Archives

978-0078025679 Chapter 1 Lecture Note

Financial Reporting and Analysis 6e The Economic and Institutional Setting for Financial Reporting CHAPTER 1 THE ECONOMIC AND INSTITUTIONAL SETTING FOR FINANCIAL REPORTING CHAPTER OVERVIEW Financial statements contain information about a company, its economic health, and its products that help […]

978-0078025679 Chapter 1 Solution Manual Part 1

1-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (6th Ed.) Chapter 1 Solutions The Economic and Institutional Setting for Financial Reporting Problems Problems […]

978-0078025679 Chapter 1 Solution Manual Part 2

1-14 1) By identifying the key business and financial risks facing the company, the audit committee can ensure that those risks are properly disclosed in the MD&A (Management Discussion & Analysis) section of the annual report. A second reason is […]

978-0078025679 Chapter 10 Lecture Note

Financial Reporting and Analysis 6e Long-Lived Assets CHAPTER 10 LONG-LIVED ASSETS CHAPTER OVERVIEW Generally accepted accounting principles for long–lived assets are far from perfect. The need for reliable (unbiased and accurate), cost–effective, and objective (verifiable) numbers causes these assets to […]

978-0078025679 Chapter 10 Solution Manual Part 1

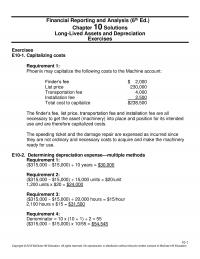

Financial Reporting and Analysis (6th Ed.) Chapter 10 Solutions Long-Lived Assets and Depreciation Exercises Exercises E10–1. Capitalizing costs Requirement 1: Phoenix may capitalize the following costs to the Machine account: Finder’s fee $ 2,000 List price 230,000 Transportation fee 4,000 […]

978-0078025679 Chapter 10 Solution Manual Part 2

10–16 P10–7. Determining asset impairment Requirement 1: Book value: = $35,000,000 – [($35,000,000/7) x 4] = $35,000,000 – 20,000,000 = $15,000,000 Requirement 2: Yes, the asset is impaired. The book value of $15,000,000 is greater than the undiscounted future cash […]

978-0078025679 Chapter 10 Solution Manual Part 3

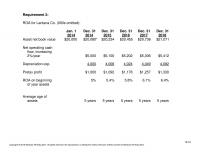

10–31 Requirement 2: ROA for Lantana Co. (000s omitted): Jan. 1 Dec. 31 Dec. 31 Dec. 31 Dec. 31 Dec. 31 2014 2014 2015 2016 2017 2018 Asset net book value $20,000 $20,080* $20,234 $20,455 $20,736 $21,071 Net operating cash […]

978-0078025679 Chapter 10 Solution Manual Part 4

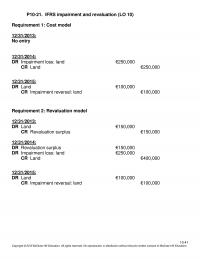

10–41 P10–21. IFRS impairment and revaluation (LO 10) Requirement 1: Cost model 12/31/2013: No entry 12/31/2014: DR Impairment loss: land €250,000 CR Land €250,000 12/31/2015: DR Land €100,000 CR Impairment reversal: land €100,000 Requirement 2: Revaluation model 12/31/2013: DR Land […]

978-0078025679 Chapter 11 Lecture Note

Financial Reporting and Analysis 6e Financial Instruments as Liabilities CHAPTER 11 FINANCIAL INSTRUMENTS AS LIABILITIES CHAPTER OVERVIEW A financial statement liability is (1) a currently existing obligation arising from past events, which necessitates (2) payment of cash, or provision of […]

978-0078025679 Chapter 11 Solution Manual Part 1

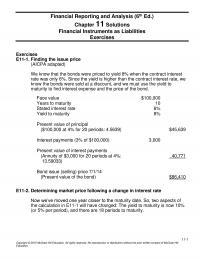

11-1 Financial Reporting and Analysis (6th Ed.) Chapter 11 Solutions Financial Instruments as Liabilities Exercises Exercises E11–1. Finding the issue price (AICPA adapted) We know that the bonds were priced to yield 8% when the contract interest rate was only […]

