Exercise 8-12 (45 minutes)

1. The planning budget based on 3 courses and 45 students appears

below:

Gourmand Cooking School

Planning Budget

For the Month Ended September 30

Budgeted courses (q1) ……………………………………….

3

Budgeted students (q2) ………………………………………

45

Revenue ($800q2) …………………………………………….

$36,000

Expenses:

Instructor wages ($3,080q1) ……………………………..

9,240

Classroom supplies ($260q2) …………………………….

11,700

Utilities ($870 + $130q1) ………………………………….

1,260

Campus rent ($4,200) ……………………………………..

4,200

Insurance ($1,890) …………………………………………

1,890

Administrative expenses ($3,270 + $15q1 +$4q2) ….

3,495

Total expense ………………………………………………….

31,785

Net operating income ………………………………………..

$ 4,215

2. The flexible budget based on 3 courses and 42 students appears below:

Gourmand Cooking School

Flexible Budget

For the Month Ended September 30

Actual courses (q1) ……………………………………………

3

Actual students (q2) …………………………………………..

42

Revenue ($800q2) …………………………………………….

$33,600

Expenses:

Instructor wages ($3,080q1) ……………………………..

9,240

Classroom supplies ($260q2) …………………………….

10,920

Utilities ($870 + $130q1) ………………………………….

1,260

Campus rent ($4,200) ……………………………………..

4,200

Insurance ($1,890) …………………………………………

1,890

Administrative expenses ($3,270 + $15q1 +$4q2) ….

3,483

Total expense ………………………………………………….

30,993

Net operating income ………………………………………..

$ 2,607

Exercise 8-12 (continued)

3. The revenue and spending variances for September appears below:

Gourmand Cooking School

Revenue and Spending Variances

For the Month Ended September 30

Actual

Results

Revenue

and

Spending

Variances

Flexible

Budget

Courses (q1) …………………………....

3

3

Students (q2) …………………………...

42

42

Revenue ($800q2) ……………………..

$32,400

$1,200

U

$33,600

Expenses:

Instructor wages ($3,080q1) ……..

9,080

160

F

9,240

Classroom supplies ($260q2) ……..

8,540

2,380

F

10,920

Utilities ($870 + $130q1) ………….

1,530

270

U

1,260

Campus rent ($4,200) ………………

4,200

0

4,200

Insurance ($1,890) ………………….

1,890

0

1,890

Administrative expenses

($3,270 + $15q1 +$4q2) ………..

3,790

307

U

3,483

Total expense …………………………..

29,030

1,963

F

30,993

Net operating income …………………

$ 3,370

$ 763

F

$ 2,607

Exercise 8-13 (20 minutes)

1.

Actual Quantity

of Input, at

Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

20,000 pounds ×

$2.35 per pound

20,000 pounds ×

$2.50 per pound

18,400 pounds* ×

$2.50 per pound

= $47,000

= $50,000

= $46,000

Price Variance =

$3,000 F

Quantity Variance =

$4,000 U

Spending Variance = $1,000 U

*4,000 units × 4.6 pounds per unit = 18,400 pounds

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

Exercise 8-13 (continued)

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

750 hours ×

$12.00 per hour

800 hours* ×

$12.00 per hour

$10,425

= $9,000

= $9,600

Rate Variance =

$1,425 U

Efficiency Variance =

$600 F

Spending Variance = $825 U

*4,000 units × 0.2 hours per unit = 800 hours

Alternatively, the variances can be computed using the formulas:

Exercise 8-14 (15 minutes)

Notice in the solution below that the materials price variance is

computed for the entire amount of materials purchased, whereas the

materials quantity variance is computed only for the amount of materials

used in production.

Actual Quantity of

Input, at Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

20,000 pounds ×

$2.35 per pound

20,000 pounds ×

$2.50 per pound

13,800 pounds* ×

$2.50 per pound

= $47,000

= $50,000

= $34,500

Price Variance =

$3,000 F

14,750 pounds × $2.50 per pound = $36,875

Quantity Variance =

$2,375 U

*3,000 units × 4.6 pounds per unit = 13,800 pounds

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

Exercise 8-15 (20 minutes)

Via Gelato

Revenue and Spending Variances

For the Month Ended June 30

Actual

Results

Flexible

Budget

Revenue and

Spending

Variances

Liters (q) ……………………………….

