18 400

18 240

24 6,400

25 3,800

2.

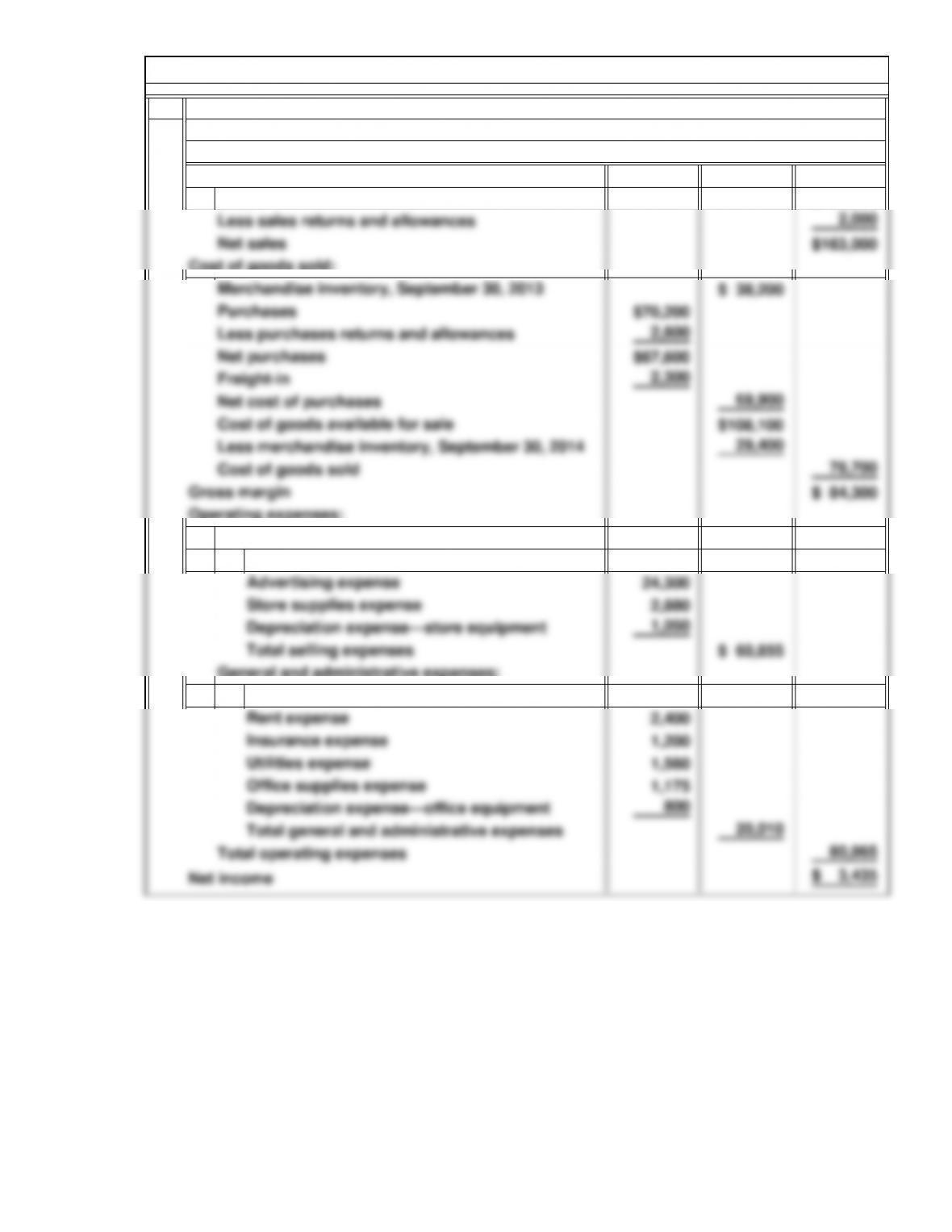

Net sales reflects gross sales adjusted for any sales discounts, sales returns, or allow-

P9. Merchandising Transactions: Perpetual Inventory System (Concluded)

