DQ1.

DQ2.

DQ3.

DQ4.

DQ5.

DQ6.

DQ7.

DQ8.

amount paid on a lease is tax-deductible and provides greater liquidity. This is

debt to equity and interest coverage ratios. The analysis may also include a his-

can then judge how well the company has met its past debt obligations.

materially different from that produced by the effective interest method.

of repayment.

in relation to the stated rate of interest on the face of the bond.

A company may choose to lease rather than buy a long-term asset because the

torical comparison that reflects both good and poor economic times. The lender

The relationship between the prevailing market rate of interest and the stated rate

The straight-line method is acceptable only when it does not produce a result

The company would most likely issue a secured bond because rather than being

of interest on the face of the bond are the determining factors.

issued on the company’s general credit, certain assets are pledged as a guarantee

refinance or call the bonds if interest rates change.

The market price of a bond varies over time because the market interest rate varies

CHAPTER 14—Solutions

LONG-TERM LIABILITIES

Discussion Questions

Callable and convertible bonds are considered to add to management’s future

The lender reviews the enterprise’s current earnings and cash flows as well as its

Bond interest expense must be accrued at the close of each accounting period to

sometimes referred to as off-balance-sheet financing.

flexibility in financing a business because they offer options for management to

ensure proper matching of all the borrowing costs associated with bonds payable.

Interest payment dates rarely coincide with the end of the accounting period.

14-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 5.

2. 6.

3. 7.

4.

Reduction

in Debt

1. 4.

2. 5.

3. 6.