6,200

6,200

Revenue ($12.00q) ………………….

$71,540

$74,400

$2,860

U

Expenses:

Raw materials ($4.65q) ………….

29,230

28,830

400

U

Wages ($5,600 + $1.40q) ………

13,860

14,280

420

F

Utilities ($1,630 + $0.20q) ………

3,270

2,870

400

U

Rent ($2,600) ………………………

2,600

2,600

0

Insurance ($1,350) ……………….

1,350

1,350

0

Miscellaneous ($650 + $0.35q) ..

2,590

2,820

230

F

Total expense …………………………

52,900

52,750

150

U

Net operating income ……………….

$18,640

$21,650

$3,010

U

Exercise 8-16 (45 minutes)

1. The planning budget appears below. Note that the report does not

include revenue or net operating income because the production

department is a cost center that does not have any revenue.

Packaging Solutions Corporation

Production Department Planning Budget

For the Month Ended March 31

Budgeted labor-hours (q) ………………………..

8,000

Direct labor ($15.80q) …………………………….

$126,400

Indirect labor ($8,200 + $1.60q) ……………….

21,000

Utilities ($6,400 + $0.80q) ……………………….

12,800

Supplies ($1,100 + $0.40q) ……………………..

4,300

Equipment depreciation ($23,000 + $3.70q) ..

52,600

Factory rent ($8,400) ……………………………..

8,400

Property taxes ($2,100) …………………………..

2,100

Factory administration ($11,700 + $1.90q) ….

26,900

Total expense ……………………………………….

$254,500

2. The flexible budget appears below. Like the planning budget, this report

does not include revenue or net operating income because the

production department is a cost center that does not have any revenue.

Packaging Solutions Corporation

Production Department Flexible Budget

For the Month Ended March 31

Actual labor-hours (q) …………………………....

8,400

Direct labor ($15.80q) …………………………….

$132,720

Indirect labor ($8,200 + $1.60q) ……………….

21,640

Utilities ($6,400 + $0.80q) ……………………….

13,120

Supplies ($1,100 + $0.40q) ……………………..

4,460

Equipment depreciation ($23,000 + $3.70q) ..

54,080

Factory rent ($8,400) ……………………………..

8,400

Property taxes ($2,100) …………………………..

2,100

Factory administration ($11,700 + $1.90q) ….

27,660

Total expense ……………………………………….

$264,180

Exercise 8-16 (continued)

3. The spending variances appear below. This report does not include

revenue or net operating income because the production department is

a cost center that does not have any revenue.

Packaging Solutions Corporation

Spending Variances

For the Month Ended March 31

Actual

Results

Spending

Variances

Flexible

Budget

Labor-hours (q) ………………………….

8,400

8,400

Direct labor ($15.80q) ………………….

$134,730

$2,010

U

$132,720

Indirect labor ($8,200 + $1.60q) ……

19,860

1,780

F

21,640

Utilities ($6,400 + $0.80q)…………….

14,570

1,450

U

13,120

Supplies ($1,100 + $0.40q) …………..

4,980

520

U

4,460

Equipment depreciation

($23,000 + $3.70q) …………………..

54,080

0

54,080

Factory rent ($8,400) …………………..

8,700

300

U

8,400

Property taxes ($2,100) ………………..

2,100

0

2,100

Factory administration

($11,700 + $1.90q) …………………..

26,470

1,190

F

27,660

Total expense …………………………….

$265,490

$1,310

U

$264,180

Exercise 8-17 (30 minutes)

1. a. Notice in the solution below that the materials price variance is

computed on the entire amount of materials purchased, whereas the

materials quantity variance is computed only on the amount of

materials used in production.