978-0078025679 Chapter 11 Solution Manual Part 2

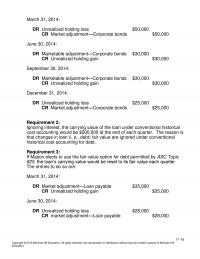

11–16 March 31, 2014: DR Unrealized holding loss $50,000 CR Market adjustment—Corporate bonds $50,000 June 30, 2014: DR Marketable adjustment—Corporate bonds $30,000 CR Unrealized holding gain $30,000 September 30, 2014: DR Marketable adjustment—Corporate bonds $30,000 CR Unrealized holding gain $30,000 […]

978-0078025679 Chapter 11 Solution Manual Part 3

11–31 It does not appear as though Checkpoint Systems has already recognized a loss contingency reserve related to this law suit because there is no mention of a recorded loss accrual or provision. (By comparison, notice what Visa has to […]

978-0078025679 Chapter 11 Solution Manual Part 4

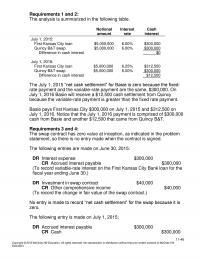

11–46 Requirements 1 and 2: The analysis is summarized in the following table. Notional amount Interest rate Cash interest July 1, 2015: First Kansas City loan $5,000,000 6.00% $300,000 Quincy B&T swap $5,000,000 6.00% $300,000 Difference in cash interest $0 […]

978-0078025679 Chapter 11 Solution Manual Part 5

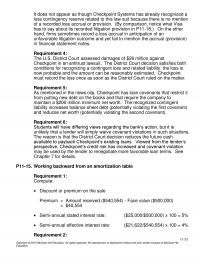

11–54 The issue price would by $219.231 million if the market yield is 8.125% and $290.816 million if the market yield is 6.125%. Requirement 8: Century and millennium bonds share a common feature: a very large share of the issue […]

978-0078025679 Chapter 12 Lecture Note

Financial Reporting and Analysis 6e Financial Reporting for Leases CHAPTER 12 FINANCIAL REPORTING FOR LEASES Chapter Overview The treatment of leases in FASB ASC 840 represents a compromise between the unperformed–contract and property-right approaches. FASB ASC 840 adopts a middle-of–the- […]

978-0078025679 Chapter 12 Solution Manual Part 1

12-1 Financial Reporting and Analysis (6th Ed.) Chapter 12 Solutions Financial Reporting for Leases Exercises Exercises E12–1. Accounting for lessee with purchase option (LO 3, 4, 5) Requirement 1: Amount capitalized by Leland at 07/01/2014 The $100,000 represents a bargain […]

978-0078025679 Chapter 12 Solution Manual Part 2

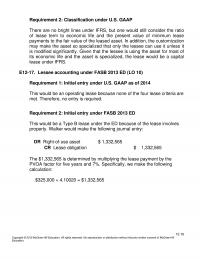

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Requirement 2: Classification under U.S. GAAP There are no bright lines under IFRS, but one would still consider the ratio […]

978-0078025679 Chapter 12 Solution Manual Part 3

12–31 P12–6. Assessing guaranteed and unguaranteed residual values for the lessee (LO 3, 4, 5) Requirement 1: This is a capital lease for Task because the lease meets at least one of the criteria for capital lease treatment. The lease […]

978-0078025679 Chapter 12 Solution Manual Part 4

12–46 Requirement 4: MONTHLY REDUCTION PAYMENT INTEREST LEASE IN RECEIVABLE DATE INCOME PAYMENTS RECEIVABLE BALANCE 09/01/14 60,000.00$ 09/01/14 –$ 1,789.20$ 1,789.20$ 58,210.80 10/01/14 582.11 1,789.20 1,207.09 57,003.71 11/01/14 570.04 1,789.20 1,219.16 55,784.55 12/01/14 557.85 1,789.20 1,231.35 54,553.20 01/01/15 545.53 1,789.20 […]

978-0078025679 Chapter 12 Solution Manual Part 5

12–61 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (5th Ed.) Chapter 12 Solutions Financial Reporting for Leases Cases Cases C12-1. AMR Corporation: Constructively […]

978-0078025679 Chapter 12 Solution Manual Part 6

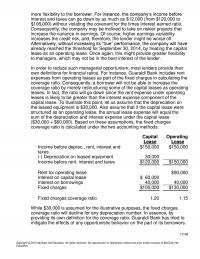

12–69 more flexibility to the borrower. For instance, the company’s income before interest and taxes can go down by as much as $12,000 (from $120,000 to $108,000) without violating the covenant for the times interest earned ratio. Consequently, the company […]

