DQ1.

Discussion Questions

Both are important. Accrual accounting is essential to dividing inventory between

CHAPTER 7—Solutions

INVENTORIES

what benefits the current period (cost of goods sold) and what benefits the next

7-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

**

Rounded

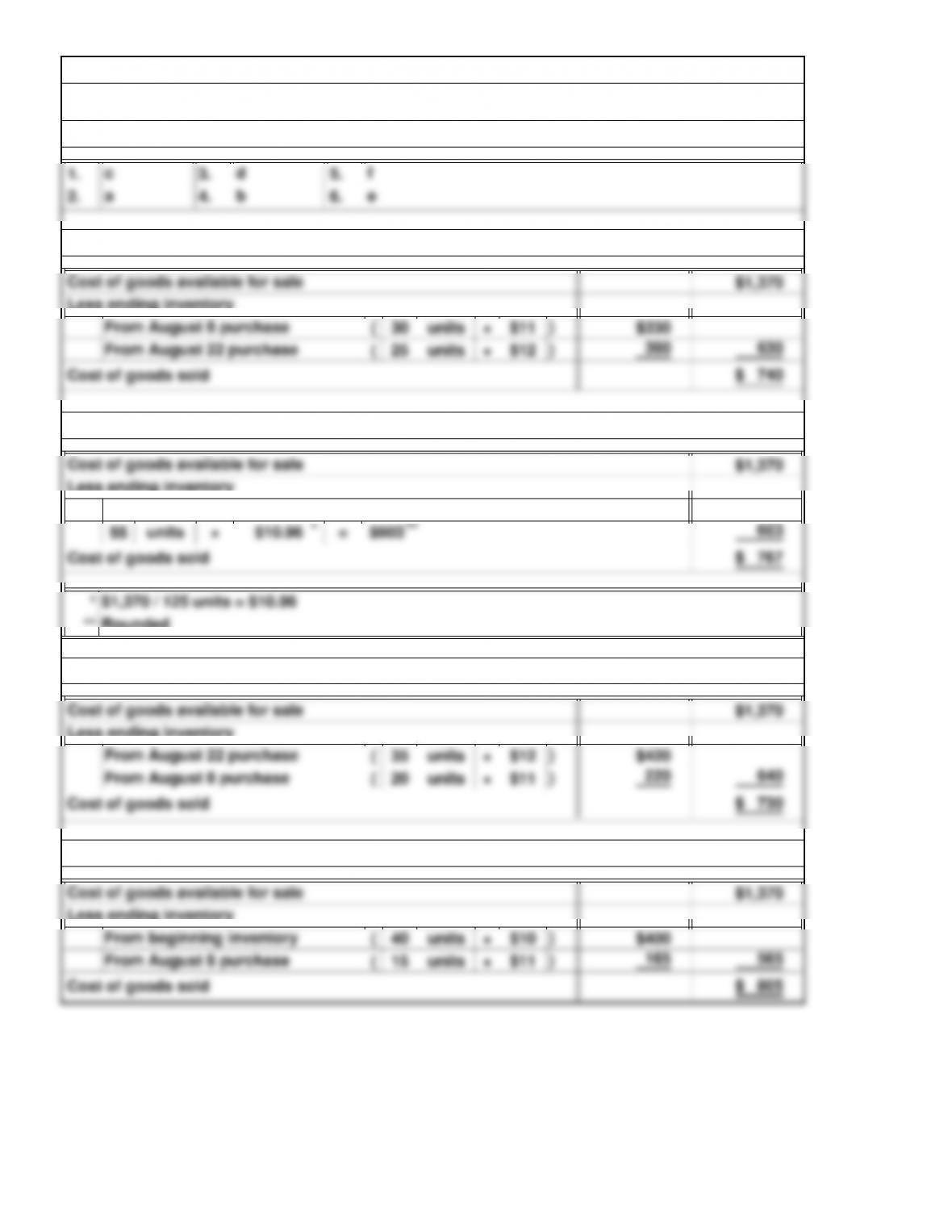

SE1. Inventory Concepts

SE2. Specific Identification Method