Actual Quantity

of Input, at

Actual Price

Actual Quantity of

Input, at Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

25,000 microns ×

$0.48 per micron

25,000 microns ×

$0.50 per micron

18,000 microns* ×

$0.50 per micron

= $12,000

= $12,500

= $9,000

Price Variance =

$500 F

20,000 microns × $0.50 per micron

= $10,000

Quantity Variance =

$1,000 U

*3,000 toys × 6 microns per toy = 18,000 microns

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

Exercise 8-17 (continued)

b. Direct labor variances:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours Allowed

for Output, at the

Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

4,000 hours ×

$8.00 per hour

3,900 hours* ×

$8.00 per hour

$36,000

= $32,000

= $31,200

Rate Variance =

$4,000 U

Efficiency Variance =

$800 U

Spending Variance = $4,800 U

*3,000 toys × 1.3 hours per toy = 3,900 hours

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

4,000 hours ($9.00 per hour* – $8.00 per hour) = $4,000 U

*$36,000 ÷ 4,000 hours = $9.00 per hour

Labor efficiency variance = SR (AH – SH)

$8.00 per hour (4,000 hours – 3,900 hours) = $800 U

Exercise 8-17 (continued)

2. A variance usually has many possible explanations. In particular, we

should always keep in mind that the standards themselves may be

incorrect. Some of the other possible explanations for the variances

observed at Dawson Toys appear below:

Materials Price Variance

Since this variance is favorable, the actual price

Labor Rate Variance

Since this variance is unfavorable, the actual

average wage rate was higher than the standard wage rate. Some of

the possible explanations include an increase in wages that has not been

reflected in the standards, unanticipated overtime, and a shift toward

more highly paid workers.

Problem 8-18A (45 minutes)

1. a.

Actual Quantity of

Input, at Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

60,000 pounds ×

$1.95 per pound

60,000 pounds ×

$2.00 per pound

45,000 pounds* ×

$2.00 per pound

= $117,000

= $120,000

= $90,000

Price Variance =

$3,000 F

49,200 pounds × $2.00 per pound = $98,400

Quantity Variance =

$8,400 U

*15,000 pools × 3.0 pounds per pool = 45,000 pounds

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

60,000 pounds ($1.95 per pound – $2.00 per pound) = $3,000 F

Materials quantity variance = SP (AQ – SQ)

$2.00 per pound (49,200 pounds – 45,000 pounds) = $8,400 U

Problem 8-18A (continued)

b.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

11,800 hours ×

$7.00 per hour

11,800 hours ×

$6.00 per hour

12,000 hours* ×

$6.00 per hour

= $82,600

= $70,800

= $72,000

Rate Variance =

$11,800 U

Efficiency Variance =

$1,200 F

Spending Variance = $10,600 U

*15,000 pools × 0.8 hours per pool = 12,000 hours

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

11,800 hours ($7.00 per hour – $6.00 per hour) = $11,800 U

Labor efficiency variance = SR (AH – SH)

$6.00 per hour (11,800 hours – 12,000 hours) = $1,200 F

Problem 8-18A (continued)

c.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,900 hours ×

$3.00 per hour

6,000 hours* ×

$3.00 per hour

$18,290

= $17,700

= $18,000

Rate Variance =

$590 U

Efficiency Variance =

$300 F

Spending Variance = $290 U

*15,000 pools × 0.4 hours per pool = 6,000 hours

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR – SR)

5,900 hours ($3.10 per hour* – $3.00 per hour) = $590 U

*$18,290 ÷ 5,900 hours = $3.10 per hour

Variable overhead efficiency variance = SR (AH – SH)

$3.00 per hour (5,900 hours – 6,000 hours) = $300 F

Problem 8-18A (continued)

2. Summary of variances:

Material price variance ……………………..

$ 3,000

F

Material quantity variance …………………

8,400

U

Labor rate variance ………………………….

11,800

U

Labor efficiency variance …………………..

1,200

F

Variable overhead rate variance ………….

590

U

Variable overhead efficiency variance …..

300

F

Net variance …………………………………..

$16,290

U

Budgeted cost of goods sold at $12 per pool ………

$180,000

Add the net unfavorable variance, as above ……….

16,290

Actual cost of goods sold ……………………………….

$196,290

Budgeted net operating income ……………………….

