2014

Dec. 31 12,810

31 7,915

31 4,895

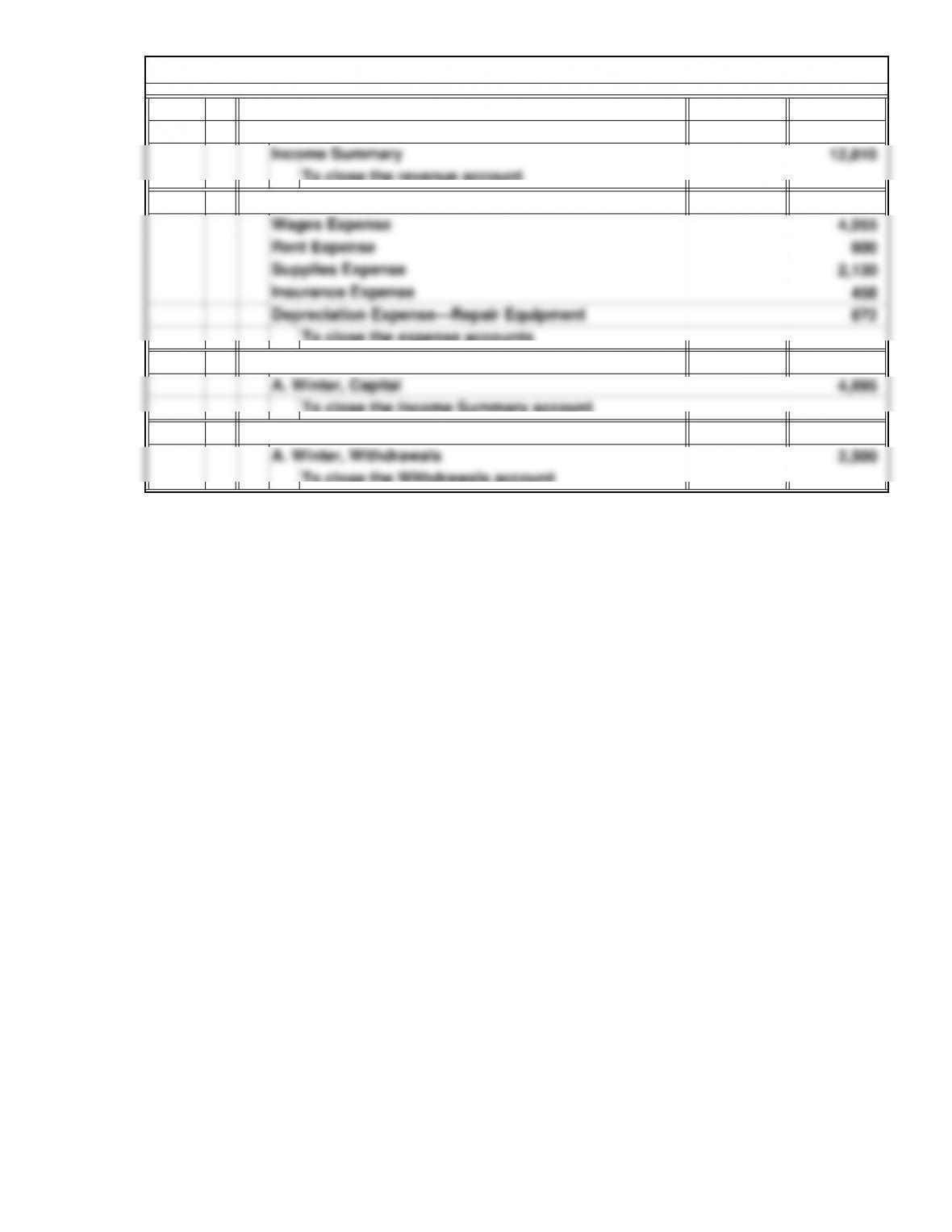

31 2,500

To close the expense accounts

Income Summary

To close the Income Summary account

To close the Withdrawals account

