Archives

978-1133939283 Chapter 1 Lecture Note Part 1

Chapter 1 Accounting Principles and the Financial Statements Learning Objectives 1. Dene accounting, and explain the concepts underlying accounting measurement. 2. Dene nancial position, and state the accounting equation. 3. Identify the four basic nancial statements and their interrelationships. 4. […]

978-1133939283 Chapter 1 Lecture Note Part 2

Section 2: Accounting Applications Accounting Applications Describe the income statement Describe the statement of owner’s equity Describe the balance sheet Describe the statement of cash ows Lecture Outline 0. There are four basic nancial statements that are interrelated. 0. Income […]

978-1133939283 Chapter 1 Solution Manual Part 1

DQ1. DQ7. CVS and Southwest are comparable in that like all companies they have two main goals: profitability and liquidity. How companies such as CVS and Southwest achieve organizations in a financially prudent way. these goals may make them incomparable […]

978-1133939283 Chapter 1 Solution Manual Part 2

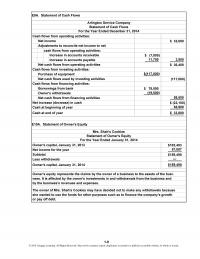

$ 32,500 cash flows from operating activities: $(117,000) (117,000) $ 78,000 (19,500) 58,500 $ (22,100) 55,900 $ 33,800 Borrowings from bank Net increase (decrease) in cash Owner’s withdrawals Net cash flows from financing activities Cash at beginning of year Cash […]

978-1133939283 Chapter 1 Solution Manual Part 3

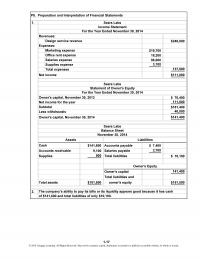

1. $248,000 $ 70,400 111,000 $181,400 40,000 $141,400 Subtotal Less withdrawals Owner’s capital, November 30, 2014 $141,600 Accounts payable $ 7,400 9,100 2,700 800 $ 10,100 141,400 $151,500 $151,500 Total assets owner’s equity Owner’s Equity Supplies Total liabilities Owner’s capital […]

978-1133939283 Chapter 10 Lecture Note Part 1

Chapter 10 Long-Term Assets Learning Objectives 1. Identify the classications of long-term assets, and describe how they are valued by allocating their cost to the periods that they benet. 2. Account for the acquisition cost of property, plant, and equipment. […]

978-1133939283 Chapter 10 Lecture Note Part 2

Summary The cost of a long-term asset includes the purchase cost, freight charges, insurance while in transit, installation, and other costs involved in the acquisition of the asset. Interest incurred during the construction of a plant asset is included in […]

978-1133939283 Chapter 10 Solution Manual Part 1

1. 7. 8. cipates superior earnings and believes it will more than recoup the goodwill it extra funds to invest and expand. The major advantage for a company that has positive free cash flow is that it has purchased. A […]

978-1133939283 Chapter 10 Solution Manual Part 2

2015 225 Accumulated Depreciation—Computer ( – ) / 5 $250 years $2,500 ×6/12= $225 2,500 Computer 2,500 Computer 3. 2015 July 1 Accumulated Depreciation—Computer Cash Computer sold for $400; loss recognized Computer sold for $1,100; gain recognized 1,100 1,575 *($2,500 […]

978-1133939283 Chapter 10 Solution Manual Part 3

1. Carrying Value * † $22,500 – $2,500 = $20,000 100% / 4 = 25%; 25% × 2 = 50% ** *** 2. a. A loss of ( – b. A loss of ( – $12,500 $12,500 $12,000 $12,000 $500 […]

978-1133939283 Chapter 11 Lecture Note Part 1

Chapter 11 Current Liabilities and Fair Value Accounting Learning Objectives 1. Dene current liabilities, and identify the concepts underlying them. 2. Identify, compute, and record denitely determinable and estimated current liabilities. 3. Distinguish contingent liabilities from commitments. 4. Identify the […]

978-1133939283 Chapter 11 Lecture Note Part 2

Summary Current liabilities consist of denitely determinable liabilities and estimated liabilities. Denitely determinable liabilities are obligations that can be measured exactly. They include accounts payable, bank loans and commercial paper, notes payable, accrued liabilities, dividends payable, sales and excise taxes […]

978-1133939283 Chapter 11 Solution Manual Part 1

DQ1. DQ6. DQ7. The present value concept allows the decision maker to compare various alterna- Increasing payables turnover is good for the company in the sense that it is able to creasing payables turnover is bad for the company because […]

978-1133939283 Chapter 11 Solution Manual Part 2

12. 13. 14. 2. Problems P1. Identification of Current Liabilities, Contingencies, and Commitments sheet with a dollar amount and the ones that would involve the most judgment or discretion include the estimated liabilities such as income taxes payable, property taxes […]

978-1133939283 Chapter 11 Solution Manual Part 3

1. (×) (×) (×) 2. the documents are missing. For instance, there may be a bank loan or other loan out- Total current liabilities Federal income tax withholding $14,000 Federal unemployment tax payable 0.008 $36,988.20 952.00 112.00 Current liabilities may […]

978-1133939283 Chapter 12 Lecture Note Part 1

Chapter 12 Accounting for Partnerships Learning Objectives 1. Dene the partnership form of business, and identify its principal characteristics. 2. Record partners’ investments of cash and other assets when a partnership is formed. 3. Compute and record the income or […]

978-1133939283 Chapter 12 Lecture Note Part 2

Dissolution of a partnership occurs whenever there is a change in partners. Dissolution can occur upon admission of a new partner, withdrawal of a partner, or death of a partner. For example, when a new partner is admitted to a […]

