Problem 10-23A (continued)

4. Under these circumstances, the company should make the 100,000

boxes of tubes and purchase the remaining 20,000 boxes from the

outside supplier. The costs would:

Cost of making: 100,000 boxes × $1.15 per box …..

$115,000

Cost of buying: 20,000 boxes × $1.35 per box ……..

27,000

Total cost ……………………………………………………..

$142,000

Total cost ……………………………………………………..

Problem 10-24A (45 minutes)

1. Product RG-6 has a contribution margin of $8 per unit ($22 – $14 = $8).

If the plant closes, this contribution margin will be lost on the 16,000

units (8,000 units per month × 2 months) that could have been sold

during the two-month period. However, the company will be able to

avoid some fixed costs as a result of closing down. The analysis is:

Contribution margin lost by closing the plant for

two months ($8 per unit × 16,000 units) ……….

$(128,000)

Costs avoided by closing the plant for two months:

Fixed manufacturing overhead cost ($45,000

per month × 2 months = $90,000) …………….

$90,000

Fixed selling costs ($30,000 per month × 10%

× 2 months) …………………………………………

6,000

96,000

Net disadvantage of closing, before start-up

costs ……………………………………………………..

(32,000)

Add start-up costs ………………………………………

8,000

Disadvantage of closing the plant …………………..

$ (40,000)

No, the company should not close the plant; it should continue to

operate at the reduced level of 8,000 units produced and sold each

month. Closing will result in a $40,000 greater loss over the two-month

period than if the company continues to operate. An additional factor is

the potential loss of goodwill among the customers who need the 8,000

units of RG-6 each month. By closing down, the needs of these

customers will not be met (no inventories are on hand), and their

business may be permanently lost to another supplier.

Problem 10-24A (continued)

Alternative Solution:

Plant

Kept

Open

Plant

Closed

Difference:

Net

Operating

Income

Increase or

(Decrease)

Sales (8,000 units × $22 per

unit × 2)………………………..

$ 352,000

$ 0

$(352,000)

Variable expenses (8,000 units

× $14 per unit × 2) ………….

224,000

0

224,000

Contribution margin ……………

128,000

0

(128,000)

Less fixed costs:

Fixed manufacturing

overhead costs ($150,000

× 2) …………………………...

300,000

210,000

90,000

Fixed selling costs

($30,000 × 2) ………………

60,000

54,000

*

6,000

Total fixed costs …………………

360,000

264,000

96,000

Net operating loss before

start-up costs ………………….

(232,000)

(264,000)

(32,000)

Start-up costs ……………………

0

(8,000)

(8,000)

Net operating loss ………………

$(232,000)

$(272,000)

$ (40,000)

*

$30,000 × 90% = $27,000 × 2 = $54,000

Problem 10-24A (continued)