978-0078025679 Chapter 13 Lecture Note

Financial Reporting and Analysis 6e Income Tax Reporting CHAPTER 13 INCOME TAX REPORTING CHAPTER OVERVIEW The rules for computing income for financial reporting purposes—book income—differ from the rules for computing income for tax purposes. The differences between book income and […]

978-0078025679 Chapter 13 Solution Manual Part 1

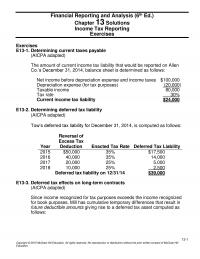

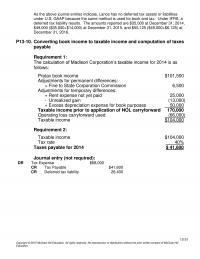

13-1 Financial Reporting and Analysis (6th Ed.) Chapter 13 Solutions Income Tax Reporting Exercises Exercises E13–1. Determining current taxes payable (AICPA adapted) The amount of current income tax liability that would be reported on Allen Co.’s December 31, 2014, balance […]

978-0078025679 Chapter 13 Solution Manual Part 2

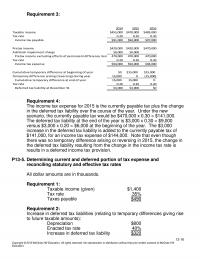

13–16 Requirement 3: 2014 2015 2016 Taxable income $455,000 $470,000 $485,000 Tax rate 0.20 0.20 0.20 Income tax payable $91,000 $94,000 $97,000 Pretax income $420,000 $420,000 $470,000 Add back impairment charge 50,000 50,000 Pretax income excluding effects of permanent difference […]

978-0078025679 Chapter 13 Solution Manual Part 3

13–31 As the above journal entries indicate, Lance has no deferred tax assets or liabilities under U.S. GAAP because the same method is used for book and tax. Under IFRS, a deferred tax liability results. The amounts reported are $35,000 […]

978-0078025679 Chapter 13 Solution Manual Part 4

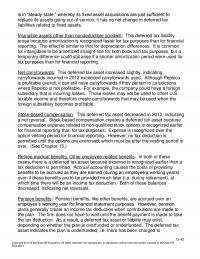

13–42 is in “steady–state,” whereby its fixed asset acquisitions are just sufficient to replace its assets going out of service, it has no net change in deferred tax liabilities related to fixed assets. Intangible assets other than nondeductible goodwill: This […]

978-0078025679 Chapter 14 Lecture Note

Financial Reporting and Analysis 6e Pensions and Postretirement Benefits CHAPTER 14 PENSIONS AND POSTRETIREMENT BENEFITS CHAPTER OVERVIEW Pension plan contracts allow employees to exchange current service for payments to be received during retirement. Defined contribution pension plans specify amounts to […]

978-0078025679 Chapter 14 Solution Manual Part 1

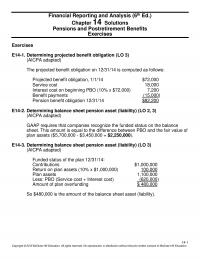

14-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (6th Ed.) Chapter 14 Solutions E14–1. Determining projected benefit obligation (LO 3) (AICPA adapted) The […]

978-0078025679 Chapter 14 Solution Manual Part 2

14–16 E14-21. Determining pension elements (LO 3, 4, 6) Requirement 1: Prior Service Cost Amortization Year ended 2014 ($650,000/20) = $32,500 Year ended 2015 ($650,000/20) = 32,500 Requirement 2: Pension Expense for 2014: Service cost $ 45,000 Interest cost ($650,000 […]

978-0078025679 Chapter 14 Solution Manual Part 3

14–31 P14–5. Calculating PBO, ABO and pension expense Requirement 1: Calculation of PBO on January 1, 2014: Annual pension benefits starting on 12/31/2029 and continuing for 10 years thereafter (11 years total = 76 – 66). Years of service credit […]

978-0078025679 Chapter 14 Solution Manual Part 4

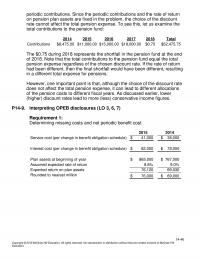

14–46 periodic contributions. Since the periodic contributions and the rate of return on pension plan assets are fixed in the problem, the choice of the discount rate cannot affect the total pension expense. To see this, let us examine the […]

978-0078025679 Chapter 14 Solution Manual Part 5

14–55 + Contributions 150.00 – Pension Benefits Paid at end of Year (350.00) = Dec 31 2013 / Jan 1 2014 PBO Balance $4,160.00 The corridor is 10% of Maximum $($6,650 PBO, $4,160 plan assets) or $665. The “cost” of […]

