Chapter 8

Flexible Budgets, Standard Costs, and

Variance Analysis

Solutions to Questions

8-1 The planning budget is prepared for the

planned level of activity. It is static because it is

8-2 A flexible budget can be adjusted to

reflect any level of activity—including the actual

8-3 Actual results can differ from the budget

for many reasons. Very broadly speaking, the

8-4 From a manager’s perspective,

differences between the planning budget and

actual results that are due to a change in

activity are very different from variances that are

8-5 A revenue variance is the difference

between how much the revenue should have

because the revenue is less than expected for

the actual level of activity.

given the actual level of activity, and the actual

amount of the cost. Like the revenue variance,

spending variance occurs because the cost is

higher than expected for the actual level of

happened at the actual level of activity to what

actually happened. A planning budget does not

enable these comparisons because it is based on

the planned level of activity rather than the

may be a function of the second cost driver, and

some costs may be a function of both cost

8-10 Separating a spending variance into a

price variance and a quantity variance provides

8-11 The materials price variance is usually

the responsibility of the purchasing manager.

8-12 The materials price variance can be

computed either when materials are purchased

or when they are placed into production. It is

8-13 This combination of variances may

8-14 Several factors other than the

contractual rate paid to workers can cause a

labor rate variance. For example, skilled workers

8-15 If poor quality materials create

production problems, a result could be excessive

8-16 If overhead is applied on the basis of

direct labor-hours, then the variable overhead

comparing the number of direct labor-hours

actually worked to the standard hours allowed.

rate, differs between the two variances.

output of the entire system is limited by the

capacity of the bottleneck. If workstations

before the bottleneck in the production process

The Foundational 15

1., 2., and 3.

The raw materials cost included in the flexible budget (SQ × SP =

$1,200,000), the materials quantity variance ($80,000 U), and the

The Foundational 15 (continued)

4. and 5.

The materials quantity variance ($80,000 U), and the materials price

The Foundational 15 (continued)

6., 7., and 8.

The direct labor cost included in the flexible budget (SH × SR = $840,000),

the labor efficiency variance ($70,000 F), and the labor rate variance

The Foundational 15 (continued)

9., 10., and 11.

The variable overhead cost included in the flexible budget (SH × SR =

$300,000), the variable overhead efficiency variance ($25,000 F), and the

The Foundational 15 (continued)

12. The amounts included in the flexible budget are computed as follows:

Preble Company

Flexible Budget

For the Month Ended March 31

Units sold (

q

) …………………………………………………….

30,000

Expenses:

Advertising ($200,000) …………………………..

$200,000

Sales salaries and commissions

($100,000 + $12.00

q

) …………………………..

$460,000

Shipping expenses ($3.00

q

) …………………………..

90,000

13., 14., and 15.

The spending variances for advertising ($), sales salaries and commissions

($), and shipping expenses ($) are computed as follows:

Preble Company

Spending Variances

For the Month Ended March 31

Flexible

Budget

Actual

Results

Spending

Variances

Units sold(

q

) …………………………..

30,000

30,000

Expenses:

Advertising ($200,000) …………..

$200,000

$210,000

$10,000

U

Sales salaries and commissions

($100,000 + $12.00

q

) …………

$460,000

$455,000

$5,000

F

Shipping expenses ($3.00

q

) …….

$90,000

$115,000

$25,000

U

Exercise 8-1 (10 minutes)

Puget Sound Divers

Flexible Budget

For the Month Ended May 31

Actual diving-hours ……………………………….

105

Revenue ($365.00q) ……………………………..

$38,325

Expenses:

Wages and salaries ($8,000 + $125.00q) …

21,125

Supplies ($3.00q) ……………………………….

315

Equipment rental ($1,800 + $32.00q) …….

5,160

Insurance ($3,400) …………………………..…

3,400

Miscellaneous ($630 + $1.80q) ……………..

819

Total expense ………………………………………

30,819

Net operating income …………………………….

