Issuing bonds between interest payment dates will have the effect of decreasing a bond

issuance discount or increasing a bond issuance premium.

Once an owner of convertible preferred stock has converted to common, he or she

cannot convert back to preferred.

Accounting methods may be a source of incomparability among companies.

One way of stating the accounting equation is: Assets – Liabilities = Owner’s Equity.

Treasury shares are shares that are authorized but unissued.

It is unlikely that a company would want to bond its employees who handle cash or

inventory.

The use of major credit cards does not require sellers to establish the customer’s credit.

The amount of property tax payable is usually an estimated liability for a portion of the

year.

A natural resource is expensed in the year it is extracted rather than when it is sold.

The general ledger is used to record the details of each transaction. The general journal

is used to update each account.

All decreases in owner’s equity are a result of expenses.

If a retailer makes a sale of $100 on a MasterCard, and MasterCard takes a 5 percent

discount on the sale, the retailer would record Cash for $100 and Accounts Payable for

$5.

Overhauling a company’s cooling system is an example of an extraordinary repair.

Normally, the value of an asset remains at its initial fair value or cost until the asset is

sold, expires, or is consumed.

In accounting, depreciation refers to the decline in fair value of a plant asset.

Accelerated methods of depreciation result in lower net income in the last years of an

asset’s life compared to the straight-line method.

It is not possible for one company to influence the operating policies of another

company unless it owns more than a 50 percent interest in that company.

The declaration of dividends is solely the decision of the corporation’s board of

directors.

In a liquidation, one partner may have to make up the deficit in another partner’s

account.

Cash and inventory are very vulnerable to theft.

The present value of a bond is determined by subtracting the discounted value of the

payment at maturity from the discounted value of a series of fixed interest payments.

The copyright granting the exclusive rights to sell artistic materials and computer

programs ends with the author’s life.

Liabilities related to assets invested in a partnership by a new partner can be transferred

to the partnership.

On a work sheet, the balance of the owner’s Capital account is its ending amount for the

period.

The inventory turnover measures the relative size of the inventory and the effectiveness

of credit policies.

At the time a company signs a contract to pay an employee a certain salary in the

future, it records a liability.

Net income is misleading when revenue is overstated or expenses are understated by

significant amounts.

The operating cycle involves the purchase and sale of merchandise inventory as well as

the subsequent collection of cash from credit sales.

If bonds are retired by an issuer by purchase on the open market at a price below the

bonds’ carrying value, a loss will result.

The cost-benefit convention holds that the benefits to be gained from providing

accounting information should be greater than the costs of providing it.

Unsecured bonds are also known as debentures.

Owner’s withdrawals should appear on the statement of owner’s equity.

A company with a profit margin of 6 percent earns sixty cents profit for every dollar of

net sales.

When bonds are sold between the interest payment dates, the issuing corporation pays

to investors the interest that has accrued since the last interest payment date.

The LIFO method tends to create peaks and valleys in the business cycle.

A company’s management can improve overall profitability by decreasing the profit

margin,

the asset turnover, or both.

Unless there is evidence to the contrary, an investor owning 35 percent of the stock of

an investee is assumed to have significant influence.

On a statement of cash flows prepared using the direct method, the FASB requires that

cash payments for interest be classified as operating activities.

Because accounting measures should be verifiable, liabilities should not be estimated.

Match the following financial statement ratios with their definition.

1) Working capital _____

2) Current ratio _______

3) Profit margin ______

4) Return on assets______

5) Debt to equity ratio________

6) Return on equity_______

7) Asset turnover_________

a. A measure of profitability that shows the proportion of a company’s assets that is

financed by creditors and the proportion financed by owners

b. A measure of liquidity that shows the net current assets on hand to continue business

operations

c. A measure of profitability that relates the amount earned by a business to the owner’s

investment in the business

d. A measure of profitability that shows the percentage of each sales dollar that results

in net income

e. A measure of liquidity; current assets divided by current liabilities

f. A measure of profitability that shows how efficiently a company uses its assets to

