The statement of owner’s equity relates the income statement to the balance sheet by

showing how the owner’s capital account changed during the accounting period.

The Retained Earnings portion of a corporation represents the initial contribution of

capital to the business.

Corporations represent the largest number of businesses in the United States.

Ending merchandise inventory is not included in the calculation of cost of goods

available for sale.

In calculating the depletion of a natural resource, its useful life in years is irrelevant.

Both profit margin and asset turnover affect a company’s return on assets.

Unrealized gains and losses on trading securities appear on the income statement.

When the date of declaration and the payment date occur in the same period, the

amount of dividends shown on the statement of stockholders’ equity and on the

statement of cash flows will be equal.

The materiality concept dictates that no internal controls be established over petty cash.

Taking a physical inventory refers to making a count of all merchandise on hand at a

particular time.

The use of the lower-of-cost-or-market method for inventory is an application of the

convention of conservatism.

Journal entries are typically posted to the ledger only at the end of the year.

A partnership is an accounting entity separate and apart from its owners.

In the financial statements, the balance of the Petty Cash account and the balance of the

Cash account are shown separately.

The term owner’s equity is preferred over the term net worth because most assets are

carried at original cost rather than at current value.

In the general journal, the year appears on the first line of the first column, the month

on the next line of the first column, and the day in the second column opposite the

month.

When a new partner is admitted, the old partnership agreement is still in effect.

A partnership is dissolved when any partner leaves the business or dies.

Terms of “n/10 eom” mean that payment is due 10 days after the end of the month.

Bond issue costs have the effect of increasing a premium, or reducing a discount, on

bonds issued.

Payables turnover measures the relative size of accounts payable.

When individuals invest property in a partnership, the property becomes an asset of the

partnership and is owned jointly by the partners.

The replacement of tires on a truck is considered an ordinary repair.

Business transactions are economic events that should be recorded in the accounting

records.

When a company uses an accounts receivable subsidiary ledger, it cannot also maintain

an Accounts Receivable account in the general ledger.

Revenue should be recognized, even when collectibility is not reasonably assured.

Revenue is produced when accounts receivable are collected.

When the buyer bears the transportation charge, it is called freight-out.

A company would be more likely to know the amount of inventory on hand if it used

the periodic inventory system rather than the perpetual inventory system.

Supplies Expense is a temporary account.

The proposed purchase price of an asset should be compared to the present value of the

benefits it will generate over its useful life.

When a bond has been issued at a discount, the carrying value at the end of one period

is equal to the carrying value at the beginning of the period minus the amount of

discount that was amortized during the period.

If a bond with a face value of $1,000 and a face interest rate of 7 percent is issued for

$970, the market interest rate at the date of issuance must have been less than 7 percent.

Working capital is the amount by which current liabilities exceed current assets and

measures how efficiently liabilities are used to produce sales.

The exclusive right to use an identifying symbol is called a patent.

If the amount of a liability cannot be exactly determined, it should not be recorded.

If a company has suffered only net losses since its inception, the owner’s equity account

will always have a negative balance.

Promises to pay employees pensions after they retire are difficult to identify and value

and therefore need not be recognized in the financial statements until cash payment is

made.

Improvements to real estate are never subject to depreciation.

After all closing entries have been posted, which of the following accounts is most

likely to have a nonzero balance?

A. Interest Expense

B. Unearned Revenue

C. Service Revenue

D. Income Summary

Mike Nickell obtained a ten-year sublease on a busy corner to open a used car business.

To obtain the sublease, he had to pay $7,000 to the current tenant, who had 12 years to

go on his lease. The annual cost of the lease is $9,000. In addition to paying for the

sublease, Mike paid $5,000 to pave the lot. The paving will have no residual value after

its useful life of ten years. Prepare entries in journal form to record the following (omit

explanations):

a. The payment for the sublease

b. The payment for the paving

c. The lease payment for the first year

d. The expense, if any, associated with the sublease for the first year

e. The expense, if any, associated with the paving, using the straight-line method for the

first year

Which of the following is correct regarding the present value calculations associated

with bonds?

A. The amount of interest a bond pays is fixed over its life.

B. The market interest rate varies from day to day and is the rate used to determine the

bond’s present value.

C. The amount investors are willing to pay for a bond varies because the bond’s present

value changes as the market interest rate changes.

D. All of these choices.

Which of the following describes a limited liability company?

A. Entities with limited lives that a company creates to achieve a specific objective.

B. An association of two or more entities for the purpose of achieving a specific goal.

C. Corporations that U.S. tax laws treat as partnerships, and they do not pay income

taxes.

D. A special type of partnership that confines the limited partner’s potential loss to the

amount of his or her investment.

On January 1, 2014, Huan Manufacturing Company purchased for $94,000 a machine

that will produce an estimated 75,000 units of Product X. The machine has an estimated

useful life of five years and an estimated residual value of $4,000. Calculate the

following amounts: (a) the carrying value of the machine after it has been used for three

and one-half years, under the straight-line method; (b) depreciation expense for 2015,

under the production method (assume that 13,000 units were produced that year); and

(c) accumulated depreciation at the end of 2015, under the double-declining-balance

method. (Show your work.)

a. $31,000 [($94,000 – $4,000) 5 = $18,000; $18,000 3.5 = $63,000; $94,000 –

$63,000]

b. $15,600 [($94,000 – $4,000) 75,000 = $1.20; $1.20 13,000]

c. $60,160 ($94,000 40% = $37,600; $94,000 – $37,600 = $56,400; $56,400 40% =

$22,560; $22,560 + $37,600 = $60,160)

Which of the following costs normally is expensed in the year incurred, regardless of

the extent of future benefit?

A. Technology

B. Customer lists

C. Research and development

D. Leasehold improvements

Which of the following situations severely limits the use of industry norms as standards

of comparison?

A. The fact that little information exists on industry norms

B. The existence of conglomerates

C. The presentation of segmented information

D. A downward turn in the economy

Garcia Corporation purchased 22,000 shares of Lee Corporation common stock for $80

per share on January 1, 2014. Lee reported net income of $140,000 for 2014 and paid

dividends of $90,000 during 2014. As of December 31, 2014, the market value of Lee

Corporation common stock was $78 per share. Assuming the shares owned by Orlov

represent 10 percent of the total outstanding stock of Lee, the year-end adjustment entry

in Garcia Corporation’s books is:

A. Cash 44,000

Dividend Income 44,000

B. Cash 44,000

Long-Term Investments 44,000

C. Unrealized Loss on Long-Term Investments 44,000

Allowance to Adjust Long-Term Investments to Market 44,000

D. Loss on Long-Term Investments 44,000

The post-closing trial balance contains

A. neither real accounts nor nominal accounts.

B. nominal accounts only.

C. real accounts only.

D. both real accounts and nominal accounts.

Which of the following is not one of the conditions for recognition of an expense?