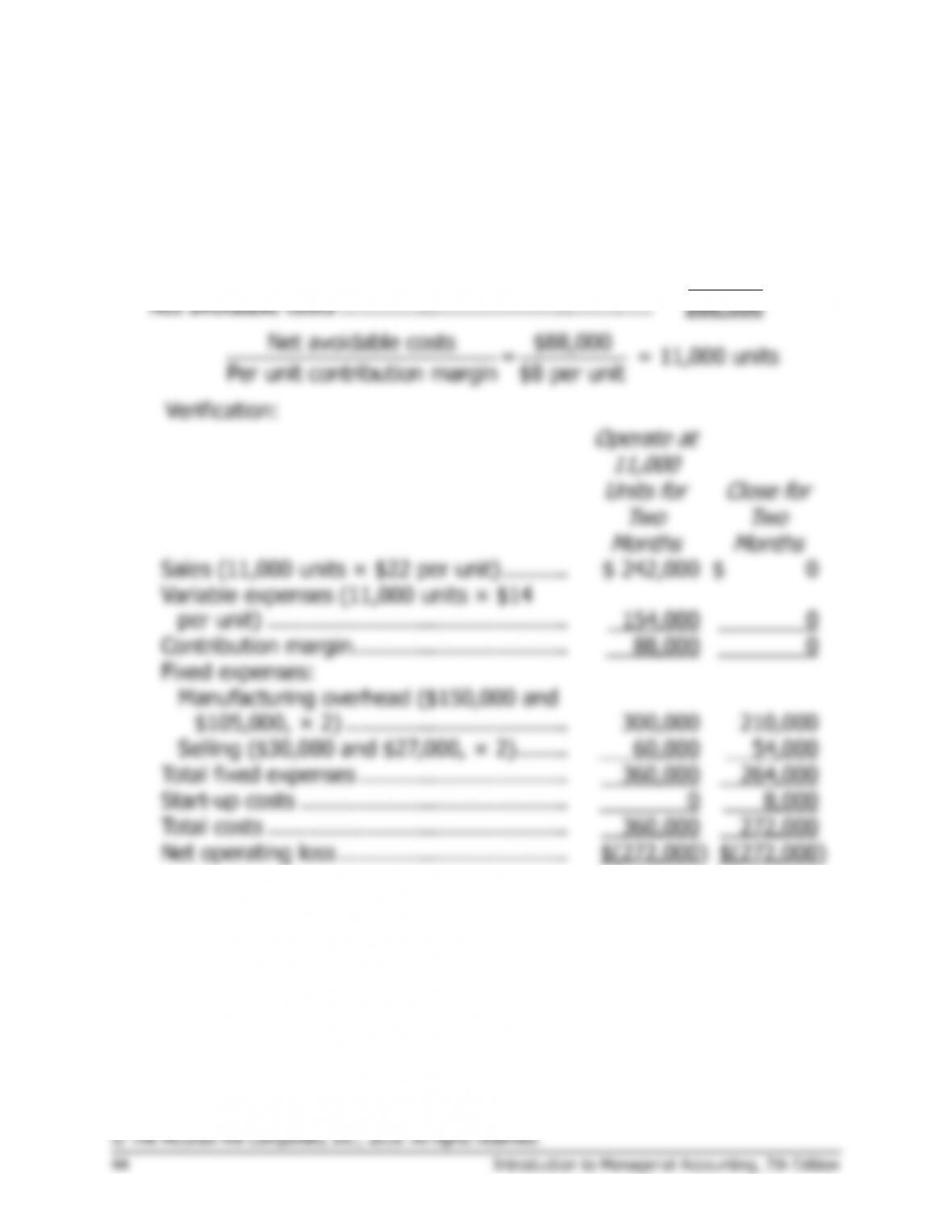

2. Birch Company will not be affected at a level of 11,000 total units sold

over the two-month period. The computations are:

Cost avoided by closing the plant for two months

(see above) …………………………………………………

$96,000

Less start-up costs ………………………………………….

8,000

Net avoidable costs …………………………………………

$88,000

Net avoidable costs $88,000

Operate at

11,000

Units for

Two

Months

Close for

Two

Months

Sales (11,000 units × $22 per unit) ……….

$ 242,000

$ 0

Variable expenses (11,000 units × $14

per unit) ……………………………………….

154,000

0

Contribution margin …………………………...

88,000

0

Fixed expenses:

Manufacturing overhead ($150,000 and

$105,000, × 2) …………………………….

300,000

210,000

Selling ($30,000 and $27,000, × 2)……..

60,000

54,000

Total fixed expenses …………………………..

360,000

264,000

Start-up costs …………………………………..

0

8,000

Total costs ……………………………………….

360,000

272,000

Net operating loss …………………………..…

$(272,000)

$(272,000)

Problem 10-25A (60 minutes)

1.

Debbie

Trish

Sarah

Mike

Sewing

Kit

Direct labor cost per unit ..

$ 3.20

$2.00

$ 5.60

$ 4.00

$ 1.60

Direct labor hours per

unit* (a) …………………..

0.40

0.25

0.70

0.50

0.20

Selling price …………………

$13.50

$5.50

$21.00

$10.00

$ 8.00

Variable costs:

Direct materials ………….

4.30

1.10

6.44

2.00

3.20

Direct labor ……………….

3.20

2.00

5.60

4.00

1.60

Variable overhead ……….

0.80

0.50

1.40

1.00

0.40

Total variable costs ………..

8.30

3.60

13.44

7.00

5.20

Contribution margin (b) ….

$ 5.20

$1.90

$ 7.56

$ 3.00

$ 2.80

Contribution margin per

DLH (b) ÷ (a) …………….

$13.00

$7.60

$10.80

$ 6.00

$14.00

* Direct labor cost per unit ÷ 8 direct labor hours.

2.

Product

DLH Per

Unit

Estimated

Sales

(units)

Total

Hours

Debbie……………………

0.40

hours

50,000

20,000

Trish ………………………

0.25

hours

42,000

10,500

Sarah …………………….

0.70

hours

35,000

24,500

Mike ………………………

0.50

hours

40,000

20,000

Sewing Kit ………………

0.20

hours

325,000

65,000

Total hours required ….

140,000

3. Because the Mike doll has the lowest contribution margin per labor hour,

its production should be reduced by 20,000 dolls (10,000 excess hours

Problem 10-25A (continued)

An alternative means of deriving this solution is as follows:

Amount of constrained resource available …………….