978-0078025679 Chapter 15 Lecture Note Part 1

Financial Reporting and Analysis 6e Financial Reporting for Owner’s Equity CHAPTER 15 FINANCIAL REPORTING FOR OWNERS’ EQUITY CHAPTER OVERVIEW Statement readers must understand accounting procedures and reporting conventions for owner’s equity for the following reasons: (1) Appropriate income measurement; (2) […]

978-0078025679 Chapter 15 Lecture Note Part 2

Financial Reporting and Analysis 6e Financial Reporting for Owner’s Equity Black–Scholes model or some other theoretically sound approach. e. The fair value of the options is expensed on a straight-line basis over the vesting period (with the offset credited to […]

978-0078025679 Chapter 15 Solution Manual Part 1

15-1 Financial Reporting and Analysis (6th Ed.) Chapter 15 Solutions Financial Reporting for Owners’ Equity Exercises Exercises E15–1. Understanding Shareholders’ Equity Requirement 1: Preferred stock is a class of “capital stock” that pays dividends at a specified rate and that […]

978-0078025679 Chapter 15 Solution Manual Part 2

15–16 The year-end balance in retained earnings is $99,027 so the maximum legal dividend would be this amount plus dividends paid for the year, or $102,203, assuming the 1984 Revised Model Business Corporation Act does not apply. Requirement 5: Neither […]

978-0078025679 Chapter 15 Solution Manual Part 3

15–28 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (6th Ed.) Chapter 15 Solutions Financial Reporting for Owners’ Equity Cases Cases C15-1. Groupe Casino: […]

978-0078025679 Chapter 16 Lecture Note

Financial Reporting and Analysis 6e Intercorporate Equity Investments CHAPTER 16 INTERCORPORATE EQUITY INVESTMENTS CHAPTER OVERVIEW Financial reporting for intercorporate equity investments depends upon the degree to which the investor is able to influence the investee’s operating decisions. Proportionate share size […]

978-0078025679 Chapter 16 Solution Manual Part 1

16-1 Financial Reporting and Analysis (6th Ed.) Chapter 16 Solutions Intercorporate Equity Investments Exercises Exercises E16–1. Fair value accounting for trading and available-for-sale securities (AICPA adapted) Requirement 1: Only the unrealized holding gains/losses from trading securities are recognized as income. […]

978-0078025679 Chapter 16 Solution Manual Part 2

16–16 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 16–17 Dollar carrying value of payable at January 1, 2015 ($140,000 – $2,000) $138,000 Dollar equivalent of settlement amount […]

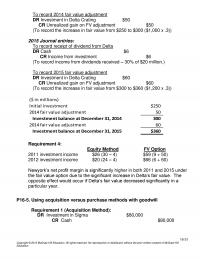

978-0078025679 Chapter 16 Solution Manual Part 3

16–31 To record 2014 fair value adjustment DR Investment in Delta Crating $50 CR Unrealized gain on FV adjustment $50 (To record the increase in fair value from $250 to $300 ($1,000 x .3)) 2015 Journal entries: To record receipt […]

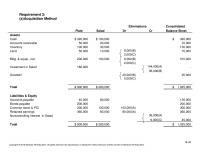

978-0078025679 Chapter 16 Solution Manual Part 4

16–45 Requirement 3: (a) Acquisition Method Plate Salad Eliminations Consolidated Dr Cr Balance Sheet Assets Cash $ 320,000 $ 100,000 $ 420,000 Accounts receivable 50,000 20,000 70,000 Inventory 100,000 30,000 130,000 Land 50,000 10,000 8,000(B) 70,000 2,000(C) Bldg. & equip., […]

978-0078025679 Chapter 17 Lecture Note

Financial Reporting and Analysis 6e Statement of Cash Flows CHAPTER 17 STATEMENT OF CASH FLOWS CHAPTER OVERVIEW The statement of cash flows provides information for assessing the the firm’s ability to generate sufficient cash to pay operating expenses, pay for […]

978-0078025679 Chapter 17 Solution Manual Part 1

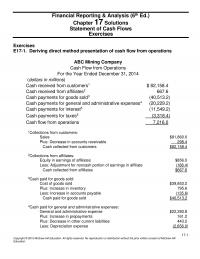

17-1 Financial Reporting & Analysis (6th Ed.) Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Deriving direct method presentation of cash flow from operations ABC Mining Company Cash Flow from Operations For the Year Ended December 31, 2014 […]