A. A price has been established or can be determined.

B. There is an agreement to purchase goods or services.

C. The goods will be delivered or the services will be provided within the accounting

cycle.

D. The goods or services are used to produce revenue.

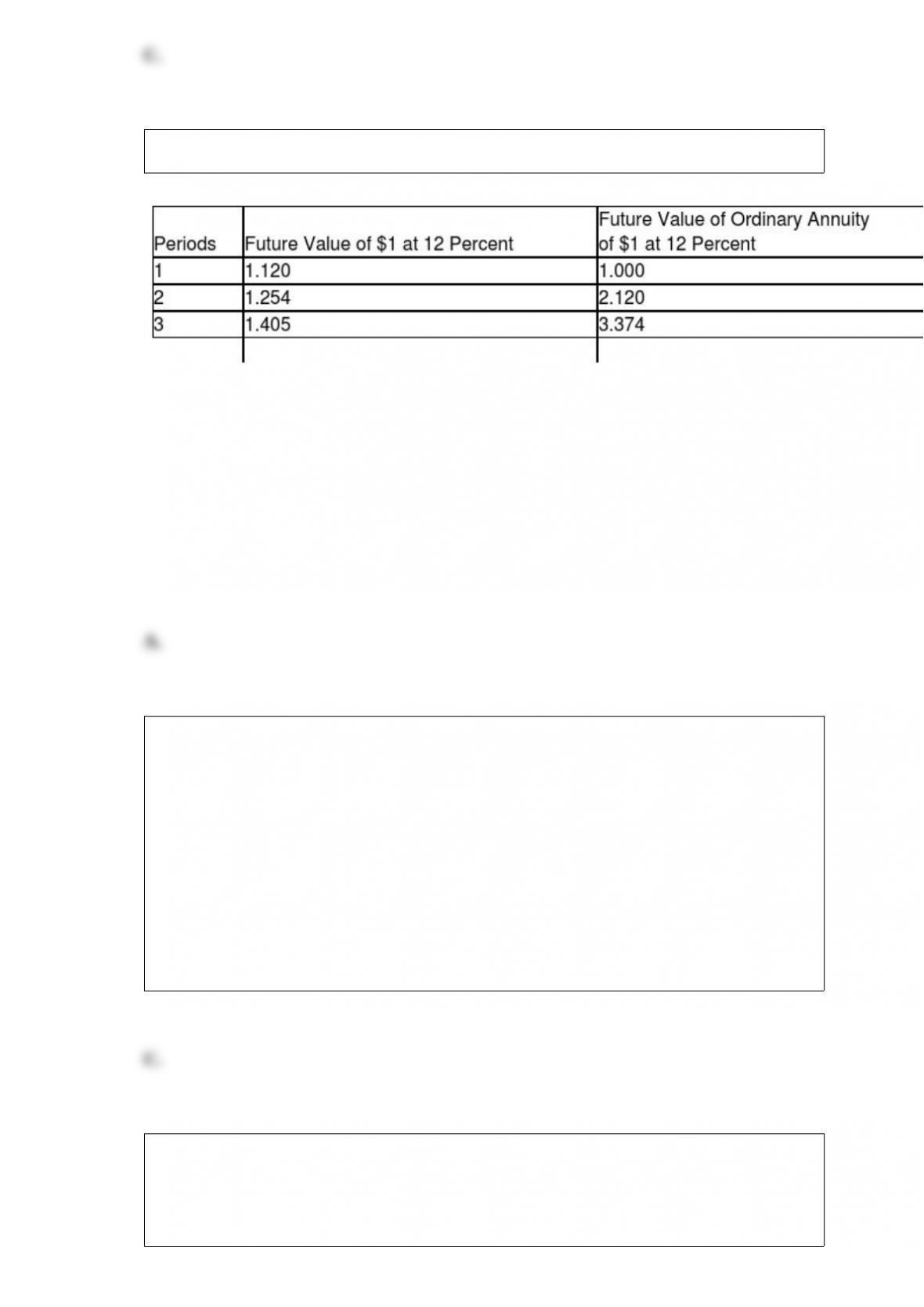

Use this information to answer the following question.

If an accumulation of $16,000 is desired at the end of three years, what amount must be

deposited at the end of each of the three years, assuming an APR of 12 percent?

A. $4,742.15

B. $53,984.00

C. $11,387.90

D. $22,480.00

On July 1, 20×5, Blaylock Corporation had 40,000 shares of its $100 par value common

stock outstanding. On July 2, 20×5, Blaylock declared a 15 percent stock dividend to be

distributed on August 6, 20×5, to shareholders of record on July 16, 20×5. What amount

of retained earnings should be transferred to contributed capital because of this

dividend?

A. None

B. Market value of the stock at the date of distribution multiplied by the number of

dividend shares

C. Market value of the stock at the date of declaration multiplied by the number of

dividend shares

D. Par value per share multiplied by the number of dividend shares

Which of the following companys would be required to files its Form 10-K

electronically?