produce income

g. A measure of how efficiently assets are used to produce sales

A result of a separation of duties is that

A. operations become extremely inefficient because of constant training of employees.

B. more employees will need to be bonded.

C. theft by employees becomes impossible.

D. theft is possible only if several employees scheme together

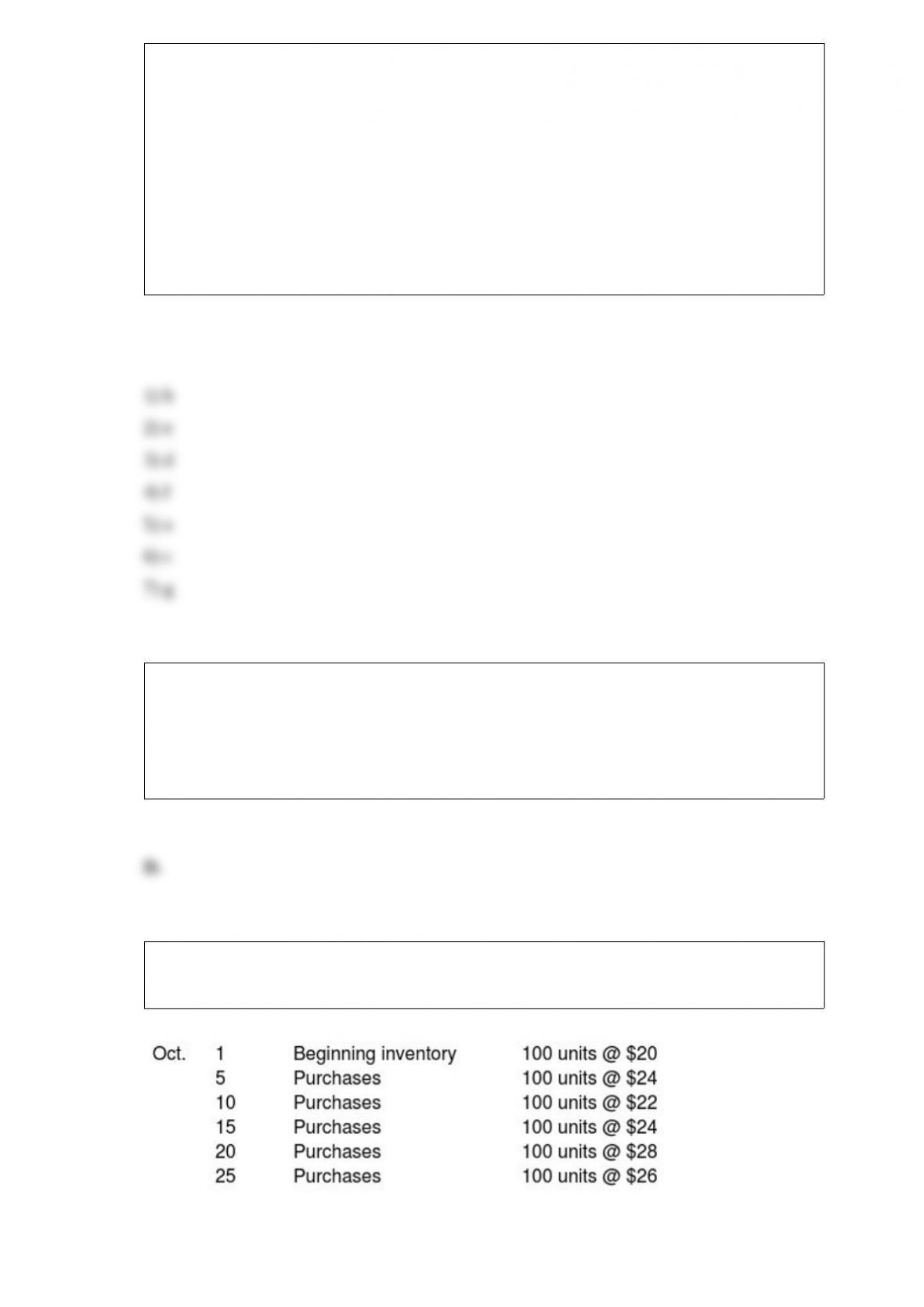

Graczyk Company uses a periodic inventory system. During October, it sold 360 units

of Product Z. Its beginning inventory and purchases during the month were as follows:

Compute the cost of goods sold under each of three methods: (a) average-cost, (b) LIFO,

and (c) FIFO. (Show your work.)

a. Average-cost: (100 $20) + (100 $24) + (100 $22) + (100 $24) + (100 $28) + ($100 $26)

= $14,400; 14,400 600 = $24; $24 360 = $8,640

b. LIFO: (100 $26) + (100 $28) + (100 $24) + (60 $22) = $9,120

c. FIFO: (100 $20) + (100 $24) + (100 $22) + (60 $24) = $8,040

The entry to record the sale of equipment costing $40,000, with accumulated

depreciation of $34,000 and sale price of $7,700, will include

A. a gain on sale of equipment of 1,700.

B. a gain on sale of equipment of 7,700.

C. a loss on sale of equipment of 32,300.

D. a loss of sale of equipment of 26,300.

Which of the following is expressed in terms of a percentage?

A. Return on equity

B. Current ratio

C. Asset turnover

D. Working capital

In some liquidations, a partner’s share of the loss is greater than his or her capital

balance. In such a situation,

A. the partner must make up the deficit in his or her Capital account from personal

assets.

B. if the partner does not have the cash to cover his or her obligations, the deficit is

distributed according to the partners’ stated ratios.

C. all partners have unlimited liability.

D. All of these choices.

Bond issue costs

A. must be expensed when incurred.

B. must be amortized over the life of the bonds.

C. are recorded in an asset account and not amortized.

D. appear on the balance sheet as a liability.

When an adjusting entry is made debiting an expense account, the credit can be made to

any of the following accounts except

A. a liability.

B. a contra-asset account.

C. an asset.

D. a revenue.

Use this information to answer the following question.

A periodic inventory system is used.

Using the average-cost method, the cost assigned to ending inventory is

A. $3,036.

B. $3,168.

C. $3,384.

D. $8,556.

The depletion calculation is similar to which of the following depreciation methods?