978-1133939283 Chapter 12 Solution Manual Part 1

DQ1. to decide how to pay the liabilities, and they will have to settle their capital accounts, just as they would if cash were involved. Discussion Questions Partnerships are indeed separate entities from the partners from an accounting standpoint, CHAPTER […]

978-1133939283 Chapter 12 Solution Manual Part 2

Amit’s equity ( ×$ 80,000 $120,000 80,000 $ 40,000 ) Bonus to the original partners $400,000 Amit’s investment Less Amit’s equity 0.20 * ×1/5 ×1/5 ×3/5 $ 8,000 24,000 ) ) Ronald ( 8,000 Fenny ( ) $40,000 $40,000 $40,000 […]

978-1133939283 Chapter 12 Solution Manual Part 3

×= 0.20 $90,000 $18,000 b. 31 40,000 40,000 c. 31 60,000 48,000 6,000 2,000 4,000 $180,000 60,000 $240,000 $ 60,000 ×48,000 $ 12,000 Frank, Capital Frank, Capital Computation: Sale of a 20 percent interest in the James, Capital Capital of […]

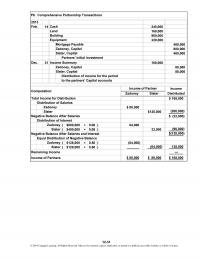

978-1133939283 Chapter 12 Solution Manual Part 4

Income of Partner Zadoney Slater Distributed $ 168,000 $ 80,000 $120,000 (200,000) $ (32,000) ( $800,000 × 0.08 ) 64,000 ( $400,000 × 0.08 ) 32,000 (96,000) $(128,000) ( $128,000 × 0.50 ) (64,000) ( $128,000 × 0.50 ) (64,000) […]

978-1133939283 Chapter 13 Lecture Note Part 1

Chapter 13 Accounting for Corporations Learning Objectives 1. Dene the corporate form of business and its characteristics. 2. Identify the components of stockholders’ equity and their characteristics. 3. Account for the issuance of stock for cash and other assets. 4. […]

978-1133939283 Chapter 13 Lecture Note Part 2

Summary A corporation’s balance sheet contains assets, liabilities, and a stockholders’ equity section. Stockholders’ equity is made up of contributed capital (the stockholders’ investments) and retained earnings (earnings that have remained in the business), and sometimes treasury stock. A corporation […]

978-1133939283 Chapter 13 Solution Manual Part 1

DQ1. DQ5. DQ6. record, the seller will not receive the dividend because the date of record is the own stock, the company is in effect reducing its stockholders’ equity. date at which ownership of the stock of a company and […]

978-1133939283 Chapter 13 Solution Manual Part 2

1. 4. 2. 5. 3. 1. 4. 7. 2. 5. 8. Preferred stock, $100 par value, 9% cumulative, 10,000 shares authorized, P CPP E3A. Characteristics of Common and Preferred Stock PC Total stockholders’ equity 3. 6. 9. PCP Contributed capital: […]

978-1133939283 Chapter 13 Solution Manual Part 3

8,000,000 $12,800,000 16,000,000 $28,800,000 $ 4,800,000 Common stock, $4 par value, 1,600,000 shares authorized, 1,200,000 shares issued and outstanding 8,000,000 $12,800,000 16,000,000 $28,800,000 Common stock, $12 par value, 1,600,000 shares authorized, Additional paid-in capital Total contributed capital Total stockholders’ equity […]

978-1133939283 Chapter 13 Solution Manual Part 4

2. * $11,500 – $980 = $10,520 3. (+ )/2 Preferred stock, $100 par value, 9%, 5,000 shares $11,500 times Average Stockholders’ Equity $236,520 $245,500 $11,500 Net Income = $0.02 $20.00 = 0.1% = = Dividend Yield Dividends per Share […]

978-1133939283 Chapter 13 Solution Manual Part 5

4. P9. Preferred and Common Stock Dividends and Dividend Yield (Concluded) have to be made up. The difference is that with noncumulative preferred stock, if Both cumulative and noncumulative preferred stock have a fixed level of dividends and are thus […]

978-1133939283 Chapter 13 Solution Manual Part 6

2015 Jan. 4 Mar. 8 Apr. 20 144,000 144,000 May 4 64,000 48,000 16,000 July 15 412,800 412,800 Dividends Payable share Dividends Treasury Stock, Common Paid-in Capital, Treasury Stock Sold 4,000 shares of treasury stock for $16 per share; originally […]

978-1133939283 Chapter 14 Lecture Note Part 1

Chapter 14 Long-Term Liabilities Learning Objectives 1. Explain the concepts underlying long-term liabilities, and identify the types of long-term liabilities. 2. Describe the features of a bond issue and the major characteristics of bonds. 3. Record bonds issued at face […]

978-1133939283 Chapter 14 Lecture Note Part 2

Summary A bond is a security, usually long-term, that represents money that a corporation or some other entity borrows from the investing public. Bondholders are considered creditors (not owners) of the issuing corporation, who are entitled to periodic interest plus […]

978-1133939283 Chapter 14 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. DQ7. DQ8. amount paid on a lease is tax-deductible and provides greater liquidity. This is debt to equity and interest coverage ratios. The analysis may also include a his- can then judge how well […]

978-1133939283 Chapter 14 Solution Manual Part 2

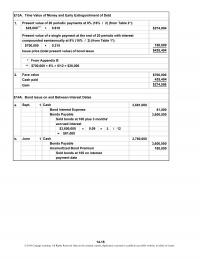

Present value of 40 periodic payments at 6% (from Table 2*): *From Appendix B E3A. Valuing Bonds Using Present Value Choice A 14-8 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a […]