A. A privately-held corporation with 1,500 shareholders.

B. A municipality with $20 million in assets.

C. A public company with 520 shareholders.

D. All of these choices.

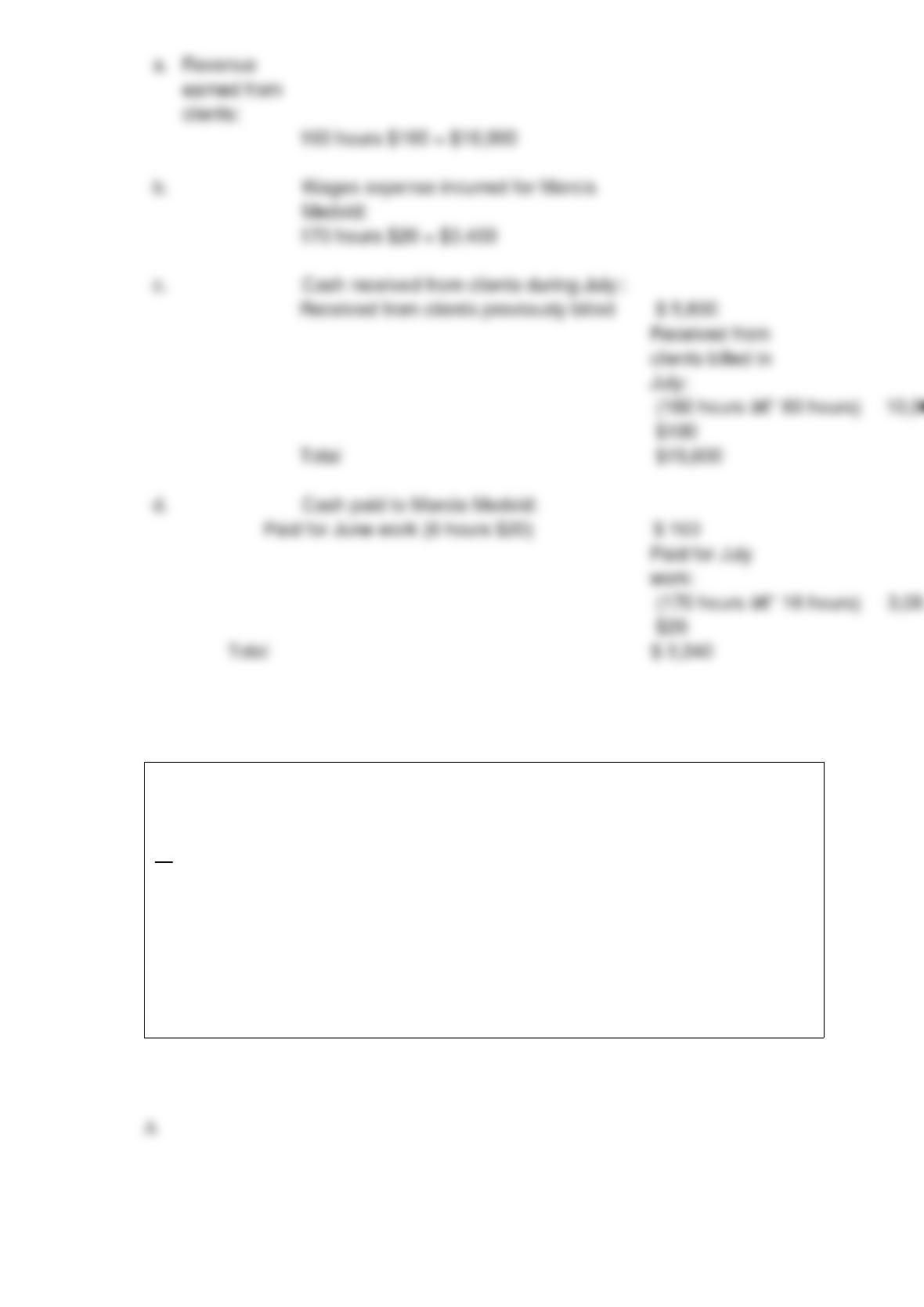

Kyle Biehl, an attorney, bills his clients at a rate of $100 per hour. At the beginning of

July, clients owed him $8,000, of which he collected $5,600 during the month. In July,

Kyle billed clients for 160 hours of work. By the end of July, 60 of these hours were

unpaid.

Kyle has one employee, Marcia Medvid, who is paid $20 per hour. During July, Marcia

worked 170 hours, of which 16 hours will be paid in August. The rest were paid in July

along with wages for 8 hours worked the last day of June.

Show calculations as you determine the following for the month of July:

a. Amount of revenue earned

b. Wages expense incurred

c. Cash received from clients

d. Cash paid to Marcia Medvid

Merckle Corporation owns 40 percent of the voting stock of Grant Corporation and

accounts for the investment using the equity method; Grant Corporation reports a net

loss of $30,000. Merckle Corporation’s entry to record the share of loss is:

A. Loss, Grant Corporation Investment 12,000

Investment in Grant Corporation 12,000

B. Loss, Grant Corporation Investment 12,000

Loss, Grant Corporation Investment 12,000

C. Investment in Grant Corporation 30,000

Cash 30,000

D. Investment in Grant Corporation 12,000

Cash 12,000

Which of the following would be deducted from the balance per books on a bank

reconciliation?

A. Notes collected by the bank

B. Deposits in transit

C. Service charges

D. Outstanding checks

All of the following must certify that a public company’s financial statements are

accurate, complete, and not misleading, except for the

A. chief financial officer.

B. director of human resources.

C. chief executive officer.

D. independent auditor.

Dividends Payable is an example of a(n)

A. contingent liability.

B. definitely determinable liability.

C. estimated liability.

D. long-term liability.

Which of the following is not a condition required by the SEC for the recognition of

revenue?

A. Delivery of goods or rendering of services.

B. Transfer of cash from the buyer to the seller.

C. Fixed or determinable price.

D. Existence of an arrangement.

Under which circumstance would one less closing entry than usual be made?

A. When a net loss has been suffered

B. When withdrawals by the owner are equal to net income for the period

C. When net income is zero

D. When the owner’s Capital account is zero prior to posting of closing entries

Under the perpetual inventory system

A. the cost of each item is recorded in the Merchandise Inventory account when it is

purchased.

B. when an inventory item is sold, its cost is transaferred to the Cost of Goods Sold

account.

C. the balance of the Merchandise Inventory account equals the cost of goods on hand.

D. All of these choices.

If the direct method is used to prepare a statement of cash flows, credit sales may not