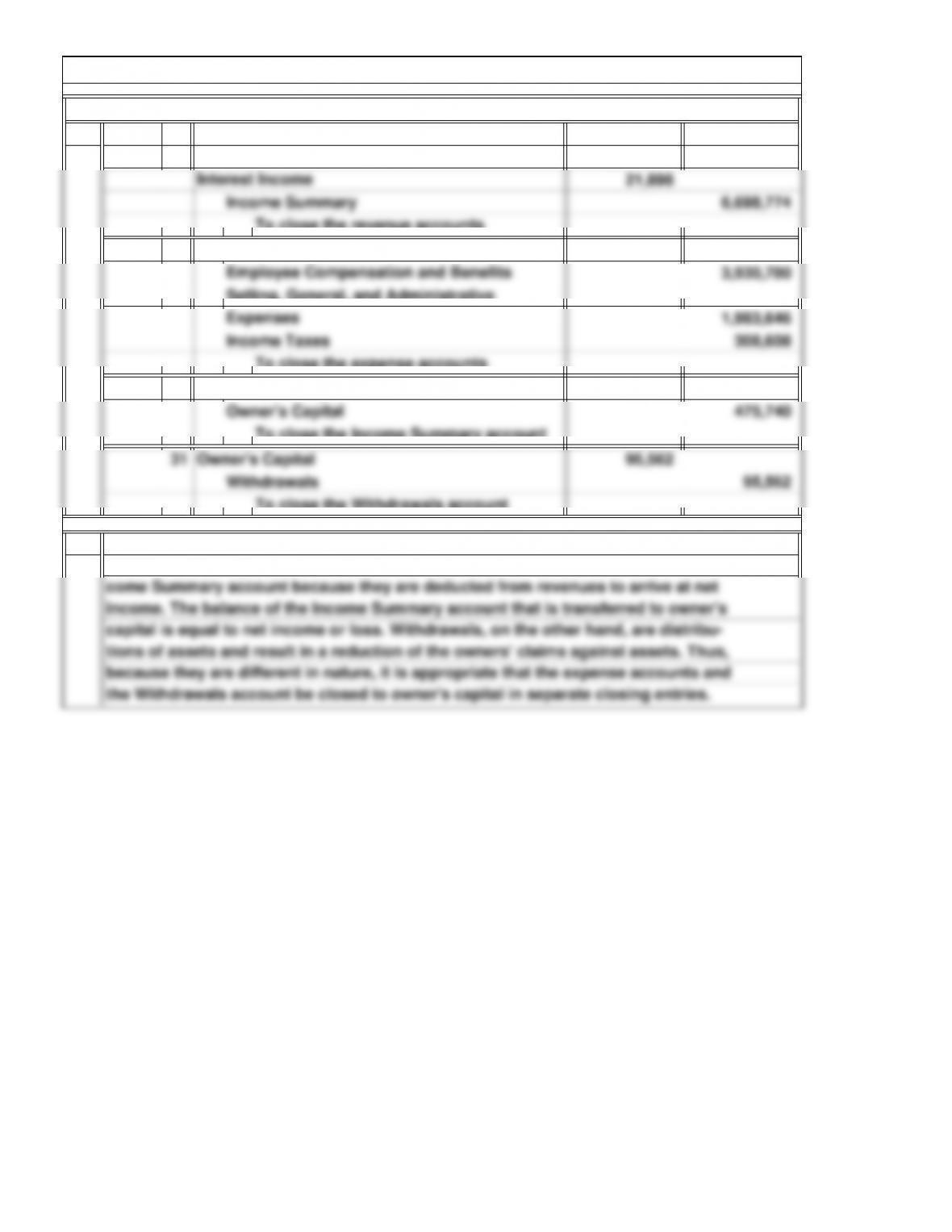

A. Winter, Capital

E7A. Preparation of Closing Entries from the Work Sheet

To close the revenue account

Income Summary

Repair Revenue

