Chapter 12

Accounting for Partnerships

Learning Objectives

1. Dene the partnership form of business, and identify its principal characteristics.

2. Record partners’ investments of cash and other assets when a partnership is formed.

3. Compute and record the income or losses that partners share, based on stated ratios,

capital balance ratios, and partners’ salaries and interest.

4. Record a person’s admission to or withdrawal from a partnership

5. Compute and record the distribution of assets to partners when they liquidate their

partnership.

6. Identify alternate forms of partnership-type entities.

Section 1: Concepts

Concept

Separate entity

Lecture Outline

I. A partnership is an association of two or more persons to carry on as co-owners of a

business for prot.

II. Partnerships are considered separate accounting entities but not separate legal

entities.

III. The partnership form of business has the following important characteristics:

A. A partnership is a voluntary association.

B. A partnership agreement should outline the following details:

1. Name, location, and purpose of the business

2. Names of the partners and their respective duties

3. Investments of each partner

4. Method of distributing income and losses

5. Procedures for the admission and withdrawal of partners, the withdrawal of

assets allowed each partner, and liquidation of the business

C. A partnership has limited life and may be dissolved when:

1. A new partner is admitted.

2. When a partner withdraws, goes bankrupt, is incapacitated, or dies

3. When the terms of the partnership agreement are met, if the partnership. was

formed for the completion of a specic project.

D. A partnership is a mutual agency

1. Any partner can bind the partnership to a business agreement as long as it is

within the scope of the business’s normal operations.

E. Each partner has personal unlimited liability for partnership debts.

F. Invested property becomes jointly owned.

G. Each partner has the right to share income and the responsibility to share

losses.

1. Income and losses do not have to be distributed in the same proportions.

2. If partnership agreement does not describe how losses are distributed, then

the losses are distributed the same way as income.

3. If partnership agreement does not describe income or loss distributions, the

partners share income and losses equally

IV. A partnership’s advantages include that it:

A. Is easy to form, change, and dissolve.

B. Facilitates pooling of capital and individual talents.

C. Has no corporate tax burden.

D. Allows 8exibility.

V. A partnership’s disadvantages include that it:

A. Has limited life.

B. Can bind an unwilling partner to a contract through mutual agency.

C. Gives unlimited personal liability to the partners.

D. Is more di9cult to raise capital and transfer ownership for a partnership than

for a corporation.

Summary

A partnership is an association of two or more persons to carry on as co-owners of

business for prot. Partnerships are treated as separate entities with their own accounting

records and nancial statements. However, there is no legal separation between the partner

and the partnership. A partnership is a voluntary association of individuals. The partnership

does not have to be in writing, but it is good business practice to put the agreement in

writing. Partnership agreements should clearly state:

Name, location, and purpose of the business

Names of the partners and their respective duties

Investments of each partner

Method of distributing income and losses

Procedures for the admission and withdrawal of partners, withdrawal of assets

allowed each partner, and liquidation of the business

Partnerships have a limited life in that the partnership may be dissolved upon admission,

withdrawal, bankruptcy, incapacity, or death of a partner. Under the concept of mutual

agency, each partner can act as an agent for the partnership, binding the partnership to

business agreements as long as they are in the scope of the business’s normal operations.

Each partner has personal unlimited liability for the debts of the partnership. When

individuals invest property in a partnership, the property becomes an asset of the

partnership and is owned jointly by the partners. Each partner has the right to share in the

income and the responsibility to share in the losses of the partnership as stated in the

partnership agreement. If the partnership agreement is silent regarding loss distributions,

then losses will be distributed in the same way as income. If the partnership agreement is

silent regarding income and losses, then income and losses are shared equally by the

partners.

Advantages of a partnership include that it:

Is easy to form, change, and dissolve

Facilitates pooling of capital and individual talents

Has no corporate tax burden

Allows 8exibility

Disadvantages of a partnership include that it:

Has limited life

Can bind an unwilling partner to a contract through mutual agency

Gives unlimited personal liability of the partners

Is more di9cult to raise capital and transfer ownership for a partnership than

for a corporation

Teaching Strategy

Students should be reminded that a partnership is a separate entity for accounting and

reporting purposes, but there is no legal separation between partner and partnership.

Review the characteristics of partnerships focusing on the details of a partnership

agreement, limited life, mutual agency, single level of taxation, and unlimited liability.

Emphasize that unlimited liability is often addressed by the formation of LLCs which will be

discussed in a later section of the chapter. Then walk through the advantages and

disadvantages of partnerships.