$ 7,506

Exercise 8-2 (15 minutes)

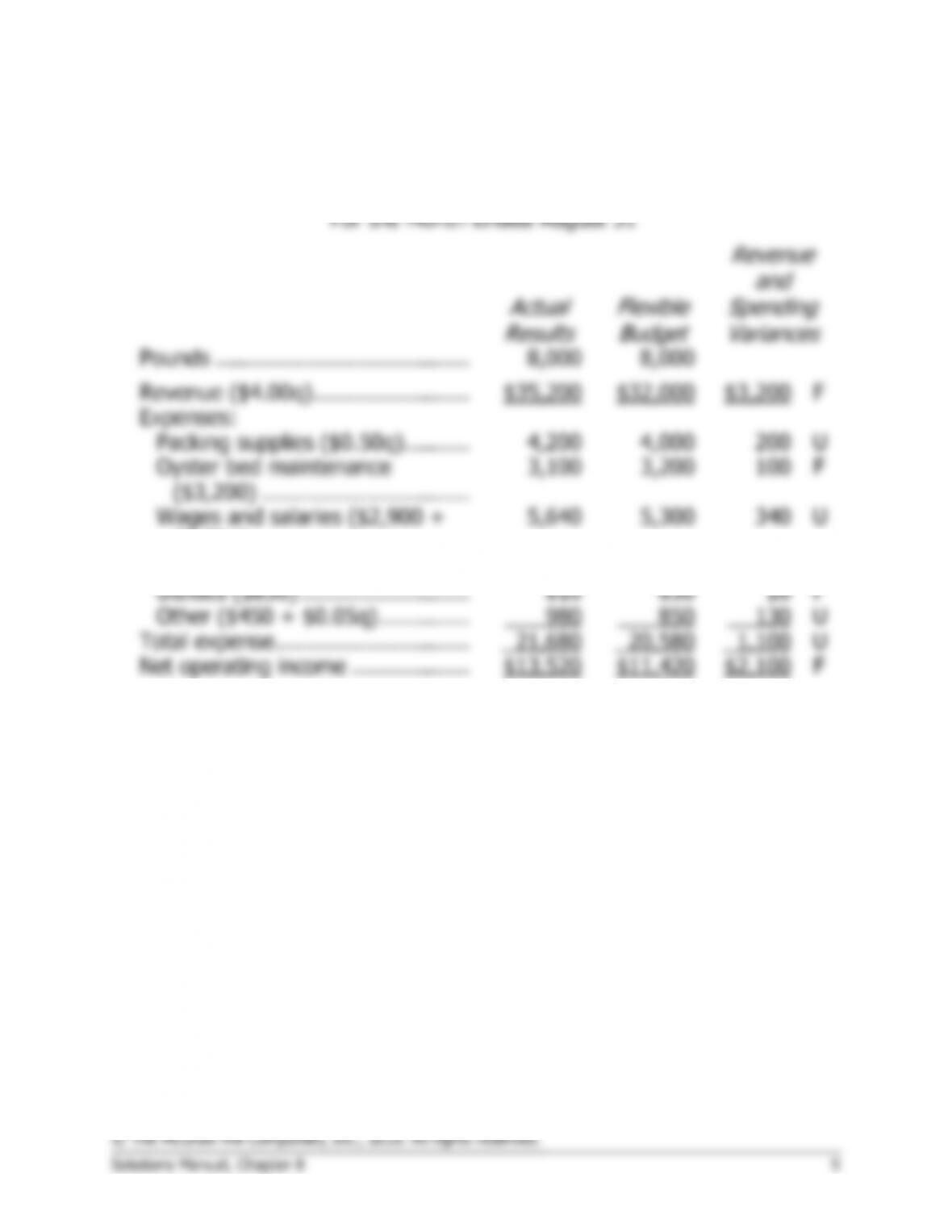

Quilcene Oysteria

Revenue and Spending Variances

For the Month Ended August 31

Actual

Results

Flexible

Budget

Revenue

and

Spending

Variances

Pounds …………………………………

8,000

8,000

Revenue ($4.00q) ……………………

$35,200

$32,000

$3,200

F

Expenses:

Packing supplies ($0.50q) ……….

4,200

4,000

200

U

Oyster bed maintenance

($3,200) …………………………..

3,100

3,200

100

F

Wages and salaries ($2,900 +

$0.30q) …………………………….

