Quick ratio*

Days’ sales

uncollected*

Receivables

turnover*

Current ratio* $150,000

P4. Comprehensive Ratio Analysis of Two Companies

Ratio Name

1.

$192,400

6. Company

with More

Favorable Ratio

Single

Single

$80,000

22.7

+

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

timestimes

times

=

6. Company

with More

Favorable Ratio

Inventory

turnover* =

e.

times

f.

P4. Comprehensive Ratio Analysis of Two Companies (Continued)

g.

25.9 Design

Payables

turnover*

Days’

inventory

on hand*

365 days

= 30.9

37.2 days

i. Financing

period

h.

Days’

payable*

*Rounded

Design

times

365 days

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

6. Company

with More

Favorable Ratio

times

$4,987,200

1.7%

2. Profitability and

Design

= 1.2%

= Single

$4,987,200 4.3%

P4. Comprehensive Ratio Analysis of Two Companies (Continued)

Single

Design=

=

Single

16-33

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Single

P4. Comprehensive Ratio Analysis of Two Companies (Continued)

3.

6. Company

with More

Favorable Ratio

Design

+

time

Design

$2,112,000

$2,000,000

Design

–– ––

6. Company

with More

Favorable Ratio

times1.6

Design

Design

=

$215,400 1.3

4.

Cash flows to

sales*

$271,500 =

$271,500

$25,210,000

times

Single

5.3%

$492,500

=5.4% $9,326,600

$1,050,000$114,000

Free cash

flow ($403,500)

$50,000 Single

yield*

$271,500 =

P4. Comprehensive Ratio Analysis of Two Companies (Continued)

Ratio Name Single

($671,500)

Cash flows to

assets*

$625,000

Neutral

$4,987,200

=

16-35

//

7.

$114,000

Price/

earnings

(P/E) ratio*

Design

$76.00 =

Single

times

P4. Comprehensive Ratio Analysis of Two Companies (Concluded)

5.

Ratio Name Single

times

$60.00

$4.31

shares

$76.00

Design

==

5.0%= $3.80

=

$60.00

$60.00

7.5

30,000

$1.00

=

shares

Dividend

yield*

$50,000

1.7%

6. Company

with More

Favorable Ratio

16-36

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

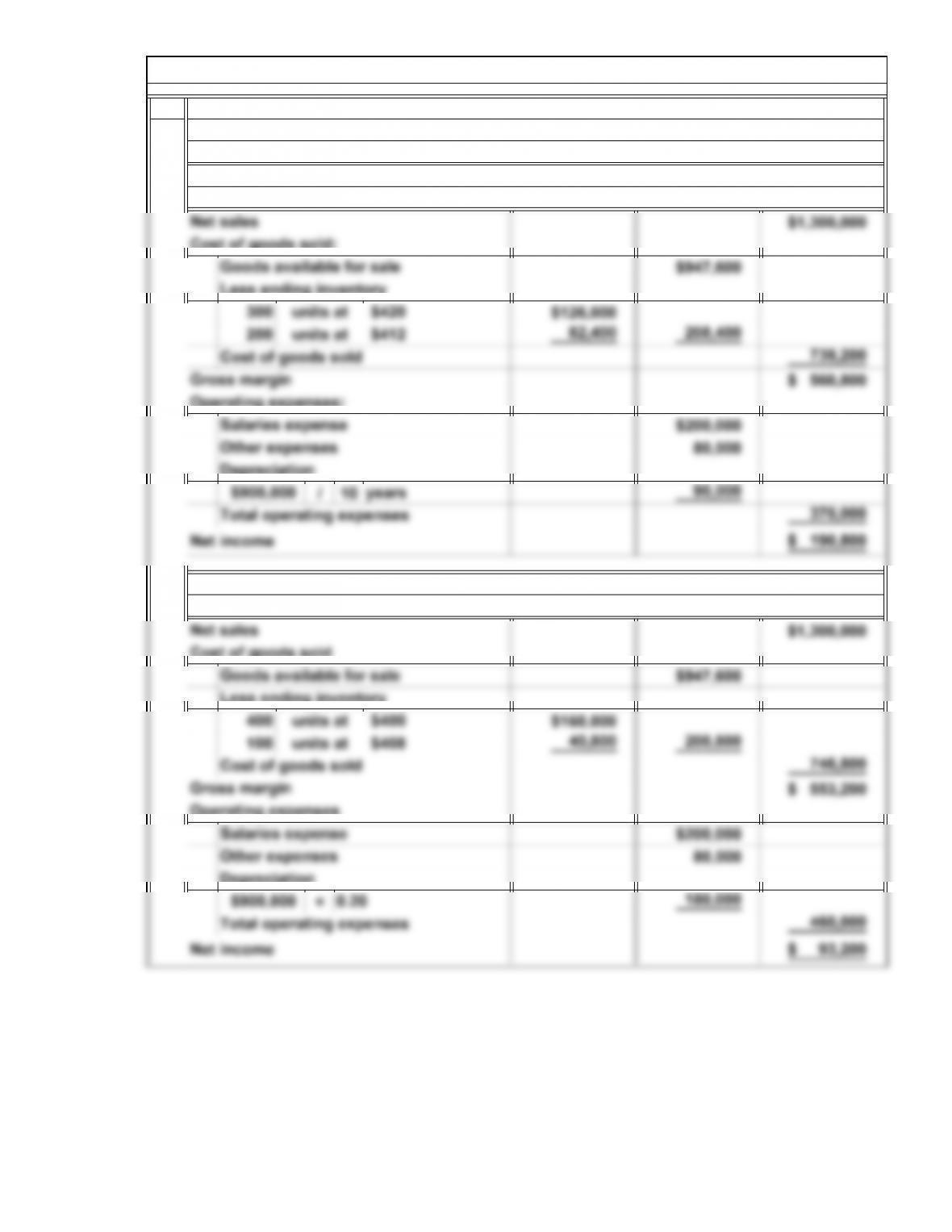

P5. Effect of Alternative Accounting Methods

For the Year Ended December 31, 2014

Furlong Corporation

Alternative Income Statements

Income Statement Using FIFO

and Straight-Line Methods

16-37

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2.

