Problem 11-25A (continued)

2. Considering all three investments together, Linda did not earn a 16%

rate of return. The computation is:

Net

Present

Value

Common stock …………………….

$ 7,560

Preferred stock …………………….

(8,650)

Bonds ………………………………..

(2,743)

Overall net present value ……….

$(3,833)

The defect in the broker’s computation is that it does not consider the

time value of money and therefore has overstated the rate of return

earned.

3.

Investment required

Factor of the internal =

rate of return Annual net cash inflow

Ethics Challenge (45 minutes)

1. Rachel Arnett’s revision of her first proposal can be considered a

violation of the IMA’s Statement of Ethical Professional Practice. She

discarded her reasonable projections and estimates after she was

questioned by William Earle. She used figures that had a remote chance

2. Earle was clearly in violation of the Standards of Ethical Conduct for

Management Accountants because he tried to persuade a subordinate to

prepare a proposal with data that was false and misleading. Earle has

Ethics Challenge (continued)

3. The internal controls Fore Corporation could implement to prevent

unethical behavior include:

approval of all formal capital expenditure proposals by the Controller

and/or the Board of Directors.

Case (45 minutes)

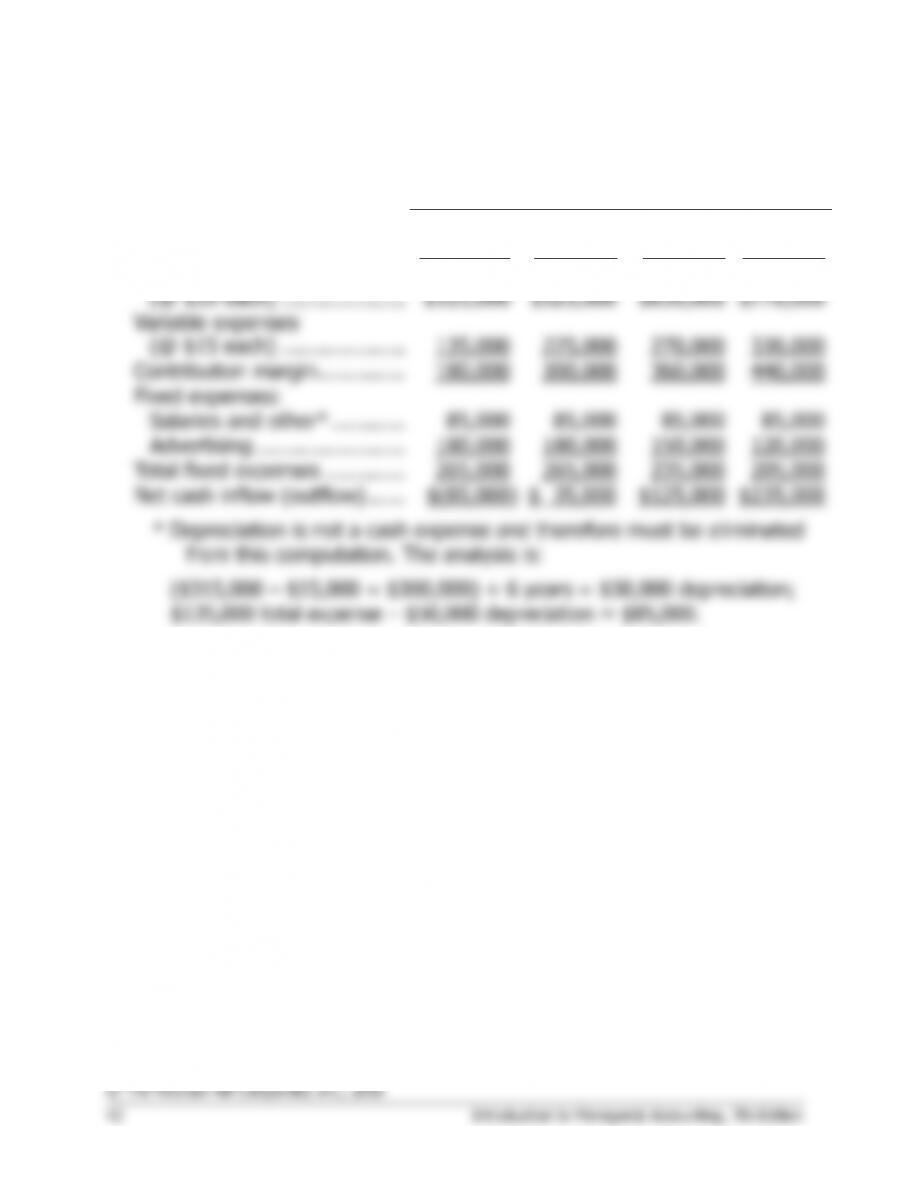

1. The net cash inflow from sales of the device for each year would be:

Year

1

2

3

4-6

Sales in units ……………………

9,000

15,000

18,000

22,000

Sales in dollars

(@ $35 each) ………………..

$315,000

$525,000

$630,000

$770,000

Variable expenses

(@ $15 each) ………………..

135,000

225,000

270,000

330,000

Contribution margin …………..

180,000

300,000

360,000

440,000

Fixed expenses:

Salaries and other* …………

85,000

85,000

85,000

85,000

Advertising ……………………

180,000

180,000

150,000

120,000

Total fixed expenses ………….

265,000

265,000

235,000

205,000

Net cash inflow (outflow) ……

$(85,000)

$ 35,000

$125,000

$235,000

*

Depreciation is not a cash expense and therefore must be eliminated

from this computation. The analysis is:

($315,000 – $15,000 = $300,000) ÷ 6 years = $50,000 depreciation;

$135,000 total expense – $50,000 depreciation = $85,000.

Case (continued)