4-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

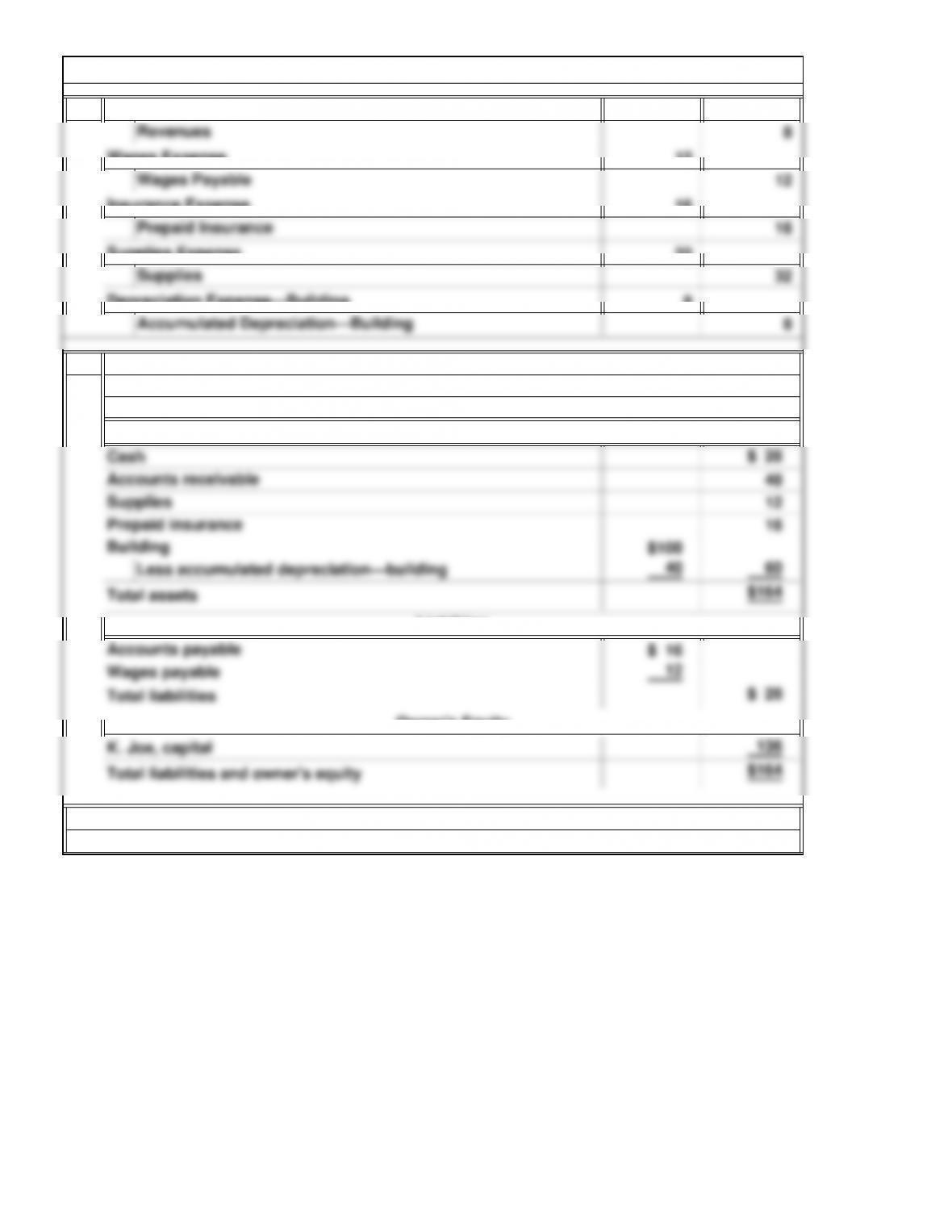

1. 8

12

16

32

8

2.

Note to Instructor: Solutions for Exercises: Set B are provided separately on the Instructor’s