A. Double-declining-balance

B. Straight-line

C. Group

D. Production

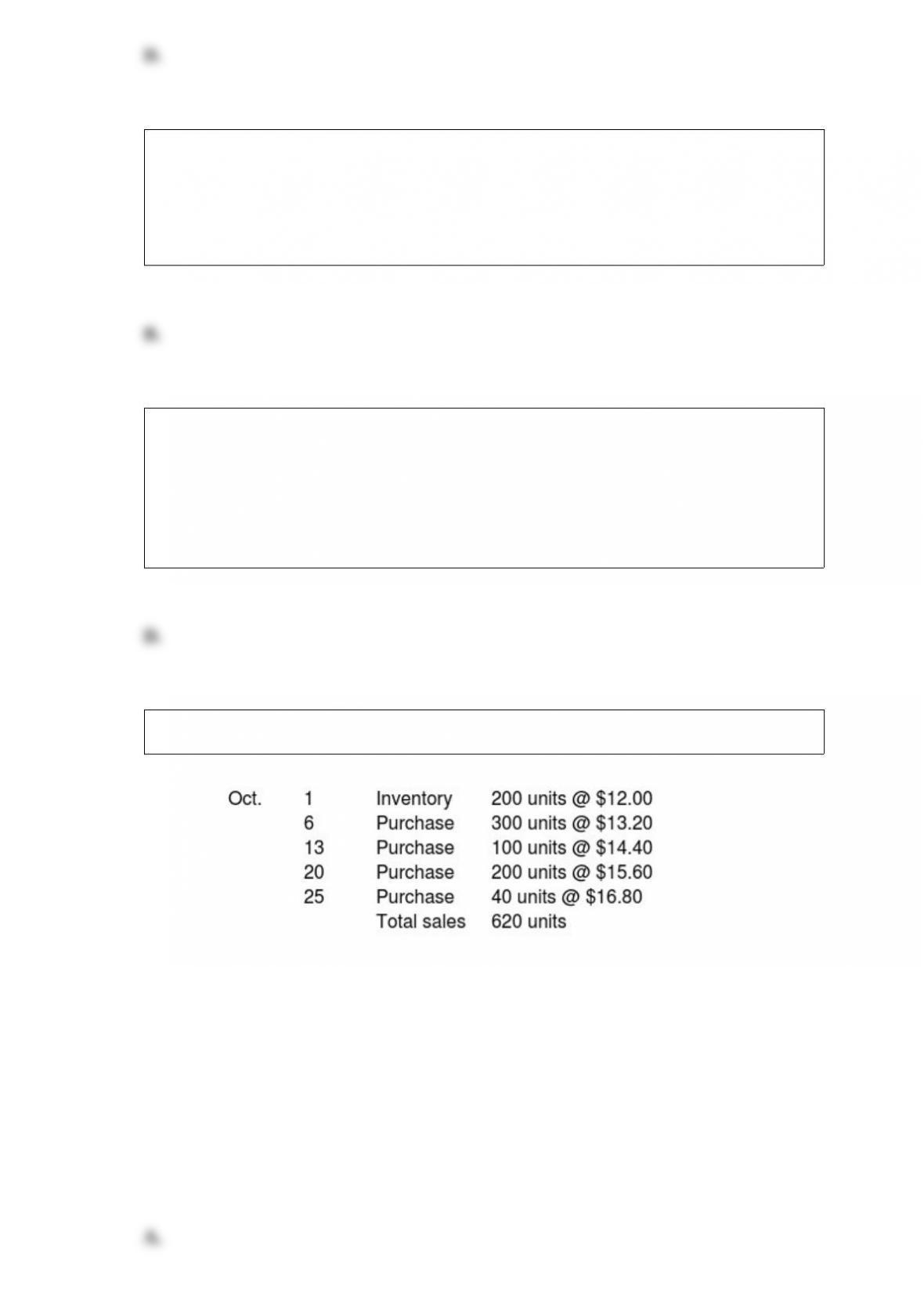

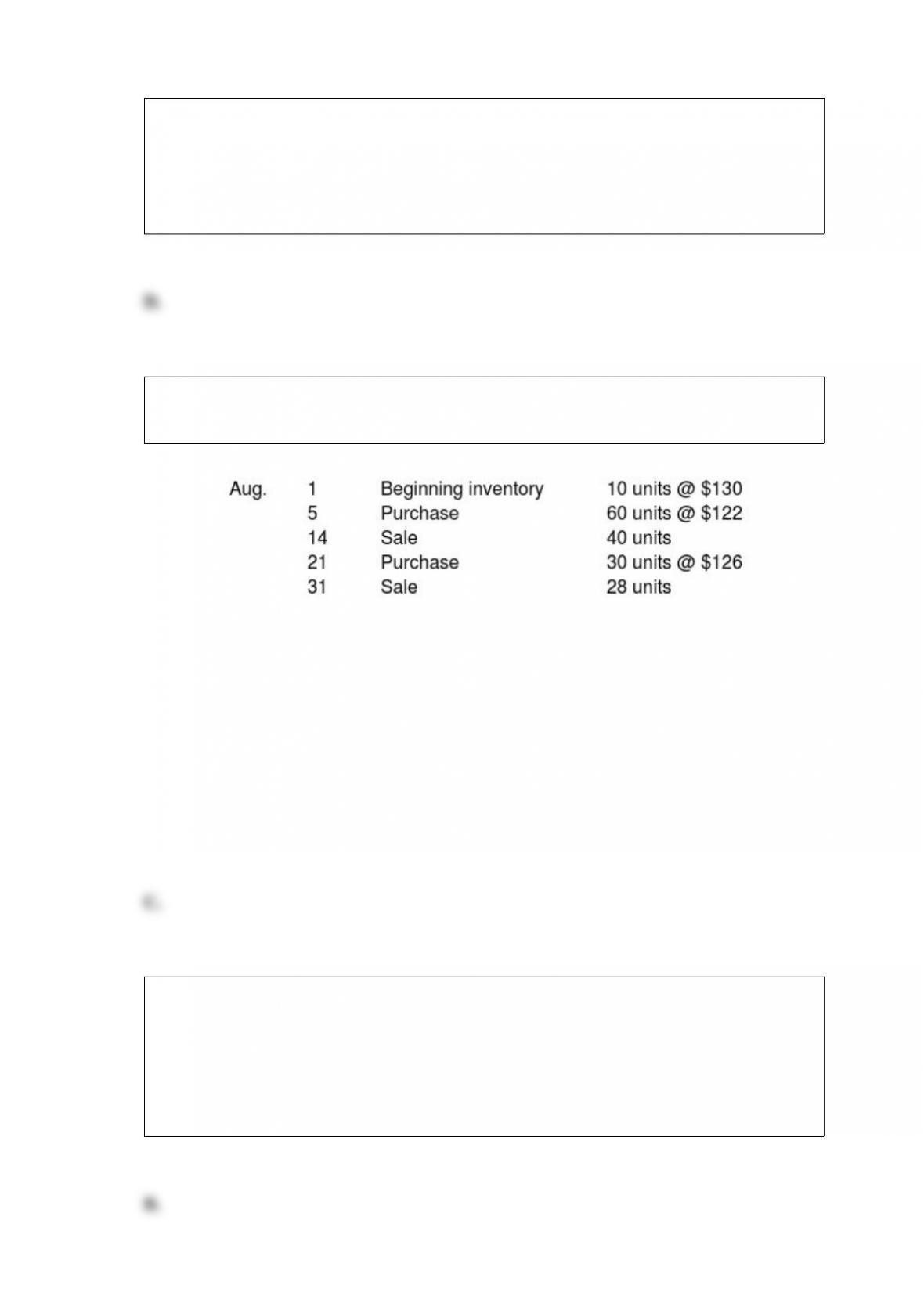

Use this inventory information for the month of August to answer the following

question.

Assuming that a perpetual inventory system is used, what is ending inventory on a FIFO

basis?

A. $3,904

B. $3,984

C. $4,024

D. More information is needed.

Which of the following must be reported by diversified companies for each of their

operating segments?

A. Segment profit or loss, expenses, and earnings per share

B. Segment profit or loss, certain revenue and expense items, and segment assets

C. Assets, liabilities, and earnings per share

D. Segment profit or loss, expenses, and unidentifiable assets

When special-purpose journals are used, which of the following is an entry that would

be recorded in the general journal rather than in a special journal?

A. Sale of merchandise on account.

B. Cash purchase of merchandise for resale.

C. A return of merchandise bought on account.

D. Cash receipt from a customer for payment on their account.

For available-for-sale equity securities, the Unrealized Loss on Long-Term Investments

account should be reported as a(n)

A. realized loss item on the income statement.

B. prior period adjustment.

C. contra-asset on the balance sheet.

D. other comprehensive income (loss).

Average inventory equals $200,000, and cost of goods sold equals $442,000. Days’

inventory on hand equals

A. 165.2 days.

B. Not enough information available to answer the question.

C. 154.3 days.

D. 188.7 days.

Use the following information to answer the question below.

When Langston Corporation was formed on January 1, 20×5, the corporate charter

provided for 100,000 shares of $10 par value common stock. The following transactions

were among those engaged in by the corporation during its first month of operation:

1) The corporation issued 400 shares of stock to its lawyer in full payment of the

$10,000 bill for assisting the company in drawing up its articles of incorporation and

filing the proper papers with the state agency.

2) The company issued 16,000 shares of stock at a price of $50 per share.

3) The company issued 14,000 shares of stock in exchange for equipment that had a fair

market value of $320,000.

The entry to record transaction 3 is:

A. Equipment 320,000

Common Stock 320,000

B. Common Stock 140,000

Equipment 140,000

C. Equipment 140,000

Common Stock 140,000

D. Equipment 320,000

Which of the following forms of organization are considered to be separate entities by

accountants?