Cash

to Merchandise Inventory account

Received check from Lina Lopez

July

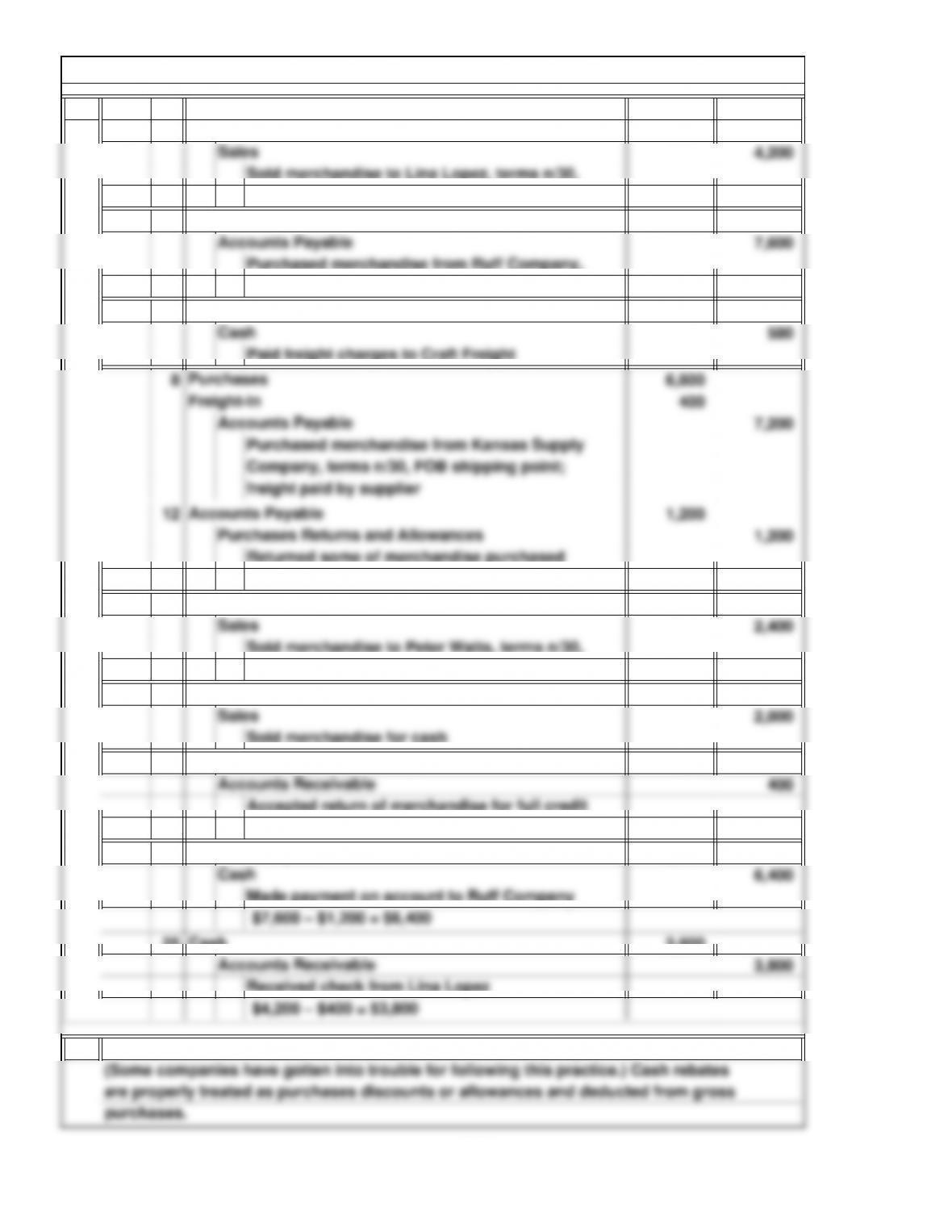

Made payment on account to Ruff Company

To transfer cost of merchandise returned

Sales Returns and Allowances

credit from Lina Lopez

Accepted return of merchandise for full

Merchandise Inventory

Accounts Payable

2014

6-29

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

1 4,200

3 7,600

5 580

15 2,400

17 2,000

18 400

24 6,400

25 3,800

2. Cash rebates should not be recorded as revenue because doing so overstates revenues.

Made payment on account to Ruff Company

Received check from Lina Lopez

Cash

Sales Returns and Allowances

Accounts Payable

from Lina Lopez

Accepted return of merchandise for full credit

Sold merchandise to Peter Watts, terms n/30,

Accounts Receivable

Returned some of merchandise purchased

P10. Merchandising Transactions: Periodic Inventory System

FOB shipping point

from Ruff Company

FOB shipping point

Sold merchandise to Lina Lopez, terms n/30,

Purchases

2014

Accounts Receivable

July

Freight-In

terms n/30, FOB shipping point

Purchased merchandise from Ruff Company,

Sold merchandise for cash

Cash

6-30

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

$165,000

$32,625

$12,875

P11. Merchandising Income Statement: Periodic Inventory System

Office salaries expense

General and administrative expenses:

Income Statement

For the Year Ended September 30, 2014

Store salaries expense

Selling expenses:

Operating expenses:

Sales

Net sales:

Will’s Sports Equipment

6-31

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2.