130,000 hours

Less: Constrained resource required for production

of 325,000 units of the Sewing Kit …………………..

65,000 hours

Remaining constrained resource available …………….

65,000 hours

Less: Constrained resource required for production

of 50,000 units of the Debbie doll …………………..

20,000 hours

Remaining constrained resource available …………….

45,000 hours

Less: Constrained resource required for production

of 35,000 units of the Sarah doll …………………….

24,500 hours

Remaining constrained resource available …………….

20,500 hours

Less: Constrained resource required for production

of 42,000 units of the Trish doll ………………………

10,500 hours

Remaining constrained resource available …………….

10,000 hours

Less: Constrained resource required for production

of 20,000 units of the Mike doll ………………………

10,000 hours

Remaining constrained resource available …………….

0 hours

4. The highest possible contribution margin is the sum of the contribution

margins earned on each of the five products, or $1,574,400:

Sewing

Kit

Debbie

Sarah

Trish

Mike

Unit contribution

margin (a) ……….

$2.80

$5.20

$7.56

$1.90

$3.00

Optimal production

plan (b) …………..

325,000

50,000

35,000

42,000

20,000

Total contribution

margin (a) × (b) .

$910,000

$260,000

$264,600

$79,800

$60,000

Problem 10-25A (continued)

5. Because the additional capacity would be used to produce the Mike doll,

the company should be willing to pay up to $14 per hour ($8 usual rate

profit.

6. Additional output could be obtained in a number of ways including

working overtime, adding another shift, expanding the workforce,

contracting out some work to outside suppliers, and eliminating wasted

labor time in the production process. The first four methods are costly,

Problem 10-26A (60 minutes)

1. The simplest approach to the solution is:

Gross margin lost if the store is closed …………

$(316,800)

Costs that can be avoided:

Sales salaries …………………………………….

$70,000

Direct advertising ……………………………….