978-1133939283 Chapter 14 Solution Manual Part 3

1. * ** 2. $700,000 425,404 $274,596 a. 1 3,681,000 81,000 3,600,000 Face value Cash paid Bond Interest Expense Bonds Payable Sept. Cash Gain E14A. Bond Issue on and Between Interest Dates ××3/ = $81,000 b. 1 3,780,000 3,600,000 180,000 […]

978-1133939283 Chapter 14 Solution Manual Part 4

(××6/12)− (××6/12)= −= (××6/12)− (××6/12)= −= Paid semiannual interest and amortized 0.09 the discount on 9%, 20-year bonds 0.10 2015 $9,147,000 $10,000,000 $457,000 $457,350 $450,000 $7,000 $450,000 $7,350 * 31 457,350 7,350 450,000 May Cash Unamortized Bond Discount Bond Interest […]

978-1133939283 Chapter 14 Solution Manual Part 5

4. a. b. c. $10,000,000 Bonds payable (×) (150,000) $ 9,850,000 ( × $ 5,000,000 4,850,000 $ 9,850,000 Total common stock issue amount $20shares $150,000 of the $300,000 discount remains to be amortized. Since the call takes place after 10 […]

978-1133939283 Chapter 14 Solution Manual Part 6

Cases C1. Conceptual Understanding: Bond Issue Unsecured notes (or debenture bonds) are bonds issued on the general credit of the or- the original issue price was face value or 100, both the interest expense and the interest payment were 6.125 […]

978-1133939283 Chapter 15 Lecture Note

Chapter 15 The Statement of Cash Flows Learning Objectives 1. Describe the principal purposes and concepts underlying the statement of cash ows, and identify its components and format. 2. Use the indirect method to determine cash ows from operating activities. […]

978-1133939283 Chapter 15 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. current liabilities, the results could overwhelm the earnings and create negative cash flows from operating activities. statement. cash flows are the details of the changes. For instance, cash flows from oper- ating activities is […]

978-1133939283 Chapter 15 Solution Manual Part 2

Net Cash Flows from Operating Activities Instructor’s Resource CD and website. E9A. Cash-Generating Efficiency Ratios and Free Cash Flow $390,000 =Net Income Cash Flow Yield 15-9 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or […]

978-1133939283 Chapter 15 Solution Manual Part 3

Operating Investing Financing Noncash Activity Activity Activity Transaction Increase Decrease No Effect dividend. X X issuing stock. XX ment with cash. X X equipment. X X securities (long-term). X X stock. X X 10. Sold a machine at a loss. […]

978-1133939283 Chapter 15 Solution Manual Part 4

ating activities. The financial press would give a better picture of a company’s cash posi- tion by focusing on cash flows from operating activities and cash flow yield. assets and current liabilities, which can have a significant effect on cash […]

978-1133939283 Chapter 15 Solution Manual Supplement- Solutions

=+(–) =+ = = +(–)+(–) =+ + = = –(–)+(–)– =– + – = =+ = CHAPTER 15 SUPPLEMENT—Solution s $96,200 THE STATEMENT OF CASH FLOWS $12,500 $600 $79,000 Cost of $294,200 $294,200 $304,800 Expense $58,700 $79,000 $426,500 $457,700 $426,500 […]

978-1133939283 Chapter 16 Lecture Note

Chapter 16 Financial Statement Analysis Learning Objectives 1. Describe the concepts, standards of comparison, and sources of information used in measuring nancial performance. 2. Apply horizontal analysis, vertical analysis, and ratio analysis to nancial statements. 3. Apply nancial ratio analysis […]

978-1133939283 Chapter 16 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ9. DQ10. are full values similar to those at year end. Thus, any ratios that use data from the income statement or statement of cash flows as their basis will be less than they increase in […]

978-1133939283 Chapter 16 Solution Manual Part 2

1. c 6. 2. e 7. 3. c 8. 4. b 9. 5. a 10. 2014 2013 2012 2011 2010 *Rounded Exercises: Set A Although sales increased over the five-year period, operating income decreased because cost of goods sold increased […]

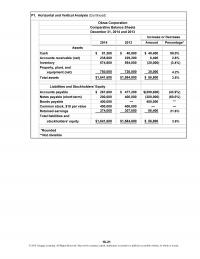

978-1133939283 Chapter 16 Solution Manual Part 3

2014 2013 Amount Percentage* Property, plant, and equipment (net) 750,000 720,000 30,000 4.2% Total assets $1,641,600 $1,584,800 $ 56,800 3.6% Accounts payable $ 267,600 $ 477,200 $(209,600) (43.9%) Notes payable (short-term) 200,000 400,000 (200,000) (50.0%) Bonds payable 400,000 — 400,000 […]

978-1133939283 Chapter 16 Solution Manual Part 4

Quick ratio* Operating asset management analysis b. d. c. Design a. *Rounded $552,800 2.8 days16.1= times times Days’ sales uncollected* Receivables turnover* = times Design Single $1,253,400 $400,000 $73,400 $985,400$84,600 $400,000 times= $1,262,400 = $1,046,000 1.2 25.6 14.3= days times […]

978-1133939283 Chapter 16 Solution Manual Part 5

1. 2014 2013 Amount Percentage* Alternate Problems P7. Horizontal and Vertical Analysis Comparative Income Statements For the Years Ended December 31, 2014 and 2013 Increase or Decrease Rylander Corporation *Rounded 16-41 © 2014 Cengage Learning. All Rights Reserved. May not […]