3.

$208,400 $200,800

FIFO Method

Inventory Turnover

LIFO Method

$ 90,000

180,000 90,000

$ 97,600

$ 7,600

746,800

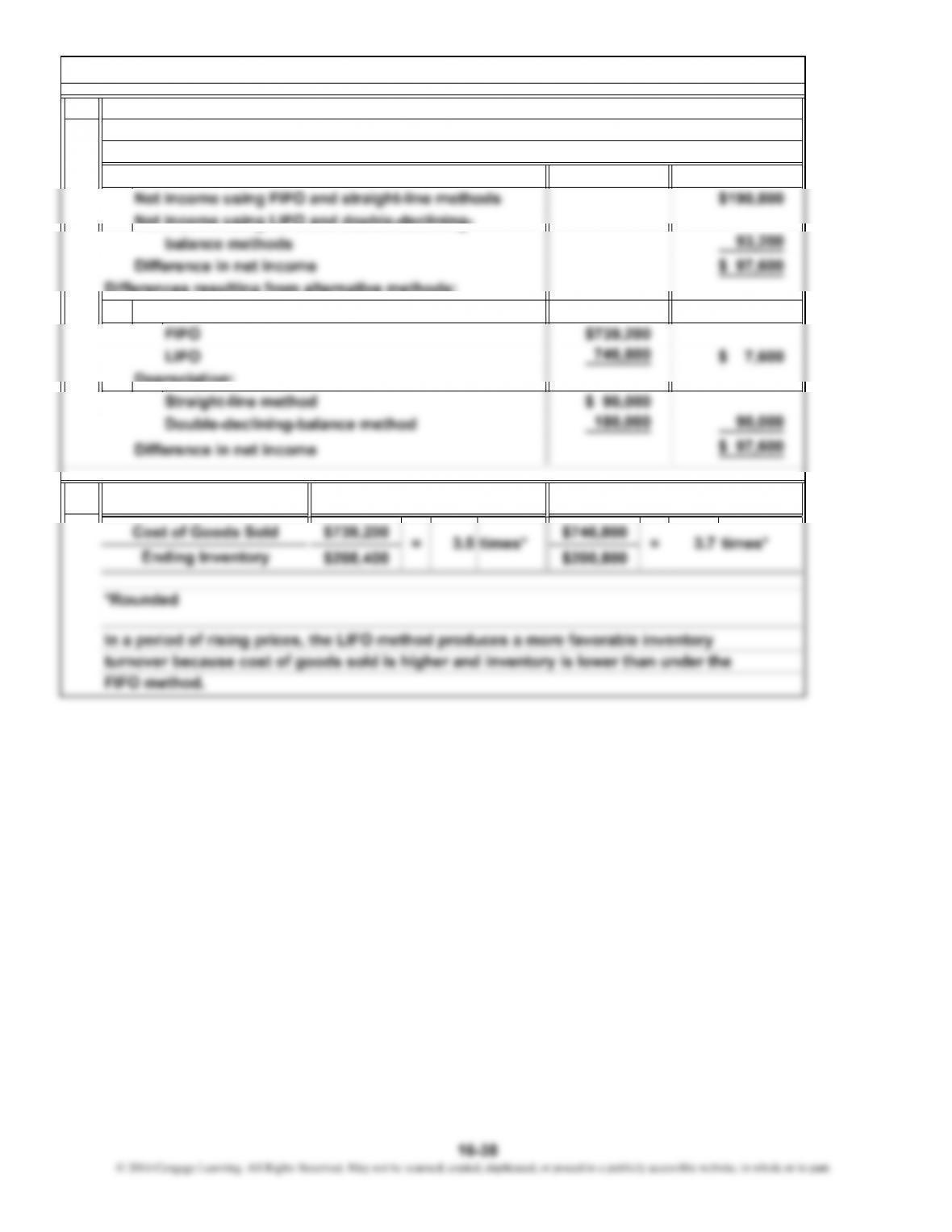

P5. Effect of Alternative Accounting Methods (Continued)

*Rounded

Ending Inventory

Depreciation:

Straight-line method

Double-declining-balance method

Difference in net income

Schedule of Differences in Net Income

For the Year Ended December 31, 2014

LIFO

Furlong Corporation

Difference in net income:

Net income using LIFO and double-declining-

Differences resulting from alternative methods:

Cost of goods sold:

16-38

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

4.

$190,800

$80,000 + $200,800 + $900,000 – $180,000

$93,200

$1,000,800

FIFO/Straight-Line Methods

would be more willing to accept a lower return on assets in the LIFO/double-declining-

balance case.

Return on Assets

sold and depreciation costs against revenues in earlier years. Therefore, analysts

$93,200

Net Income =

=

The LIFO and double-declining-balance methods produce a lower return on assets.

This combination of accounting methods produces a more conservative net income

figure than the FIFO/straight-line methods because it charges higher cost of goods

$190,800

P5. Effect of Alternative Accounting Methods (Concluded)

*Rounded

= = 9.3%

LIFO/Double-Declining-Balance Methods

*

16-39

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

P6. Corporate Income Statement

Income Statement

For the Year Ended December 31, 2014

Krall Corporation

16-40

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.