DQ1.

DQ2.

DQ3.

DQ4.

DQ9.

DQ10.

are full values similar to those at year end. Thus, any ratios that use data from the

income statement or statement of cash flows as their basis will be less than they

increase in receivables.

On quarterly financial statements, all numbers on the income statement and state-

CHAPTER 16—Solutions

analysis will be different each year.

A limitation of using past performance as a benchmark is that it may not be a good

Discussion Questions

In a five-year trend analysis for a new five-year period, the base year changes.

A company’s past performance indicates whether performance is improving, but

may not be strictly comparable with other companies in the industry.

industry norms tell how well a company is performing in relation to its peer group.

measure of present needs. A limitation of using industry norms is that the company

If the overall financial plan is expected to increase the owners’ wealth, then linking

Unless two successive base years have exactly the same dollar values, the trend

own and the owners’ best interests.

Many companies attempt to improve their earnings per share by reducing the num-

ber of shares outstanding through buybacks of their own stock.

managers’ compensation to financial targets encourages managers to act in their

receivable to finance. Consequently, the company needs more cash to cover the

When receivable turnover decreases, it means that the company has more days’

FINANCIAL STATEMENT ANALYSIS

16-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. c 4.

2. b 5.

3. a 6.

1. c 4.

2. a 5.

3. d

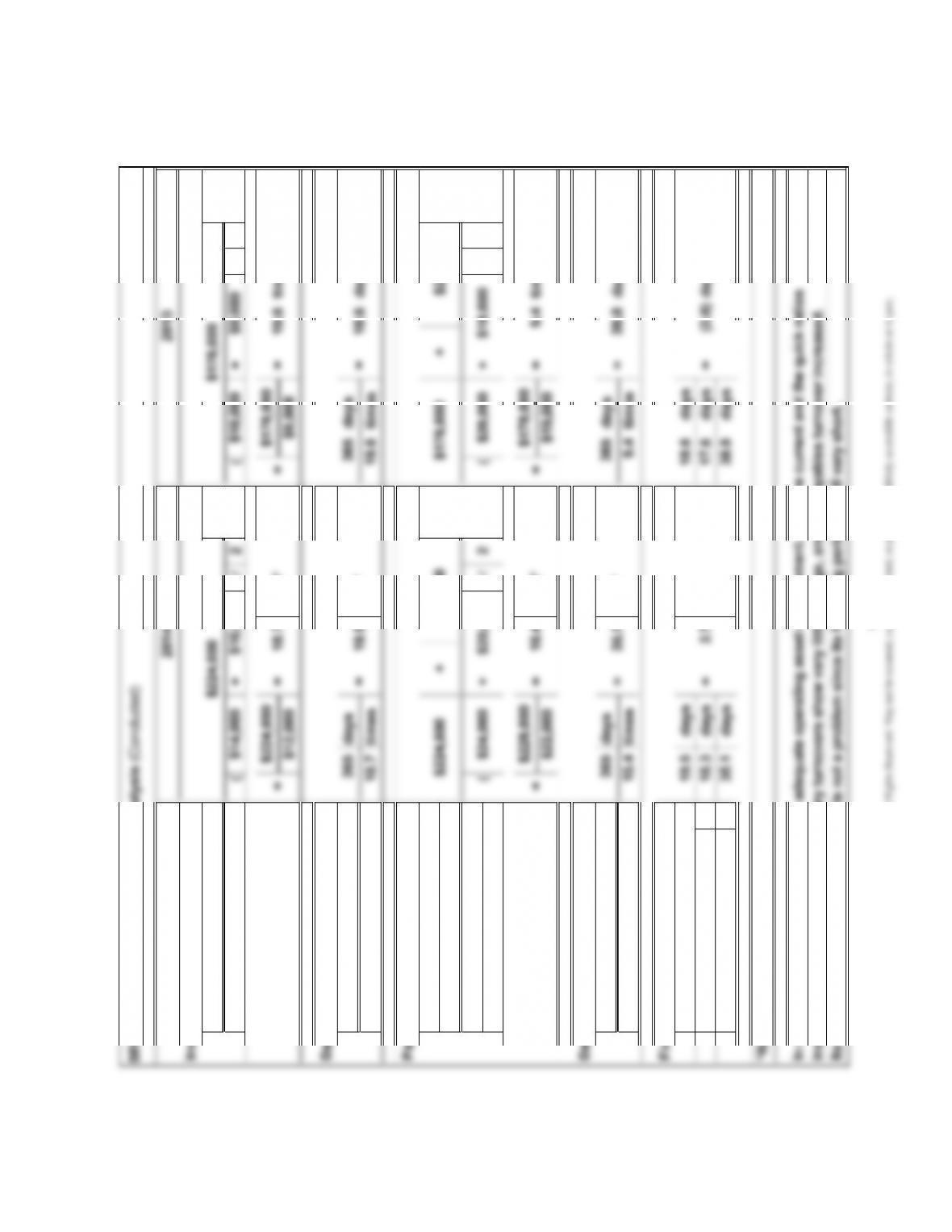

2014 2013 2012

SE3. Trend Analysis

SE1. Objectives and Standards of Financial Performance Evaluation

b

SE2. Sources of Information

b

a

c

c

16-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2014 2013 Amount Percentage

2014 2013

Common-Size Balance Sheets

December 31, 2014 and 2013

Comparative Income Statements

For the Years Ended December 31, 2014 and 2013

Vision, Inc.

SE5. Vertical Analysis

SE4. Horizontal Analysis

Vision, Inc.

Increase or Decrease

19.3 percent. Also, although sales and gross margin have increased by a large percen-

tage, operating income is up only 3.7 percent because of the 33.3 percent increase in

operating expenses. Income before income taxes has decreased as a result of the 40.0

percent increase in interest expense. That increase, however, was offset by a decrease

(27.3 percent versus 24.1 percent). As a result, the increase in gross margin is limited to

Assets

The percentage increase in cost of goods sold was greater than the increase in net sales