Unpaid Balance

** Rounded

at End of Period

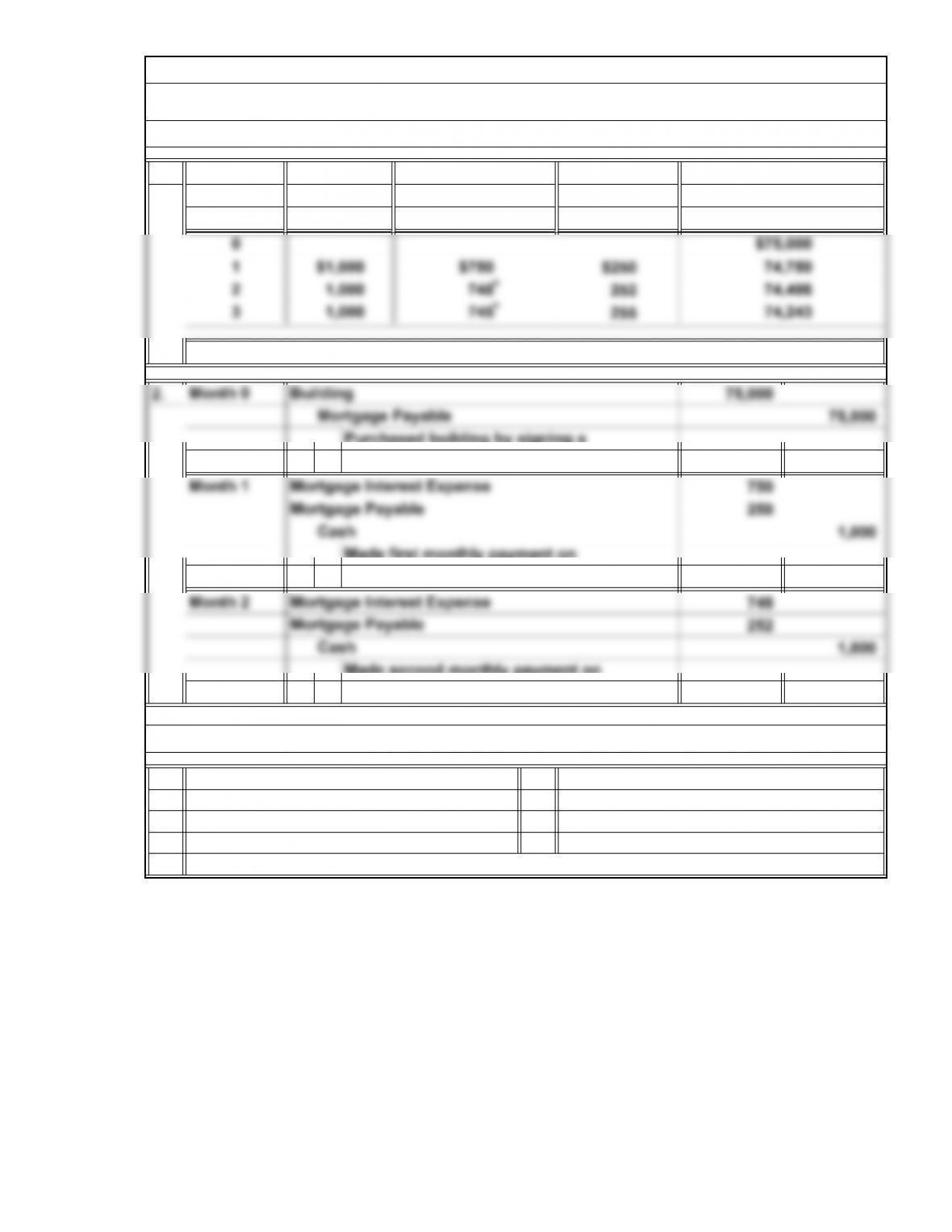

SE1. Types of Long-Term Liabilities

Month

Interest for 1

Short Exercises

SE2. Mortgage Payable

b

d

Payment

Monthly Month at 0.6667%*

on Unpaid Balance

e

SE3. Bond Characteristics

bc

f

a

d

a

cg

ef

14-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

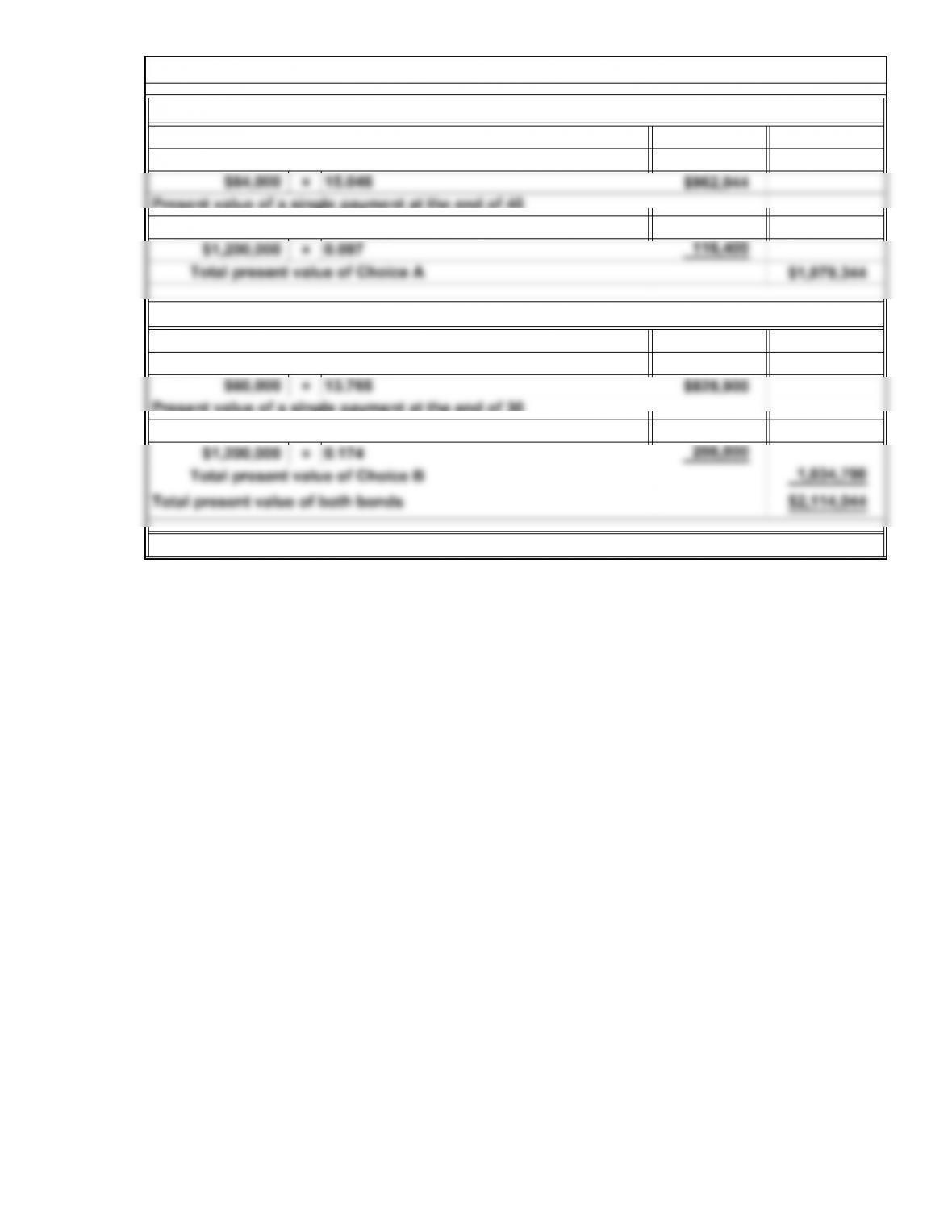

SE4. Valuing Bonds Using Present Value

(from Table 2*)