automatically create a cash inflow because

A. some receivables may be uncollectible.

B. sales from a prior period may be collected in the current period.

C. sales from the current period may be collected in a future period.

D. All of these choices.

Start-up and organization costs

A. are capitalized, but never amortized.

B. are capitalized and amortized, usually over five years.

C. are expensed in the year incurred.

D. appear on the balance sheet as a current asset.

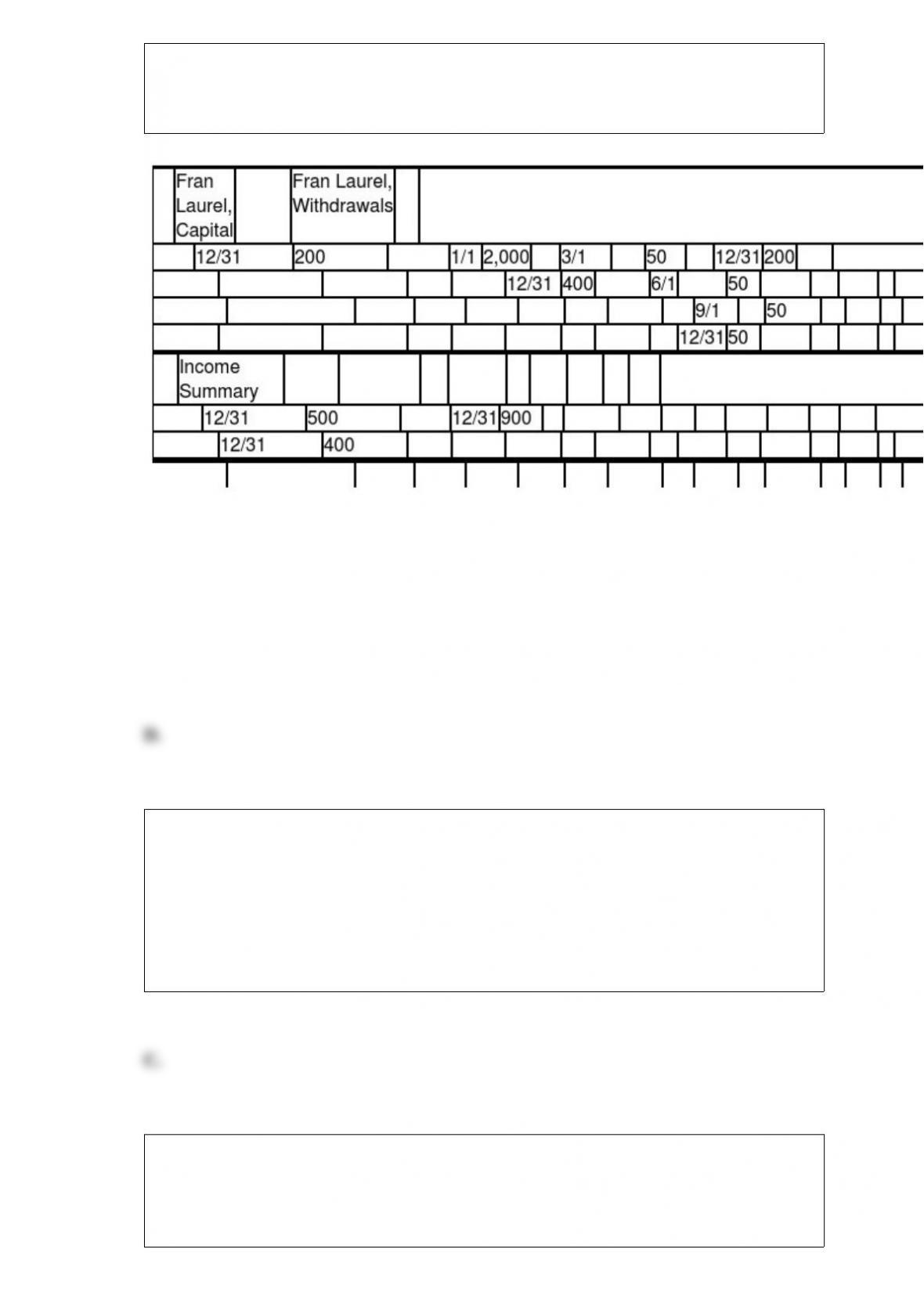

The owner’s Capital, Withdrawals, and Income Summary accounts for Laurel Repair

Company for the accounting period are presented below in T account form after the

recording and posting of closing entries:

The total amount of expenses for the period is

A. $200.

B. $400.

C. $900.

D. $500.

A retail store had goods available for sale during the period of $250,000 at retail and

$100,000 at cost. It has ending inventory of $28,500 at retail. What is the estimated cost

of goods sold?

A. $71,500

B. $94,300

C. $88,600

D. $82,900

Under an operating lease, the lessee records which of the following?

A. Rent expense

B. Capital lease obligations

C. Depreciation on the leased asset

D. Capital lease assets

All of the following statements about corporations are true except

A. they are chartered by the state.

B. ownership is represented by shares of stock.

C. the sale of stock does not dissolve the business.

D. the stockholders have direct control of the business.

Assume that on October 1, a note which has a face value of $2,000, bears interest at 6

percent for 90 days, received from a customer as an extension of his past-due account is

honored on its due date. The entry that would be made to record the receipt on due date

is:

A. Notes Receivable 2,000

Cash 2,000

B. Accounts Receivable 2,000

Interest Revenue 30

Cash 2,030

C. Accounts Receivable 2,030

Notes Receivable 2,030

D. Cash 2,030

The purchase of land is an example of a(n)

A. investing activity.

B. operating activity.

C. capital activity.

D. financing activity.

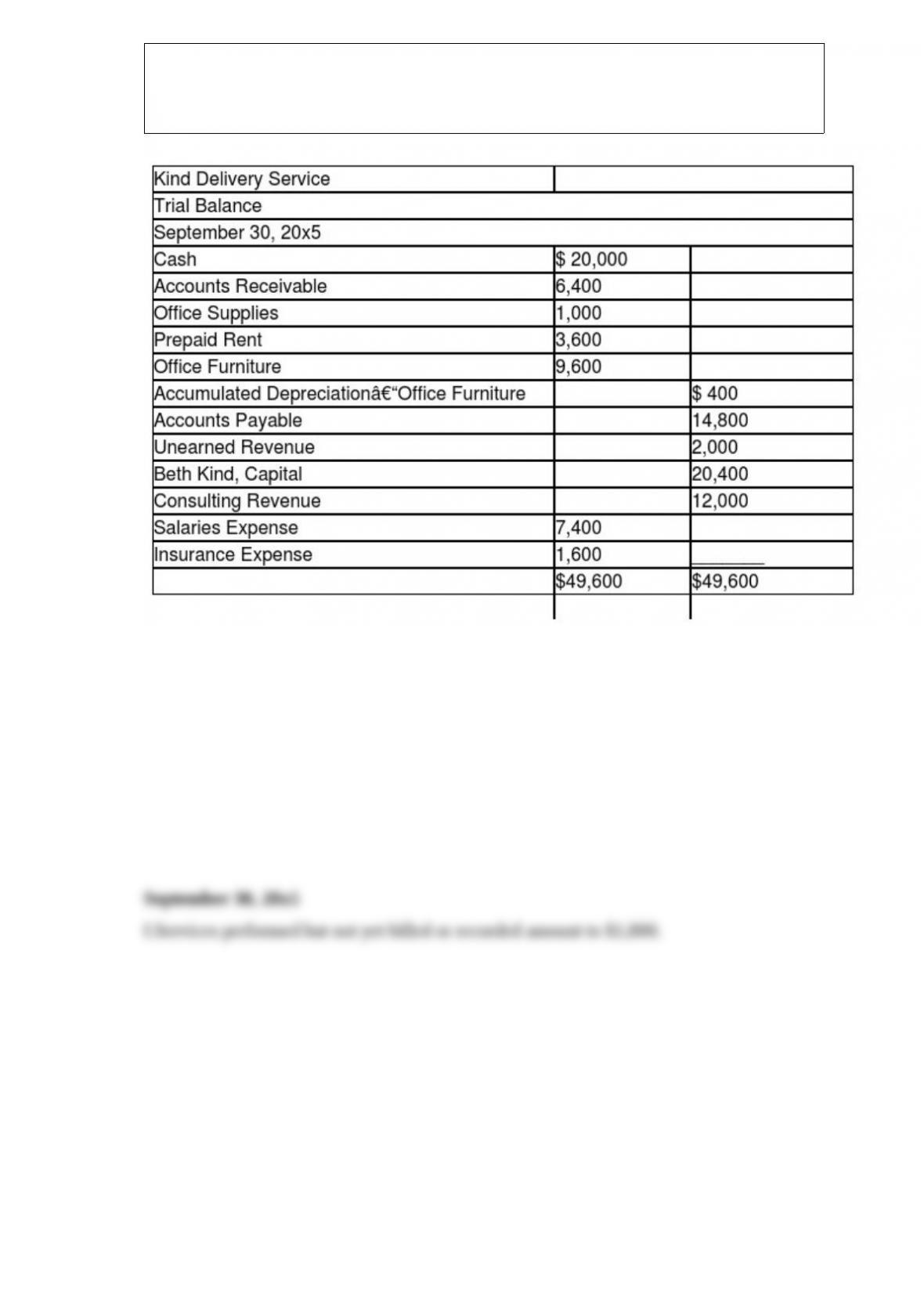

Use the following unadjusted trial balance to prepare adjusting entries, given the

additional information below it. Assume financial statements are prepared quarterly.