5,640

5,300

340

U

Shipping ($0.80q) …………………

6,950

6,400

550

U

Utilities ($830) ……………………..

810

830

20

F

Other ($450 + $0.05q) …………..

980

850

130

U

Total expense …………………………

21,680

20,580

1,100

U

Net operating income ………………

$13,520

$11,420

$2,100

F

Exercise 8-3 (15 minutes)

Alyeski Tours

Planning Budget

For the Month Ended July 31

Budgeted cruises (q1) ………………………………………………….

24

Budgeted passengers (q2) ……………………………………………

1,400

Revenue ($25.00q2) ……………………………………………………

$35,000

Expenses:

Vessel operating costs ($5,200 + $480.00q1 +$2.00q2) ……

19,520

Advertising ($1,700) …………………………………………………

1,700

Administrative costs ($4,300 + $24.00q1 +$1.00q2) ………..

6,276

Insurance ($2,900) …………………………………………………..

2,900

Total expense ……………………………………………………………

30,396

Net operating income ………………………………………………….

$ 4,604

Exercise 8-4 (20 minutes)

1.

Number of helmets …………………………………….

35,000

Standard kilograms of plastic per helmet …………

× 0.6

Total standard kilograms allowed …………………..

21,000

Standard cost per kilogram …………………………..

× $8

Total standard cost …………………………………….

$168,000

Actual cost incurred (given) ………………………….

$171,000

Total standard cost (above) ………………………….

168,000

Total material variance—unfavorable ………………

$ 3,000

2.

Actual Quantity

of Input, at

Actual Price

Actual Quantity of Input,

at Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

22,500 kilograms ×

21,000 kilograms* ×

$8 per kilogram

$8 per kilogram

$171,000

= $180,000

= $168,000

Price Variance =

$9,000 F

Quantity Variance =

$12,000 U

Spending Variance = $3,000 U

*35,000 helmets × 0.6 kilograms per helmet = 21,000 kilograms

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

22,500 kilograms ($7.60 per kilogram* – $8.00 per kilogram)

= $9,000 F

* $171,000 ÷ 22,500 kilograms = $7.60 per kilogram

Materials quantity variance = SP (AQ – SQ)

$8 per kilogram (22,500 kilograms – 21,000 kilograms)