Present value of 40 periodic payments at 6%

Choice A

*From Appendix B

14-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2014

×=

2015

=

=

2014

(××6/12

‒ (××6/12

=– =

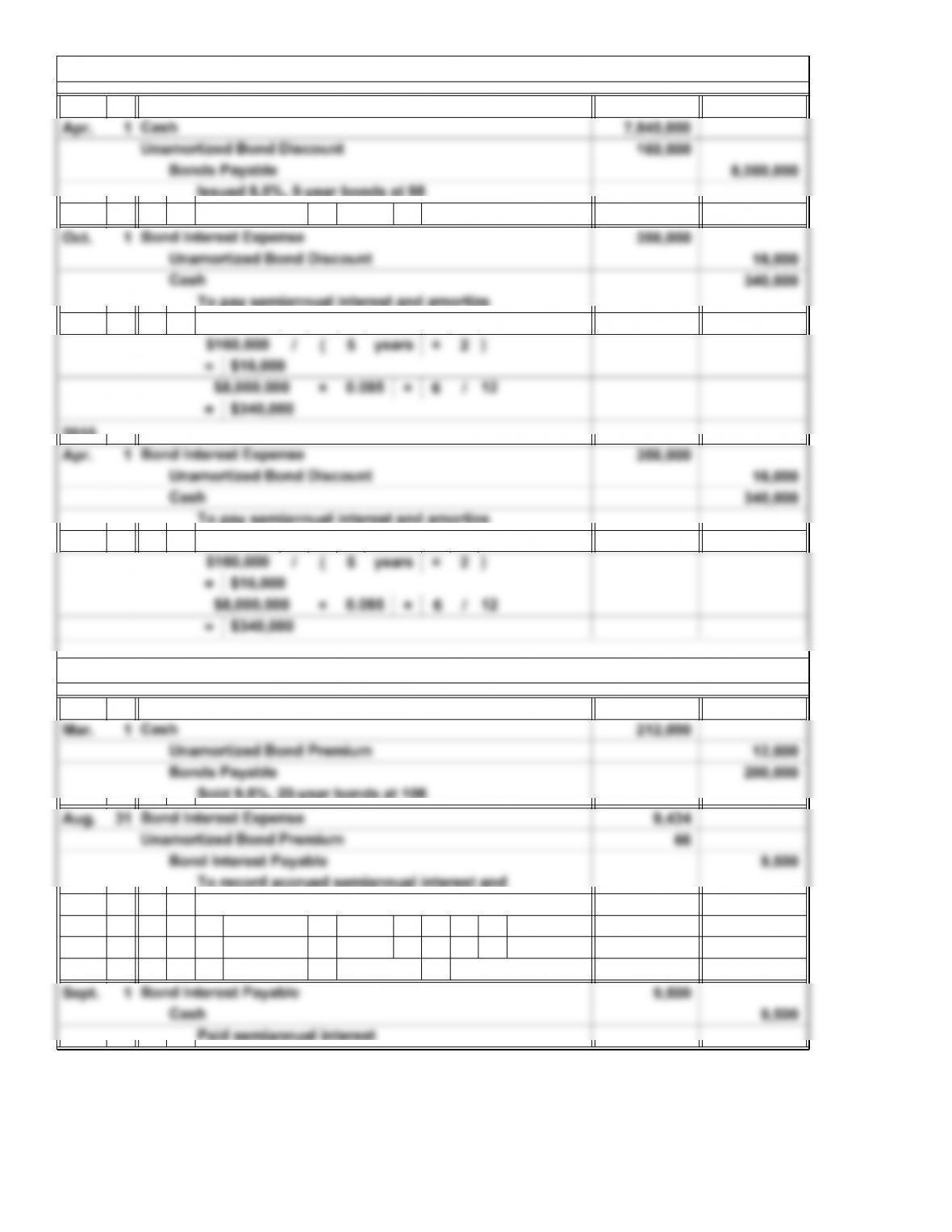

$8,000,000 0.98 $7,840,000

Issued 8.5%, 5-year bonds at 98

SE5. Straight-Line Method

$16,000

To record accrued semiannual interest and

amortize premium on 9.5%, 20-year bonds

$66$9,434

Paid semiannual interest

$200,000

$212,000

$9,500

0.089

0.095 )

)

