1.

Carrying

Value

**

***

2.

3.

Rounded

To reduce to estimated residual value

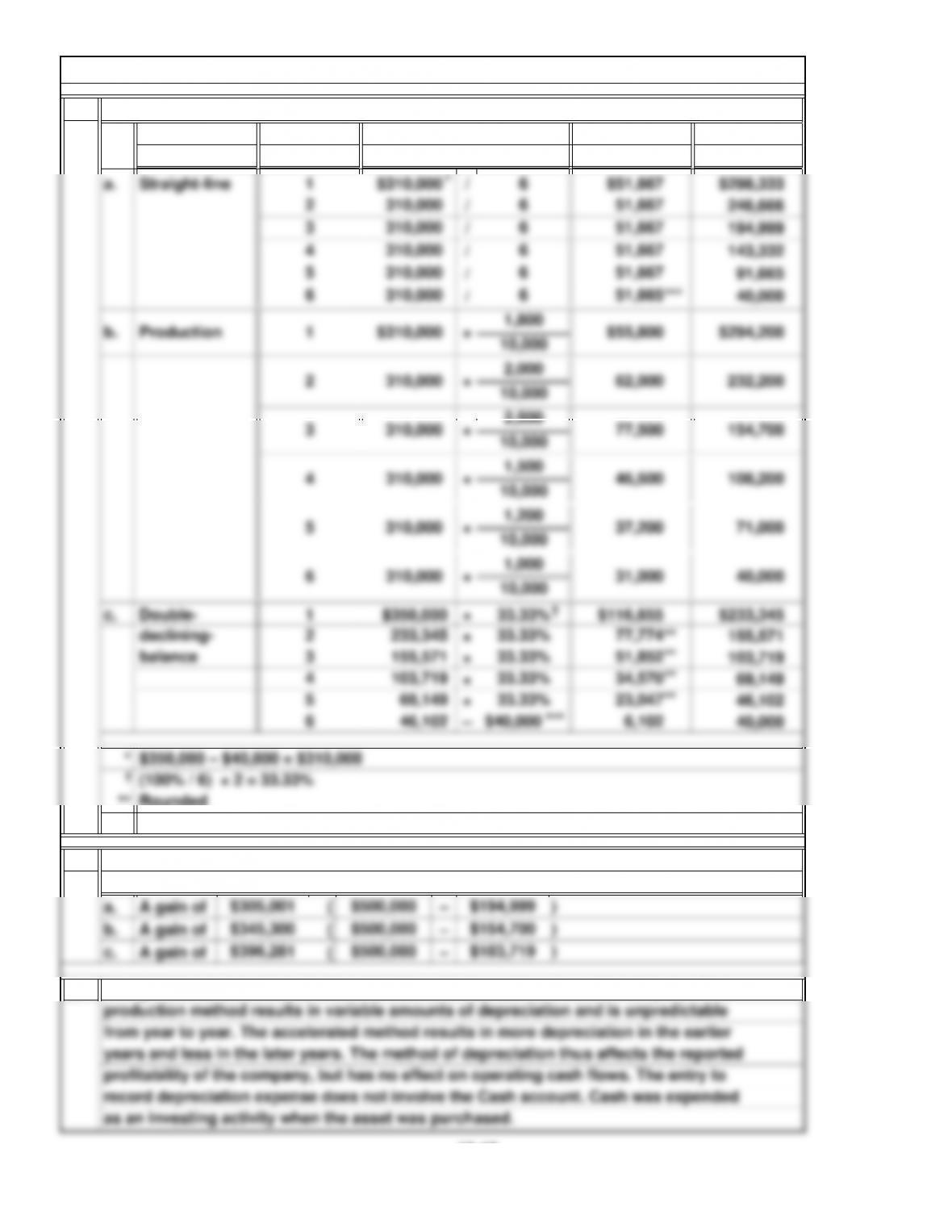

P7. Comparison of Depreciation Methods

If the printer was sold for $12,000 after year 2, the gain or loss under each method

follows:

Depreciation Table

Straight-line results in equal amounts of annual depreciation over the five years. The

Depreciation

Method Year Computation

Depreciation

10-17

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

Carrying

Value

Depreciation

Year Computation

Depreciation

Method

Depreciation Table

P8. Comparison of Depreciation Methods

10-18

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

b.

5.