$36,000

Deduct the net unfavorable variance added to cost

of goods sold for the month …………………………

16,290

Net operating income ……………………………………

$19,710

3. The two most significant variances are the materials quantity variance

and the labor rate variance. Possible causes of the variances include:

Materials quantity variance:

Outdated standards, unskilled workers,

poorly adjusted machines,

carelessness, poorly trained workers,

inferior quality materials.

Labor rate variance:

Outdated standards, change in pay

scale, overtime pay.

Problem 8-19A (30 minutes)

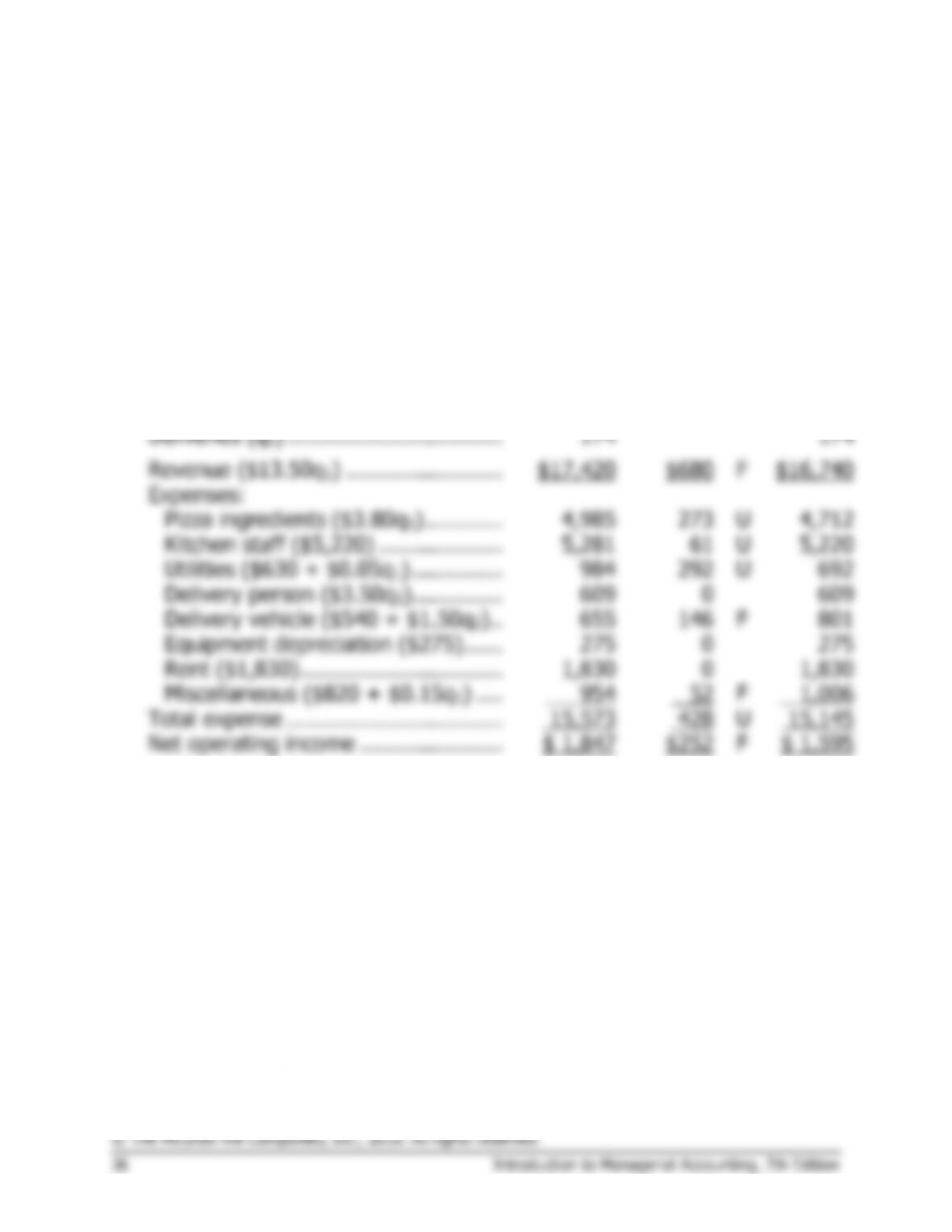

1.