K. Joe Company

Balance Sheet

Assets

December 31, 2014

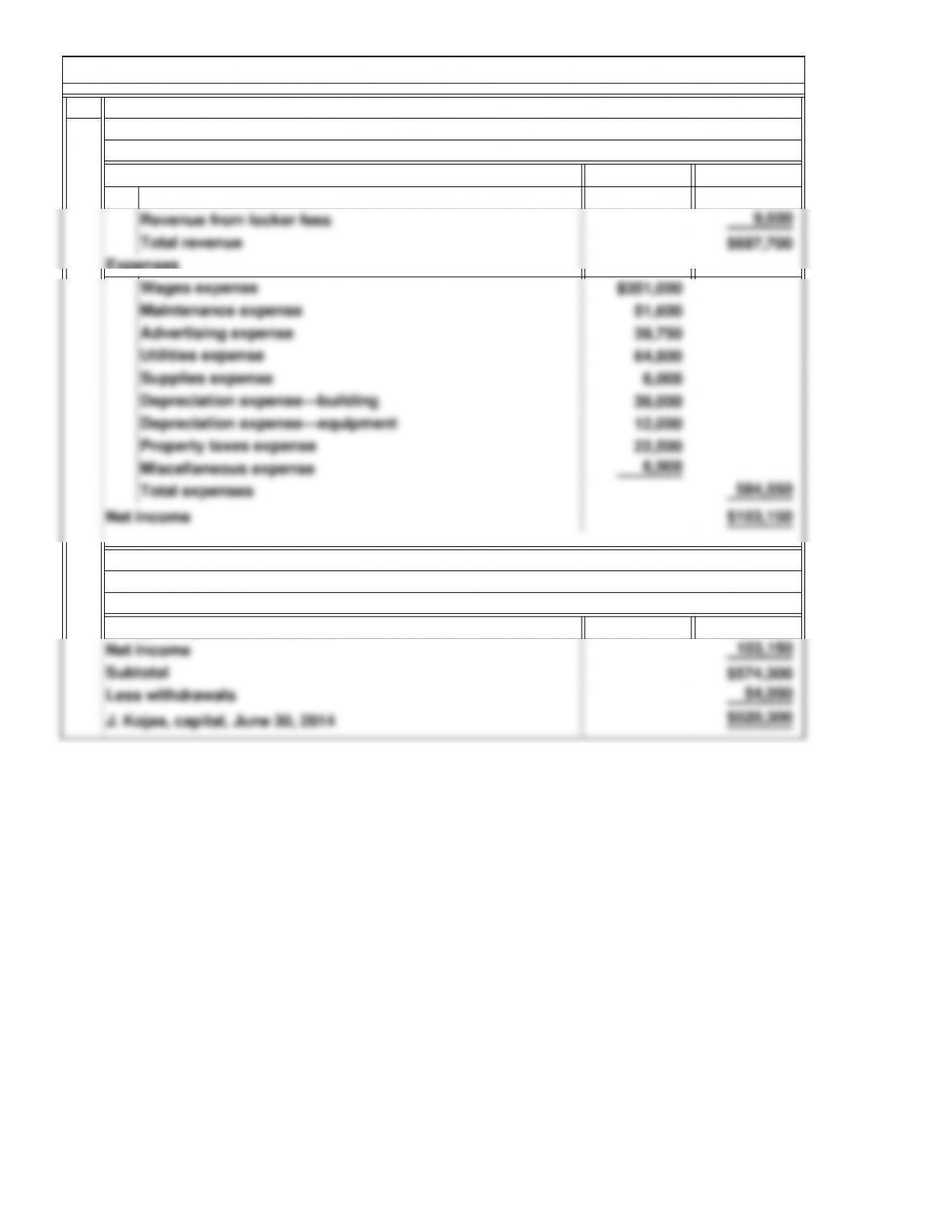

Wages Expense

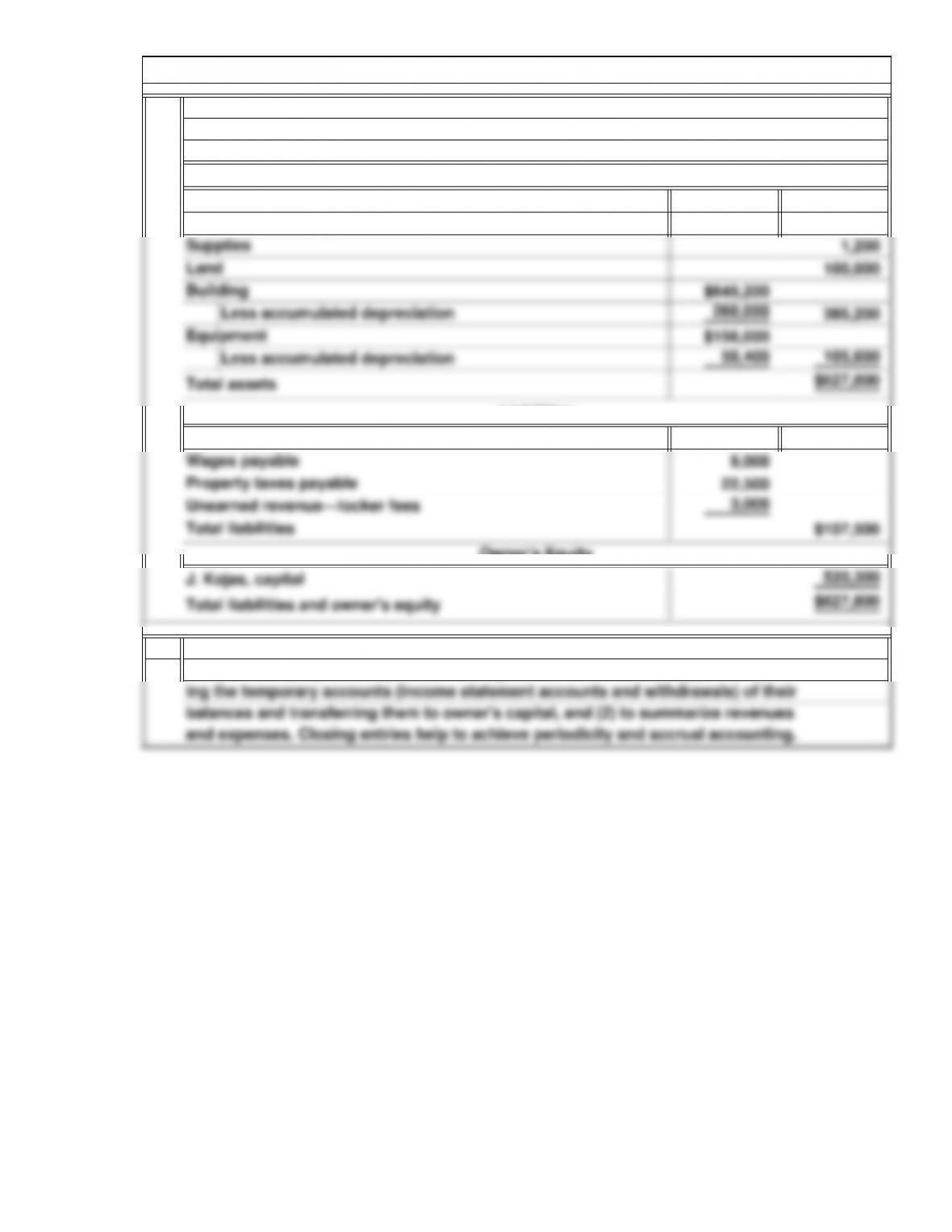

Unearned Revenues

Depreciation Expense—Building

Supplies Expense

E8A. Adjusting Entries and Preparation of a Balance Sheet

Insurance Expense

Resource CD and website.

4-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 2014

June 30 91,092

30 75,136

30 15,956

30 14,400

2.

Trailer Rentals Revenue

Income Summary

D. Anatole, Capital

P1. Preparation of Closing Entries

To close the Withdrawals account

To close the expense accounts

To close the Income Summary account

Income Summary

If closing entries were not made at the end of the accounting period, two serious