P11. Merchandising Income Statement: Periodic Inventory System (Concluded)

First, the statement shows net income of $3,435, which was earned on net sales of

$163,000. This is a profit margin of only 2.1 percent.

The gross margin is $84,300, or 51.7 percent of net sales; the operating expenses are

An analyst would want to examine the balance sheet in relation to the income

statement.

for Will’s Sports Equipment to prior years and to other companies of similar size,

within the same industry, and covering the same period of time.

(1) as a whole, (2) in components, and (3) in relation to other information.

This question is meant to get the students thinking about how to analyze financial

Third, the net income, $3,435, can be compared with the total assets of the business

Second, the components of gross margin and operating expenses can be examined.

Fourth, when possible, an analysis would also include comparing the ratios above

to compute return on assets and with total owner’s equity to compute return on equity.

gross margin and/or by decreasing the operating expenses.

$80,865, or 49.6 percent of net sales. Net income can be improved by increasing the

6-32

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

7 12,000

8 24,000

9 1,016

14 9,600

14 2,400

17 12,000

19 7,200

20 38,400

21 21,600

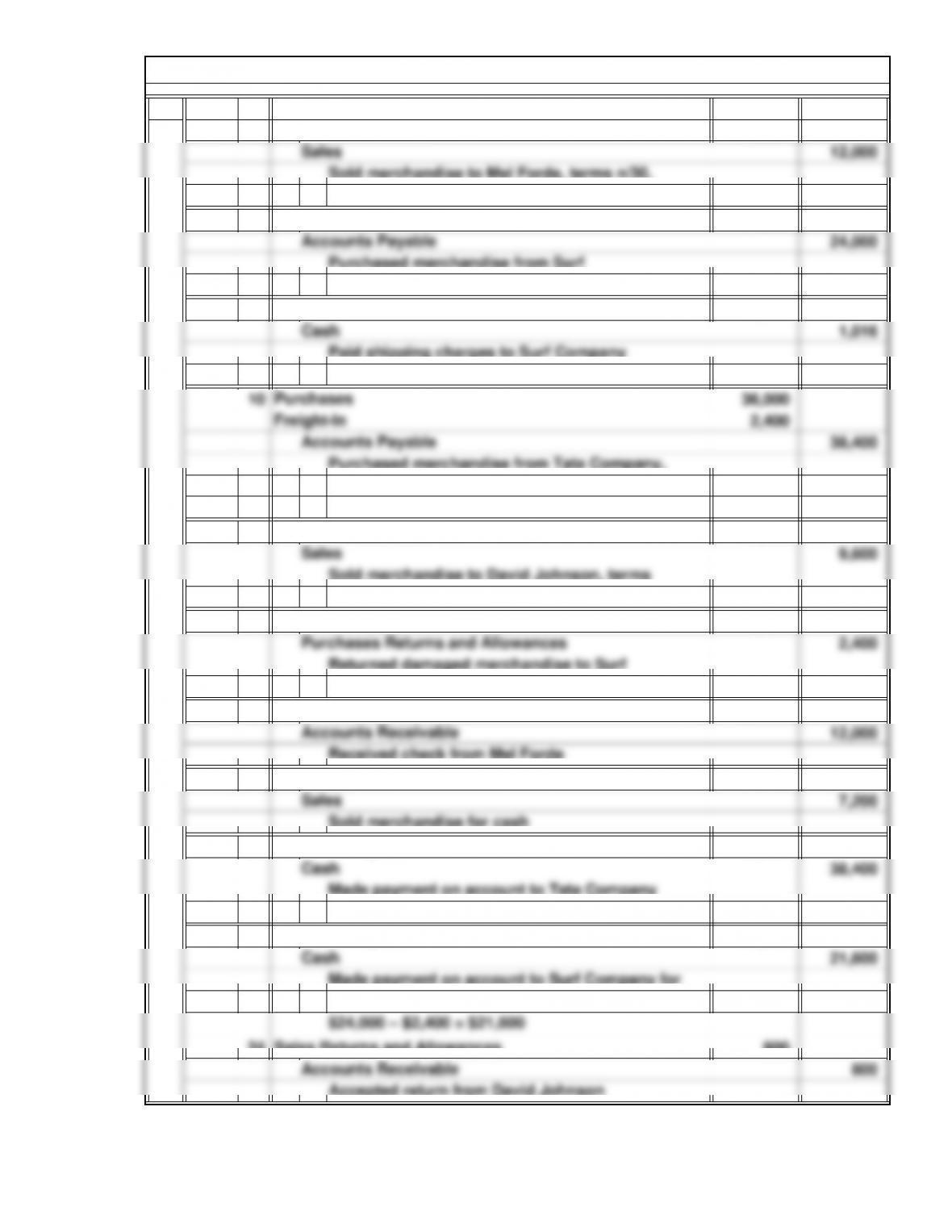

24 800

Accepted return from David Johnson

Sales Returns and Allowances

Accounts Payable

Made payment on account to Surf Company for

purchase of October 8, net of return on October 14

P12. Merchandising Transactions: Periodic Inventory System

Made payment on account to Tata Company

Received check from Mel Forde

for purchase of October 10

Accounts Payable

Sold merchandise for cash

Cash

Returned damaged merchandise to Surf

Company for credit

Sold merchandise to David Johnson, terms

Accounts Payable

n/30, FOB shipping point

Accounts Receivable

Purchased merchandise from Tata Company,

Accounts Receivable

FOB shipping point

Oct.

Sold merchandise to Mel Forde, terms n/30,

Company, terms n/30, FOB shipping point

2014

Freight-In

Purchases

Purchased merchandise from Surf

terms n/30, FOB shipping point; Tata Company

paid freight costs

Cash

6-33

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

inventory system like the one proposed for Books Unlimited. Sales are monitored at the

Note to Instructor: Many specialty store chains, including bookstores, use a perpetual

can be monitored on a day-by-day basis. Fast-selling books can be reordered quickly,

and slow-selling books can be moved to other stores or returned to the publisher before

