Problem 2-21B (30 minutes)

1. The predetermined overhead rate was:

Estimated fixed manufacturing overhead ………………

$1,278,000

Estimated variable manufacturing overhead

$3.40 per computer hour × 82,000 hours……………

278,800

Estimated total manufacturing overhead cost …………

$1,556,800

÷ Estimated total computer hours ……………..

hours

= Predetermined overhead rate ………………..

per hour

Actual manufacturing overhead cost …………………..

Underapplied overhead cost ……………………………..

Cost of Goods Sold ……………………………….

Finished goods inventory, beginning* ………….

$ 37,000

Add: Cost of goods manufactured ……………….

688,000

Cost of goods available for sale* ………………..

725,000

Deduct: Finished goods inventory, ending …….

Unadjusted cost of goods sold* ………………….

663,000

Add: Underapplied overhead ……………………..

Problem 2-22B (30 minutes)

Alexsandar Company

Schedule of Cost of Goods Manufactured

Direct materials:

Raw materials inventory, beginning* ……….

$ 59,000

Add: Purchases of raw materials*……………

263,000

Total raw materials available ………………….

322,000

Deduct: Raw materials inventory, ending* ..

30,000

Raw materials used in production ……………

$292,000

Direct labor ……………………………………………

57,000

Manufacturing overhead applied to work in

process inventory* ………………………………..

336,000

Total manufacturing costs* ……………………….

685,000

Add: Beginning work in process inventory …….

32,000

717,000

Deduct: Ending work in process inventory* …..

29,000

Cost of goods manufactured………………………

$688,000

Problem 2-22B (continued)

Alexsandar Company

Income Statement

Sales ………………………………………………….

$1,093,000

Cost of goods sold ($663,000 + $23,000) ….

686,000

Gross margin ……………………………………….

407,000

Selling and administrative expenses:

Selling expenses* ……………………………….

$217,000

Administrative expense* ………………………

151,000

368,000

Net operating income* …………………………..

$ 39,000

* Given

2-4 Introduction to Managerial Accounting, 6th edition

Problem 2-23B (45 minutes)

1. The cost of raw materials put into production was:

Raw materials inventory, 1/1 …………………..

$ 38,000

Debits (purchases of materials) ……………….

450,000

Materials available for use ………………………

488,000

Raw materials inventory, 12/31 ……………….

55,000

Materials requisitioned for production ……….

$433,000

2. Of the $433,000 in materials requisitioned for production, $328,000 was

3.

Total factory wages accrued during the year

(credits to the Factory Wages Payable account) ..

$181,000

Less direct labor cost (from Work in Process) ……..

119,000

Indirect labor cost ………………………………………..

$ 62,000

4. The cost of goods manufactured for the year was $780,000—the credits

5. The Cost of Goods Sold for the year was:

Finished goods inventory, 1/1 ……………………………………

$ 47,000

Add: Cost of goods manufactured (from Work in Process) .

780,000

Cost of goods available for sale ………………………………….

827,000

Deduct: Finished goods inventory, 12/31 ……………………..

138,000

Cost of goods sold …………………………………………………..

$689,000

6. The predetermined overhead rate was:

Predetermined

overhead rate

=

Manufacturing overhead cost applied

Direct materials cost

Predetermined

overhead rate

=

$420,000

=

128.05% of direct materials cost

$328,000

2-6 Introduction to Managerial Accounting, 6th edition

Problem 2-23B (continued)

7. Manufacturing overhead was overapplied by $32,000, computed as

follows:

Actual manufacturing overhead cost for the year (debits) .

$388,000

Applied manufacturing overhead cost (from Work in

Process—this would be the credits to the Manufacturing

Overhead account) ………………………………………………

420,000

Overapplied overhead …………………………..…………………

$(32,000)

8. The ending balance in Work in Process is $166,000. Direct labor makes

up $92,567.90 of this balance, and manufacturing overhead makes up

Balance, Work in Process, 12/31 …………………………...

$166,000.00

Less: Direct materials cost (given) ………………………….

(32,200.00)

Manufacturing overhead cost

($32,200 × 128.05%) ……………………………….

(41,232.10)

Direct labor cost (remainder) ………………………………..

$92,567.90

Problem 2-24B (60 minutes)

1. a.