A. Partnerships only

B. Sole proprietorships only

C. Corporations only

D. Sole proprietorships, partnerships, and corporations

Goods held on consignment are

A. kept for sale on the premises of the consignee.

B. included as part of no one’s ending inventory.

C. owned by the consignee.

D. included in the consignee’s ending inventory.

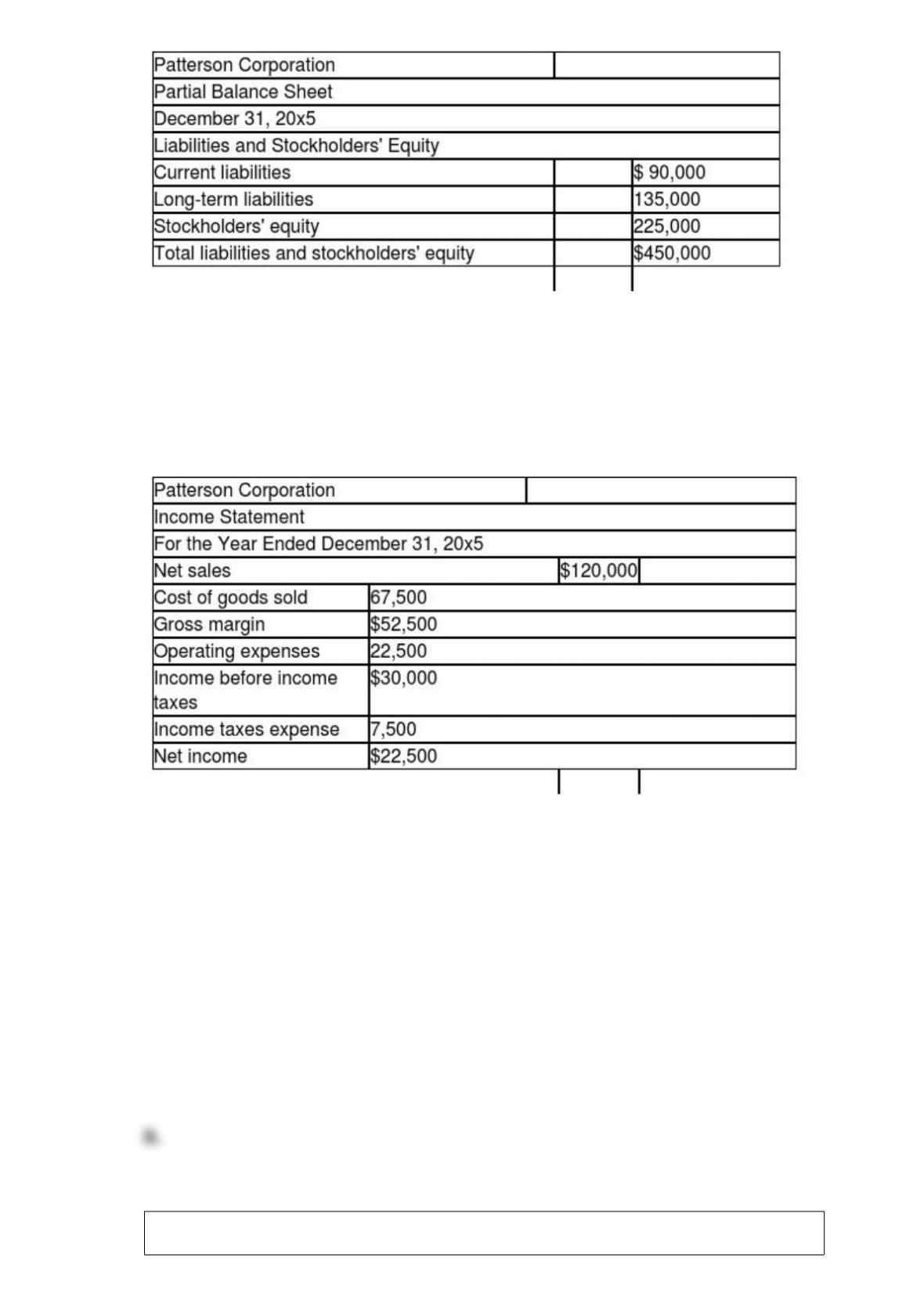

The following information pertains to Patterson Corporation. Assume that all balance

sheet amounts represent both average and ending figures.

Patterson Corporation had 6,000 shares of common stock issued and outstanding. The

market price of Patterson common stock on December 31, 20×5, was $20. Patterson paid

dividends of $0.90 per share during 20×5.

What is the return on equity for this corporation? Round your answer to 1 decimal place.

A. 5.0 percent

B. 10.0 percent

C. 23.3 percent

D. 53.3 percent

Which of the following items is associated with a purpose of the work sheet?

A. Recording adjusting entries.

B. Financial statements that are up to date for measuring financial progress.

C. Preparing budgets.

D. All of these choices.

Leah, Cameron, and Ryan each receive a $20,000 salary, as well as 10 percent interest

on their respective average investments of $120,000, $200,000, and $40,000. If they

share remaining income and losses in a 2:1:3 ratio, respectively, by how much would

Cameron’s account increase or decrease (indicate a decrease by placing parentheses

around the amount), assuming (a) net income of $144,000, (b) net income of $72,000,

and (c) net loss of $72,000.

Use the following information to answer the question below.

On January 1, 20×5, Falcon Corporation had 40,000 shares of $10 par value common

stock issued and outstanding. All 40,000 shares had been issued in a prior period at $17

per share. On February 1, 20×5, Falcon purchased 1,000 shares of treasury stock for

$19 per share and later sold the treasury shares for $26 per share on March 2, 20×5.