978-0078025679 Chapter 17 Solution Manual Part 2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Bl dgs. Def. Mkt. A/R Ppd. and Acc. Inta ng. Accrd. Accrd. Def. Inc. Tx. Notes Inc. Com. Re t. […]

978-0078025679 Chapter 17 Solution Manual Part 3

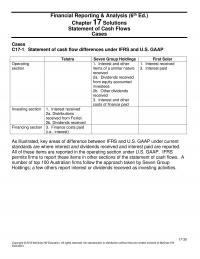

Financial Reporting & Analysis (6th Ed.) Chapter 17 Solutions Statement of Cash Flows Cases Cases C17-1. Statement of cash flow differences under IFRS and U.S. GAAP Telstra Seven Group Holdings First Solar Operating section 1. Interest and other items of […]

978-0078025679 Chapter 2 Lecture Note

Financial Reporting and Analysis 6e Accrual Accounting and Income Determination CHAPTER 2 ACCRUAL ACCOUNTING AND INCOME DETERMINATION CHAPTER OVERVIEW This chapter highlights the key differences between cash and accrual income measurement, and why the latter generally provides a better measure […]

978-0078025679 Chapter 2 Solution Manual Part 1

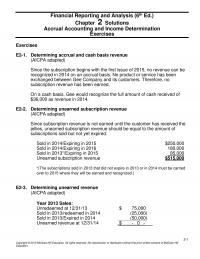

2-1 Financial Reporting and Analysis (6th Ed.) Chapter 2 Solutions Accrual Accounting and Income Determination Exercises Exercises E2–1. Determining accrual and cash basis revenue (AICPA adapted) Since the subscription begins with the first issue of 2015, no revenue can be […]

978-0078025679 Chapter 2 Solution Manual Part 2

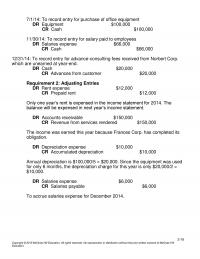

2-16 7/1/14: To record entry for purchase of office equipment DR Equipment $100,000 CR Cash $100,000 11/30/14: To record entry for salary paid to employees DR Salaries expense $66,000 CR Cash $66,000 12/31/14: To record entry for advance-consulting fees received […]

978-0078025679 Chapter 2 Solution Manual Part 3

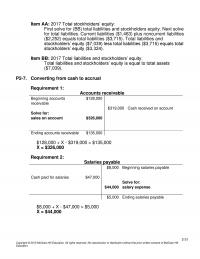

2-31 Item AA: 2017 Total stockholders’ equity: First solve for (BB) total liabilities and stockholders equity. Next solve for total liabilities. Current liabilities ($1,463) plus noncurrent liabilities ($2,252) equals total liabilities ($3,715). Total liabilities and stockholders’ equity ($7,039) less total […]

978-0078025679 Chapter 2 Solution Manual Part 4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Commercial service income (215,000) **Income from continuing operations, before taxes 2,355,600 Estimated selling price of commercial service component $ 87,000 […]

978-0078025679 Chapter 3 Lecture Note

Financial Reporting and Analysis 6e Additional Topics in Income Determination CHAPTER 3 ADDITIONAL TOPICS IN INCOME DETERMINATION Chapter Overview This chapter emphasizes the special accounting procedures used when revenue recognition doesn’t occur at the point of sale. The “critical event” […]

978-0078025679 Chapter 3 Solution Manual Part 1

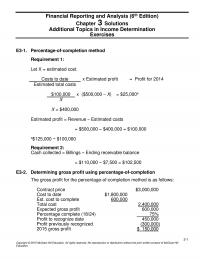

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (6th Edition) Chapter 3 Solutions Additional Topics in Income Determination Exercises E3–1. Percentage-of-completion method Requirement 1: […]

978-0078025679 Chapter 3 Solution Manual Part 2

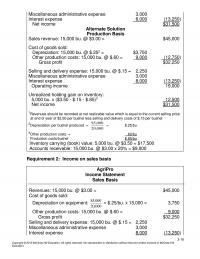

3-16 Miscellaneous administrative expense 3,000 Interest expense 8,000 (13,250) Net income $31,500 Alternate Solution Production Basis Sales revenue: 15,000 bu. @ $3.00 = $45,000 Cost of goods sold: Depreciation: 15,000 bu. @ $.252 = $3,750 Other production costs: 15,000 bu. […]