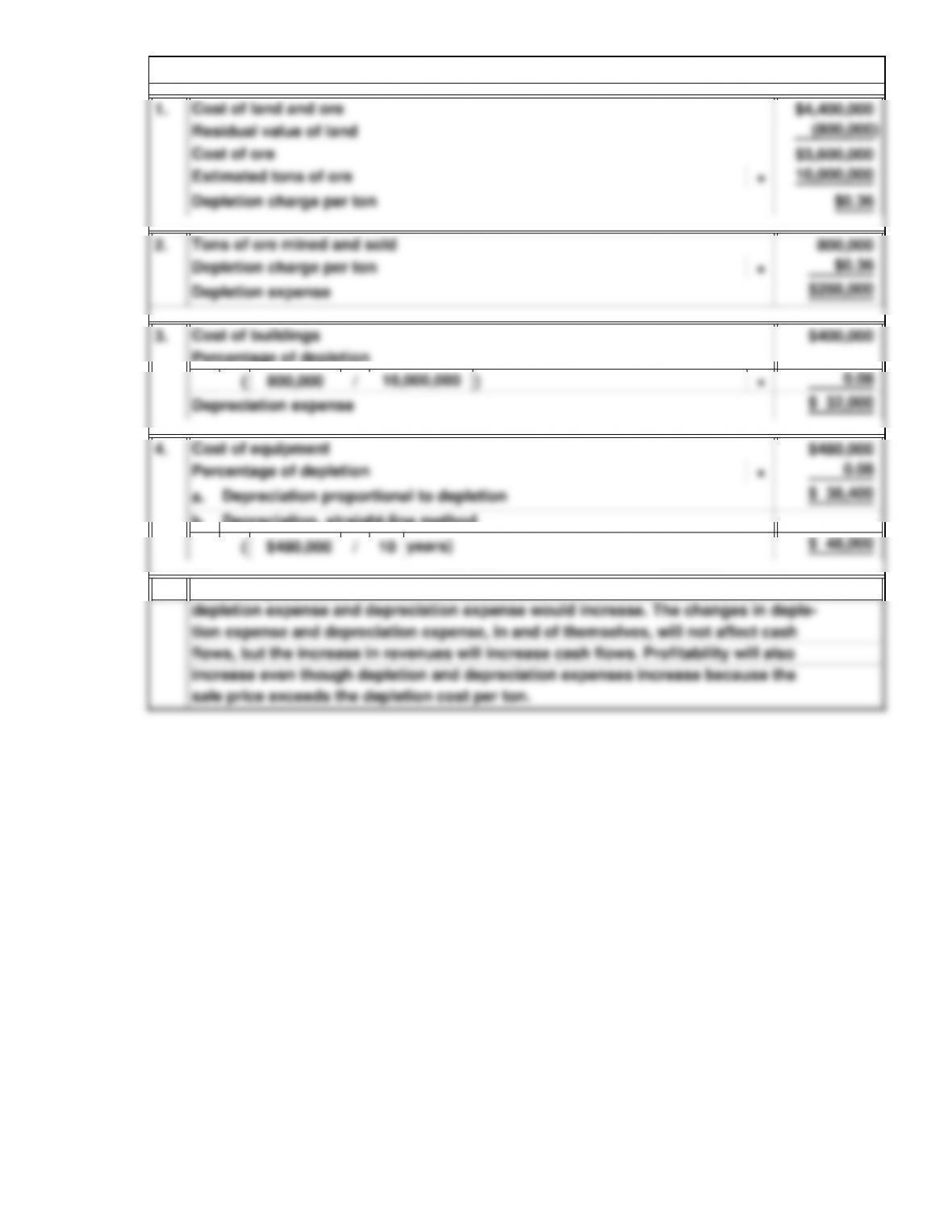

P9. Natural Resource Depletion and Depreciation of Related Plant Assets

Depreciation, straight-line method

If the company sold and mined 1,000,000 tons of ore instead of 800,000, the amount of

10-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Cases

C3. Conceptual Understanding: Accounting Estimates

return on assets. Therefore, a comparison of these two companies would result in Marriott

terioration that will occur and the rate at which the asset will become obsolete.

are the estimated useful life and the residual value. The two most important factors that

must be taken into consideration in making these estimates are the extent of physical de-

The two principal estimates that must be made to compute the annual depreciation charge

C1. Conceptual Understanding: Effect of Change in Estimates

C4. Interpreting Financial Reports: Brands

The advantage to the airlines of increasing the useful life of aircraft is that the annual de-

Brands are recorded when purchased from other companies; therefore Starwood’s asset

appearing to outperform Starwood.

10-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

3.

When evaluating assets for impairment, CVS first compares the carrying value of the

Property, equipment, and improvements to leased premises are depreciated using

the straight-line method. Estimated useful lives generally range from 10 to 40 years

for buildings, building improvements, and leasehold improvements, and 3 to 10

years for fixtures and equipment and internally developed software. CVS will have

and equipment have shorter useful lives than the buildings.

ciated over the life of the leases and thus reduce income by the amount of the de-

preciation (excluding tax effects).