The entry to record the sale of the treasury shares on March 2, 20×5 is

A. Cash 26,000

Common Stock 19,000

Retained Earnings 7,000

B. Cash 24,000

Retained Earnings 2,000

Treasury Stock, Common 26,000

C. Cash 26,000

Treasury Stock, Common 19,000

Gain on Treasury Stock, Common 7,000

D. Cash 26,000

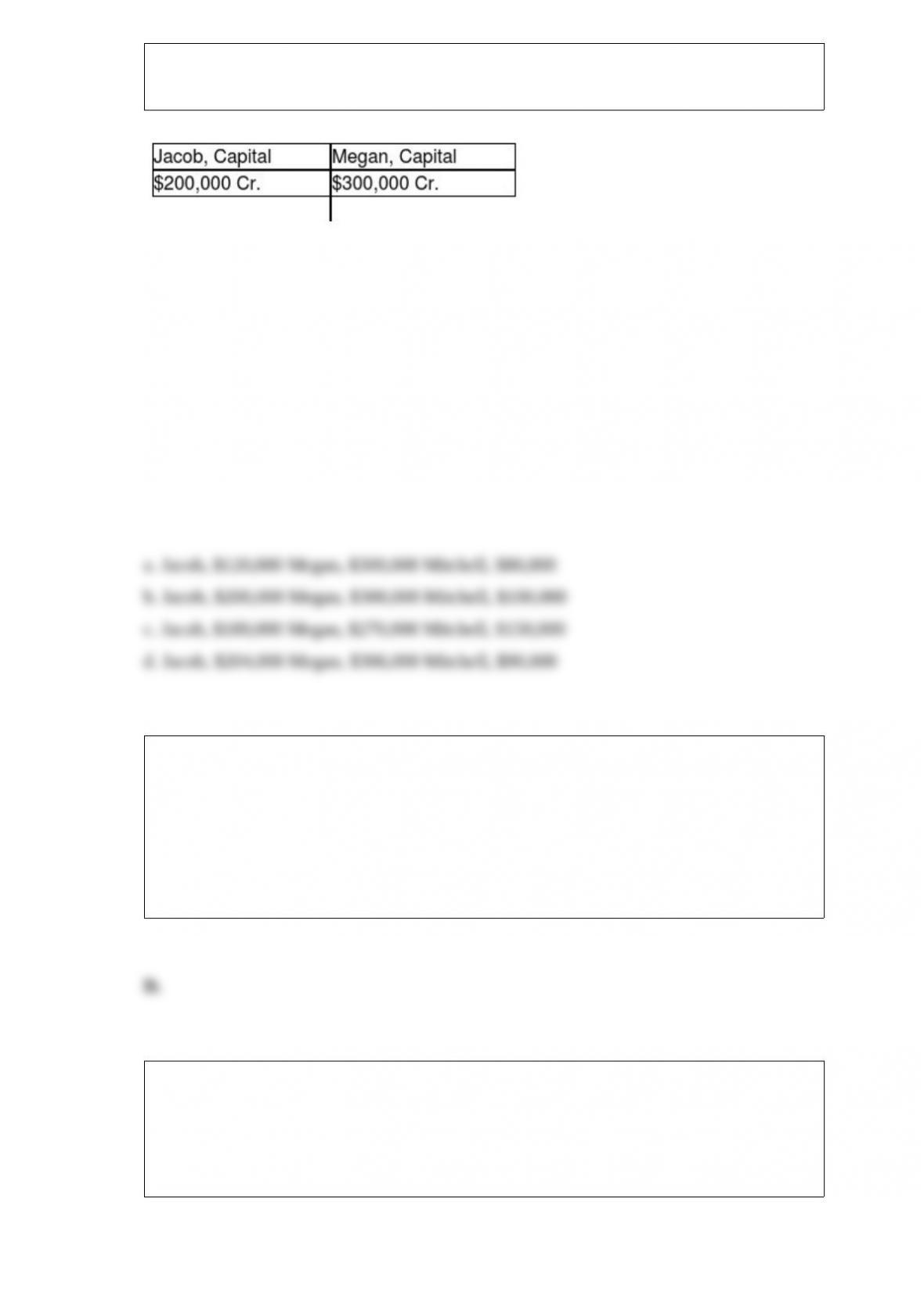

Jacob and Megan are partners who share profits and losses in a ratio of 2:3,

respectively, and have the following capital balances on September 30, 20×5:

The partners agree to admit Mitchell to the partnership. Calculate the capital balances of

each partner after the admission of Mitchell, assuming that bonuses are recorded when

appropriate for each of the following assumptions:

a. Mitchell pays Jacob $100,000 for 40 percent of his interest

b. Mitchell invests $100,000 for a one-sixth interest in the partnership

c. Mitchell invests $100,000 for a 25 percent interest in the partnership

d. Mitchell invests $100,000 for a 15 percent interest in the partnership

A truck that cost $24,000 and on which $18,000 of accumulated depreciation has been

recorded was disposed of on January 1. Assume that the truck was disposed of for

$4,000 cash. The entry to record this event would include

A. a debit to Cash.

B. a debit to Accumulated Depreciation.

C. a debit to Loss on Sale of Truck.

D. all of these choices.

When special journals are used, the general journal is used to record

A. purchase returns.

B. sales of merchandise on credit.

C. receipts of cash.

D. purchases on credit.

Which of the following statements is true regarding the time value of money?

A. Compound interest will produce equal amounts of interest each period on a fixed

deposit.

B. Earning simple interest is more beneficial than earning compound interest.

C. When making a purchase, it is better to make payment as soon as possible.

D. It is better to receive $1 now than a year from now.

Which of the following assets could be described as nonphysical?

A. Inventory

B. Cash

C. Trademarks

D. Supplies

The following lettered items represent a classification scheme for a balance sheet, and

the numbered items represent accounts. In the blank next to each account, write the

letter indicating to which category it belongs.

Par value is the minimum cushion of capital established for the protection of

A. investors (stockholders).

B. management.

C. creditors.

D. customers.

An adjusting entry would not include which of the following accounts?