= $12,000 U

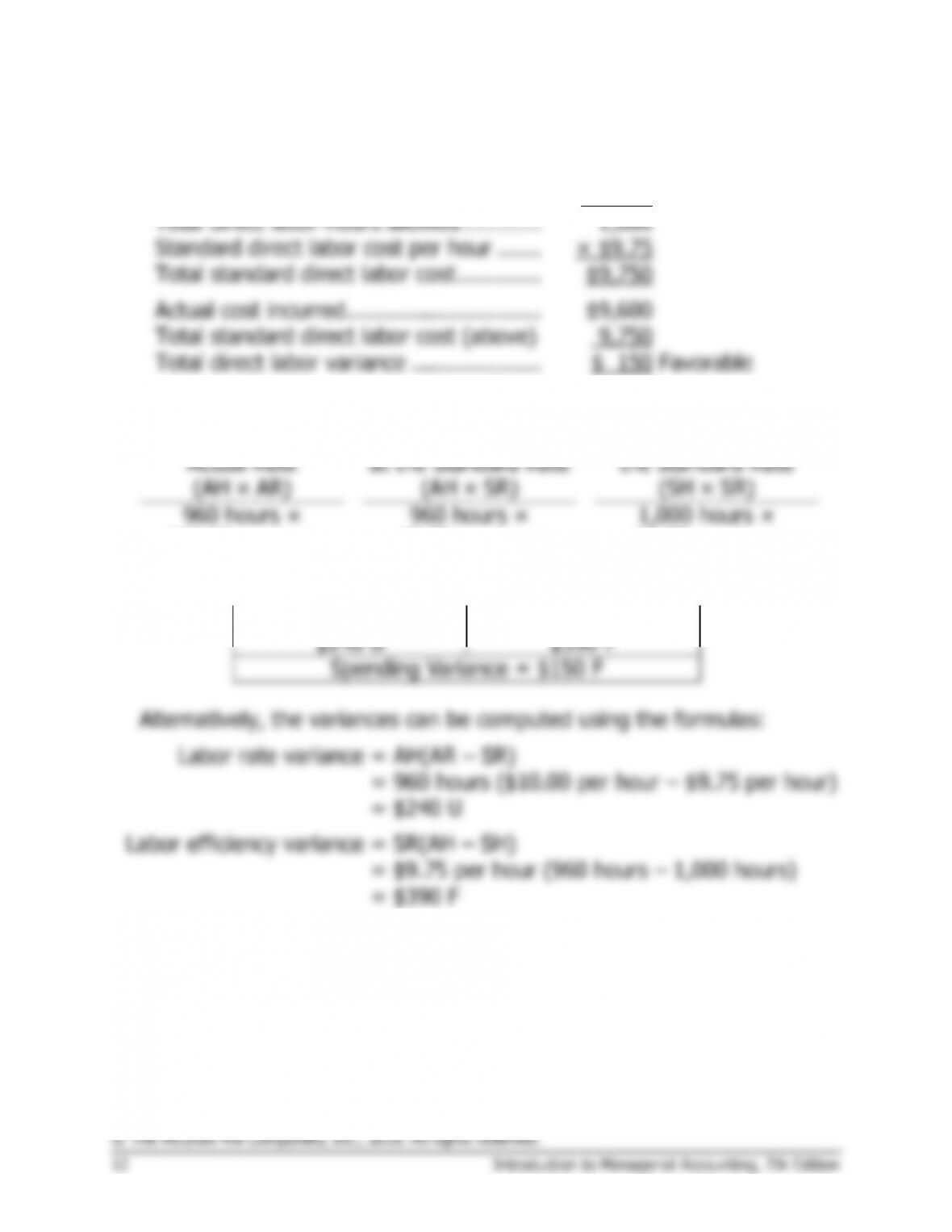

Exercise 8-5 (20 minutes)

1.

Number of meals prepared ……………….

4,000

Standard direct labor-hours per meal ….

× 0.25

Total direct labor-hours allowed …………

1,000

Standard direct labor cost per hour …….

× $9.75

Total standard direct labor cost ………….

$9,750

Actual cost incurred …………………………

$9,600

Total standard direct labor cost (above)

9,750

Total direct labor variance ………………..

$ 150

Favorable

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

960 hours ×

$10.00 per hour

960 hours ×

$9.75 per hour

1,000 hours ×

$9.75 per hour

= $9,600

= $9,360

= $9,750

Rate Variance =

$240 U

Efficiency Variance =

$390 F

Spending Variance = $150 F

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH(AR – SR)

= 960 hours ($10.00 per hour – $9.75 per hour)

= $240 U

Labor efficiency variance = SR(AH – SH)

= $9.75 per hour (960 hours – 1,000 hours)

