Bal. —

5,000 e. 1,000

*

**

Net sales:

Sales

Less sales returns and allowances

The balance of Cash is a credit because there is no data about the beginning balance

and entries have been posted only to the credit side of the account.

$2,800 – $1,000 = $1,800

a.

Merchandise Inventory

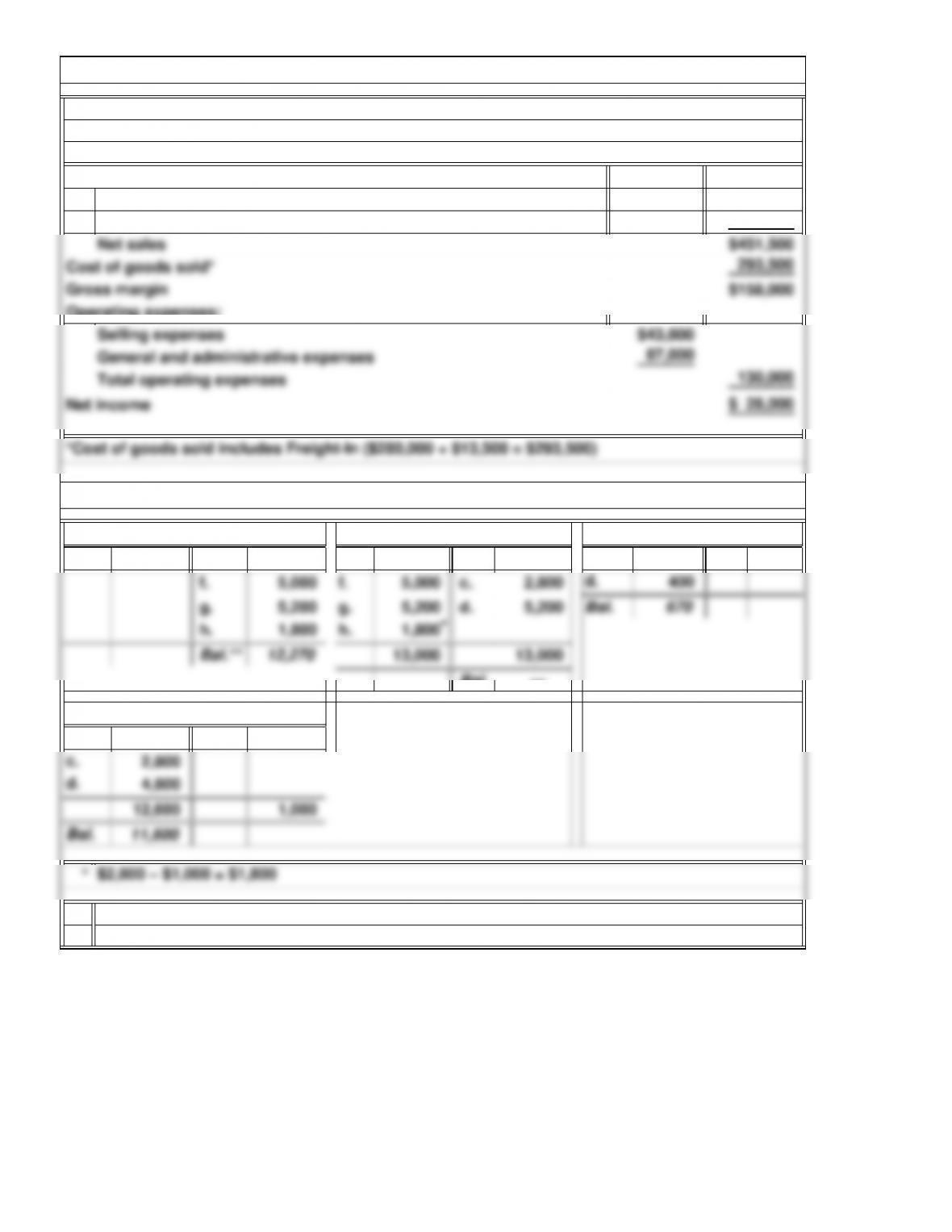

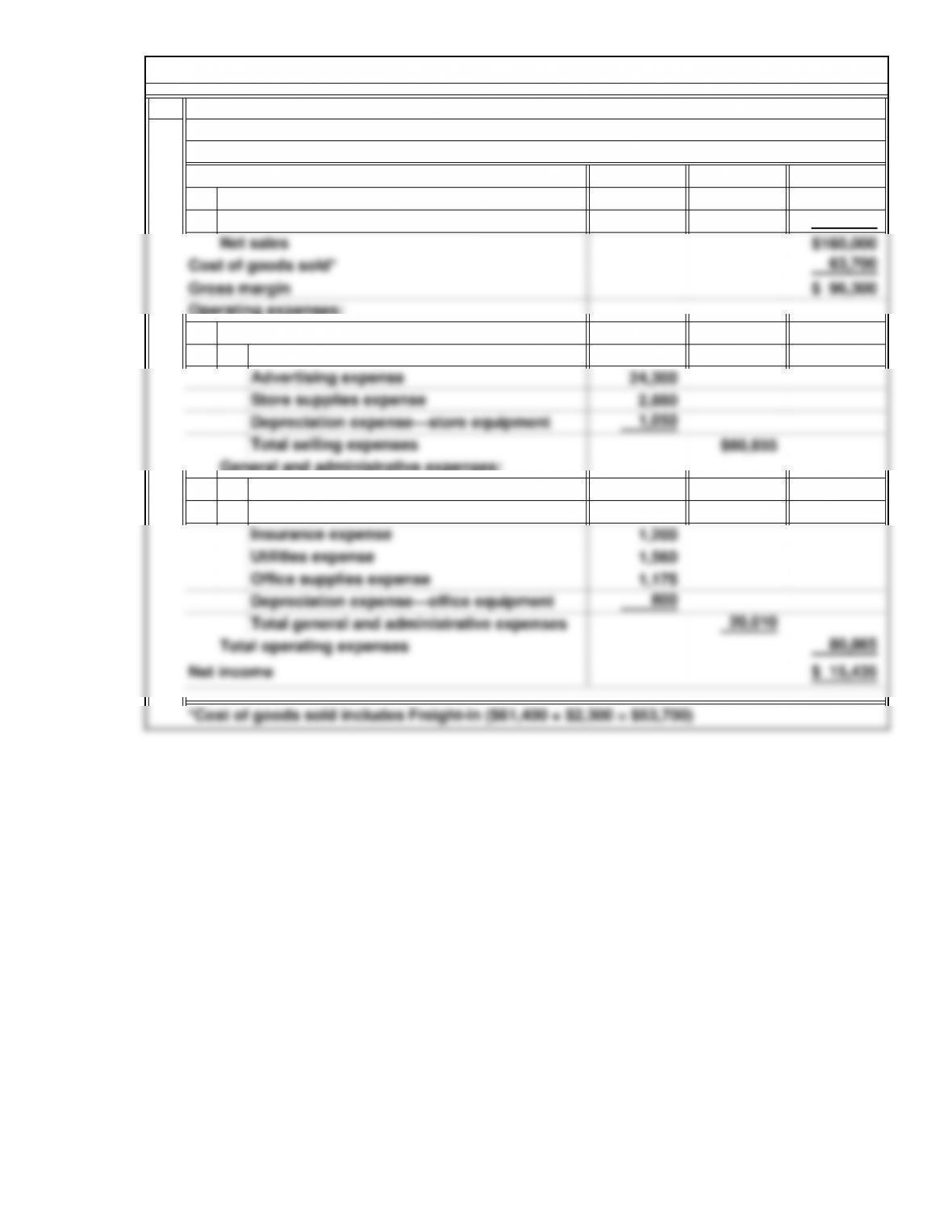

E8A. Preparation of the Income Statement: Perpetual Inventory System

Infosys Company

Income Statement

For the Year Ended December 31, 2014

$475,000

23,500

6-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2,000 2,600

600

—

350 11/15 1,500 1,500 350

**

$297,000

15,200

Sales

Less sales returns and allowances

11/20

11/15

Income Statement

For the Year Ended December 31, 2014

Net sales:

11/20

Bal.

2,600

E10A. Recording Sales: Perpetual Inventory System

Sales

Merchandise Inventory

11/20

11/20 600

Cash

11/15

The balance of Merchandise Inventory is a credit because there is no data about the be-

ginning balance and a larger amount has been posted to the credit side of the account.