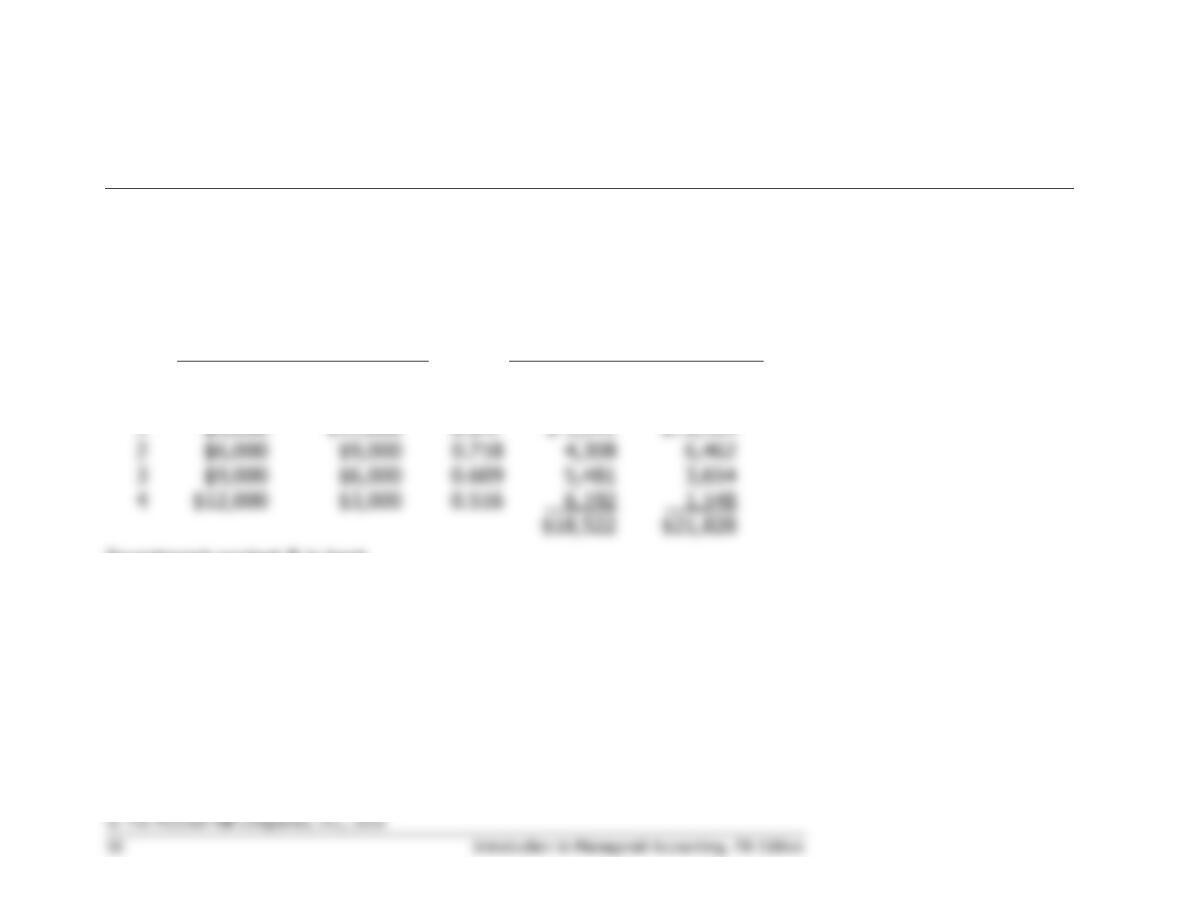

2. The net present value of the proposed investment would be:

Now

1

2

3

4

5

6

Cost of equipment …

$(315,000)

Working capital ……..

(60,000)

Yearly net cash

flows …………………..

$(85,000)

$35,000

$125,000

$235,000

$235,000

$235,000

Release of working

capital …………………

60,000

Salvage value of

equipment ……………

_______

______

______

______

______

______

15,000

Total cash flows (a) .

$(375,000)

$(85,000)

$35,000

$125,000

$235,000

$235,000

$310,000

Discount factor

(14%) (b) ……………

1.000

0.877

0.769

0.675

0.592

0.519

0.456

Present value

(a)×(b) ……………….

$(375,000)

$(74,545)

$26,915

$84,375

$139,120

$121,965

$141,360

Net present value ….

$64,190

Chapter 11

Take Two Solutions

Exercise 11-1 (10 minutes)

1. The payback period is determined as follows:

Year

Investment

Cash Inflow

Unrecovered

Investment

1

$17,500

$1,000

$16,500

2

$8,000

$2,000

$22,500

3

$2,500

$20,000

4

$4,000

$16,000

5

$5,000

$11,000

6

$6,000

$5,000

7

$5,000

$0

8

$4,000

$0

9

$3,000

$0

10

$2,000

$0

The investment in the project is fully recovered in the 7th year. The