Omit explanations.

a.Of the revenue received in advance, 40 percent remained unearned on September 30.

b.The office furniture has an estimated five-year useful life and zero value at the end of

that time. Record depreciation for the quarter.

c.Salaries earned, but unpaid, totaled $1,520.

d.The Prepaid Rent applies to the six months beginning August 1, 20×5.

e.Office supplies on hand totaled $400 at the end of the quarter.

Which of the following accounts probably would have a smaller balance in the Adjusted

Trial Balance columns of a work sheet than in the Trial Balance columns?

A. Accumulated Depreciation–Equipment

B. Wages Payable

C. Wages Expense

D. Prepaid Advertising

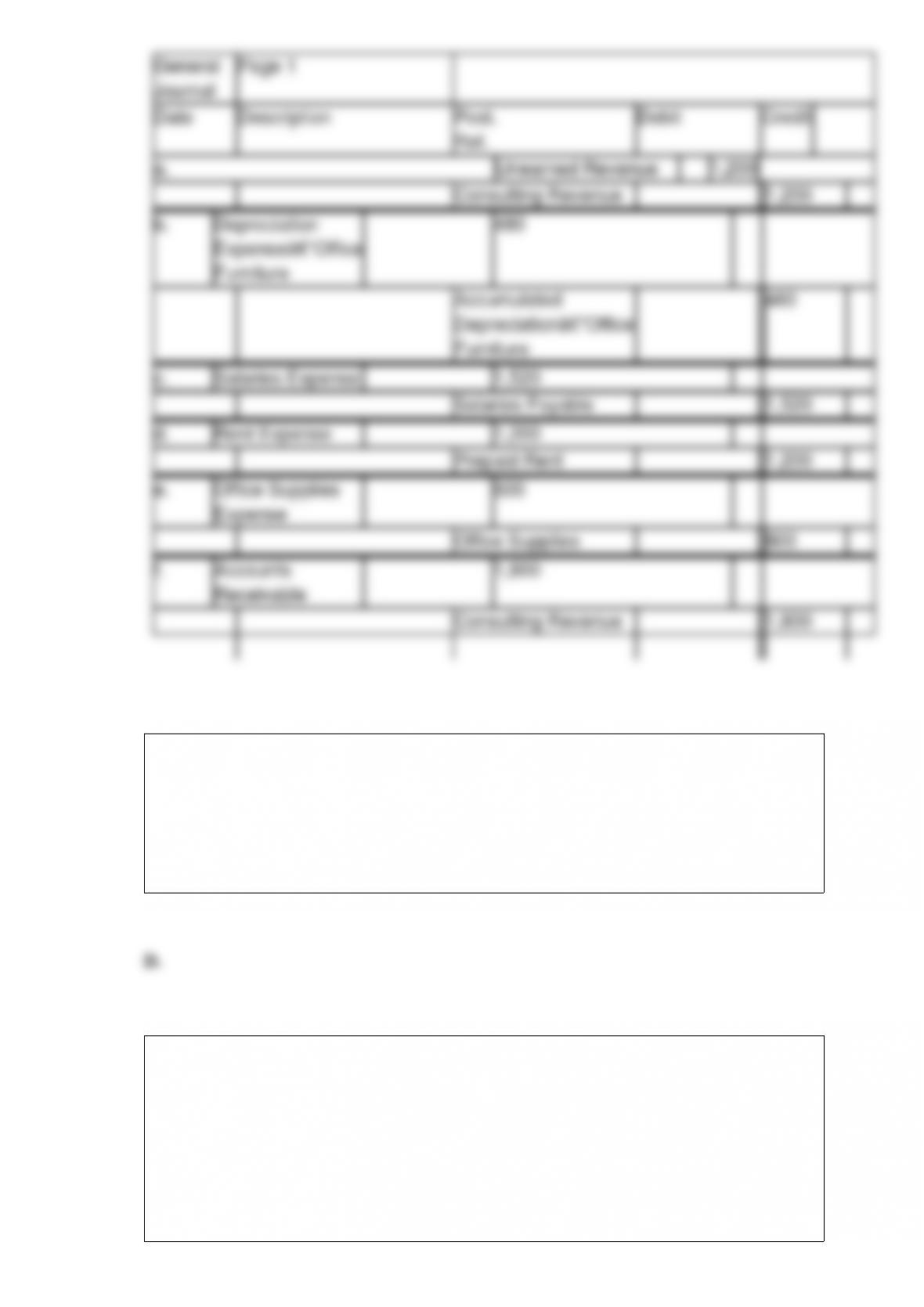

In the journal provided, prepare adjusting entries for the following items. Omit

explanations.

a. Depreciation on machinery is $940 for the accounting period.

b. Interest incurred on a loan but not paid or recorded is $635.

c. Office supplies of $600 were on hand at the beginning of the period. Purchases of

office supplies during the period totaled $200. At the end of the period, $80 in office

supplies remained.

d. Commissions amounting to $540 were earned but not recorded or collected by year

end.

e. Prepaid Rent had an $8,000 normal balance prior to adjustment. By year end, 40

percent had expired.

Juan invests $120,000 for a one-fifth interest in a partnership in which the other

partners have capital totaling $240,000 before admitting Juan. After distribution of the