A. Salaries Payable

B. Unearned Revenue

C. Interest Receivable

D. Cash

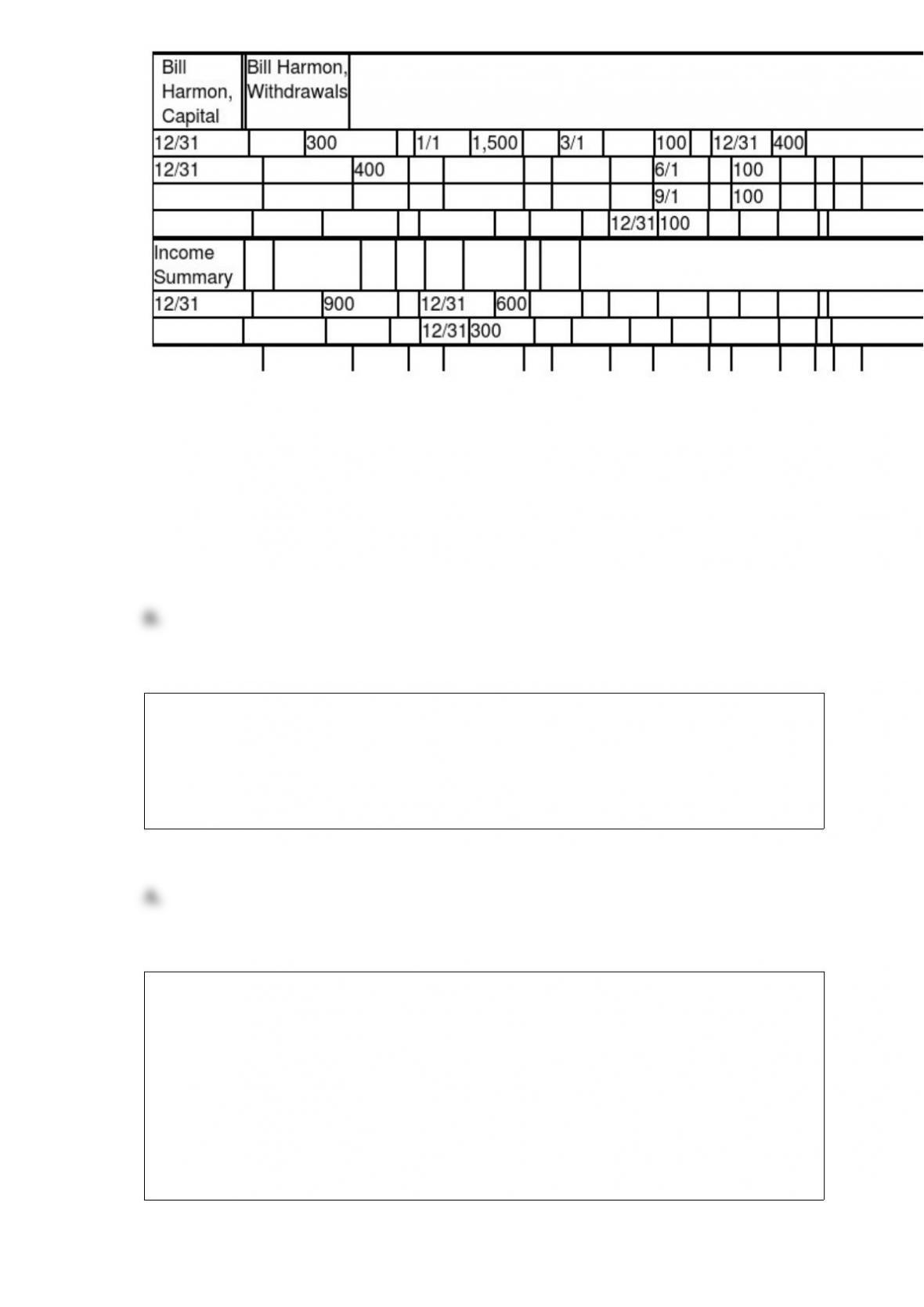

The owner’s Capital, Withdrawals, and Income Summary accounts for Harmon Repair

Company for the accounting period are presented below in T account form after the

recording and posting of closing entries:

The total amount of revenue earned for the period is

A. $300.

B. $600.

C. $700.

D. $900.

The Public Company Accounting Oversight Board was created by the

A. Sarbanes-Oxley Act.

B. GASB.

C. IRS.

D. IASB.

Mariposa Corporation had a Retained Earnings balance on January 1, 20×4, of

$936,000; declared cash dividends during 20×4 in the amount of $159,900, of which

$39,000 were not paid until 20×5; and reported an ending balance of Retained Earnings

of $1,326,000. Based on these facts alone, net income for 20×4 for Mariposa

Corporation must have been

A. $211,900.

B. $419,900.

C. $510,900.

D. $549,900.

Measures how efficiently assets are used to produce sales.

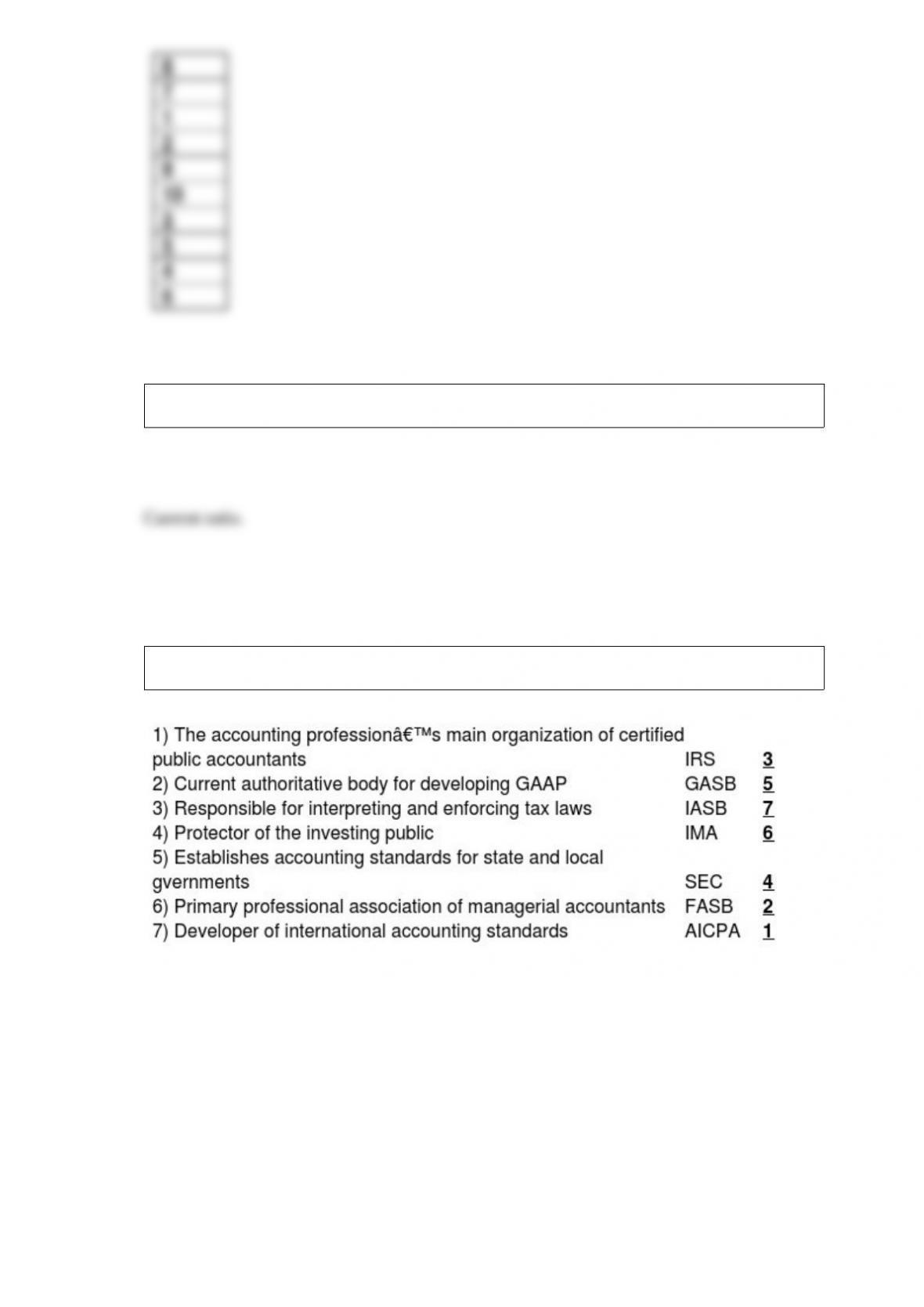

Indicate by letter the agency that applies to each statement.