978-0078025679 Chapter 3 Solution Manual Part 3

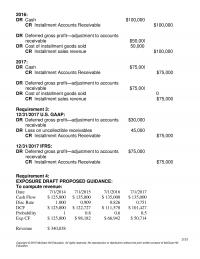

3-31 2016: DR Cash $100,000 CR Installment Accounts Receivable $100,000 DR Deferred gross profit—adjustment to accounts receivable $50,000 DR Cost of installment goods sold 50,000 CR Installment sales revenue $100,000 2017: DR Cash $75,000 CR Installment Accounts Receivable $75,000 DR […]

978-0078025679 Chapter 3 Solution Manual Part 4

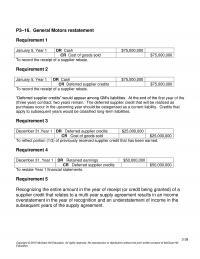

3-39 P3–16. General Motors restatement Requirement 1 January 5, Year 1 DR Cash $75,000,000 CR Cost of goods sold $75,000,000 To record the receipt of a supplier rebate. Requirement 2 January 5, Year 1 DR Cash $75,000,000 CR Deferred supplier […]

978-0078025679 Chapter 4 Lecture Note

Financial Reporting and Analysis 6e Structure of the Balance Sheet and Statement of Cash Flows CHAPTER 4 STRUCTURE OF THE BALANCE SHEET AND STATEMENT OF CASH FLOWS Chapter Overview The balance sheet and statement of cash flows are two of […]

978-0078025679 Chapter 4 Solution Manual Part 1

4-1 Financial Reporting and Analysis (6th Ed.) Chapter 4 Solutions Structure of the Balance Sheet and Statement of Cash Flows Exercises Exercises E4–1. Balance sheet classification b Long-term receivables (d) Accumulated amortization f Current maturities of long-term debt f Notes […]

978-0078025679 Chapter 4 Solution Manual Part 2

4-16 (2) $39,000 + $50,000 (3) $109,000 – $14,000 – $12,000 + $75,000 (4) $0 + $35,000 (5) $80,000 – $30,000 + $75,000 (6) $90,000 + $40,000 (7) $133,000 + $35,500 – $5,000 Copyright © 2015 McGraw-Hill Education. All rights […]

978-0078025679 Chapter 4 Solution Manual Part 3

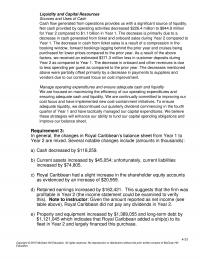

4-31 Liquidity and Capital Resources Sources and Uses of Cash Cash flow generated from operations provides us with a significant source of liquidity. Net cash provided by operating activities decreased $226.4 million to $844.9 million for Year 2 compared to […]

978-0078025679 Chapter 4 Solution Manual Part 4

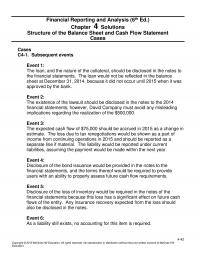

4-42 Financial Reporting and Analysis (6th Ed.) Chapter 4 Solutions Structure of the Balance Sheet and Cash Flow Statement Cases Cases C4–1. Subsequent events Event 1: The loan, and the nature of the collateral, should be disclosed in the notes […]

978-0078025679 Chapter 5 Lecture Note

Financial Reporting and Analysis 6e Essentials of Financial Statement Analysis CHAPTER 5 ESSENTIALS OF FINANCIAL STATEMENT ANALYSIS CHAPTER OVERVIEW Financial ratios, along with common size and trend statements, provide analysts with powerful tools for tracking a company’s performance over time, […]

978-0078025679 Chapter 5 Solution Manual Part 1

5-1 Financial Reporting and Analysis (6th Ed.) Chapter 5 Solutions Essentials of Financial Statement Analysis Exercises Exercises E5-1 Calculating profitability ratios (AICPA adapted) Requirement 1: 𝑅𝑂𝐴= (𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒 + 𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝐸𝑥𝑝𝑒𝑛𝑠𝑒 𝑥(1−𝑡𝑎𝑥 𝑟𝑎𝑡𝑒) 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐴𝑠𝑠𝑒𝑡𝑠 ) =($2,450,000+$800,000 𝑥 (1−0.40) $24,500,000 […]

978-0078025679 Chapter 5 Solution Manual Part 2

5-16 term debt to assets ratio is generally less than 1, the result of capitalizing leases will be to increase the long-term debt to assets ratio. Requirement 2: A firm’s creditworthiness represents its ability to repay its obligations on a […]

