fixed overhead:

Budget variance ………………………..

3,000

U

Volume variance ………………………..

24,000

F

Overapplied overhead—see part 3 …..

$23,500

F

5. Only the volume variance would have changed. It would have been

Problem 8A–9A (45 minutes)

1.

$297,500

Total rate: = $8.50 per hour

35,000 hours

$87,500

Variable rate: = $2.50 per hour

35,000 hours

$210,000

Fixed rate: = $6.00 per hour

35,000 hours

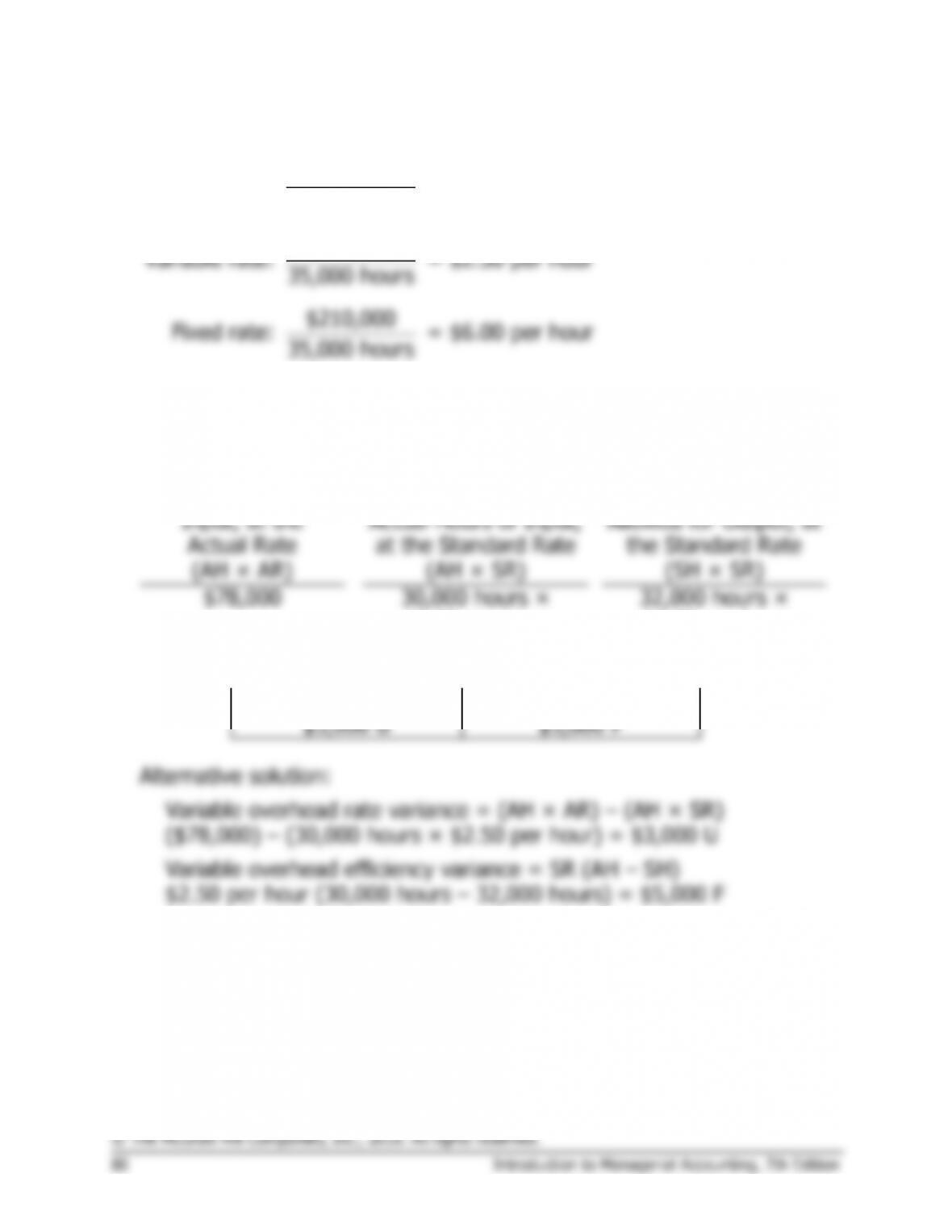

2. 32,000 standard hours × $8.50 per hour = $272,000.

3. Variable overhead variances:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$78,000

30,000 hours ×

$2.50 per hour

32,000 hours ×

$2.50 per hour

= $75,000

= $80,000

Rate Variance =

$3,000 U

Efficiency Variance =

$5,000 F

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

($78,000) – (30,000 hours × $2.50 per hour) = $3,000 U

Variable overhead efficiency variance = SR (AH – SH)

$2.50 per hour (30,000 hours – 32,000 hours) = $5,000 F