= $390 F

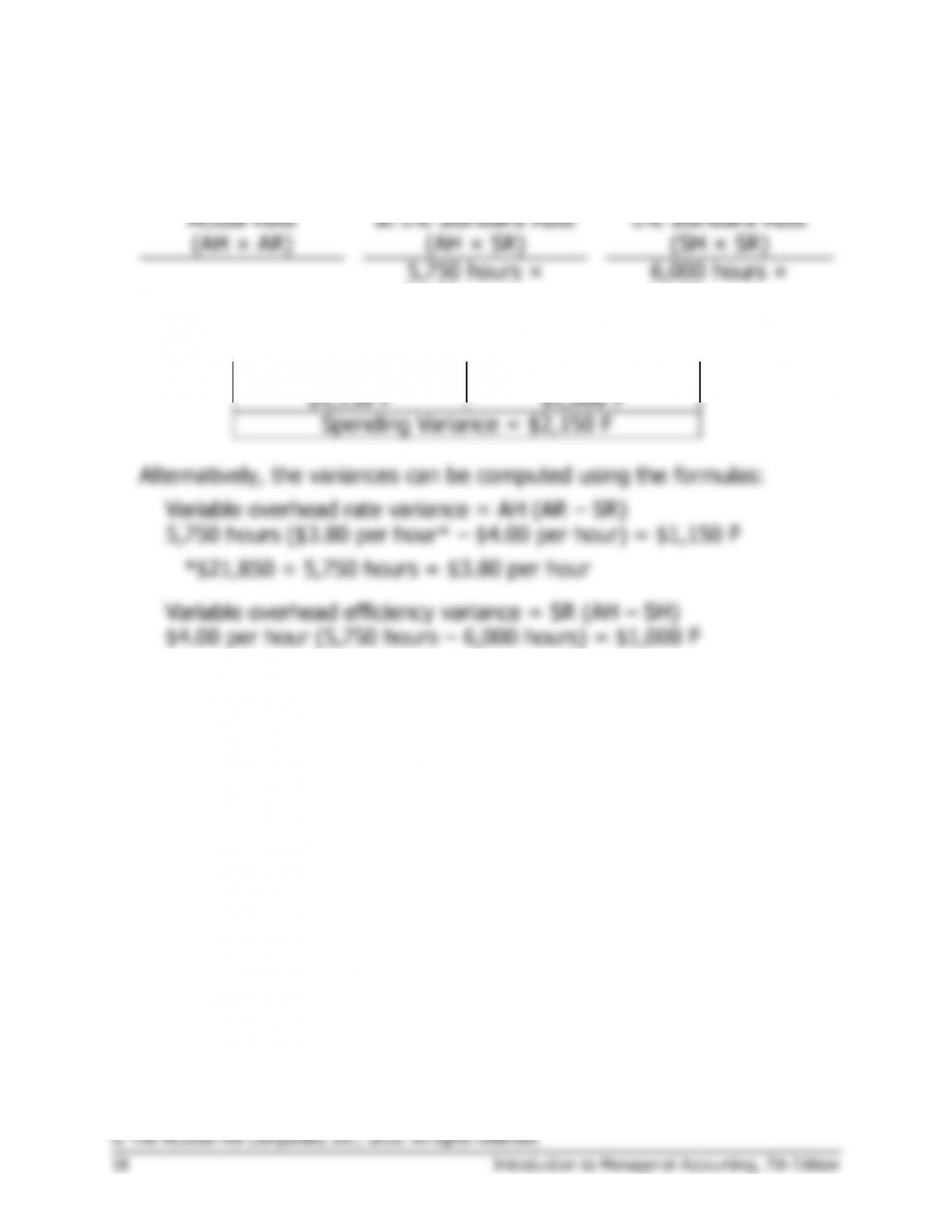

Exercise 8-6 (20 minutes)

1.

Number of items shipped …………………………...

120,000

Standard direct labor-hours per item …………….

× 0.02

Total direct labor-hours allowed …………………..

2,400

Standard variable overhead cost per hour ………

× $3.25

Total standard variable overhead cost …………..

$ 7,800

Actual variable overhead cost incurred ………….

$7,360

Total standard variable overhead cost (above) ..

7,800

Total variable overhead variance ………………….

$ 440

Favorable

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

2,300 hours ×

$3.20 per hour*

2,300 hours ×

$3.25 per hour

2,400 hours ×

$3.25 per hour

= $7,360

= $7,475

= $7,800

Variable Overhead Rate

Variance = $115 F

Variable Overhead

Efficiency Variance =

$325 F

Spending Variance = $440 F

*$7,360 ÷ 2,300 hours = $3.20 per hour

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance:

AH(AR – SR) = 2,300 hours ($3.20 per hour – $3.25 per hour)

= $115 F

Variable overhead efficiency variance:

SR(AH – SH) = $3.25 per hour (2,300 hours – 2,400 hours)

= $325 F

Exercise 8-7 (15 minutes)

Lavage Rapide

Planning Budget

For the Month Ended August 31

Budgeted cars washed (q) ………………………..

9,000

Revenue ($4.90q) …………………………………..

$44,100

Expenses:

Cleaning supplies ($0.80q) ……………………..

7,200

Electricity ($1,200 + $0.15q) ………………….

2,550

Maintenance ($0.20q)…………………………...

1,800

Wages and salaries ($5,000 + $0.30q) ……..