978-1133939283 Chapter 16 Solution Manual Part 6

*Rounded days times $293,600 25.6 2.5 times Ranbaxy 1.2 $3,941,600 $293,600 $338,400 + $338,400 $456,000$5,013,600 = $1,600,000 $3,941,600 14.3 $1,600,000 a. 1. Quick ratio* d. Operating asset management analysis b. Current ratio* $10,519,200 $4,184,000 $4,184,000 $1,376,000 22.7 $2,211,200 $1,376,000 $320,000 […]

978-1133939283 Chapter 16 Solution Manual Part 7

had problems but did not go bankrupt. Both companies have shown improved results of Thus, liquidity measures such as cash flow yield and cash flows to sales and assets, as their operations since 2009. Standard & Poor’s (S&P) judges the […]

978-1133939283 Chapter 2 Lecture Note Part 1

Chapter 2 Analyzing and Recording Business Transactions Learning Objectives 1. Explain how the concepts of recognition, valuation, and classication apply to business transactions. 2. Explain the double-entry system and the usefulness of T accounts in analyzing business transactions. 3. Demonstrate […]

978-1133939283 Chapter 2 Lecture Note Part 2

Teaching Strategy Students will wonder why the rules of debit and credit are as they are. Simply state they are an arbitrary set of rules whose careful interrelationships make them work. In addition, students need to dispel any preconceived notions […]

978-1133939283 Chapter 2 Solution Manual Part 1

DQ1. DQ6. DQ7. The most common violation of the recognition concept is when a revenue is recog- penses. They appear on opposite sides of the accounting equation. nized before the earnings process is complete. For instance, the recording of an […]

978-1133939283 Chapter 2 Solution Manual Part 2

f. 400 c. 1,000 h. 1,200 1,000 g. 3,720 3,200 e. 900 600 3,800 b. 800 Rent Expense d. Bal. a. a. b. c. d. e. f. Billed customer for services rendered, $2,000. Purchased equipment on account, $2,250. Paid wages […]

978-1133939283 Chapter 2 Solution Manual Part 3

f. 1,740 j. 1,080 e. 330 1,080 c. 190 Bal. 660 4,300 a. 3,600 h. 330 e. 330 480 g. 380 g. 860 4,780 Bal. 3,980 330 1,190 g. Bal. Bal. 860 a. 13,600 m. 300 f. 1,740 440 k. […]

978-1133939283 Chapter 2 Solution Manual Part 4

Cash $44,120 = $57,880 + Accounting equation without Cash: 27,500 10,120 13,760 6,500 Equipment Utilities $57,880 $57,880 Accounting equation in balance: Supplies Wages Cash P6. T Accounts, Normal Balance, and the Accounting Equation Assets Cash Accounts Receivable Alternate Problems © […]

978-1133939283 Chapter 2 Solution Manual Part 5

Ref. Debit Credit Debit Credit 31 1,870 2 J17 270 1,600 Ref. Debit Credit Debit Credit 31 1,700 9 J17 1,200 500 10 J17 700 1,200 22 J18 500 700 Ref. Debit Credit Debit Credit 4 J17 85 85 Feb. […]

978-1133939283 Chapter 3 Lecture Note

Chapter 3 Adjusting the Accounts Learning Objectives 1. Dene net income and explain the concepts underlying income measurement. 2. Distinguish cash basis of accounting from accrual accounting, and explain how accrual accounting is accomplished. 3. Identify four situations that require […]

978-1133939283 Chapter 3 Solution Manual Part 1

DQ1. DQ2. ● Discretionary expenditures can be timed to fall in a desired accounting ● Goods may be delivered or services performed before or after the end of the accrual accounting is to measure net income. Cash accounting is more […]

978-1133939283 Chapter 3 Solution Manual Part 2

$ 1,200 1,900 $ 1,100 9,750 $10,850 600 $10,250 Potential payments for wages during 2014 Less wages payable at end of 2014 Cash payments for wages during 2014 $ 2,100 4,450 $ 6,550 950 $ 5,600 Cash receipts from fees […]

978-1133939283 Chapter 3 Solution Manual Part 3

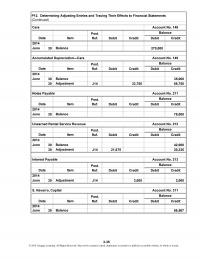

Ref. Debit Credit Debit Credit Ref. Debit Credit Debit Credit 30 428,498 30 J14 12,185 440,683 Adjustment Ref. Debit Credit Debit Credit 30 89,300 June Balance Ref. Debit Credit Debit Credit 30 206,360 June Balance Ref. Debit Credit Debit Credit […]

978-1133939283 Chapter 3 Solution Manual Part 4

P8. Determining Adjusting Entries and Tracing Their Effects to Financial Statements 1. and 2. Prepaid InsuranceAccounts Receivable Cash 3-26 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in […]

978-1133939283 Chapter 3 Solution Manual Part 5

Ref. Debit Credit Debit Credit Ref. Debit Credit Debit Credit 30 35,000 30 J14 33,750 68,750 Adjustment Ref. Debit Credit Debit Credit 30 78,000 June Balance Ref. Debit Credit Debit Credit 30 42,000 30 J14 21,675 20,325 Adjustment Ref. Debit […]

978-1133939283 Chapter 3 Solution Manual Part 6

a. June 30 14,000 b. 30 13,860 13,860 (/5 ×3 = days $13,860 days ) Salaries Payable To record accrued salaries $23,100 c. d. 30 2,837 To record supplies used Supplies Expense No entry 2,837 Supplies +– = $2,846 $2,837 […]