SE4. FIFO Method: Periodic Inventory System

Short Exercises

7-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Average-

Cost FIFO LIFO

Method Method Method

Cost

Units per Unit Amount*

SE7. Average-Cost Method: Perpetual Inventory System

*Rounded

Method

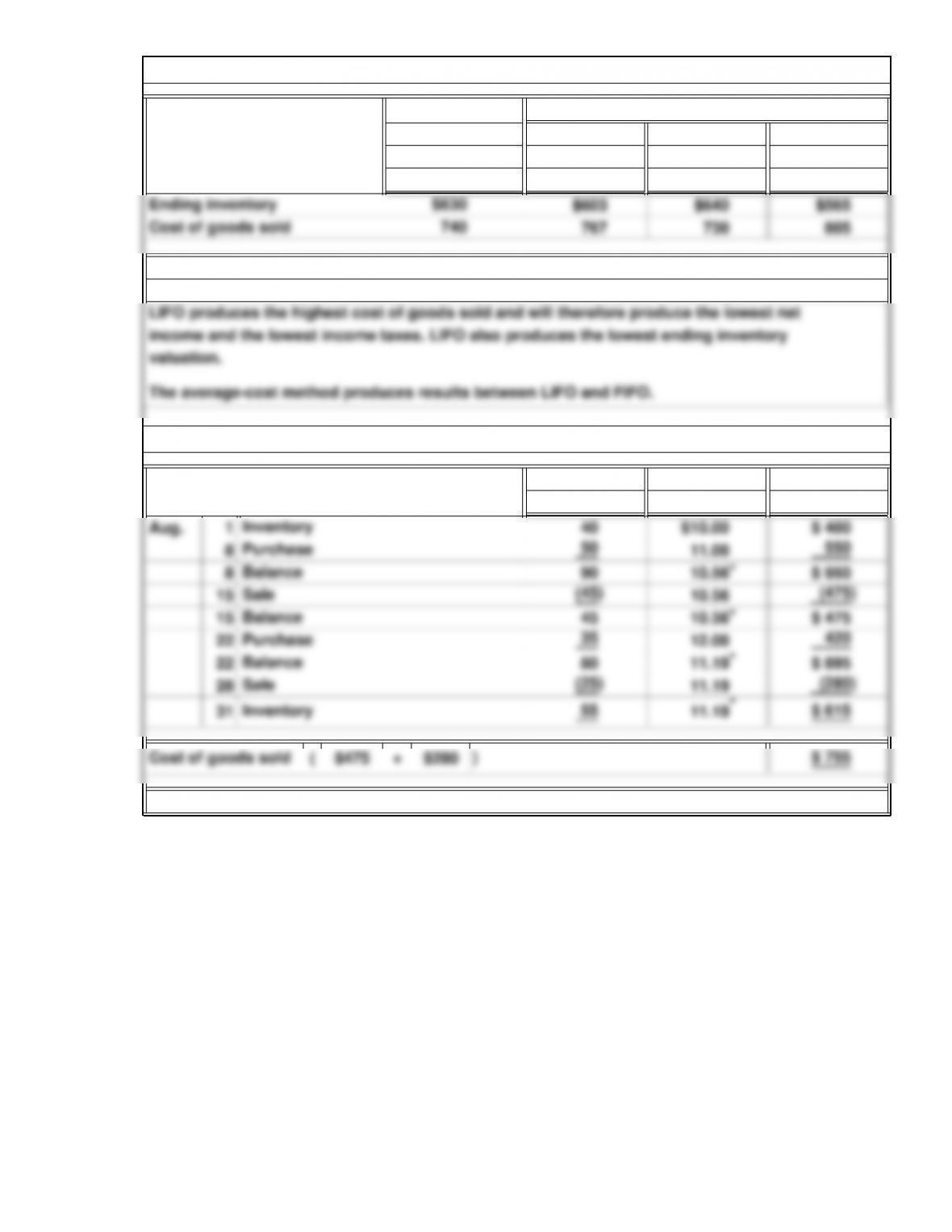

The average-cost method produces results between LIFO and FIFO.

valuation.