16-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

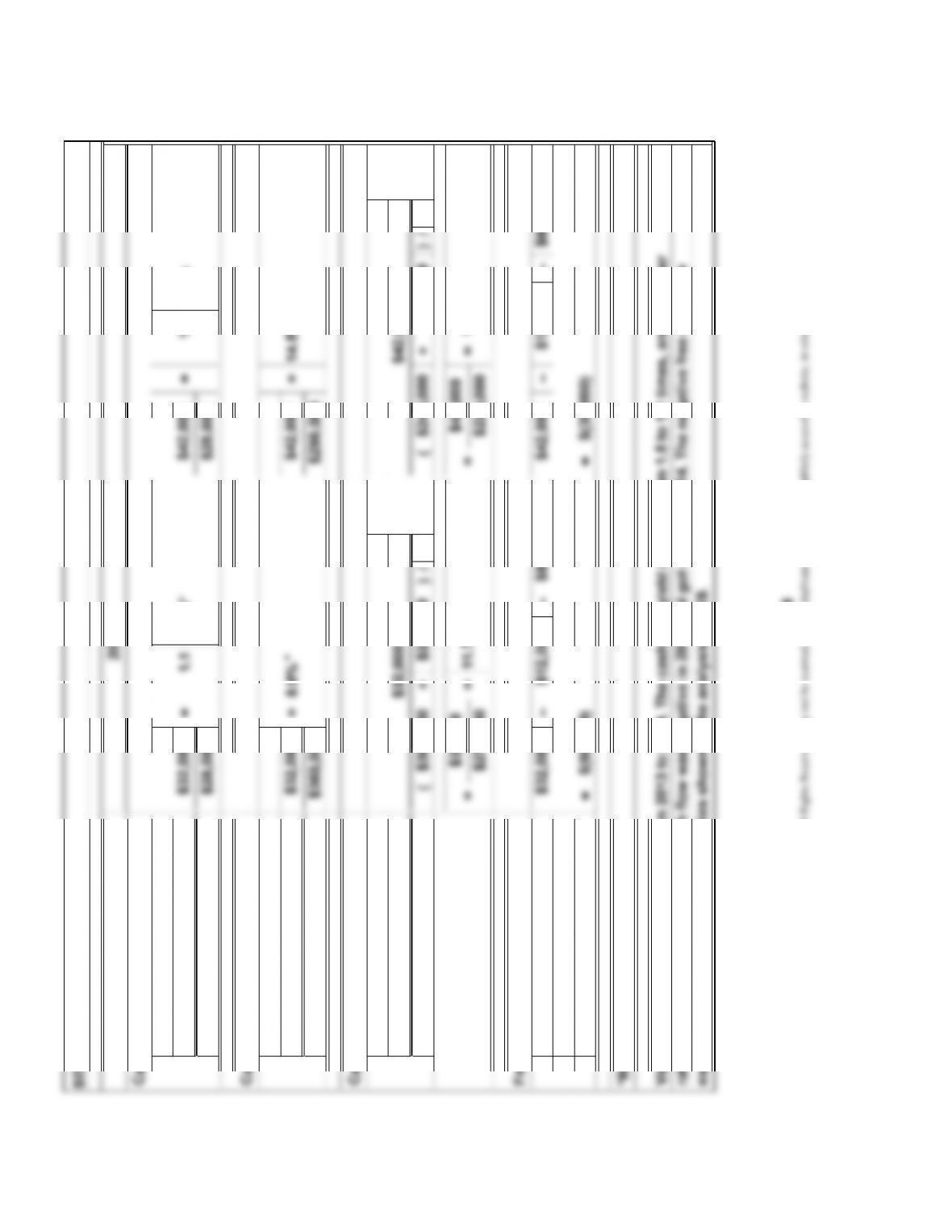

Current Assets

Current Liabilities

Cash + Marketable

Securities + Receivables + + + +

Current Liabilities

** – – *** – –

Net Sales

Average Accounts ( + ) / 2 ( + ) / 2

Receivable

Days in Year

Receivable Turnover

Current ratio:

=

SE6. Operating Asset Management Analysis

$36,000

Days’ sales uncollected:

days

Quick ratio:

365

$360,000 ==

$360,000

*Rounded

Receivables turnover:

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Days’ sales uncollected +

Days’ payable –

Days in Year

Inventory Turnover

Accounts Payable

Average

Days’ inventory on hand

Days in Year

Payables Turnover

=

Cost of Goods Sold

Average Inventory

=

times*19.6=

times*

Change in Inventories

Cost of Goods Sold +/‒

daysdays

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Total Liabilities + +

Stockholders’ Equity

Net Income

Average Stockholders’ Equity ( + ) / 2 ( + ) / 2

Income Before Income

Taxes + Interest Expense + +

Interest Expense

$14,000 timestimes

5.4

times*

$216,000

$92,000

$84,000

$92,000 $76,000 $76,000

41.2%

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Net Cash Flows from

Operating Activities

Net Income

Net Cash Flows from

Operating Activities

Net Sales

Net Cash Flows from

Operating Activities

Average Total Assets ( + ) / 2 ( + ) / 2

Net Cash Flows from Operating – – – –

Activities ‒ Dividends ‒ Net

Capital Expenditures = =

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

/=

=

$2.80 == 14.3

SE10. Market Strength Analysis

Earnings per Share 21.4

=

Price/earnings (P/E) ratio:

Dividend yield:

2013

2014

*Rounded

Investor confidence in Vision has declined, as reflected by the decline in the price/earnings (P/E) ratio. This may

reflect investor awareness of Vision’s deteriorating profitability and cash flow situation and its increasingly heavy

debt load. The dividend yield increased as a result of the drop in the market value of the stock.

$1.20 per share10,000 shares

16-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2.

5.

SE11. Quality of Earnings

Income Statement

For the Year Ended June 30, 2014

c

c

SE12. Corporate Income Statement

Karib Corporation

16-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.