51,000

Store rent …………………………………………

85,000

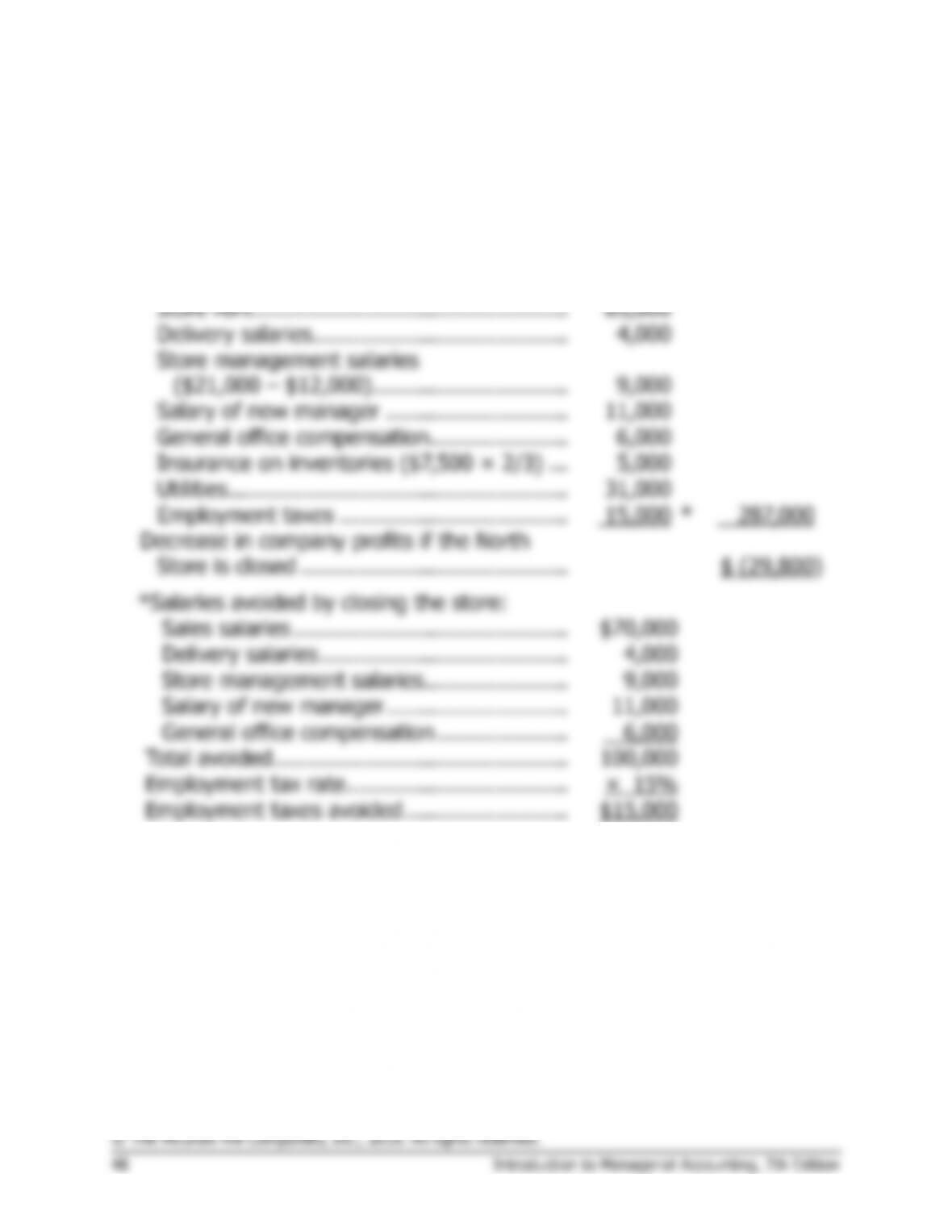

Delivery salaries …………………………………

4,000

Store management salaries

($21,000 – $12,000) …………………………

9,000

Salary of new manager ……………………….

11,000

General office compensation …………………

6,000

Insurance on inventories ($7,500 × 2/3) …

5,000

Utilities …………………………………………….

31,000

Employment taxes ……………………………..

15,000

*

287,000

Decrease in company profits if the North

Store is closed …………………………………..

$ (29,800)

*Salaries avoided by closing the store:

Sales salaries ……………………………………

$70,000

Delivery salaries ………………………………..

4,000

Store management salaries ………………….

9,000

Salary of new manager ……………………….

11,000

General office compensation ………………..

6,000

Total avoided ………………………………………

100,000

Employment tax rate …………………………….

× 15%

Employment taxes avoided …………………….

$15,000

Problem 10-26A (continued)

Alternative Solution:

North

Store

Kept

Open

North

Store

Closed

Difference:

Net

Operating

Income

Increase or

(Decrease)