SE6. Effects of Inventory Costing Methods and Changing Prices

Specific

Identification

Periodic Inventory System

7-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Cost

Units per Unit

Cost

Units per Unit

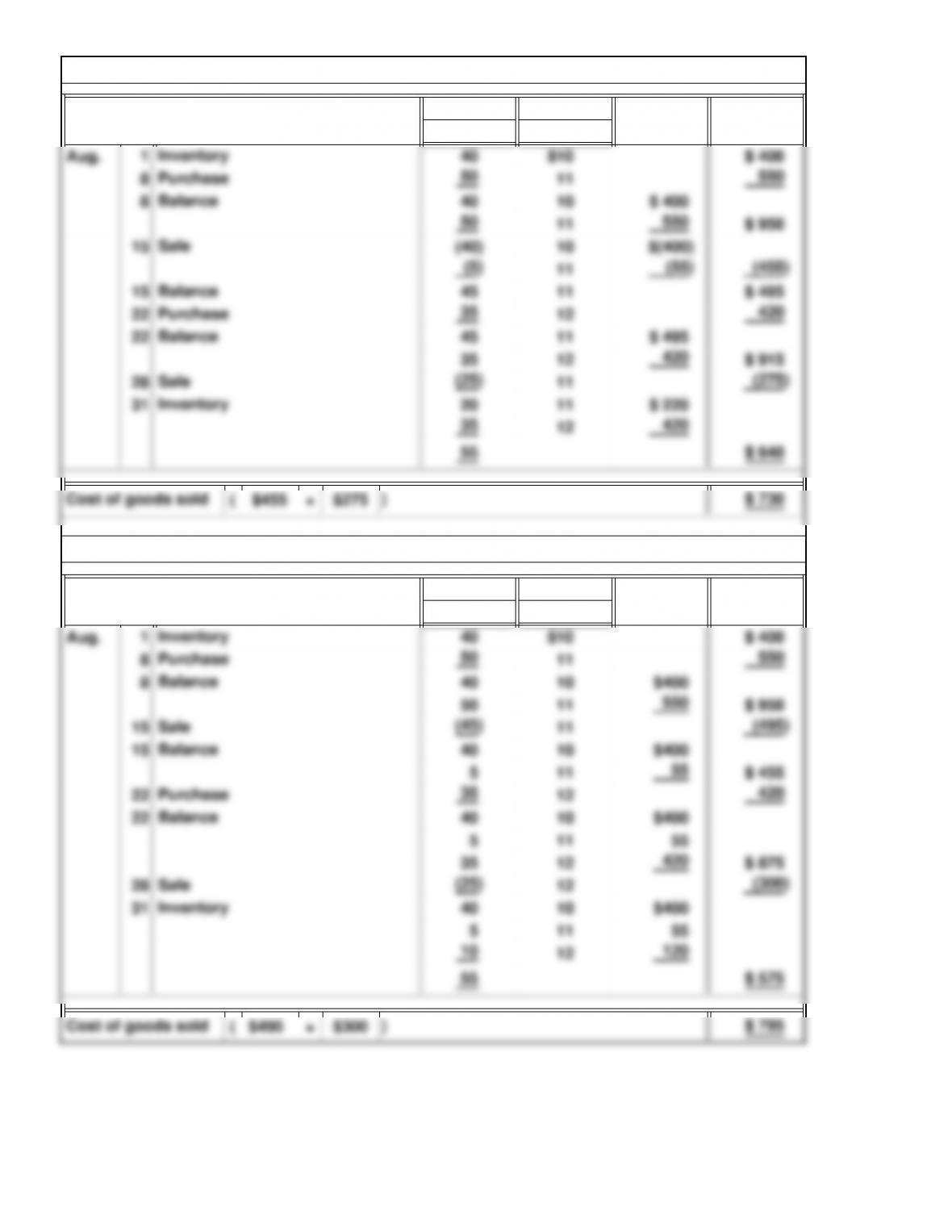

SE9. LIFO Method: Perpetual Inventory System

SE8. FIFO Method: Perpetual Inventory System

7-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Cost Retail

365

Average Inventory

Number of Days in a Year

*Rounded

$2,200,000

SE10. Retail Inventory Method

=

=

times*

days

Days’ Inventory on Hand

$520,000 = 4.2

7-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

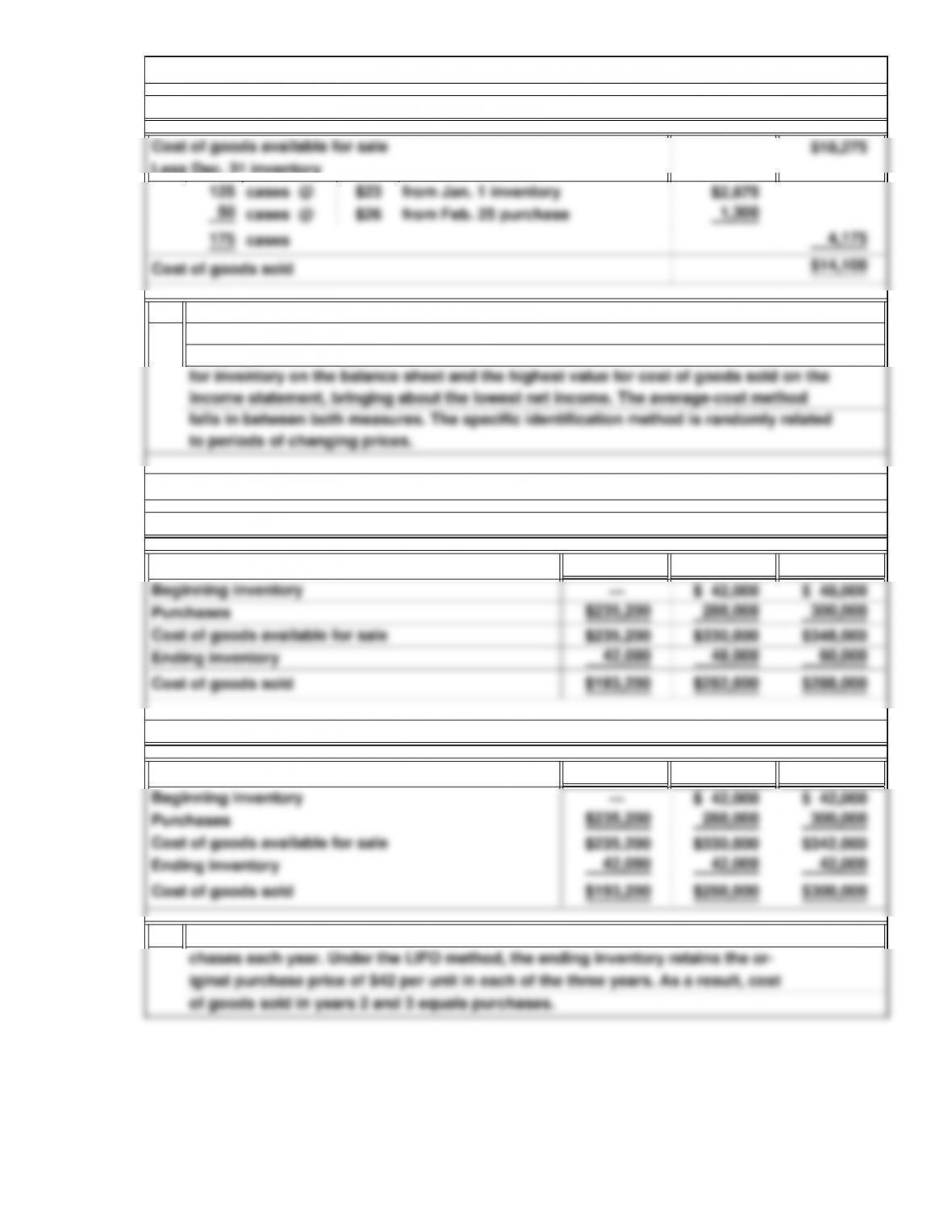

E2A. Periodic Inventory System and Inventory Costing Methods

1. Specific identification method

Ending inventory

2. Average-cost method

Exercises: Set A

E1A. Accounting Conventions and Inventory Valuation

a conservative inventory method in these circumstances as well. Under LIFO, the earlier

higher prices in inventory needed to be adjusted downward.

change be disclosed and the effects of the change described. Following the lower-of-cost-

or-market rule for valuing inventory is a conservative method of accounting because it an-

ticipates losses. Fewer adjustments will be anticipated in the future because under FIFO,

the most recent prices, which are declining, are used to price inventory. As a result, this is

According to the convention of consistency, a company must follow the same accounting

principles from year to year. Thus, a change to FIFO would violate this convention. If the

7-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

5.

Year 1 Year 2 Year 3

Year 1 Year 2 Year 3

3.