978-1133939283 Chapter 4 Lecture Note

Chapter 4 Completing the Accounting Cycle Learning Objectives 1. Describe the role of closing entries in the preparation of nancial statements. 2. Prepare closing entries. 3. Prepare reversing entries 4. Prepare a work sheet. 5. Explain the importance of the […]

978-1133939283 Chapter 4 Solution Manual Part 1

DQ1. DQ2. CHAPTER 4—Solutions COMPLETING THE ACCOUNTING CYCLE crual types of adjustments. When the accrual is resolved in the next accounting period through receipt or payment of cash, it is not necessary to know the amount accrued at the end […]

978-1133939283 Chapter 4 Solution Manual Part 2

2014 Dec. 31 12,810 31 7,915 4,055 600 2,130 458 672 Insurance Expense Wages Expense Rent Expense Supplies Expense Depreciation Expense—Repair Equipment 31 4,895 4,895 A. Winter, Capital 31 2,500 2,500 A. Winter, Withdrawals To close the expense accounts Income […]

978-1133939283 Chapter 4 Solution Manual Part 3

Debit Credit Debit Credit Debit Credit Debit Credit ( h ) 816 30,130 30,130 ( ) ( ) 13,270 1,430 1,430 ( ) 53,400 ( ) 14,400 67,800 67,800 30,900 ( ) 15,450 46,350 46,350 10,800 ( ) 9,396 9,396 […]

978-1133939283 Chapter 4 Solution Manual Part 4

4. 8,570 5. $2,750 $850 120 80 598 140 1,788 $ 962 Net income Repair supplies expense Depreciation expense—repair equipment Total expenses Insurance expense Store rent expense Advertising expense $0 10,000 962 $10,962 600 $10,362 Net income Subtotal Less withdrawals […]

978-1133939283 Chapter 4 Solution Manual Part 5

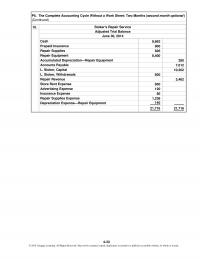

10. 8,662 800 P5. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional) (Continued) Cash Prepaid Insurance Stoker’s Repair Service Adjusted Trial Balance June 30, 2014 4-33 © 2014 Cengage Learning. All Rights Reserved. May not […]

978-1133939283 Chapter 4 Solution Manual Part 6

31 29,240 31 23,900 11,360 2,700 1,160 760 5,840 640 1,440 Supplies Expense Insurance Expense Rent Expense Wages Expense Gas, Oil, and Other Truck Expenses Depreciation Expense—Painting Equipment Depreciation Expense—Truck 31 5,340 5,340 G. Ranke, Capital 31 4,000 4,000 G. […]

978-1133939283 Chapter 4 Solution Manual Part 7

Page 3 Post. Ref. Debit Credit 2014 30 411 5,500 30 314 3,576 511 1,700 512 240 513 160 514 1,196 515 280 30 314 1,924 311 1,924 Depreciation Expense—Repair Equipment B. Lutz, Capital Income Summary To close the expense […]

978-1133939283 Chapter 4 Solution Manual Part 8

Ref. Debit Credit Debit Credit 30 J3 5,500 5,500 30 J3 3,576 1,924 Ref. Debit Credit Debit Credit 15 J1 1,600 1,600 30 J2 3,900 5,500 30 J3 5,500 — 15 J4 3,656 3,656 31 J4 3,268 6,924 31 J5 […]

978-1133939283 Chapter 5 Lecture Note

Chapter 5 Foundations of Financial Reporting and the Classied Balance Sheet Learning Objectives 1. Describe the objective of nancial reporting, and identify the conceptual framework underlying accounting information. 2. Identify and dene the basic components of nancial reporting, and prepare […]

978-1133939283 Chapter 5 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ7. tions or the economy may make financial information incomparable from year to The statement is false because neither measure is better than the other. However, presenting the financial information. It does not apply to the conditions […]

978-1133939283 Chapter 5 Solution Manual Part 2

Current A sset s Current Liabilities Working Ca p ital Current Ratio $ 85,000 $25,000 $60,000 3.40 100,000 45,000 55,000 2.22 $ 5,000 1.18 Net Income Sales Profit Margin Average Total Asset Assets Turnover Return on Assets A verage Owner’s […]

978-1133939283 Chapter 5 Solution Manual Part 3

3. cause it is a good indicator of a company’s ability to pay its bills and to repay outstanding loans. The other measure, the debt to equity ratio, shows the pro- portion of the company financed by creditors in comparison […]

978-1133939283 Chapter 5 Solution Manual Part 4

Cases of net income. The auditors may become concerned if the loss is greater in the future or if management does not take action to try to reduce it. decisions of users of financial statements. The $120,000 inventory loss represents […]

978-1133939283 Chapter 6 Lecture Note Part 1

Chapter 6 Accounting for Merchandising Operations Learning Objectives 1. Dene merchandising accounting, and dierentiate perpetual from periodic inventory systems. 2. Describe the features of multistep and single-step classied income statements. 3. Describe the terms of sale related to merchandising transactions. […]

978-1133939283 Chapter 6 Lecture Note Part 2

Teaching Strategy To help students understand the merchandising or manufacturing company’s multistep income statement, you may want to reproduce Exhibit 2 and explain it line by line. Exhibit 1 is helpful in understanding the cost of goods sold computation. Explain […]

978-1133939283 Chapter 6 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ7. balance if merchandise has been lost or stolen. dise would belong to you when it left the shipper and would be your loss. You would want the terms to be FOB destination because the loss […]