Centralization of the records would mean that sales trends among the stores could be

national or regional level, and individual store managers have little or no say in the titles

or other products that are stocked.

ing sales, purchases, and returns and in maintaining the records. This may be much more

of the periodic inventory system is that financial statements are prepared only when a

physical inventory is taken, in this case every six months.

The Perpetual Inventory System

A principal advantage of the perpetual inventory system is that sales and inventory levels

ister. There may be some merit to the system of relying on the judgment of the store man-

The Periodic Inventory System

An advantage of the periodic inventory system is that it is usually less costly to admin-

is also excellent for use with small groups, with the participants being asked to develop

arguments for either the periodic inventory system or the perpetual inventory system.

C1. Conceptual Understanding: Periodic versus Perpetual Inventory Systems

Note to Instructor: This case can be used for class discussion or as a writing exercise. It

Cases

monitored, allowing inventory to be shifted from stores where sales have been slow to

6-34

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

3.

C2. Conceptual Understanding: Effects of a Weak Dollar

A weak U.S. dollar means that one dollar may be exchanged for fewer euros or, con-

versely, that one euro is now worth more in terms of dollars. Thus, when McDonald’s pre-

pares its financial statements in dollars, sales in Europe translate into more dollars than

previously. Assume, for instance, that the company sold €12,000,000 worth of Big Macs in

Europe in each of two years. Also assume that in the first year one euro is worth $1.06

cash flow management in one or all of the following ways:

Reduce the inventory period. (Suggestions: Analyze inventory to reduce inventory

ceivables. For Amazing, it is 140 days (160 days minus 20 days). Amazing can improve its

Increase the payable period. (Suggestions: Pay suppliers at last possible time instead

6-35

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

Cash sales and collection on account: Accounts receivable are not as important to

C4. Annual Report Case: The Operating Cycle and Financing Period

Memorandum

Date: Today’s Date

To: Instructor’s Name

From: Student’s Name

Re: CVS’s Operating Cycle

The operating cycle is the length of time from the purchase of inventory until it is sold and

Purchase of inventory: Maintaining an adequate merchandise inventory is very impor-