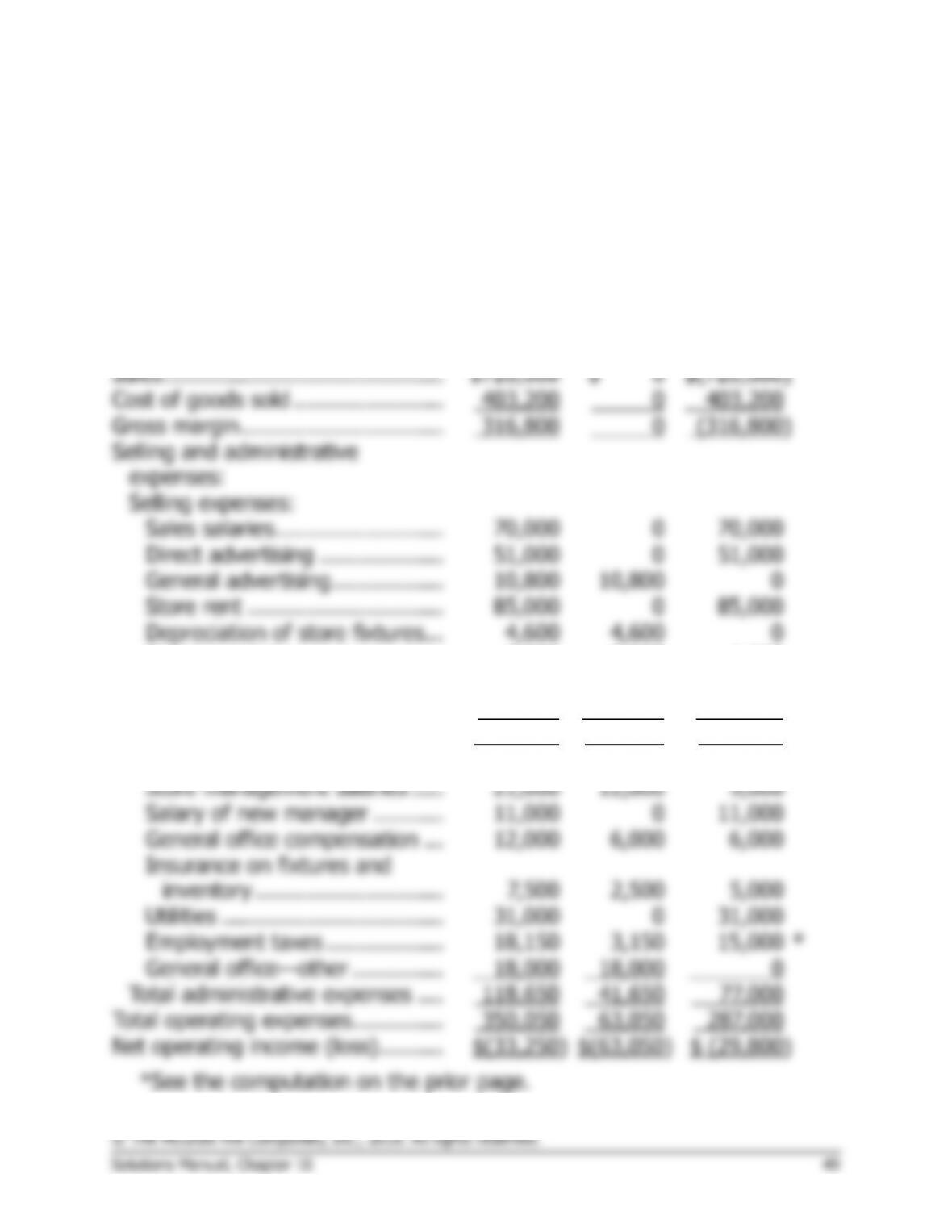

Sales …………………………………….

$720,000

$ 0

$(720,000)

Cost of goods sold …………………..

403,200

0

403,200

Gross margin ………………………….

316,800

0

(316,800)

Selling and administrative

expenses:

Selling expenses:

Sales salaries ……………………..

70,000

0

70,000

Direct advertising ……………….

51,000

0

51,000

General advertising ……………..

10,800

10,800

0

Store rent …………………………

85,000

0

85,000

Depreciation of store fixtures …

4,600

4,600

0

Delivery salaries …………………

7,000

3,000

4,000

Depreciation of delivery

equipment ………………………

3,000

3,000

0

Total selling expenses …………….

231,400

21,400

210,000

Administrative expenses:

Store management salaries …..

21,000

12,000

9,000

Salary of new manager ………..

11,000

0

11,000

General office compensation …

12,000

6,000

6,000

Insurance on fixtures and

inventory ………………………..

7,500

2,500

5,000

Utilities …………………………….

31,000

0

31,000

Employment taxes ………………

18,150

3,150

15,000

*

General office—other …………..

18,000

18,000

0

Total administrative expenses ….

118,650

41,650

77,000

Total operating expenses …………..

350,050

63,050

287,000

Net operating income (loss) ……….

$(33,250)

$(63,050)

$ (29,800)

Problem 10-26A (continued)

2. Based on the data in (1), the North Store should not be closed. If the

store is closed, then the company’s overall net operating income will

3. Under these circumstances, the North Store should be closed. The

computations are as follows:

Gross margin lost if the North Store is closed (part 1) …..

$(316,800)

Gross margin gained from the East Store: $720,000 ×

1/4 = $180,000; $180,000 × 45%* = $81,000 …………

81,000

Net operating loss in gross margin …………………………...

(235,800)

Less costs that can be avoided if the North Store is

closed (part 1) …………………………………………………..

287,000

Net advantage of closing the North Store …………………..

$ 51,200

*The East Store’s gross margin percentage is:

$486,000 ÷ $1,080,000 = 45%

Problem 10-27A (60 minutes)

1. A product should be processed further if the incremental revenue from

the further processing exceeds the incremental costs. The incremental

revenue from further processing of the Grit 337 is:

Selling price of the silver polish, per jar ……………..

$4.00

Selling price of 1/4 pound of Grit 337 ($2.00 ÷ 4) .

0.50

Incremental revenue per jar …………………………...

$3.50

Variable manufacturing overhead (25% × $1.48) ..

Variable selling costs (7.5% × $4) ……………………

0.30

Incremental variable cost per jar ……………………..

$2.80

Problem 10-27A (continued)

2. Only the cost of advertising and the cost of the production supervisor

are avoidable if production of the silver polish is discontinued.

Therefore, the number of jars of silver polish that must be sold each

month to justify continued processing of the Grit 337 into silver polish

is:

Production supervisor ……….

$3,000

Advertising—direct……………

4,000

Avoidable fixed costs ………..