978-1133939283 Chapter 6 Solution Manual Part 2

400 g. 5,200 g. 5,200 d. 5,200 Bal. 670 h. 1,800 h. 1,800 Bal.** 12,270 13,000 13,000 d. 5,000 2,800 f. f. c. 5,000 * Bal. — 5,000 e. 1,000 2,800 4,800 12,600 1,000 11,600 c. Bal. d. * ** […]

978-1133939283 Chapter 6 Solution Manual Part 3

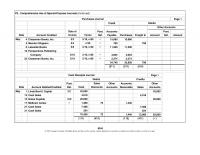

1. $433,912 $ 81,222 $221,185 30,238 $190,947 10,078 Freight-in Purchases Less purchases returns and allowances Net purchases 201,025 $282,247 76,664 205,583 $217,079 Gross margin Cost of goods sold Cost of goods available for sale Less merchandise inventory, March 31, 2014 […]

978-1133939283 Chapter 6 Solution Manual Part 4

18 400 18 240 240 Cost of Goods Sold 24 6,400 6,400 Cash 25 3,800 3,800 Accounts Receivable 2. are equivalent. Net sales reflects gross sales adjusted for any sales discounts, sales returns, or allow- ances granted the buyer. When […]

978-1133939283 Chapter 6 Solution Manual Supplement- Solutions Part 1

Page 1 Account Post. Sales Other Accounts Other Debited/Credited Ref. Cash Discounts Accounts Receivable Sales Accounts Nov. 4 J. Walker 980 20 1,000 9 Truck/Fred Kimball, Capital 10,000 14,000 24,000 14 Sales 2,834 2,834 17 P. Sivula 120 120 18 […]

978-1133939283 Chapter 6 Solution Manual Supplement- Solutions Part 2

Page 1 Credit Post. Accounts Post. Account Credited Ref. Payable Purchases Freight In Account Ref. Amount 19 Perspectives Publishing Company 4,604 4,604 23 Chassman Books, Inc. 2,374 2,374 34,748 33,958 790 5/19 5/18 5/10, n/60 5/10, n/60 (211) (511) (514) […]

978-1133939283 Chapter 7 Lecture Note

Chapter 7 Inventory Learning Objectives 1. Explain the concepts underlying inventory accounting. 2. Calculate inventory cost under the periodic inventory system using various costing methods. 3. Explain the eects of inventory costing methods on income determination and income taxes. 4. […]

978-1133939283 Chapter 7 Solution Manual Part 1

DQ1. DQ7. For one thing, the value put on inventory has a direct dollar-for-dollar effect on net tory than a smaller inventory. In addition to storage and insurance costs, there is income. For another, it is relatively easy to falsify […]

978-1133939283 Chapter 7 Solution Manual Part 2

2. FIFO LIFO Method Method E5A. Effects of Inventory Costing Methods on Cash Flows (Concluded) The results under the FIFO method are the same with or without the purchase, but Sales cause the ending inventory is below the beginning inventory […]

978-1133939283 Chapter 7 Solution Manual Part 3

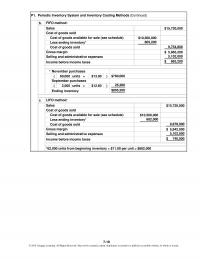

b. * ( 60,000 units × $13.00 ) ( 2,000 units × $12.60 ) September purchases $780,000 25,200 c. $15,720,000 $10,560,000 682,000 9,878,000 $ 5,842,000 5,102,000 $ 740,000 Cost of goods available for sale (see schedule) Less ending inventory* Cost […]

978-1133939283 Chapter 7 Solution Manual Part 4

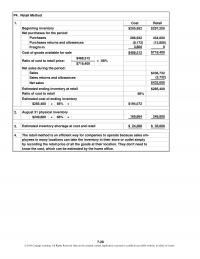

1. Cost Retail 2. $249,800 × 68% = 169,864 249,800 3. $ 24,208 $ 35,600 Estimated inventory shortage at cost and retail 4. The retail method is an efficient way for companies to operate because sales em- ployees in many […]

978-1133939283 Chapter 7 Solution Manual Part 5

Units Cost Amount 10 60 49 100 52 $ 8,140 19 (60) 49 (30) 52 (4,500) 31 70 52 $ 3,640 4120 53 6,360 Ending inventory Purchase Apr. 47052 120 53 $ 10,000 15 50 54 2,700 Purchase 15 70 […]

978-1133939283 Chapter 8 Lecture Note

Chapter 8 Cash and Internal Control Learning Objectives 1. Describe the components of internal control, control activities, and limitations on internal control. 2. Apply internal control activities to common merchandising transactions. 3. Dene cash equivalents, and explain methods of controlling […]

978-1133939283 Chapter 8 Solution Manual Part 1

DQ1. independently. greater risk of human error in recording the large number of transactions involved and because there is a greater risk of theft. CHAPTER 8—Solutions with GAAP and that the company’s assets are protected. A system of internal control […]

978-1133939283 Chapter 8 Solution Manual Part 2

1. 2. Periodic independent verification The accountant compares the inventory transfer transfer sheets, all of which are prenumbered and accounted for. onstrate knowledge of control procedures. Physical controls The warehouse is secured and access is limited to authorized Sound personnel […]

978-1133939283 Chapter 8 Solution Manual Part 3

1. (the receiving clerk) are separated from recordkeeping (the accounting with the existing assets at reasonable intervals. The comparison of the cash regis- compared with the invoices before payment is authorized. In addition, prior to pay- ment, the invoice should […]