Explain that property invested in the partnership becomes an asset of the partnership,

owned jointly by all the partners. Each partner has the right to share in the company’s

income and the responsibility to share in its losses. For accounting purposes, however, the

partnership is treated as a separate entity with its own accounting records and nancial

statements.

Short Exercise 1 and Exercises 1A and 2A apply to this section.

Section 2: Accounting Applications

Accounting Applications

Record partners’ investments

Compute and record income and loss

Record a person’s admission to or withdrawal from a partnership

Compute and record distribution of assets to partners when a partnership is

liquidated

Lecture Outline

I. In accounting for partners’ equity, it is necessary to maintain separate Capital and

Withdrawals accounts for each partner.

A. When recording a partner’s investment:

1. Debit Cash for the amount of cash contributed.

2. Debit other asset accounts for the fair market value of any contributed assets.

3. Credit Partner, Capital for the total amount invested.

II. Income and losses may be distributed according to whatever method the partners

specify in the partnership agreement.

A. Income may be distributed based on stated ratios.

B. Income may be distributed according to capital balances with ratios based on:

1. Beginning capital balances.

2. Average capital balances.

C. Income may be distributed through a combination of salaries, Interest, and

stated ratios.

1. Partners may rst be paid a salary with the remainder of income (or loss)

distributed based on stated ratios.

2. Partners may rst be paid interest on their capital investments with the

remainder of income (or loss) distributed based on stated ratios.

3. Partners may rst be paid a salary, followed by a distribution for interest, with

the remainder (positive or negative) distributed based on stated ratios.

III. Dissolution of a partnership occurs when there is a change in the original association of

partners.

A. Admission of a new partner dissolves the old partnership.

1. When purchasing full interest from an original partner:

a. Actual amount paid is personal matter between individuals.

b. Ownership is transferred to new Capital account.

2. When purchasing partial interest from partners:

a. Original Capital accounts are decreased and new Capital account is

increased.

b. Asset accounts may need to be adjusted to current values with creation

of new entity.

3. When a new partner is admitted through an investment of assets, both assets

and equity increase.

4. When a new partner pays more than the value of the interest received, a

bonus is distributed to the old partners’ Capital accounts.

5. When a partner pays less than the value of the interest received, a bonus to

the new partner is transferred from old partners’ Capital accounts.

B. A partner may withdraw from a partnership in one of several ways.

1. When a partner withdrawals by selling his or her interest, it does not change

the partnership assets or the partners’ equity.

2. A partnership withdrawal may allow removal of assets equal to the

withdrawing partner’s interest.

C. When a partner dies, the partnership is dissolved.

1. The remaining partners may purchase the deceased’s equity, sell it to

outsiders, and/or deliver certain business assets to the deceased’s estate.

2. If the rm intends to continue, a new partnership is formed.

IV. Liquidation is a special form of partnership dissolution.

A. Assets are sold to pay liabilities, and remaining assets are distributed to

partners.

B. The business will not continue.

C. With a gain on the sale of assets, the cash distributed to partners is the

balance in their respective Capital accounts.

D. With a loss on the sale of assets, partners share the loss based on their stated

ratios.

1. If the loss is greater than a partners’ capital balance, the diAerence must be

paid out of personal funds.

2. If personal funds are inadequate, the remaining partners share the loss.

E. The balance sheet for a partnership is structured as shown in text Exhibit 5.

Summary

Owner’s equity in a partnership is called partners’ equity. Each partner has a separate

capital account. Each partner invests cash or other assets or both in the partnership

according to the partnership agreement. Noncash assets are valued at fair market value on

the date of transfer to the partnership.

The following journal entries are introduced in this section for initial partner investments:

Cash XX

Noncash Assets XX (at FMV)

Partner A, Capital XX

Initial investment of cash and noncash assets

Cash XX

Noncash Assets at FMV XX (at FMV)

Notes Payable XX

Partner B, Capital XX

Initial investment of cash and noncash assets plus a note payable

Partnership income and losses can be distributed according to whatever method is specied

in the partnership agreement. Income and losses can be distributed based on stated income

and loss ratios for each partner. Income and losses can be distributed based on capital

balance ratios, using either beginning capital balances or average capital balances. Income

and losses can also be distributed based on a combination of salaries, interest on capital

balances, with the remainder (positive or negative) distributed based on stated ratios.

Income and loss sharing ratios need not be the same. If the partnership is silent as to loss

ratios, then losses are distributed in the same ratios as the income ratios. A partnership

agreement can be simple or complex. Depending on the partnership agreement, income and

loss ratios can be distributed based on whatever the partners agree to with their attorneys.

The following example of income sharing ratios based on beginning year capital balances is

provided in the text:

…..

…..