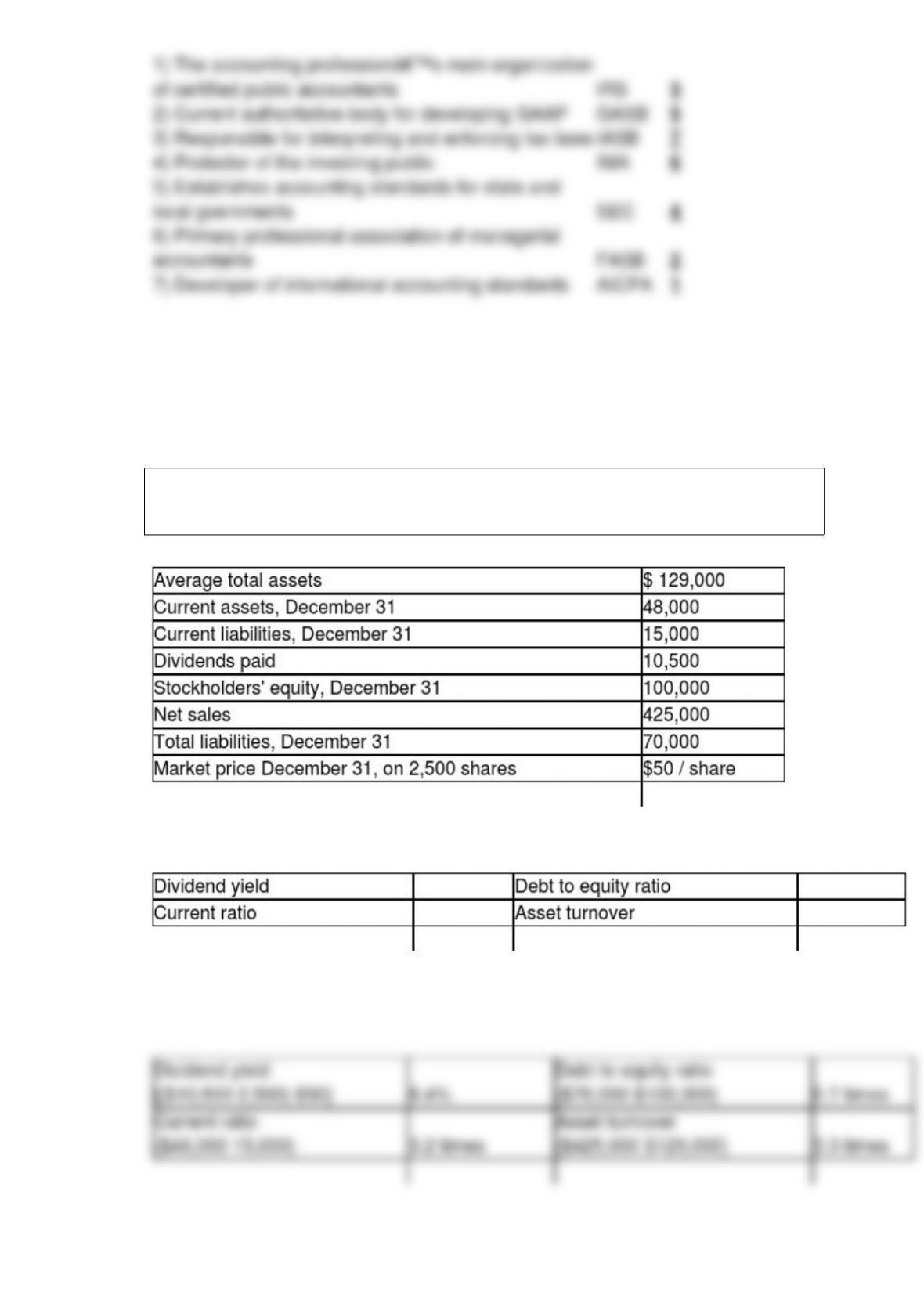

Use the following information to calculate the ratios requested below. Round answers to

two decimal places. Show your work.

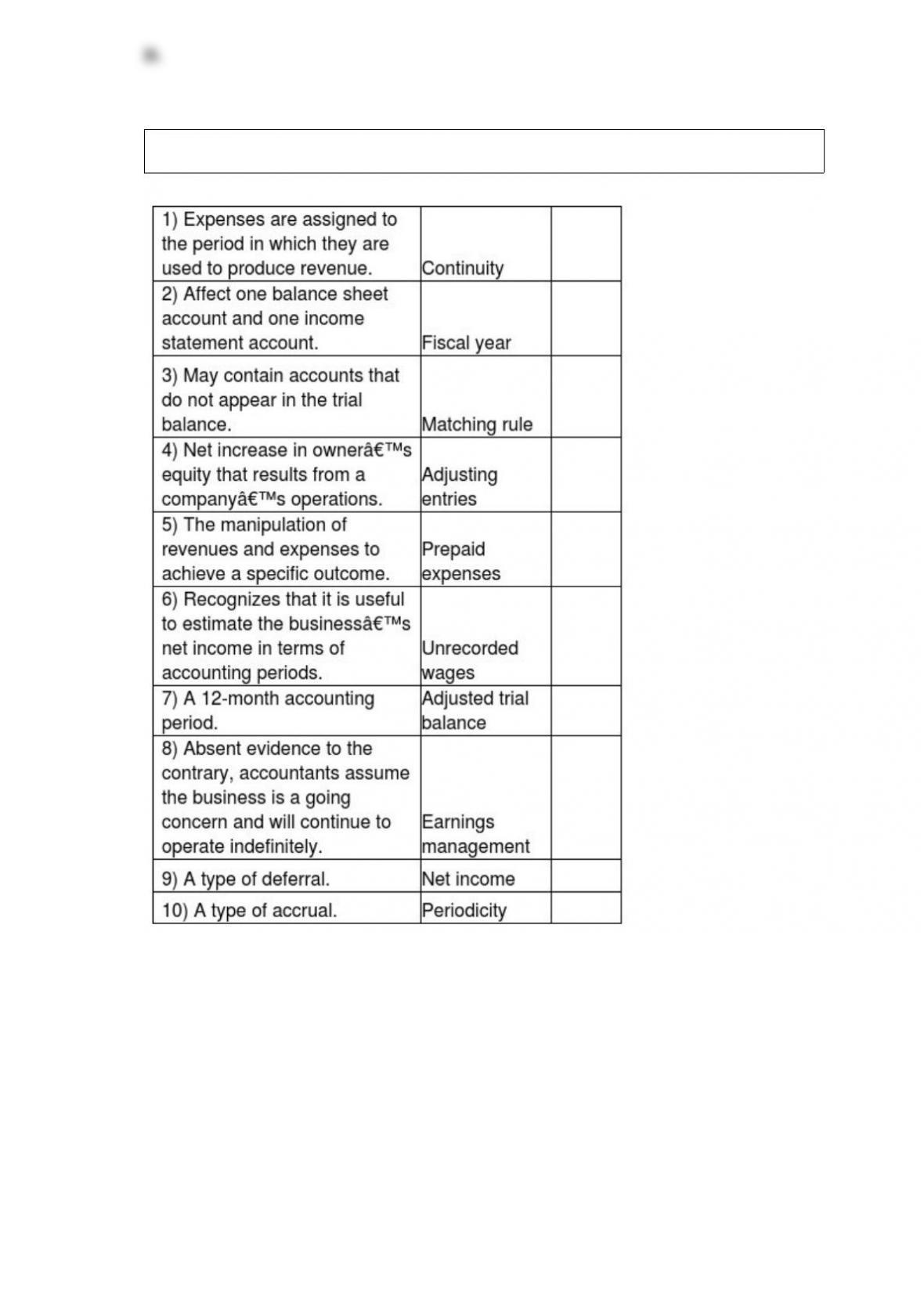

Match each description with the letter of the term to which it corresponds.