payback period is 7.0 years.

2. Because the investment is recovered prior to the last year, the amount

Exercise 11-2 (10 minutes)

1.

Now

1

2

3

4

5

Purchase of machine ………………….

$(27,000)

Reduced operating costs …………….

________

$7,000

$7,000

$7,000

$7,000

$7,000

Total cash flows (a) …………………..

$(27,000)

$7,000

$7,000

$7,000

$7,000

$7,000

Discount factor (10%) (b) …………..

1.000

0.909

0.826

0.751

0.683

0.621

Present value (a)×(b) ………………..

$(27,000)

$6,363

$5,782

$5,257

$4,781

$4,347

Net present value ……………………..

$(470)

Note: The annual reduction in operating costs can also be converted to its present value using the

discount factor of 3.791 as shown in Exhibit 11B-2 in Appendix 11B.

2.

Item

Cash

Flow

Years

Total

Cash

Flows

Annual cost savings ..

$7,000

5

$ 35,000

Initial investment …..

$(27,000)

1

(27,000)

Net cash flow ………..

$ 8,000

Exercise 11-4 (10 minutes)

This is a cost reduction project, so the simple rate of return would be

computed as follows:

Operating cost of old machine ………………..

$ 30,000

Less operating cost of new machine ………..

12,000

Less annual depreciation on the new

machine ($120,000 ÷ 8 years) ……………..