7,700

Depreciation ($6,000) …………………………...

6,000

Rent ($8,000) ……………………………………..

8,000

Administrative expenses ($4,000 + $0.10q) .

4,900

Total expense ………………………………………..

38,150

Net operating income ………………………………

$ 5,950

Exercise 8-8 (15 minutes)

Lavage Rapide

Flexible Budget

For the Month Ended August 31

Actual cars washed (q) …………………………….

8,800

Revenue ($4.90q) …………………………………..

$43,120

Expenses:

Cleaning supplies ($0.80q) ……………………..

7,040

Electricity ($1,200 + $0.15q) ………………….

2,520

Maintenance ($0.20q)…………………………...

1,760

Wages and salaries ($5,000 + $0.30q) ……..

7,640

Depreciation ($6,000) …………………………...

6,000

Rent ($8,000) ……………………………………..

8,000

Administrative expenses ($4,000 + $0.10q) .

4,880

Total expense ………………………………………..

37,840

Net operating income ………………………………

$ 5,280

Exercise 8-9 (20 minutes)

Lavage Rapide

Revenue and Spending Variances

For the Month Ended August 31

Actual

Results

Flexible

Budget

Revenue

and

Spending

Variances

Cars washed (q) ……………………..

8,800

8,800

Revenue ($4.90q) ……………………

$43,080

$43,120

$ 40

U

Expenses:

Cleaning supplies ($0.80q) ………

7,560

7,040

520

U

Electricity ($1,200 + $0.15q) …..

2,670

2,520

150

U

Maintenance ($0.20q)…………….

2,260

1,760

500

U

Wages and salaries

($5,000 + $0.30q) ……………

8,500

7,640

860

U

Depreciation ($6,000) …………….

6,000

6,000

0

Rent ($8,000) ………………………

8,000

8,000

0

Administrative expenses

($4,000 + $0.10q) ………………

4,950

4,880

70

U

Total expense …………………………

39,940

37,840

2,100

U

Net operating income ……………….

$ 3,140

$ 5,280

$2,140

U

Exercise 8-10 (30 minutes)

1.

Number of units manufactured ………………………..

20,000

Standard labor time per unit

(18 minutes ÷ 60 minutes per hour) ………………

× 0.3

Total standard hours of labor time allowed …………

6,000

Standard direct labor rate per hour …………………..

× $12

Total standard direct labor cost ……………………….

$72,000

Actual direct labor cost ………………………………….

$73,600

Standard direct labor cost ………………………………

72,000

Total variance—unfavorable …………………………...

$ 1,600

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours Allowed

for Output, at the

Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,750 hours ×

$12.00 per hour

6,000 hours* ×

$12.00 per hour

$73,600

= $69,000

= $72,000

Rate Variance =

$4,600 U

Efficiency Variance =

$3,000 F

Spending Variance = $1,600 U

*20,000 units × 0.3 hours per unit = 6,000 hours

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

5,750 hours ($12.80 per hour* – $12.00 per hour) = $4,600 U

*$73,600 ÷ 5,750 hours = $12.80 per hour

Labor efficiency variance = SR (AH – SH)

$12.00 per hour (5,750 hours – 6,000 hours) = $3,000 F

Exercise 8-10 (continued)

3.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,750 hours ×

$4.00 per hour

6,000 hours ×

$4.00 per hour

$21,850

= $23,000

= $24,000

Rate Variance =

$1,150 F

Efficiency Variance =

$1,000 F

Spending Variance = $2,150 F

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR – SR)

5,750 hours ($3.80 per hour* – $4.00 per hour) = $1,150 F

*$21,850 ÷ 5,750 hours = $3.80 per hour

Variable overhead efficiency variance = SR (AH – SH)

$4.00 per hour (5,750 hours – 6,000 hours) = $1,000 F

Exercise 8-11 (20 minutes)

1. If the labor spending variance is $93 unfavorable, and the rate variance

is $87 favorable, then the efficiency variance must be $180 unfavorable,

because the rate and efficiency variances taken together always equal

the spending variance. Knowing that the efficiency variance is $180

Exercise 8-11 (continued)

An alternative approach would be to work from known to unknown data