978-1133939283 Chapter 9 Lecture Note

Chapter 9 Receivables Learning Objectives 1. Dene receivables, and explain the allowance method for valuation of receivables as an application of accrual accounting. 2. Apply the allowance method of accounting for uncollectible accounts. 3. Make common calculations for notes receivable. […]

978-1133939283 Chapter 9 Solution Manual Part 1

DQ1. period to period, especially in the absence of changes in credit policies or economic cial flexibility (cash flows). RECEIVABLES Discussion Questions CHAPTER 9―Solutions Accrual accounting and valuation are violated by the direct charge-off method be- 9-1 © 2014 Cengage […]

978-1133939283 Chapter 9 Solution Manual Part 2

Before Write-off After Write-off Write-off 2,400 Bal. 800 3,200Bal. Accounts Receivable Bal. 32,500 32,500 3,600 Write-off 2,400 Bal. Sale Bal. 34,900 Collection 1,200 Allowance for Uncollectible Accounts E7A. Write-off of Accounts Receivable *Rounded 9-10 © 2014 Cengage Learning. All Rights […]

978-1133939283 Chapter 9 Solution Manual Part 3

×11 /×/= 2. 3 ×12/×/= May $2,288.22 $120,000 365 58 100 16 × 13 / × / = May 100 $64,000 365 45 1,025.75 31 × 11 / × / = 542.47 100 30 $60,000 365 May 3. 0 90 […]

978-1133939283 Chapter 9 Solution Manual Part 4

● Cases amount of uncollectible accounts that will arise from these credit sales and record it as C1. Conceptual Understanding: Role of Credit Sales Mitsubishi established the generous credit terms of 14 months without interest and pay- ments because management […]

AC 12889

In the calculation of free cash flow, dividends and sales of plant assets are both deducted. The term salaries refers to the compensation of employees who are paid at an hourly rate. FALSE The quick ratio and the current ratio […]

AC 49597

The following information pertains to Patterson Corporation. Assume that all balance sheet amounts represent both average and ending figures. Patterson Corporation had 6,000 shares of common stock issued and outstanding. The market price of Patterson common stock on December 31, […]

ACC 31107

Use this information to answer the following question. What is the present value of receiving $800 at the end of each year for three years, assuming an APR of 7 percent? A. $652.80 B. $1,952.40 C. $2,099.20 D. $2,244.00 Which […]

ACC 35807

If the present value of the net cash flows expected from a machine is less than its purchase price, the investment should not be made. Intangible assets are subject to a process called depreciation. FALSE Freight-in is treated as an […]

Acc 36897

Issuing bonds between interest payment dates will have the effect of decreasing a bond issuance discount or increasing a bond issuance premium. Once an owner of convertible preferred stock has converted to common, he or she cannot convert back to […]

ACC 78221

The personal assets and liabilities of an owner are not shown on the business’s financial statements because of the A. separate entity concept. B. sole proprietorship concept. C. financial position concept. D. objectivity concept. Use the following information regarding Larson […]

Acc 78888

Lines of credit from the bank need not be disclosed in the financial statements or in the notes. The information needed to record the adjusting entries can be copied from the work sheet. TRUE An ordinary annuity is a series […]

Acc 78892

If a corporation issues par value common stock and the proceeds are less than par value, the Common Stock account is credited for the par value. A capital expenditure will result in an immediate increase in long-term assets. TRUE Noncompete […]

ACC 83244

A corporation issues bond certificates to A. owners. B. principals. C. creditors. D. debtors. The following facts pertain to Alameda Corporation for 20×5: Based on the above facts, net income for 20×5 for Alameda Corporation amounted to A. $207,500. B. […]

Acc 84717

The recognition of an expense does not depend on the payment of cash. A corporation’s bondholders are the primary recipients of financial leverage. FALSE A temporary account is also known as a nominal account. TRUE Inventory turnover is a measure […]

Acc 85771

Land held for speculative purposes should be classified as a short-term investment. The degree of separation of duties varies with the size of the business. TRUE Generally accepted accounting principles state that all business transactions should be valued at fair […]

ACC 96568

It is possible to allocate income or loss to partners based solely on interest. A different set of financial statements usually is prepared for each user. FALSE Corporate earnings are subject to double taxation. TRUE A limited partnership normally has […]

Accounting 59990

The purchasing department prepares a purchase requisition addressed to the vendor (seller) containing instructions related to the items ordered. There is no limit to the amount of income subject to the FUTA tax. FALSE Contributed capital is shown on a […]

Accounting 73581

The statement of owner’s equity relates the income statement to the balance sheet by showing how the owner’s capital account changed during the accounting period. The Retained Earnings portion of a corporation represents the initial contribution of capital to the […]

Accounting 89618

Winters Corporation purchased 15,000 shares of Poores Corporation common stock for $60 per share on January 2, 2014. Poores Corporation reported net income of $1,500,000 for 2014 and paid dividends of $300,000 during 2014. Poores has a total of 50,000 […]

ACCT 24873

Which of the following partnership characteristics is an advantage? A. Mutual agency B. Ease of dissolution C. Unlimited liability D. Limited life Which of the following is the most useful aid to the accountant in preparing closing entries? A. Journal […]

Acct 27647

Responsibility for ethical financial reporting rests solely with the accountant. A bond sells at the face value when the face interest rate of the bond is identical to the market interest rate for similar bonds on the date of the […]

Acct 32558

If an asset costs $41,000, has a residual value of $3,000, and has a useful life of five years, the entry to record depreciation in the second year, using the double-declining-balance method, is A. debit to Depreciation Expense, 9,430; credit […]