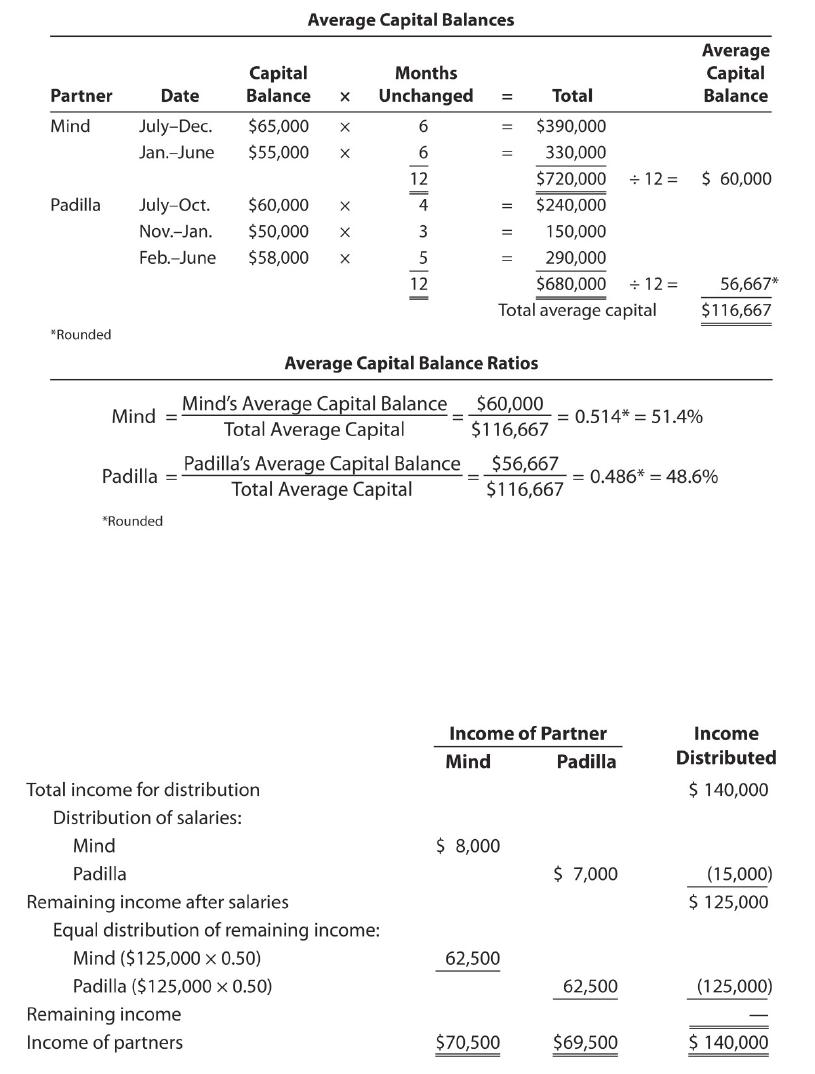

The following example of income sharing ratios based on average capital balances is

provided in the text:

…..

……..

The following example of income sharing using salaries with the remaining income (positive

or negative) distributed based on stated ratios is provided in the text:

…….

…….

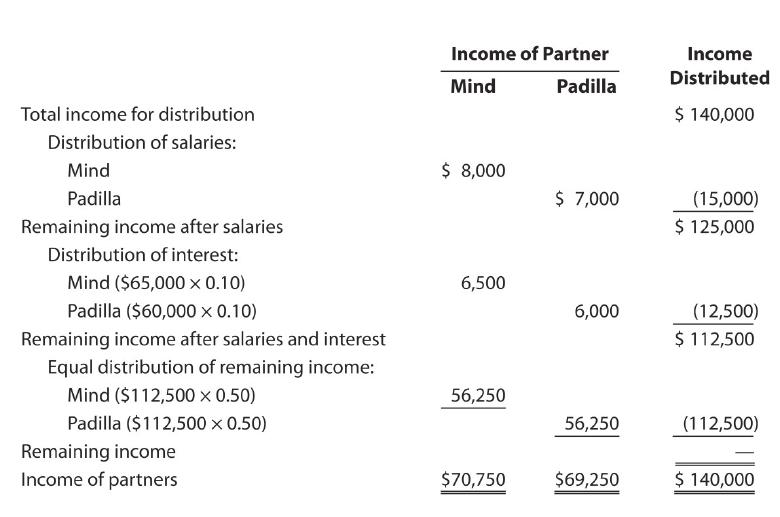

The following example of income sharing using salaries as the rst step, interest on

beginning capital balances as the second step, with the remaining income (positive or

negative) distributed based on stated ratios is provided in the text:

……

………