$7,000

Avoidable fixed costs $7,000

=

Incremental CM per jar $0.70 per jar

= 10,000 jars per month

Therefore, if 10,000 jars of silver polish can be sold each month, the

company would be indifferent between selling it or selling all of the Grit

337 as a cleaning powder. If the sales of the silver polish are greater

than 10,000 jars per month, then continued processing of the Grit 337

into silver polish would be advisable because the company’s total profits

will be increased. If the company can’t sell at least 10,000 jars of silver

polish each month, then production of the silver polish should be

discontinued. To verify this, we show on the next page the total

contribution to profits of sales of 9,000, 10,000, and 11,000 jars of silver

polish, contrasted to sales of equivalent amounts of Grit 337 sold

outright (i.e., 10,000 jars of silver polish would require the use of 2,500

pounds of Grit 337 that otherwise could be sold outright as cleaning

powder, etc.):

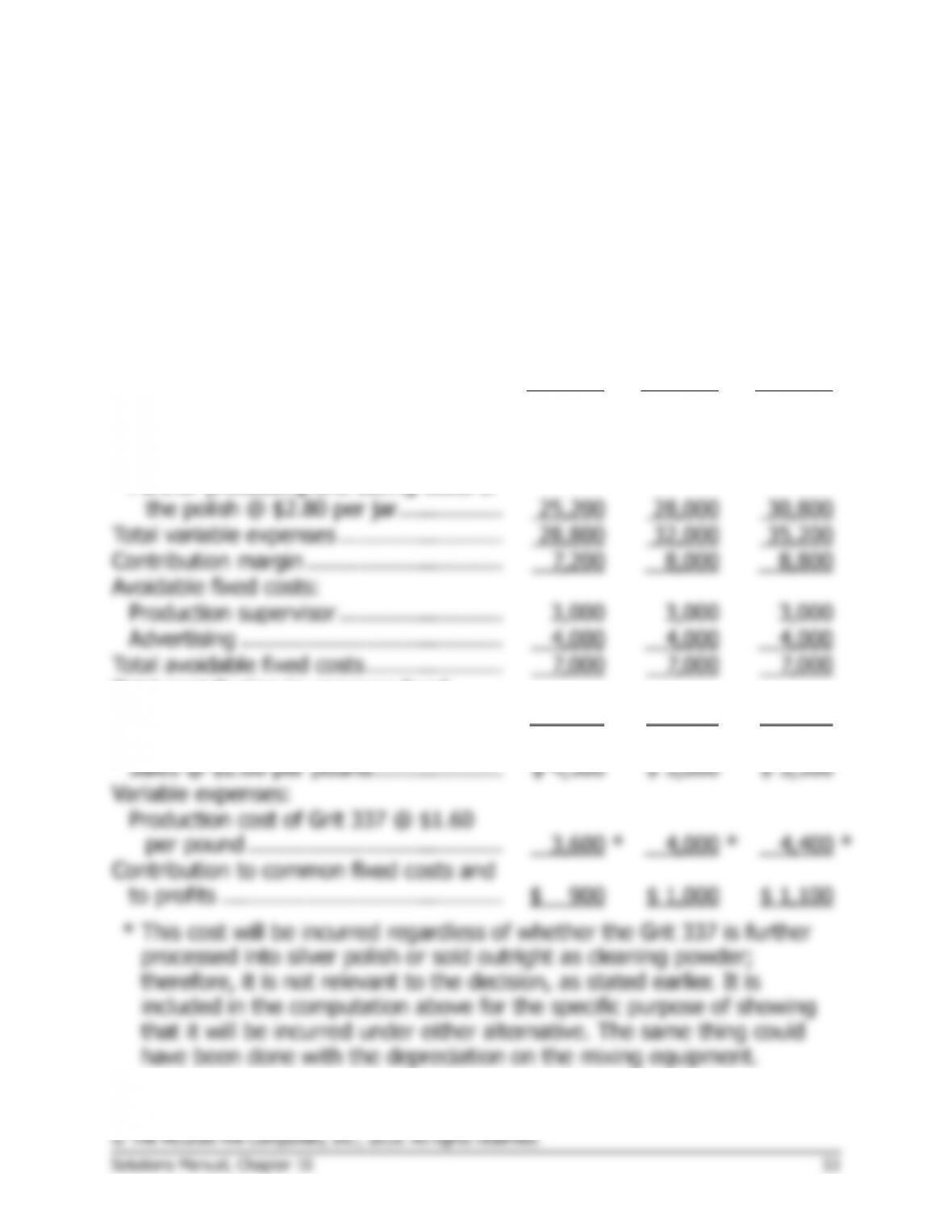

Problem 10-27A (continued)

9,000

Jars of

Polish;

or 2,250

pounds

of Grit

337

10,000

Jars of

Polish;

or 2,500

pounds

of Grit

337

11,000

Jars of

Polish;

or 2,750

pounds

of Grit

337

Sales of Silver Polish:

Sales @ $4.00 per jar …………………….

$36,000

$40,000

$44,000

Variable expenses:

Production cost of Grit 337 @ $1.60

per pound …………………………………

3,600

*

4,000

*

4,400

*

Further processing and selling costs of

the polish @ $2.80 per jar …………….