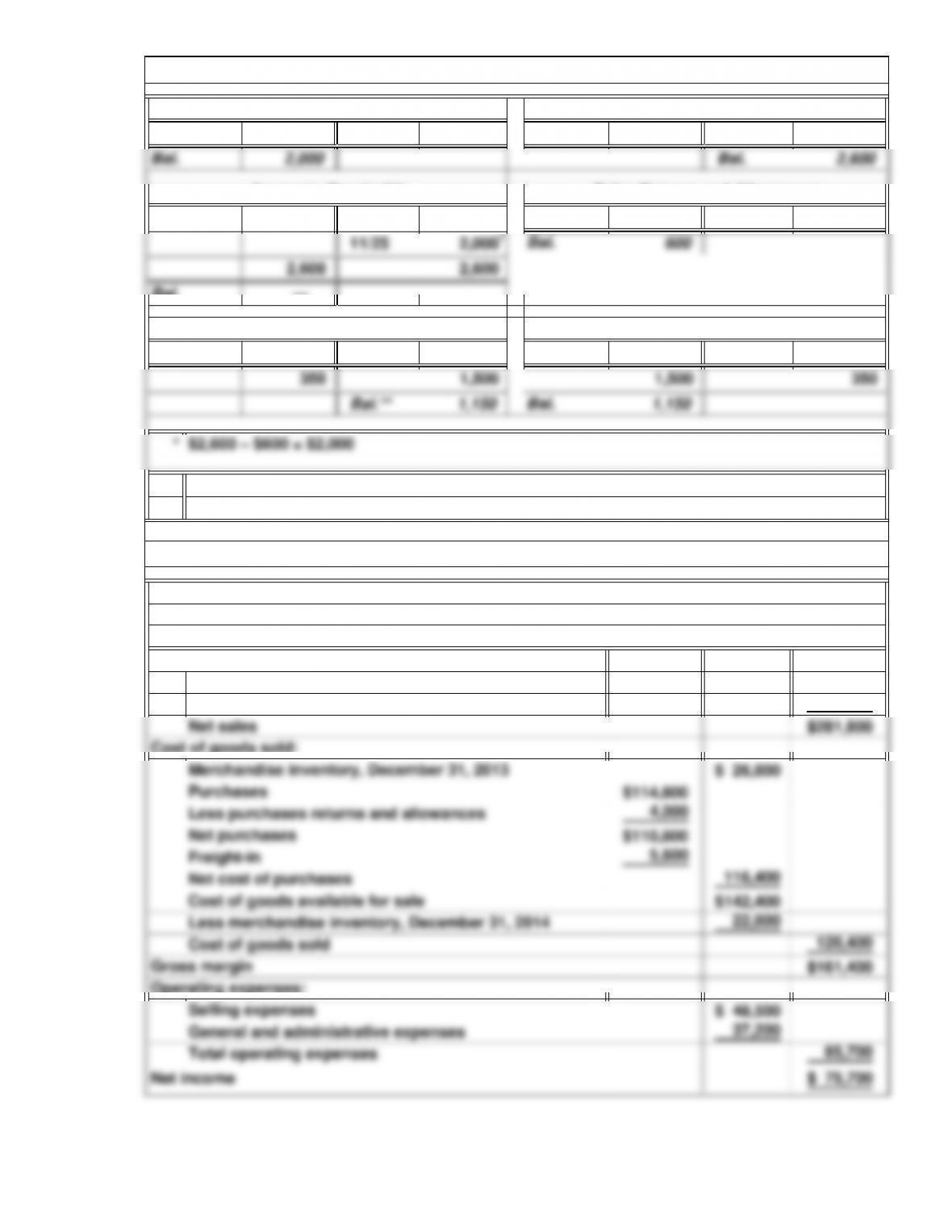

E11A. Preparation of the Income Statement: Periodic Inventory System

Proof General Store

11/25

11/15

Cost of Goods Sold

Sales Returns and Allowances Accounts Receivable

6-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(p) $1,344

76 (a)

b. 270 1,000 5,000 5,000

—

270

**

b.

Bal.

Purchases

a.

e.