Acct 41696

Under the perpetual inventory system, the Cost of Goods Sold and Merchandise Inventory accounts are updated with each sale. Inventory is classified as a long-term asset. FALSE The work sheet is prepared after the formal adjusting and closing entries. FALSE […]

Acct 54099

The receiving department must compare goods received with goods purchased, as indicated on the purchase order. A partnership agreement need not be in writing. TRUE Unearned revenue arises from the acceptance of payment in advance for a service to be […]

ACCT 61342

In trend analysis, each item is expressed as a percentage of the A. net income amount. B. total assets amount. C. base year amount. D. retained earnings amount. An unrealistic picture of the inventory’s current value on the balance sheet […]

ACCT 76128

An estimated liability is not a definite obligation of the firm because the amount cannot be definitely determined. Held-to-maturity securities are always debt securities, and never equity securities. TRUE Based on past experience, it should be possible to estimate the […]

ACCT 80480

The relevance of accounting information means that the information has a direct bearing on a decision. Vertical analysis will reveal the percentage of net sales consumed by salaries expense. TRUE The day-by-day accumulation of interest is considered a transaction involving […]

Acct 90045

During the closing process, expenses are transferred to the debit side of the Income Summary account. The Sarbanes-Oxley Act requires a company to guarantee that its financial statements are 100 percent accurate. FALSE Partner A purchases partner B’s $3,000 interest […]

Acct 90445

Investments with a maturity of less than ninety days are generally classified as cash equivalents. Callable preferred stock is preferred stock that may be redeemed or retired at the option of the issuing corporation. TRUE Under the perpetual inventory system, […]

ACCT 96470

Use this information to answer the following question. These facts concern the long-term stock investments of DeBord Corporation: The entry to record the sale of 1,000 shares of Vanhook Corporation common stock is: A. Long-Term Investments 38,000 Cash 38,000 B. […]

ACT 42067

A company with a low debt to equity ratio is in a more vulnerable position during poor economic times than a company with a high debt to equity ratio. When the equity method is used to account for an investment […]

ACT 71082

It is possible to invest no tangible assets into a partnership, yet be given a positive opening capital balance. The post-closing trial balance will typically have more accounts than the adjusted trial balance. FALSE A building not currently used because […]

ACT 88495

Product warranties are an expense of the period in which the product is sold. A company that factors its receivables will have a less favorable receivable turnover than a company that does not factor. FALSE Revenue is equal to the […]

MET MG 13262

If the market interest rate at the date of issuance of a bond exceeds the face interest rate, the present value of the face value plus the present value of all the future interest payments will equal an amount less […]

MET MG 13412

In general, in times of rising prices, using FIFO has a favorable effect on cash flows. The accrual basis of accounting results in a more accurate measurement of net income for the period than does the cash basis of accounting. […]

MET MG 22638

Ending merchandise inventory for LIFO will be the same dollar amount under a periodic inventory system as under a perpetual inventory system. Mineral deposits are subject to a process called depletion. TRUE Trading securities are valued on the balance sheet […]

MET MG 38083

The matching rule is most closely related to the cash basis of accounting. The entry to record the retirement of treasury stock will include a debit to Common Stock for the par value of the retired shares. TRUE A decrease […]

MET MG 41926

If the market interest rate at the date of issuance of a bond exceeds the face interest rate, the bond will probably be sold at a discount. Social Security and Medicare taxes are borne entirely by the employee. FALSE On […]

MET MG 74737

The purchases journal is used to record only purchases made on credit. When compound interest is used, interest accumulates less quickly than when simple interest is used. FALSE When a partner invests a noncash asset into the partnership, the partner’s […]

MET MG 77535

The sale of treasury stock cannot result in A. an increase in Retained Earnings. B. the crediting of Paid-in Capital, Treasury Stock. C. the debiting of Paid-in Capital, Treasury Stock. D. an increase in total stockholders’ equity. An important purpose […]

MET MG 83703

Recording an account with a debit balance as a credit, or vice versa, will cause the trial balance to be out of balance by an amount that is evenly divisible by two. Dividend yield is the most important ratio associated […]

MET MG 91392

Trading securities are always short-term investments. The lower-of-cost-or-market rule implies that it is a violation of the conservatism concept to carry inventory at a cost that is in excess of its market value. TRUE Intangible assets are also called wasting […]

SMG AC 15052

When the periodic inventory system is used, a physical inventory should be taken at the end of the fiscal year. A capital lease is a lease of property, plant, or equipment that is in effect an installment purchase. TRUE The […]

SMG AC 21523

Closing entries are made A. to clear revenue and expense accounts of their balances. B. to clear withdrawals of its balance. C. to summarize a period’s revenues and expenses. D. All of these choices. Assume a company uses the periodic […]

SMG AC 24195

The amount recorded for Payroll Taxes and Benefits Expense is borne entirely by the employee. If a bond has a face interest rate of 6 percent, a face value of $40,000, and pays interest semiannually, each interest payment will amount […]

SMG AC 35688

A bond with a face value of $1,000 has a current price quote of 89.00. This bond is selling for A. $1090.00. B. $1040.00. C. $990.00. D. $890.00. Improperly classifying large expenditures as assets rather than expenses A. could constitute […]

SMG AC 60576

One of the benefits of forming a partnership is limited liability. Dividend yield is a liquidity ratio. FALSE Compound interest is computed quarterly on $700 for seven years at 12 percent annual interest. The future value table is used by […]

SMG AC 71418

The collection of a $2,000 account beyond the 2 percent discount period would result in a(n) A. increase to Cash for $1,960. B. decrease to Accounts Receivable for $2,000. C. decrease to Cash for $2,000. D. increase to Sales Discounts […]