25,200

28,000

30,800

Total variable expenses …………………….

28,800

32,000

35,200

Contribution margin …………………………

7,200

8,000

8,800

Avoidable fixed costs:

Production supervisor …………………….

3,000

3,000

3,000

Advertising ………………………………….

4,000

4,000

4,000

Total avoidable fixed costs …………………

7,000

7,000

7,000

Total contribution to common fixed

costs and to profits………………………..

$ 200

$ 1,000

$ 1,800

Sales of Grit 337:

Sales @ $2.00 per pound ………………..

$ 4,500

$ 5,000

$ 5,500

Variable expenses:

Production cost of Grit 337 @ $1.60

per pound …………………………………

3,600

*

4,000

*

4,400

*

Contribution to common fixed costs and

to profits …………………………………….

$ 900

$ 1,000

$ 1,100

Problem 10-28A (60 minutes)

1. The $2.80 per drum general overhead cost is not relevant to the

decision because this cost will be the same regardless of whether the

Differential Costs

Per Drum

Total Differential Costs—

60,000 Drums

Make

Buy

Make

Buy

Outside supplier’s price .

$18.00

$1,080,000

Direct materials …………

$10.35

$621,000

Direct labor

($6.00 × 70%) ……….

4.20

252,000

Variable overhead

($1.50 × 70%) ……….

1.05

63,000

Supervision ………………

0.75

45,000

Equipment rental* ……..

2.25

*

135,000

Total cost …………………

$18.60

$18.00

$1,116,000

$1,080,000

Difference in favor of buying …………………………..

$0.60

$36,000

*

$135,000 per year ÷ 60,000 drums = $2.25 per drum.

Problem 10-28A (continued)

2. a. Notice that unit costs for both supervision and equipment rental

decrease with the greater volume because these fixed costs are

spread over more units.

Differential

Cost Per Drum

Total Differential Cost—

75,000 Drums

Make

Buy

Make

Buy

Outside supplier’s price ….

$18.00

$1,350,000

Direct materials ……………

$10.35

$776,250

Direct labor …………………

4.20

315,000

Variable overhead …………

1.05

78,750

Supervision ($45,000 ÷

75,000 drums) …………..

0.60

45,000

Equipment rental

($135,000 ÷ 75,000

drums) …………………….

1.80

135,000

Total cost ……………………

$18.00

$18.00

$1,350,000

$1,350,000

Difference …………………..

$0

$0

The company would be indifferent between the two alternatives if

75,000 drums were needed each year.

Problem 10-28A (continued)