Predetermined

overhead rate

=

Estimated total manufacturing overhead cost

Estimated total amount of the allocation base

Predetermined

overhead rate

=

$117,000

=

130% of direct labor cost

$90,000

b.

Actual manufacturing overhead costs:

Insurance, factory ………………………………

$ 8,800

Depreciation of equipment……………………

17,000

Indirect labor …………………………………….

32,700

Property taxes …………………………………..

8,500

Maintenance ……………………………………..

13,000

Rent, building ……………………………………

36,000

Total actual costs …………………………………

116,000

Applied manufacturing overhead costs:

$86,000 × 130% ……………………………….

111,800

Underapplied overhead ………………………….

$ 4,200

2.

Ilarion Manufacturing Company

Schedule of Cost of Goods Manufactured

Direct materials:

Raw materials inventory, beginning ……………..

$ 29,000

Add: Purchases of raw materials …………………

130,000

Total raw materials available ……………………..

159,000

Deduct: Raw materials inventory, ending ……..

11,000

Raw materials used in production ……………….

$148,000

Direct labor ………………………………………………

86,000

Manufacturing overhead applied to work in

process …………………………………………………

111,800

Total manufacturing cost …………………………….

345,800

Add: Work in process, beginning …………………..

45,000

390,800

Deduct: Work in process, ending …………………..

36,000

Cost of goods manufactured ………………………..

$354,800

Direct materials …………………………………..

Direct labor ………………………………………..

Manufacturing overhead ……………………….

Work in process inventory ……………………..

Problem 2-24B (continued)

3.

Unadjusted cost of goods sold:

Finished goods inventory, beginning ………………..

$ 71,000

Add: Cost of goods manufactured ……………………

354,800

Cost of goods available for sale ………………………

425,800

Deduct: Finished goods inventory, ending …………

61,000

Unadjusted cost of goods sold ………………………..

$364,800

4.

Direct materials ……………………………………………..

$ 3,300

Direct labor …………………………………………………..

4,900

Overhead applied (130% × $4,900) …………………..

6,370

Total manufacturing cost …………………………………

$14,570

$14,570 × 140% = $20,398 price to customer.

5. The amount of overhead cost in Work in Process was:

$8,700 direct labor cost × 130% = $11,310

The amount of direct materials cost in Work in Process was:

Total ending work in process ………………….

$36,000

Deduct:

Direct labor ……………………………………..

$ 8,700

Manufacturing overhead ……………………..

11,310

20,010

Direct materials …………………………………..