978-0078025679 Chapter 5 Solution Manual Part 3

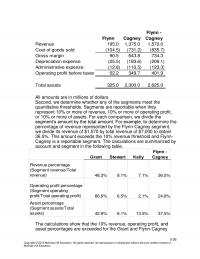

5-26 Flynn Cagney Flynn – Cagney Revenue 195.0 1,375.0 1,570.0 Cost of goods sold (104.5) (731.2) (835.7) Gross margin 90.5 643.8 734.3 Depreciation expense (25.5) (183.6) (209.1) Administrative expense (12.8) (110.5) (123.3) Operating profit before taxes 52.2 349.7 401.9 Total […]

978-0078025679 Chapter 6 Lecture Note

Financial Reporting and Analysis 6e The Role of Financial Information in Valuation and Credit Risk Assessment CHAPTER 6 THE ROLE OF FINANCIAL INFORMATION IN VALUATION AND CREDIT RISK ASSESSMENT CHAPTER OVERVIEW This chapter provides a framework for understanding the role […]

978-0078025679 Chapter 6 Solution Manual Part 1

6-1 Financial Reporting and Analysis (6th Ed.) Chapter 6 Solutions The Role of Financial Information in Valuation and Credit Risk Assessment Problems/Discussion Questions Exercises E6–1. Free cash flow valuation Requirement 1: Although the exact definition of “free cash flow” varies […]

978-0078025679 Chapter 6 Solution Manual Part 2

6-16 though the analyst concocted the forecasts used in the revised DCF model so that the original $13 share value estimate was confirmed when the share count was corrected. Requirement 9: It is difficult to discern any large stock price […]

978-0078025679 Chapter 6 Solution Manual Part 3

6-25 The value estimate from requirement 1 ($19.62 per share) is substantially below the market price of the stock ($44.00) in August 2003. There are several reasons why the abnormal earnings value estimate might differ from the company’s actual market […]

978-0078025679 Chapter 7 Lecture Note

Financial Reporting and Analysis 6e The Role of Financial Information in Contracting CHAPTER 7 THE ROLE OF FINANCIAL INFORMATION IN CONTRACTING CHAPTER OVERVIEW A contract is a legally binding exchange of rights and obligations between parties and is best expressed […]

978-0078025679 Chapter 7 Solution Manual Part 1

7-1 Financial Reporting and Analysis (6th Ed.) Chapter 7 Solutions The Role of Financial Information in Contracting Exercises Exercises E7–1. Understanding debt covenants Debt covenants are restrictive provisions written into loan agreements by the lender. Covenants are designed to reduce […]

978-0078025679 Chapter 7 Solution Manual Part 2

7-14 • Change one or more accounting methods to increase reported earnings. For instance: expand straight-line depreciation to all long-lived assets, eliminate LIFO accounting. • Change one or more accounting estimates. For instance, increase the estimated useful lives of long-term […]

978-0078025679 Chapter 8 Lecture Note

Financial Reporting and Analysis 6e Receivables CHAPTER 8 RECEIVABLES CHAPTER OVERVIEW Accounts receivables are generally reported in the balance sheet at their net realizable value (the amount a business expects to collect). This means gross accounts receivable must be reduced […]

978-0078025679 Chapter 8 Solution Manual Part 1

Financial Reporting and Analysis (6th Ed.) Chapter 8 Solutions Receivables Exercises Exercises E8–1. Analyzing accounts receivable (AICPA adapted) To find the amount of gross sales, start by determining credit sales. We can do this with the accounts receivable T-account below. […]

978-0078025679 Chapter 8 Solution Manual Part 2

P8–3. Determining allowance for uncollectibles Requirement 1: Based on the aging schedule, the ending balance in the allowance for doubtful accounts is calculated as follows: Expected Dollar Age of Receivables Amount Bad Debts Amount Zero to 30 days old $30,000 […]

978-0078025679 Chapter 8 Solution Manual Part 3

In essence, the loss on sale of receivables represents several different income statement items. While there is loss of information from combining these items into a single loss account, the above journal entry is one of the most common approaches […]

978-0078025679 Chapter 8 Solution Manual Part 4

There are substantial differences in the economics of the transactions. Crown Craft transfers the receivable without recourse as to credit losses, i.e., in effect, the factor becomes the “true” owner of the receivables by bearing the credit risk. Whereas, Ricoh […]