E2A. Periodic Inventory System and Inventory Costing Methods (Concluded)

Under the FIFO method, the ending inventory takes on the unit price of the pur-

2. LIFO method

E3A. Periodic Inventory System and Inventory Costing Methods

1. FIFO method

In this period of rising prices, the FIFO method resulted in the highest value for inven-

tory on the balance sheet and the lowest cost of goods sold on the income statement,

bringing about the highest net income. The LIFO method resulted in the lowest value

4. LIFO method

7-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

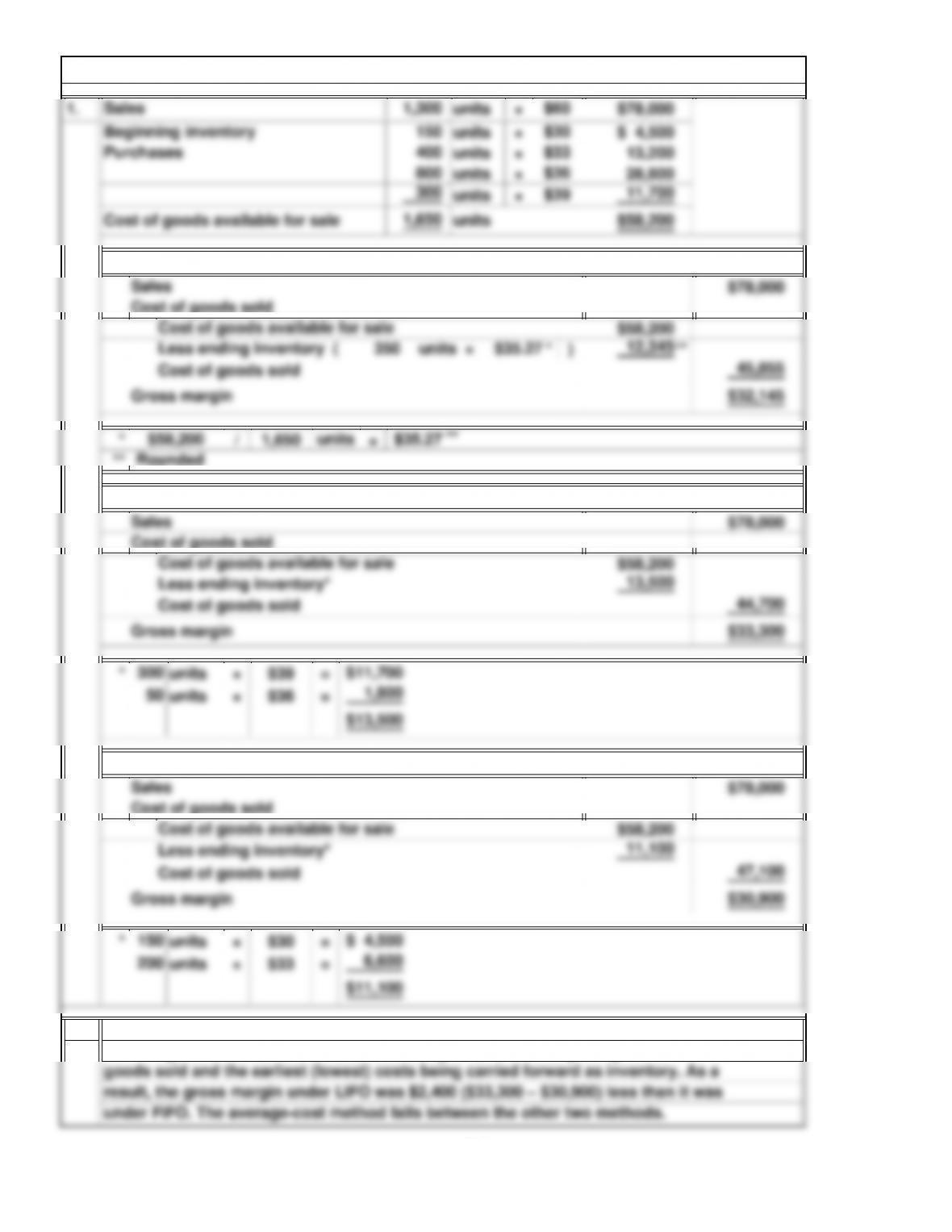

* units × $30 =

units × $33 =

2.

E4A. Periodic Inventory System and Inventory Costing Methods

$11,100

150 $ 4,500

result, the gross margin under LIFO was $2,400 ($33,300 – $30,900) less than it was

under FIFO. The average-cost method falls between the other two methods.