$15,990

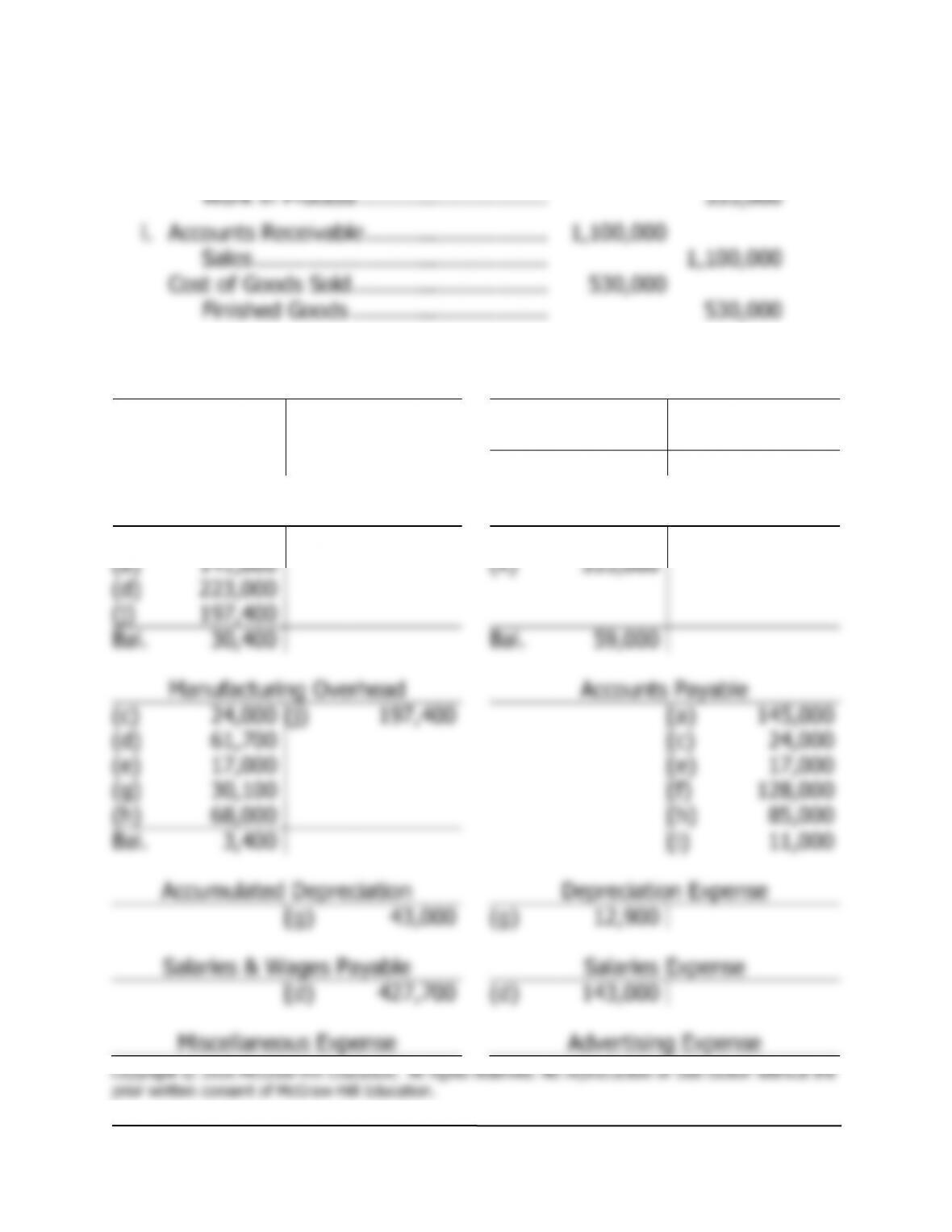

Problem 2-25B (120 minutes)

1.

a.

Raw Materials ………………………………..

145,000

Accounts Payable ………………………

145,000

b.

Work in Process ……………………………..

141,000

Raw Materials …………………………...

141,000

c.

Manufacturing Overhead ………………….

24,000

Accounts Payable ………………………

24,000

d.

Work in Process ……………………………..

223,000

Manufacturing Overhead ………………….

61,700

Salaries Expense …………………………….

143,000

Salaries and Wages Payable …………

427,700

e.

Manufacturing Overhead ………………….

17,000

Accounts Payable ………………………

17,000

f.

Advertising Expense ………………………..

128,000

Accounts Payable ………………………

128,000

g.

Manufacturing Overhead ………………….

30,100

Depreciation Expense………………………

12,900

Accumulated Depreciation ……………

43,000

h.

Manufacturing Overhead ………………….

68,000

Rent Expense …………………………..……

17,000

Accounts Payable ………………………

85,000

i.

Miscellaneous Expense …………………….

11,000

Accounts Payable ………………………

11,000

j.

Work in Process ……………………………..

197,400

Manufacturing Overhead ……………..

197,400

Predetermined

overhead rate

=

Estimated total manufacturing overhead cost

Estimated direct materials cost

Predetermined

overhead rate

=

$221,200

=

140% of direct materials cost

$158,000

$141,000 direct materials cost × 140% = $197,400 applied.

(g)

43,000

(g)

(d)

(d)

143,000

Problem 2-25B (continued)

k.

Finished Goods ……………………………..

555,000

Work in Process ………………………..

555,000

l.

Accounts Receivable ……………………….

1,100,000

Sales ………………………………………

1,100,000

Cost of Goods Sold …………………………

530,000

Finished Goods …………………………

530,000

2.

Accounts Receivable

Raw Materials

(l)

1,100,000

Bal.

23,000

(b)

141,000

(a)

145,000

Bal.

27,000

Work in Process

Finished Goods

Bal.

24,000

(k)

555,000

Bal.

34,000

(l)

530,000

(b)

141,000

(k)

555,000

(d)

223,000

(j)

197,400

Bal.

30,400

Bal.

59,000

Manufacturing Overhead

Accounts Payable

(c)

24,000

(j)

197,400

(a)

145,000

(d)

61,700

(c)

24,000

(e)

17,000

(e)

17,000

(g)

30,100

(f)

128,000

(h)

68,000

(h)

85,000

Bal.

3,400

(i)

11,000

(i)

11,000

(f)

128,000