Under a perpetual inventory system, is it necessary to take a physical inventory at the

end of the period? Why or why not?

What is the chief objective of supply-chain management? How is it accomplished?

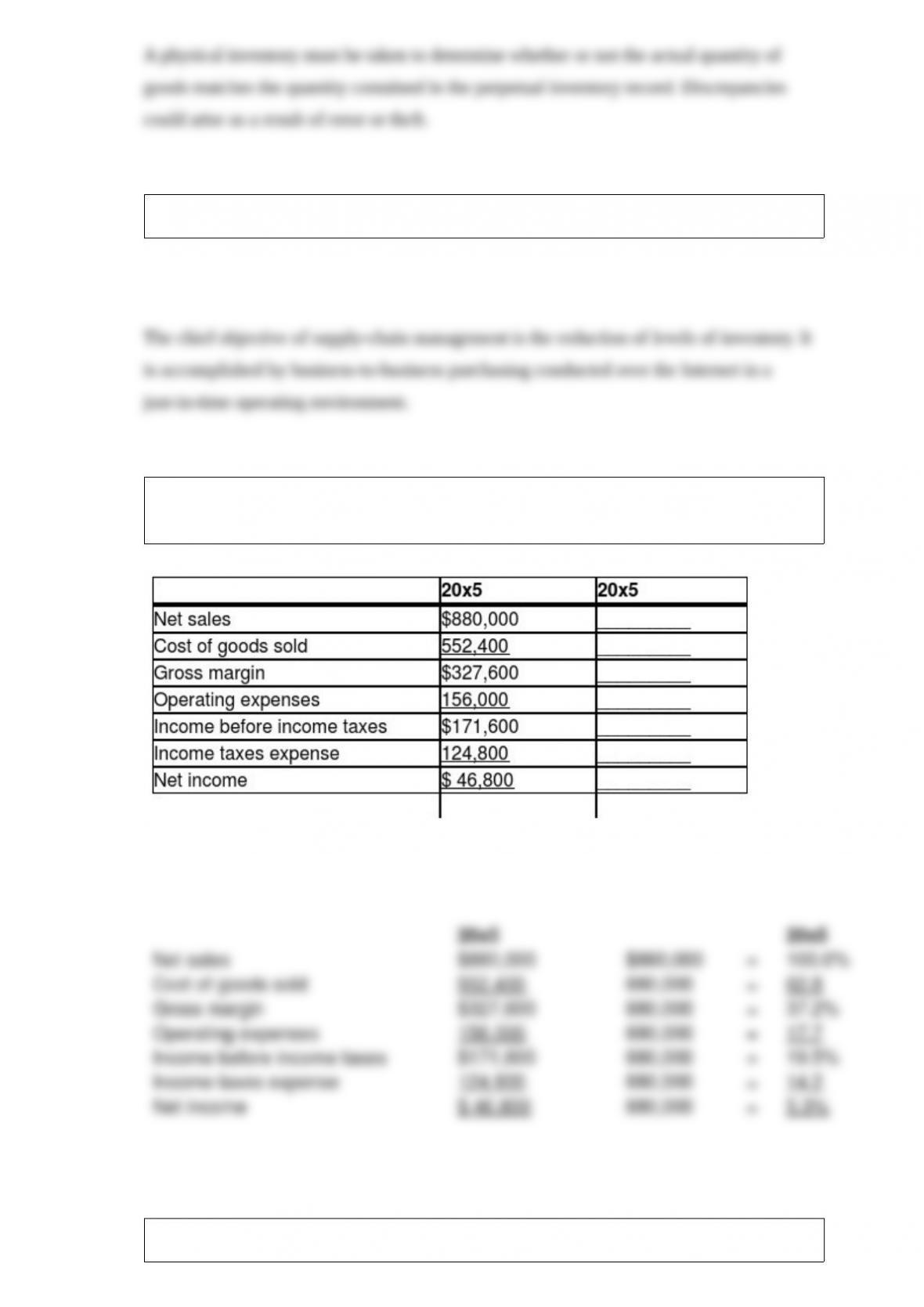

Using the income statement below, develop a common-size statement by filling in the

blanks provided. Show your work. Round to one decimal place.

When stock is issued for noncash assets or services, how does one place a valuation

(dollar amount) on the transaction?

One aspect of the corporate form can be considered both an advantage and a

disadvantage. What aspect is this, and why can it be considered both?

Assuming the use of the periodic inventory system, use the data below to calculate the

net cost of purchases and the cost of goods available for sale for the year ended

December 31, 20×5.

Kangjon Company allows each employee two weeks’ paid vacation after the employee

has worked at the company for one year (50 weeks work). On the basis of past

experience, management estimates that 80 percent of employees will qualify for

vacation pay this year. Assume that the March payroll is $400,000. Compute the

vacation pay expense for the month. Show your computation.

Briyanna and Greg form a partnership and invest the following assets and liabilities.

Parker Company has $1,000,000 worth of 7 percent convertible bonds outstanding. On

September 1, 20×5, there is $40,000 of unamortized discount associated with these

bonds. The bonds are convertible at the rate of 30 shares of $10 par value common

stock for each $1,000 bond. On September 1, 20×5, an interest payment date,

bondholders presented $700,000 of the bonds for conversion. Prepare an entry in

journal form without explanation to record the conversion of the bonds.

Describe how the current ratio is calculated. If a company has a very low current ratio,

what might this mean? If a company has a very high current ratio, what might this

mean?

You purchased Company B for $220,000 on January 1, 2014.

The following information relates to the number of common shares of the Swan

Corporation:

140,000 Authorized shares 60,000 Unissued shares 8,000 Treasury shares

Calculate the number of outstanding shares from the information given. Show your

calculations.

Doug Riley is the only accountant employed at Carmen Enterprises.