bonus, Juan’s capital is

A. $120,000

B. $72,000

C. $96,000

D. $48,000

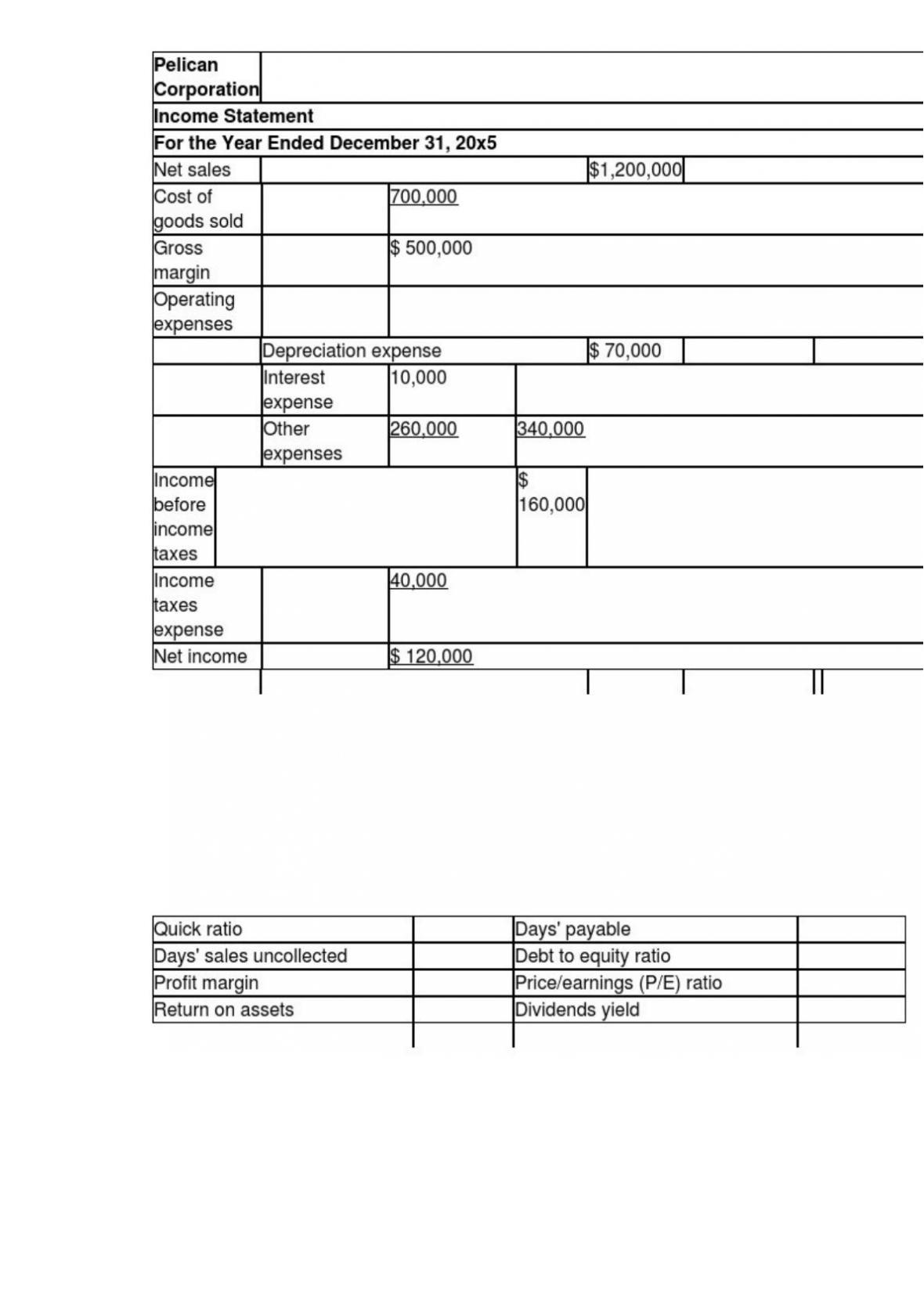

Financial statements for Pelican Corporation are presented below.

Note: Dividends of $0.60 per share were declared and paid during 20×5. The market price

of the stock on December 31, 20×5 was $18.00 per share.

Compute the following for 20×5 and place your answers in the spaces provided. Round

answers to two decimal places. Show your work.

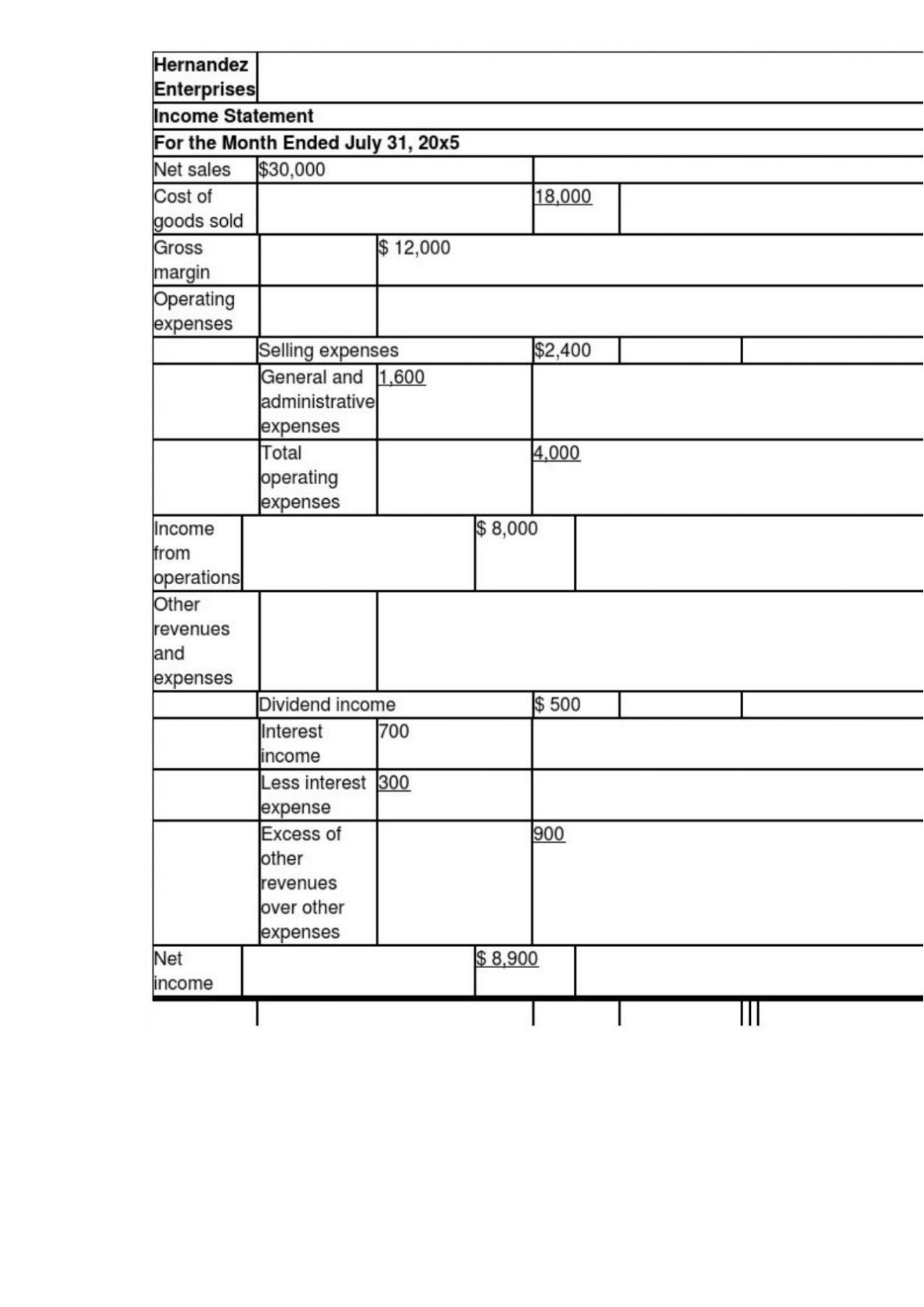

Use the information from the following multistep income statement to prepare a

single-step income statement in proper form.