Milano Pizza

Revenue and Spending Variances

For the Month Ended November 30

Actual

Results

Revenue

and

Spending

Variances

Flexible

Budget

Pizzas (q1) …………………………..……

1,240

1,240

Deliveries (q2) …………………………...

174

174

Revenue ($13.50q1) ……………………

$17,420

$680

F

$16,740

Expenses:

Pizza ingredients ($3.80q1) …………

4,985

273

U

4,712

Kitchen staff ($5,220) ……………….

5,281

61

U

5,220

Utilities ($630 + $0.05q1) …………..

984

292

U

692

Delivery person ($3.50q2)…………..

609

0

609

Delivery vehicle ($540 + $1.50q2) ..

655

146

F

801

Equipment depreciation ($275) ……

275

0

275

Rent ($1,830) ………………………….

1,830

0

1,830

Miscellaneous ($820 + $0.15q1) ….

954

52

F

1,006

Total expense …………………………...

15,573

428

U

15,145

Net operating income ………………….

$ 1,847

$252

F

$ 1,595

Problem 8-19A (continued)

2. The revenue variance of $680 F indicates that the average price per

pizza was higher than expected. Perhaps customers ordered more

toppings on their pizzas than expected. The pizza ingredients variance

Problem 8-20A (45 minutes)

1. a.

Actual Quantity of Input,

at Actual Price

(AQ × AP)

Actual Quantity of

Input,

at Standard Price

(AQ × SP)

Standard Quantity

Allowed

for Actual Output,

at Standard Price

(SQ × SP)

21,600 feet** ×

$3.30 per foot

= $71,280

21,600 feet** ×

$3.00 per foot

= $64,800

21,600 feet* ×

$3.00 per foot

= $64,800

Materials price variance =

$6,480 U

Materials quantity

variance = $0

Spending variance = $6,480 U

*

12,000 units × 1.80 feet per unit = 21,600 feet

**

12,000 units × 1.80 feet per unit = 21,600 feet

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

= 21,600 feet ($3.30 per foot – $3.00 per foot)

= $6,480 U

Materials quantity variance = SP (AQ – SQ)

= $3.00 per foot (21,600 feet – 21,600 feet)

= $0

Problem 8-20A (continued)