15,000

Annual incremental net operating income …

$ 3,000

Cost of the new machine ………………………

$120,000

Scrap value of old machine ……………………

40,000

Initial investment …………………………………

$ 80,000

Annual incremental net operating income

Simple rate =

of return Initial investment

$3,000

= = 3.75%

$80,000

Exercise 11-6 (15 minutes)

1. Computation of the annual cash inflow associated with the new

electronic games:

Net operating income ……………………………………

$50,000

Add noncash deduction for depreciation …………….

35,000

Annual net cash inflow …………………………..………

$85,000

The payback computation would be:

Investment required

Payback period = Annual net cash inflow

$300,000

= = 3.53 years

$85,000 per year

Yes, the games would be purchased. The payback period is less than

the maximum 5 years required by the company.

2. The simple rate of return would be:

Annual incremental net income

Simple rate =

of return Initial investment

Exercise 11-8 (10 minutes)

Now

1

2

3

Purchase of stock…………………………

$(13,000)

Annual cash dividend ……………………

$500

$500

$ 500

Sale of stock ……………………………….

_______

____

____

16,000

Total cash flows (a) ……………………..

$(13,000)

$500

$500

$16,500

Discount factor (14%) (b) ……………..

1.000

0.877

0.769

0.675

Present value (a)×(b) …………………..

$(13,000)

$439

$385

$11,138

Net present value ………………………..

$(1,038)

No, Kathy did not earn a 14% return on the Malti Company stock. The negative net present value

indicates that the rate of return on the investment is less than the minimum required rate of return of

14%.

Exercise 11-11 (10 minutes)

Project X:

Now

1

2

3

4

5

6

Initial investment …………..

$(35,000)

Annual cash inflows ……….

________

$12,000

$12,000

$12,000

$12,000

$12,000

$12,000

Total cash flows (a) ……….

$(35,000)

$12,000

$12,000

$12,000

$12,000

$12,000

$12,000

Discount factor (15%) (b) .

1.000

0.870

0.756

0.658

0.572

0.497

0.432

Present value (a)×(b) …….

$(35,000)

$10,440

$9,072

$7,896

$6,864

$5,964

$5,184

Net present value ………….

$10,420

Initial investment …………..

Single cash inflow ………….

______

______

______

______

90,000

Total cash flows (a) ……….

$90,000

Discount factor (15%) (b) .

0.870

0.756

0.658

0.572

0.497

Present value (a)×(b) …….

$38,880

Net present value ………….

Appendix 11A

The Concept of Present Value

Exercise 11A-1 (10 minutes)

Amount of Cash Flows

18%

Present Value of Cash

Flows

Year

Investment

A

Investment

B

Factor

Investment

A

Investment

B

1

$3,000

$12,000

0.847

$ 2,541

$10,164

2

$6,000

$9,000

0.718

4,308

6,462

3

$9,000

$6,000

0.609

5,481

3,654

4

$12,000

$3,000

0.516

6,192

1,548

$18,522

$21,828

Investment project B is best.

Exercise 11A-2 (10 minutes)

The present value of the first option is $150,000, since the entire amount would be received

immediately.

Exercise 11A-3 (10 minutes)

1. From Exhibit 11B-1, the factor for 10% for 3 periods is 0.751. Therefore, the present value of the

2. From Exhibit 11B-1, the factor for 14% for 3 periods is 0.675. Therefore, the present value of the

Exercise 11A-4 (10 minutes)

1. From Exhibit 11B-1, the factor for 10% for 5 periods is 0.621. Therefore, the company must invest:

2. From Exhibit 11B-1, the factor for 14% for 5 periods is 0.519. Therefore, the company must invest:

Exercise 11A-5 (10 minutes)

1. From Exhibit 11B-2, the factor for 16% for 8 periods is 4.344. The computer system should be

2. From Exhibit 11B-2, the factor for 20% for 8 periods is 3.837. Therefore, the maximum purchase

Exercise 11A-6 (10 minutes)

1. From Exhibit 11B-2, the factor for 12% for 20 periods is 7.469. Thus, the present value of Mr.

2. Whether or not it is correct to say that Mr. Ormsby is the state’s newest millionaire depends on your