Chelsea, Jack, and Connor have a partnership. Chelsea wishes to withdraw from the

partnership by removing assets that are greater than her current capital balance. Discuss

how this transaction is accounted for on the partnership books.

Why is it important for a company to maintain the same accounting methods and

practices from period to period?

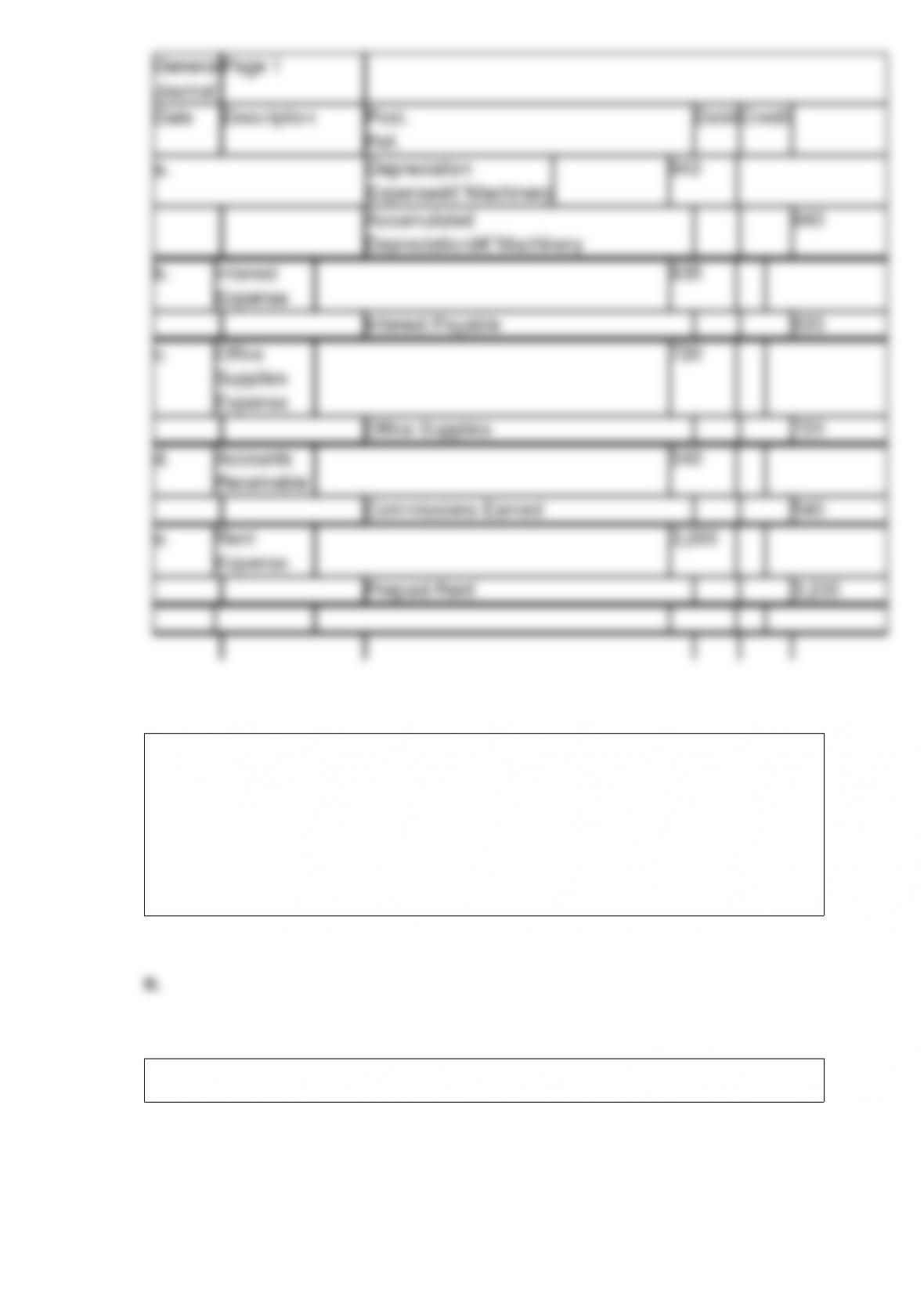

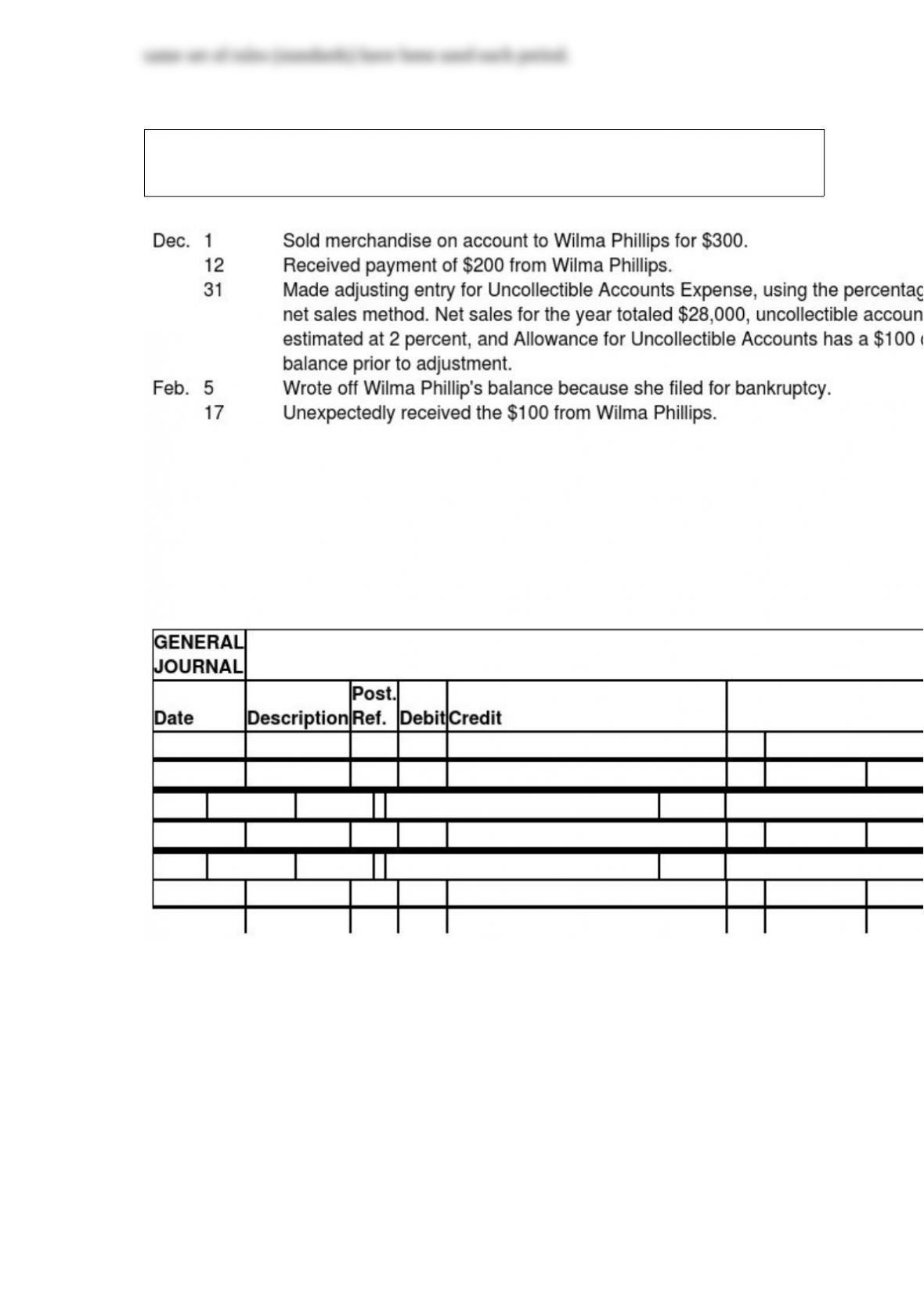

In the journal provided, prepare the entries for the following transactions. (Omit

explanations.)

Which two broad account categories are used to determine net income? Define each

category and list two examples of each type.

Custom Realty Services sold a house for a client and will be paid a commission for its

services.

Garcia Company’s owner’s equity equals one-half of the company’s total assets. The

company’s liabilities are $140,000. What is the amount of the company’s owner’s

equity?

Using the information below from the Income Statement and Balance Sheet columns of

Mesquite Company’s work sheet for the month ended April 30, 20×5, prepare the

income statement, statement of owner’s equity, and balance sheet.

Why might someone prefer to invest in a company by purchasing preferred stock rather

than common stock?

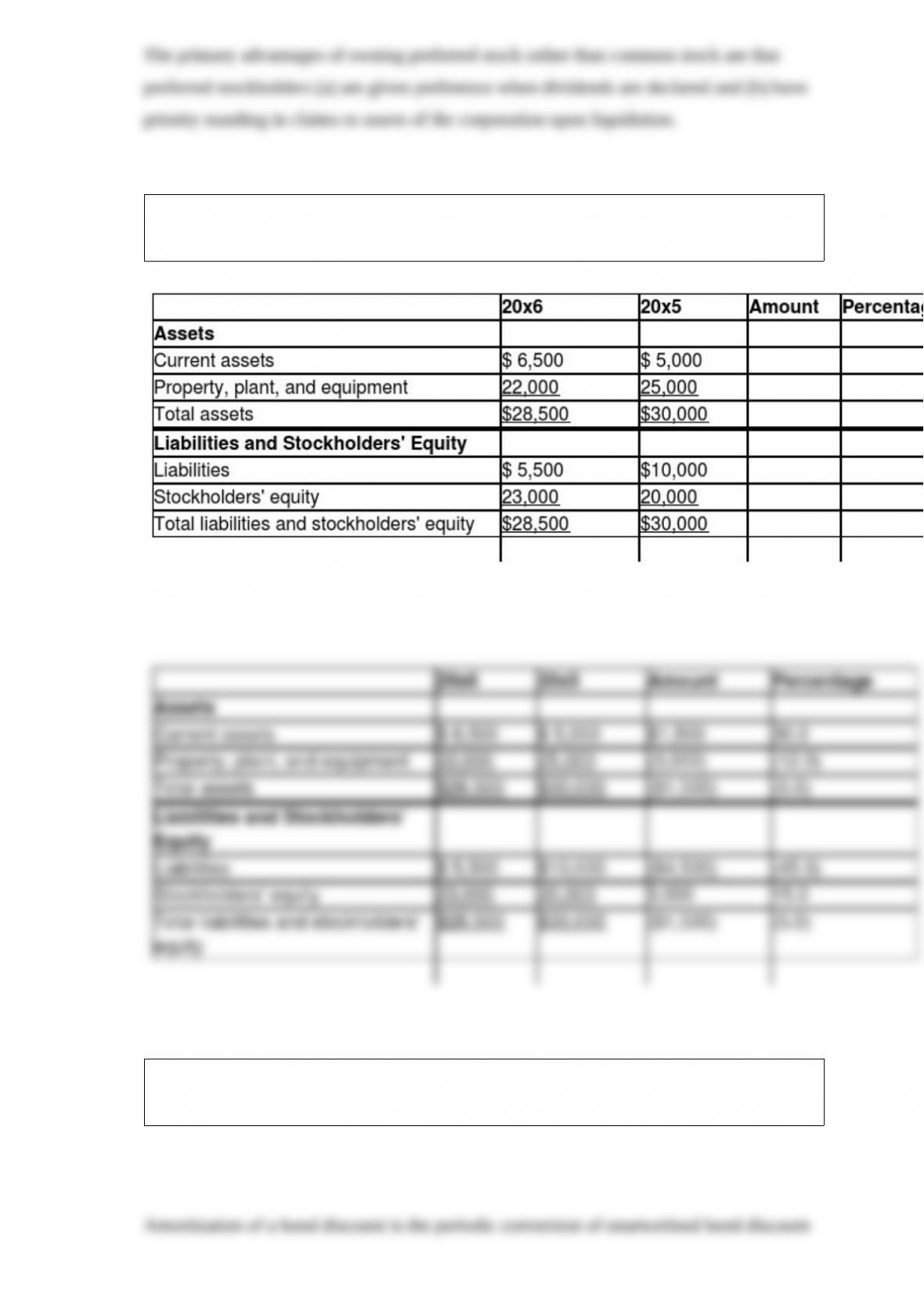

Prepare a horizontal analysis by computing the amounts and percentage changes for the

following balance sheet items; place your answers in the blanks provided.

Technically, what is meant by the amortization of a bond discount, and why is it

necessary?

A company enters into a contract to purchase a certain quantity of goods from another

company during the following month. At this point, would a liability exist? Explain

why or why not.

Waldo Ralph Company issued $40,000 of bonds with a 9 percent face rate. The bonds

are due in 5 years and interest is paid semiannually. The market rate of interest on the

date the bonds are issued is 12 percent. Calculate the present value of the bond issue,

using present value tables.

The profit margin and asset turnover ratios are important measures, but they have a

limitation. Describe these limitations and discuss the ratio that can be used to overcome

these deficiencies.

Elise, Farrah, and Gina are liquidating their business.

Ironwood Company has just started operations. The owner, Robert Ironwood, invested

$10,000 to get the business started. The company has made several sales on account,

but has not yet collected any cash from these sales. At this point, Ironwood’s cash flows

for expenses are exceeding its cash flows from revenues. How might Ironwood make

up the difference so it can maintain its liquidity?

The information that follows pertains to stockholders’ equity data of the Beagle

Corporation on December 31, 20×5. Compute the amount of each item indicated by a

letter in the listing below. Where necessary, carry answers to two decimal place.