Leasehold improvements are improvements to leased property that become the

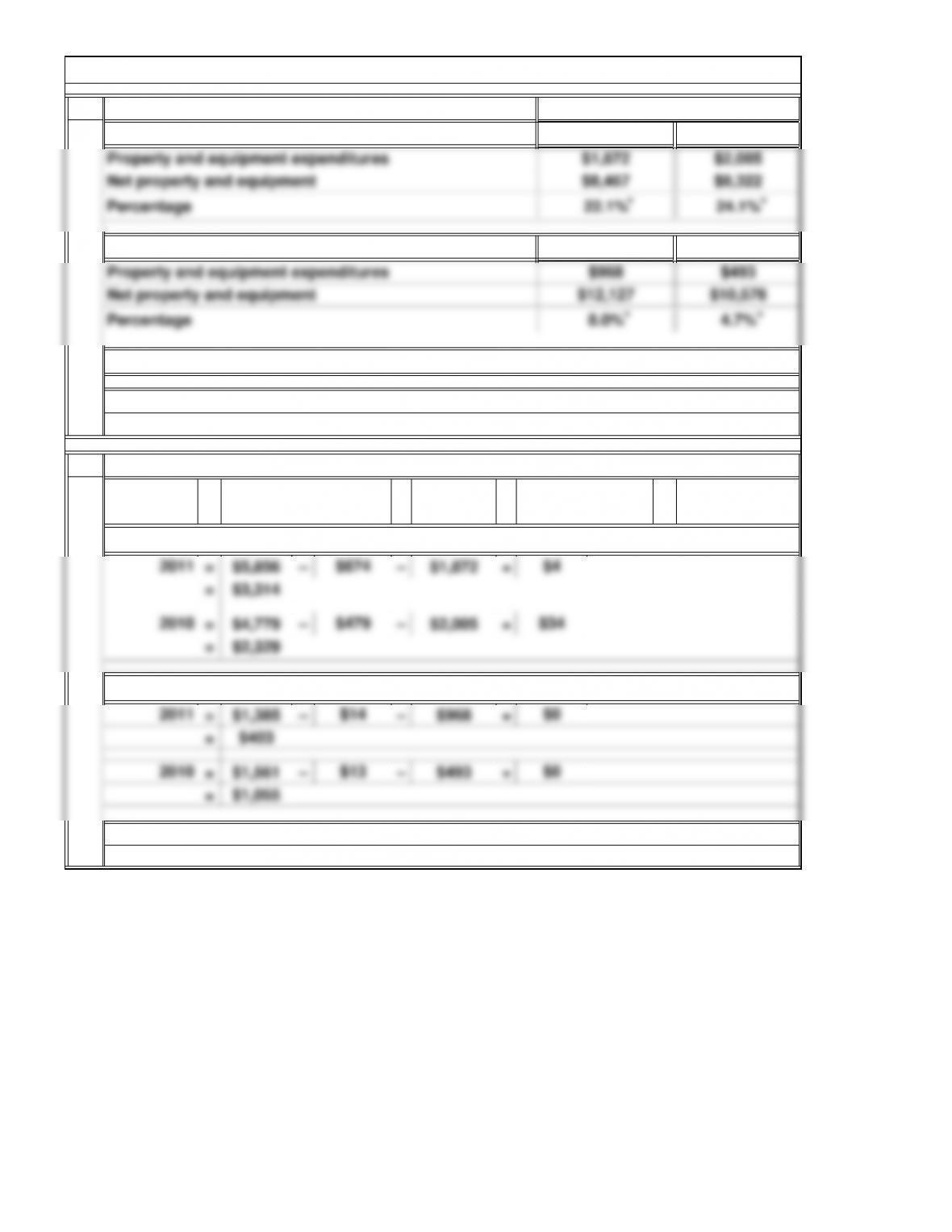

C5. Annual Report Case: Long-Term Assets

In 2011, property and equipment, net constituted 13.1 percent ($8,467 / $64,543)

of total assets.

The main components of property and equipment were land, building and improve-

used in this analysis are less than the carrying amount of the asset, an impairment

to remodel its stores several times over the life of the buildings because the fixtures

10-21

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

= $1,385 – – $968 +

= $1,561 – – $493 +

= $1,055

$132010 $0

2011 $0

Purchases of

Plant Assets Sales of

Plant Assets

(in millions)

part of their expansion through operations.

Both companies have positive free cash flow. This means both companies can fund

$14

Southwest

=

CVS

–– +

Free

Cash Flow

Southwest is growing its property and equipment more rapidly (from 4.7% to 8.0%

CVS 2011

C6. Comparison Analysis: Long-Term Assets and Free Cash Flows

(in millions)

2010

Dividends

Net Cash Flows from

Operating Activities

per year).

*Rounded

10-22

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

C8. Continuing Case: Annual Report Project

judgment. However, some reasonable allocation can usually be made based on separate

appraisals of the land and the building. The company and therefore the people who have

a stake in it, such as the stockholders and management, would probably benefit from the

approach that would save income taxes. Thus, to the extent that an appraisal of the rela-

plan) will have a possible effect on cash flows in that it will reduce income taxes by

$32,400 compared to the CFO’s plan. This is an ethical dilemma to the extent that one or

the other of the plans is a false representation of the true situation. In cases like this, the

true allocation between land and building is unlikely to be precise and is a matter of

Depreciation in and of itself does not affect cash flows because it is an allocation of the

cost of purchase and does not require a cash outlay when it is recorded. However, cash

C7. Ethical Dilemma: Ethics and Allocation of Acquisition Costs

Note to Instructor: Answers will vary depending on the company selected by the students.

10-23

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.