SE6. Effective Interest Method

$340,000

14-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

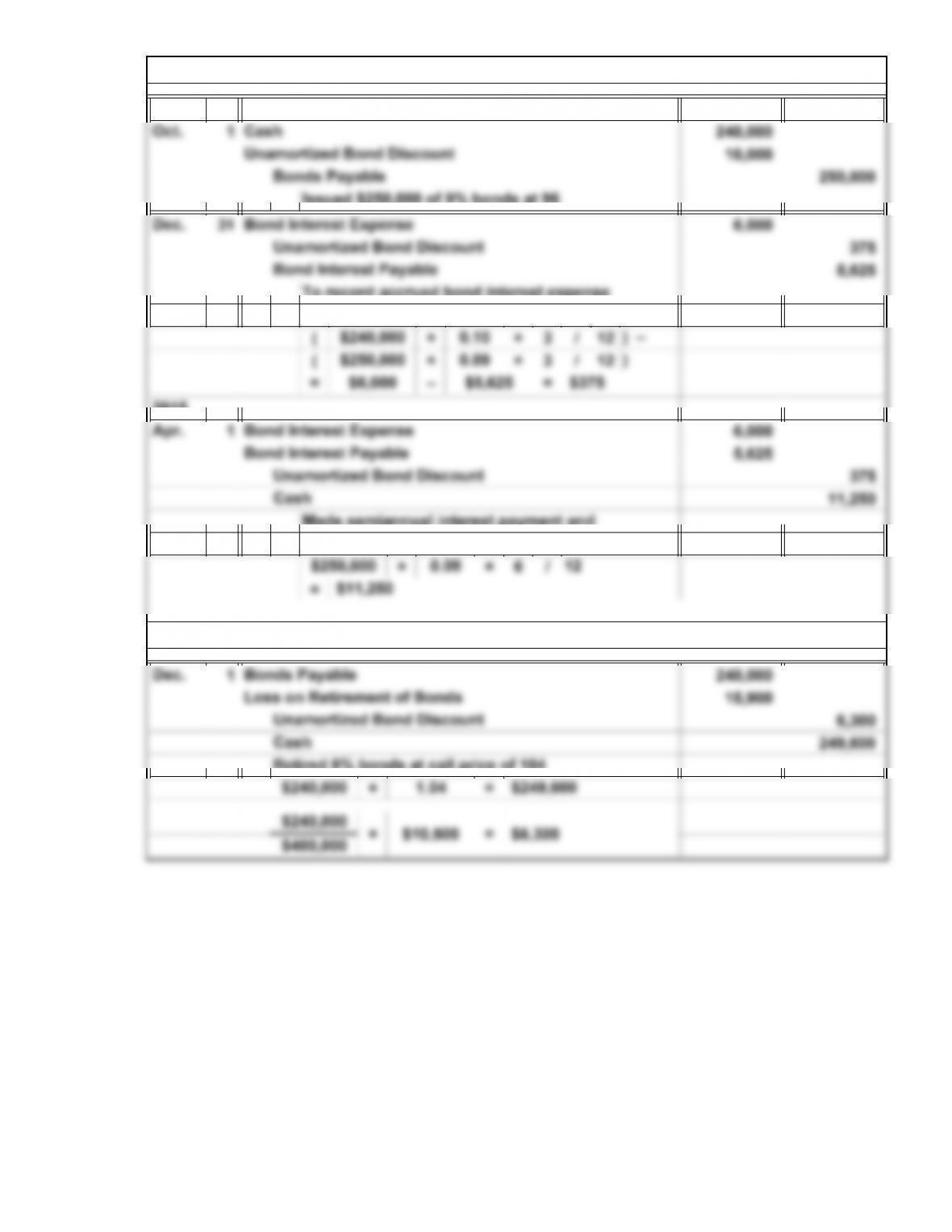

To record accrued bond interest expense

2014

SE7. Year-End Accrual of Bond Interest

2015

Made semiannual interest payment and

amortized bond discount

and amortize bond discount

$400,000 $6,300

$240,000 × $10,500 =

14-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

=

×4 /12=

×6 /12=

2.

1. 4.

2. 5.

3.

1. 4.

2. 5.

3.