6-36

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

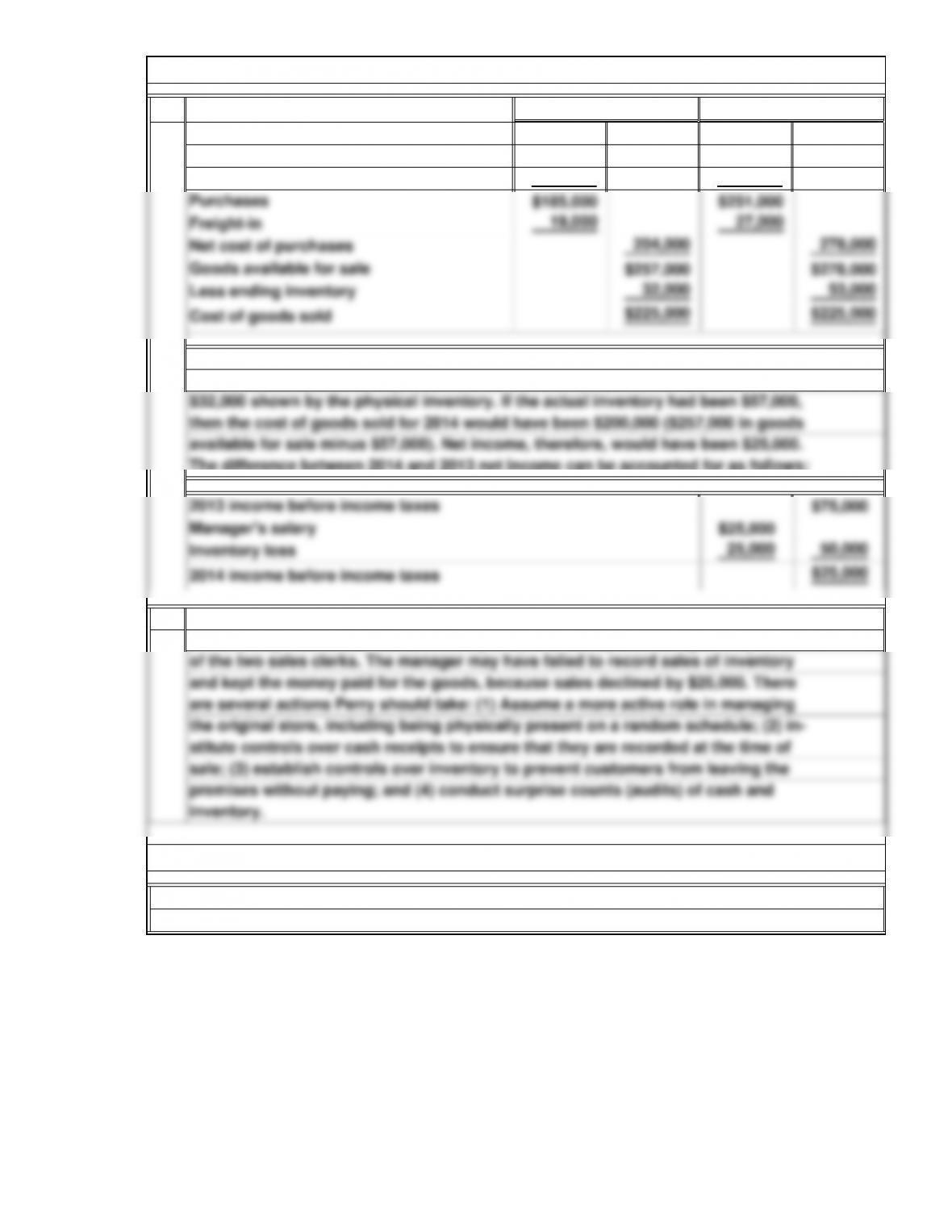

$ 53,000 $ —

$200,000 $271,000

15,000 20,000

2.

1.

2013

Beginning inventory

Purchases

C6. Decision Analysis: Analysis of a Merchandising Income Statement

2014

The inventory loss could have occurred as the result of embezzlement or theft. In-

ventory may have been stolen, either by shoplifters or by the manager or by either

of the two sales clerks. The manager may have failed to record sales of inventory

Less purchases allowances

C7. Continuing Case: Annual Report Project

students.

Note to Instructor: Answers will vary depending on the company selected by the

6-37

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.