978-0078025679 Chapter 9 Lecture Note Part 1

Financial Reporting and Analysis 6e Inventories CHAPTER 9 INVENTORIES CHAPTER OVERVIEW This chapter is designed to allow users to understand existing GAAP inventory methods and disclosures; it can also help users conduct informed comparisons and analysis of profitability and net […]

978-0078025679 Chapter 9 Lecture Note Part 2

Financial Reporting and Analysis 6e Inventories LIFO adopters. D. The market perceives LIFO earnings to be of higher quality than FIFO earnings. E. The market response to earnings news is greater after LIFO adoption. XII. LOWER OF COST OR MARKET […]

978-0078025679 Chapter 9 Solution Manual Part 1

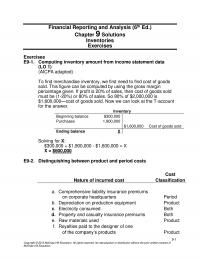

9-1 Financial Reporting and Analysis (6th Ed.) Chapter 9 Solutions Inventories Exercises Exercises E9–1. Computing inventory amount from income statement data (LO 1) (AICPA adapted) To find merchandise inventory, we first need to find cost of goods sold. This figure […]

978-0078025679 Chapter 9 Solution Manual Part 2

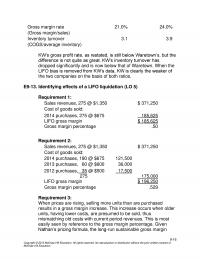

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Gross margin rate 21.0% 24.0% (Gross margin/sales) Inventory turnover 3.1 3.9 (COGS/average inventory) KW’s gross profit rate, as restated, is […]

978-0078025679 Chapter 9 Solution Manual Part 3

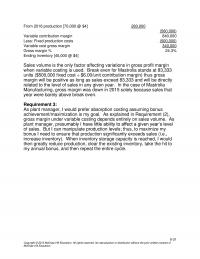

9-31 From 2016 production [70,000 @ $4] 280,000 (560,000) Variable contribution margin 840,000 Less: Fixed production costs (500,000) Variable cost gross margin 340,000 Gross margin % 24.3% Ending inventory [45,000 @ $4] Sales volume is the only factor affecting variations […]

978-0078025679 Chapter 9 Solution Manual Part 4

9-44 One possible reason for this apparent discrepancy is the equal weight given to beginning and ending LIFO reserves in the denominator, which assumes that price declines have been uniform throughout the year. P9-14. Determining LIFO amounts—comprehensive (LO 6, 7, […]

FC 232 Test 2

1) As a general rule, the proportion of pay “at risk” falls off for executives on the higher rungs of the corporate ladder. 2) The FASB endeavors to draft pronouncements that clearly identify the accounting objective, explain the accounting principle(s) […]

FC 516

1) Some intangible assets have indefinite lives and are impairment tested rather than amortized. 2) Investment analysts often compare cash flows from operations across two or more companies. Answer: TRUE 3) Stock options provide a set of “golden handcuffs” for […]

FE 271 Midterm

1) U.S. GAAP requires some firms to periodically recategorize a portion of actuarial adjustment losses relating to pensions into periodic net income. 2) In the highest risk S&P category of CCC/C, about 60% of the firms default within a year. […]

FE 311 Midterm 1

1) Most companies report their cash flow from operating activities using the direct method. 2) Companies assigned a Moody’s “Aaa” credit rating have a 2-4% default rate. Answer: FALSE 3) Reported accrual accounting net income for a period always provides […]

FE 407 Homework

1) “Book value” refers to the amount at which an account is carried in the company’s accounting records as opposed to “carrying amount” which refers to the amount at which an account is reported in the company’s financial statements. 2) […]

FE 866 Test 2

1) Because the securitization entity’s credit rating is based on the quality of the transferred receivables, it will be the same as the rating of the transferor’s general debt. 2) When conflicts of interest exist, lenders impose higher interest rates […]

FIN 120

1) If the fair value option is not elected, the company must still disclose the fair value of its all of its notes receivable. 2) The first stage of impairment testing of a long-lived asset is to take the present […]

Fin 365 1 If a firm can earn a return

1) If a firm can earn a return on net assets (common equity book value) that exceeds its cost of equity capital, it will generate positive abnormal earnings. 2) Selling, general, and administrative expenses relating to installment sales are deferred […]

FIN 446 Test 1 When agents do not

1) When agents do not act on behalf of their principals, the agency cost is borne by the principal alone. 2) Under current GAAP, volatility in asset returns translates directly into net income volatility because the return on plan assets […]