=

$2,000,000

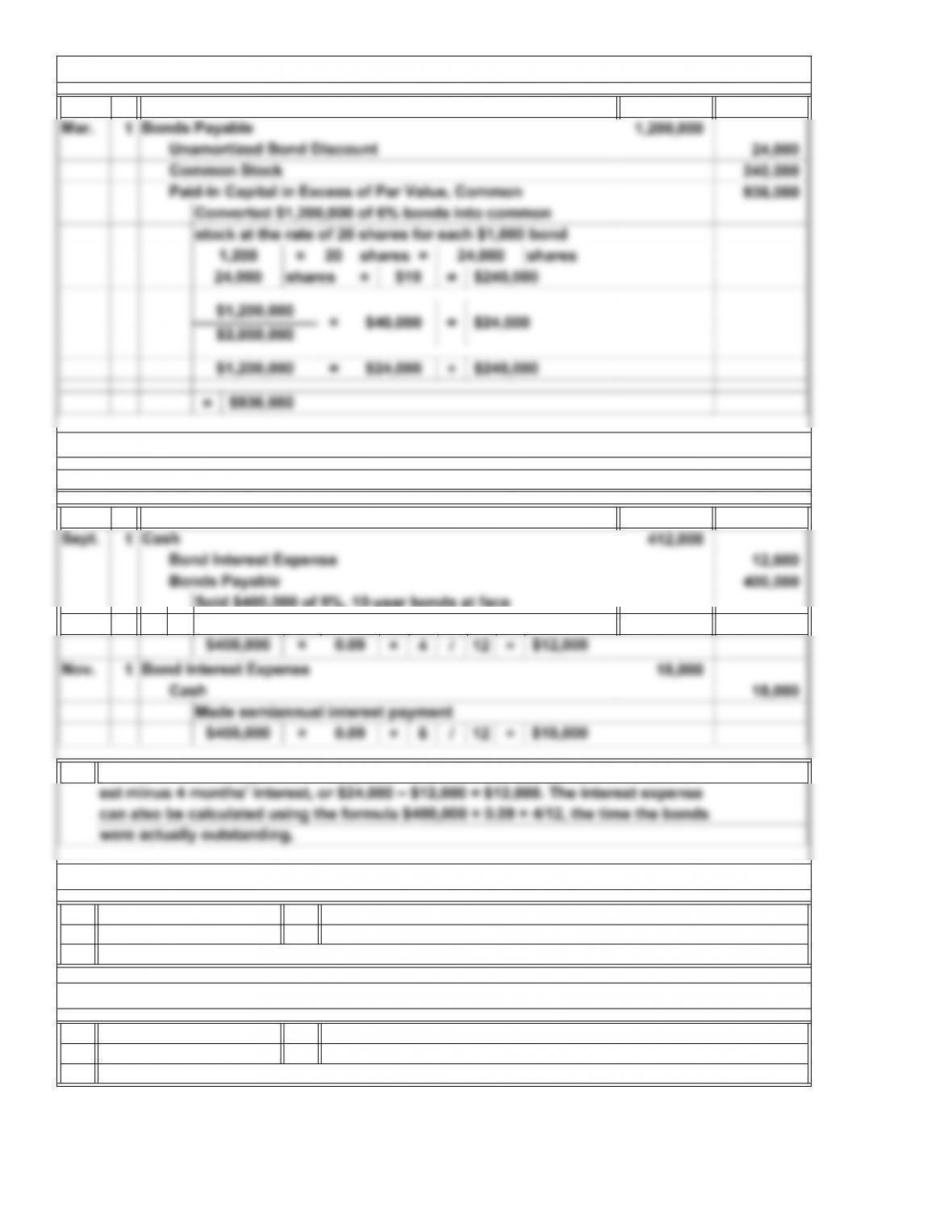

SE9. Bond Conversion

$40,000

2014

SE10. Bond Issue Between Interest Dates

1.

The bond interest expense for the year ended December 31, 2014, is 8 months’ inter-

est minus 4 months’ interest, or $24,000 – $12,000 = $12,000. The interest expense

can also be calculated using the formula $400,000 × 0.09 × 4/12, the time the bonds

were actually outstanding.

$400,000

$936,000

Made semiannual interest payment

2014

Disadvantage

Disadvantage

$400,000

d

b

c

SE11. Leases and Pensions Definitions

e

0.09

×

value plus accrued interest

×

a

SE12. Bond Versus Common Stock Financing

Advantage Advantage

Advantage

0.09 $18,000

$12,000

× $24,000

Sold $400,000 of 9%, 10-year bonds at face

14-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

Reduction

in Debt

1. 6.

2. 7.

3. 8.

4. 9.

5.

Made second monthly payment on

mortgage

at End of Period

Unpaid Balance

Month

Month at 1% onMonthly Unpaid Balance

Payment

Interest for 1

Exercises: Set A

E1A. Mortgage Payable

i

cd

E2A. Bond Issue Features and Bond Characteristics

a

h

f

e

b

g

14-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.