Problems

To close the revenue account

problems would arise. First, the income statement accounts and the Withdrawals

4-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

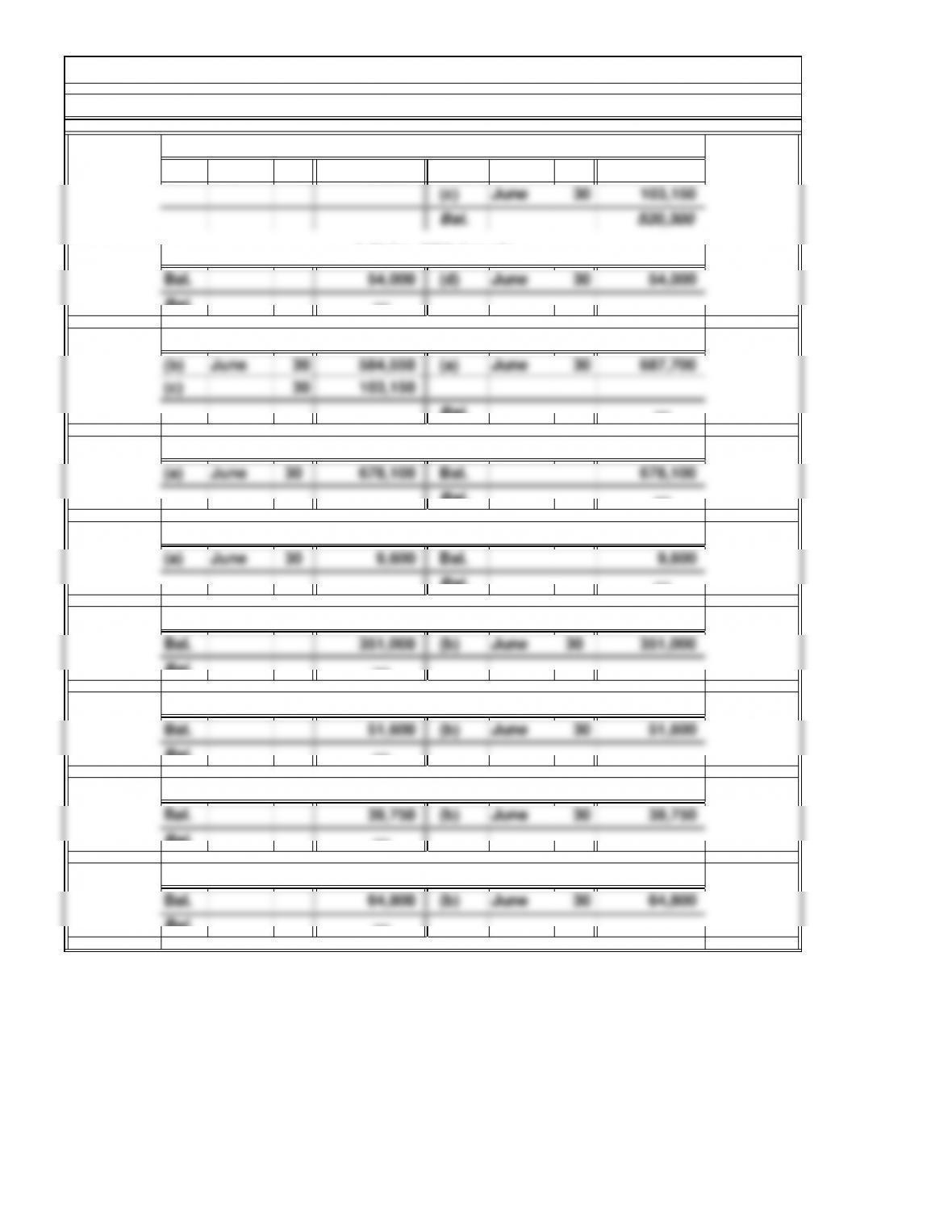

(d) June 30 54,000 Bal. 471,150

Bal. —

Bal. —

Bal. —

Bal. —

Bal. —

Bal. —

Bal. —

Bal. —

P2. Closing Entries Using T Accounts and Preparation of Financial Statements

Maintenance Expense

Wages Expense

Revenue from Court Fees

J. Kojas, Capital

Income Summary

Revenue from Locker Fees

1. and 2.

Advertising Expense

Utilities Expense

4-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Bal. —

Bal. —

Bal. —

Bal. —

Bal. —

Miscellaneous Expense

Depreciation Expense—Building

Property Taxes Expense

Depreciation Expense—Equipment

Supplies Expense

P2. Closing Entries Using T Accounts and Preparation of Financial Statements (Continued)

4-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

$678,100

$471,150

Carlton Tennis Club

For the Year Ended June 30, 2014

Revenue from court fees

Carlton Tennis Club

Statement of Owner’s Equity

Revenue

For the Year Ended June 30, 2014

Income Statement

P2. Closing Entries Using T Accounts and Preparation of Financial Statements (Continued)

J. Kojas, capital, June 30, 2013

4-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$ 26,200

9,600

$ 73,000

4.

June 30, 2014

Liabilities

Carlton Tennis Club

Balance Sheet

Assets

Accounts payable

Closing entries are journal entries made at the end of the accounting period to ac-

complish two purposes: (1) to set the stage for the next accounting period by clear-

P2. Closing Entries Using T Accounts and Preparation of Financial Statements (Concluded)

Cash

Prepaid advertising

4-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 2014

Dec. 31 Service Revenues 6,676,878

To close the revenue accounts

31 Income Summary 6,223,034

Selling, General, and Administrative

To close the expense accounts

31 Income Summary 475,740

To close the Income Summary account

To close the Withdrawals account

2.

P3. Preparation of Closing Entries

(numbers are in thousands)

Both expenses and cash distributions to owners reduce owner’s capital, but for dif-

ferent reasons. Expenses—the costs of doing business—are summarized in the In-

capital is equal to net income or loss. Withdrawals, on the other hand, are distribu-

income. The balance of the Income Summary account that is transferred to owner’s

4-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.