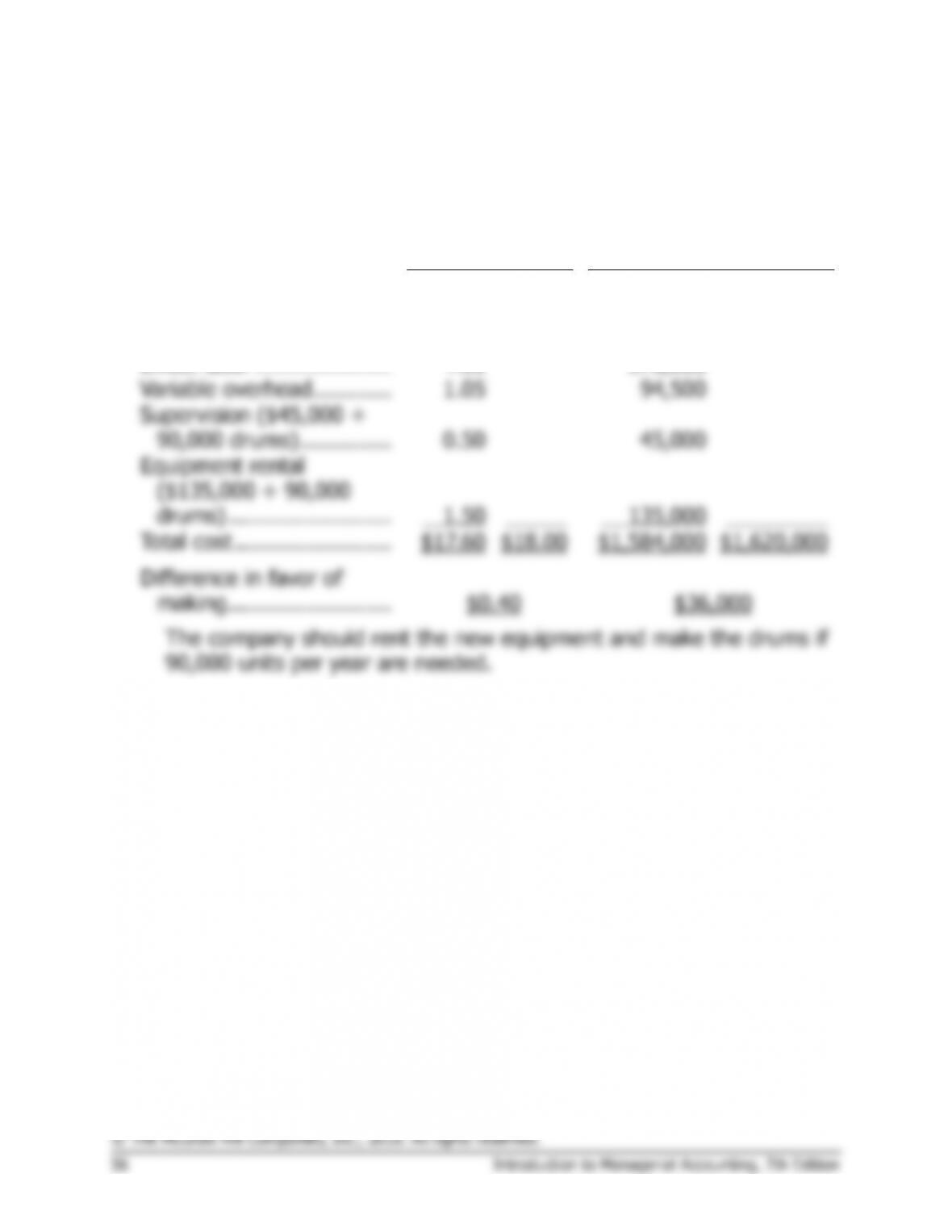

b. Again, notice that the unit costs for both supervision and equipment

rental decrease with the greater volume of units.

Differential

Costs Per Drum

Total Differential Cost—

90,000 Drums

Make

Buy

Make

Buy

Outside supplier’s price ….

$18.00

$1,620,000

Direct materials ……………

$10.35

$931,500

Direct labor …………………

4.20

378,000

Variable overhead …………

1.05

94,500

Supervision ($45,000 ÷

90,000 drums) …………..

0.50

45,000

Equipment rental

($135,000 ÷ 90,000

drums) …………………….

1.50

135,000

Total cost ……………………

$17.60

$18.00

$1,584,000

$1,620,000

Problem 10-28A (continued)

3. Other factors that the company should consider include:

a. Will volume in future years increase, or will it remain constant at

60,000 units per year? (If volume increases, then renting the new

equipment becomes more desirable, as shown in the computations

above.)

Case (45 minutes)

1. As much yarn as possible should be processed into sweaters. Products

should be processed further so long as the added revenues from further

processing are greater than the added costs. In this case, the added

revenues and costs are:

Per Sweater

Added revenue ($30.00 – $20.00) …….

$10.00

Added costs:

Buttons, thread, lining ………………….

$2.00

Direct labor ……………………………….

5.80

7.80

Added contribution margin ………………

$ 2.20

Thus, the company will gain $2.20 in contribution margin for each

spindle of yarn that is further processed into a sweater. The fixed

manufacturing overhead costs are not relevant to the decision because

they will be the same regardless of whether the yarn is sold or

processed further. In addition, we must omit the $16.00 cost of

manufacturing the yarn because this cost will be incurred whether the

yarn is sold as is or is used in sweaters.

2. The lowest price the company should accept is $27.80 per sweater. The

simplest approach to this answer is:

Present selling price per sweater ………

$30.00

Less added contribution margin being

realized on each sweater sold ………..

2.20

Minimum selling price per sweater …….

$27.80

A more involved approach to the same answer is to reason as follows:

If the wool yarn is sold outright, then the company will realize a

contribution margin of $9.40 per spindle:

Per Spindle

Selling price ……………………..

$20.00

Variable expenses:

Raw wool ………………………

$7.00

Direct labor ……………………

3.60

10.60

Contribution margin ……………

$ 9.40

Case (continued)

This $9.40 is an opportunity cost. The price of the sweaters must be

high enough to cover this opportunity cost. In addition, the company

must be able to cover all of its variable costs from the time the raw wool

is purchased until the sweater is completed. Therefore, the minimum

price is:

Variable costs of producing a spindle of yarn:

Raw wool ……………………………………………

$7.00

Direct labor …………………………………………

3.60

$10.60

Added variable costs of producing a sweater:

Buttons, etc. ………………………………………..

2.00

Direct labor …………………………………………

5.80

7.80

Total variable costs ………………………………….

18.40

Opportunity cost—contribution margin if the

yarn is sold outright ………………………………

9.40

Minimum selling price per sweater ………………

$27.80