200 6,600

The unit cost of merchandise rose steadily during the month of June. When prices

are rising, LIFO results in the most recent (highest) costs being assigned to cost of

goods sold and the earliest (lowest) costs being carried forward as inventory. As a

7-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

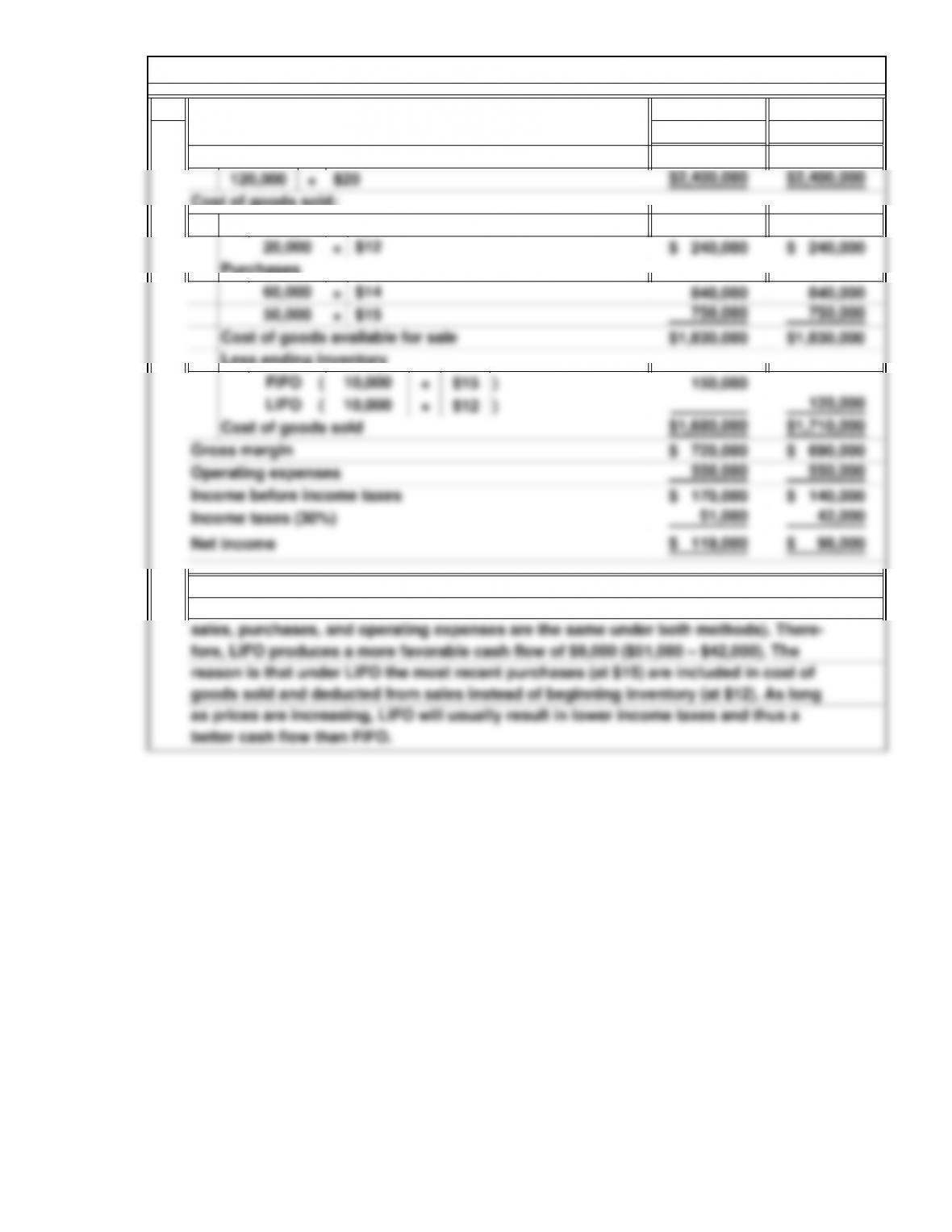

1. FIFO LIFO

Method Method

$1,830,000 $1,830,000

Sales

Less ending inventory

Cost of goods sold:

Beginning inventory

Cost of goods available for sale

E5A. Effects of Inventory Costing Methods on Cash Flows

as prices are increasing, LIFO will usually result in lower income taxes and thus a

better cash flow than FIFO.

goods sold and deducted from sales instead of beginning inventory (at $12). As long

7-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.