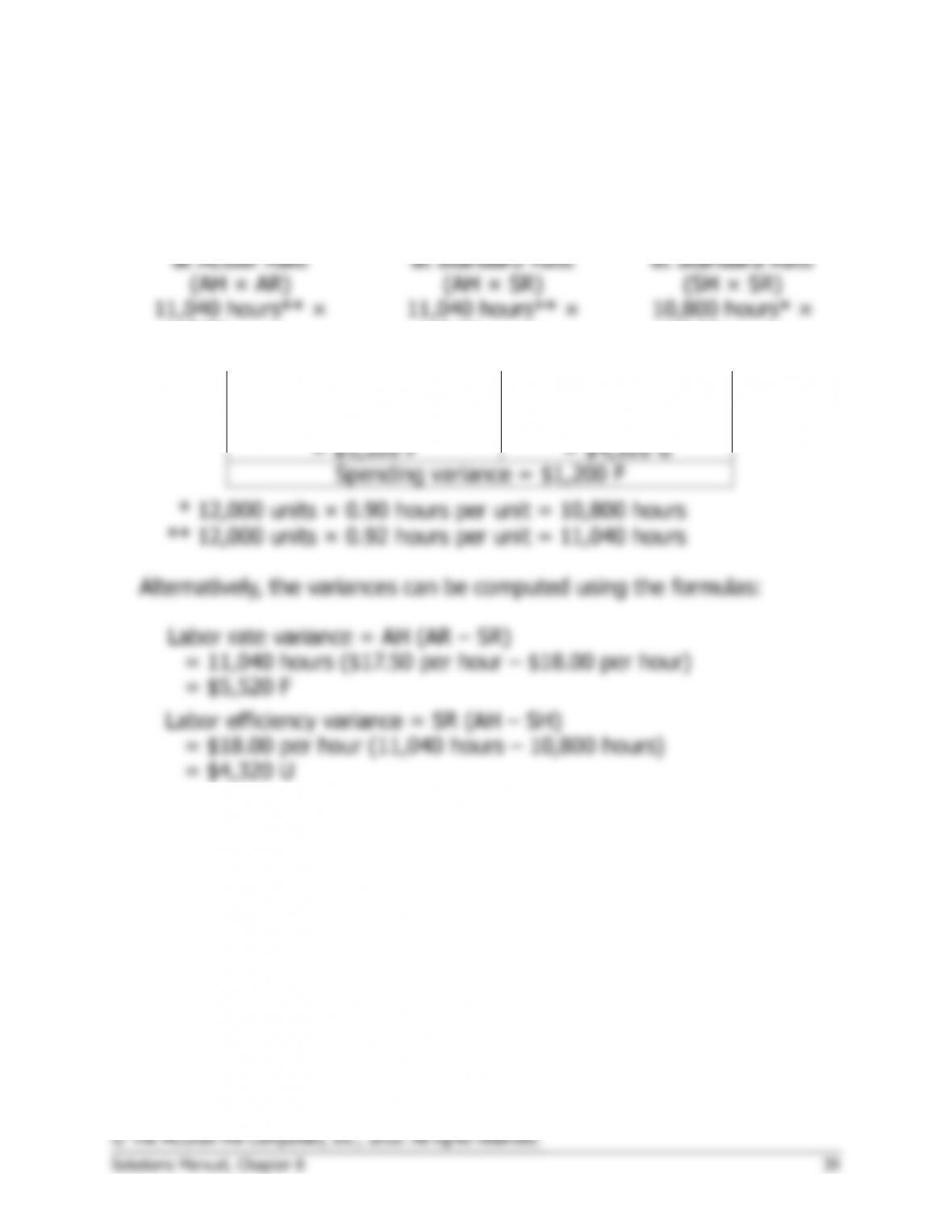

1. b.

Actual Hours of Input,

at Actual Rate

(AH × AR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

11,040 hours** ×

$17.50 per hour

= $193,200

11,040 hours** ×

$18.00 per hour

= $198,720

10,800 hours* ×

$18.00 per hour

= $194,400

Labor rate variance

= $5,520 F

Labor efficiency

variance

= $4,320 U

Spending variance = $1,200 F

*

12,000 units × 0.90 hours per unit = 10,800 hours

**

12,000 units × 0.92 hours per unit = 11,040 hours

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

= 11,040 hours ($17.50 per hour – $18.00 per hour)

= $5,520 F

Labor efficiency variance = SR (AH – SH)

= $18.00 per hour (11,040 hours – 10,800 hours)

= $4,320 U

Problem 8-20A (continued)

1. c.

Actual Hours of Input,

at Actual Rate

(AH × AR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

11,040 hours** ×

$4.50 per hour

= $49,680

11,040 hours** ×

$5.00 per hour

= $55,200

10,800 hours* ×

$5.00 per hour

= $54,000

Variable overhead rate

variance = $5,520 F

Variable overhead

efficiency variance

= $1,200 U

Spending variance = $4,320 F

*

12,000 units × 0.90 hours per unit = 10,800 hours

**

12,000 units × 0.92 hours per unit = 11,040 hours

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR – SR)

= 11,040 hours ($4.50 per hour – $5.00 per hour)

= $5,520 F

Variable overhead efficiency variance = SR (AH – SH)

= $5.00 per hour (11,040 hours – 10,800 hours)

= $1,200 U

2.

Materials:

Price variance ($6,480 ÷ 12,000 units) ………..

$0.54 U

Quantity variance ($0 ÷ 12,000 units) …………

0.00

$0.54 U

Labor:

Rate variance ($5,520 ÷ 12,000 units) ………..

0.46 F

Efficiency variance ($4,320 ÷ 12,000 units) ….

0.36 U

0.10 F

Variable overhead:

Rate variance ($5,520 ÷ 12,000 units) ………..

0.46 F

Efficiency variance ($1,200 ÷ 12,000 units) ….

0.10 U

0.36 F

Excess of actual over standard cost per unit ……..

$0.08 U