Sales returns and allowances

80

Sales

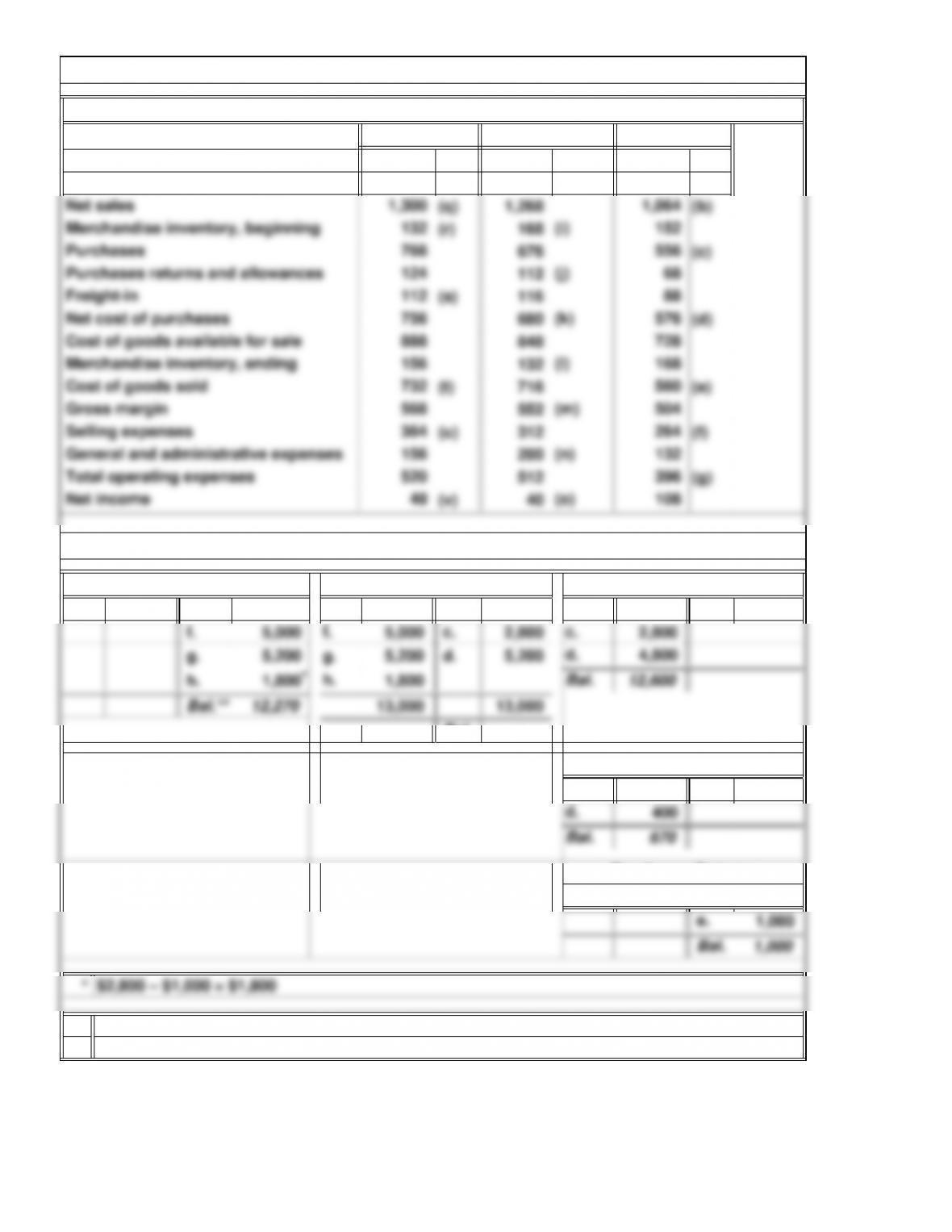

2014 2013 2012

$1,144

Freight-In

Cash

E12A. Merchandising Income Statement: Missing Data, Multiple Years

(h)

$1,396

96

(in thousands)

E13A. Recording Purchases: Periodic Inventory System

The balance of Cash is a credit because there is no data about the beginning balance

and entries have been posted only to the credit side of the account.

Accounts Payable

a.

6-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2,000

11/20

Bal. —

2,600

Resource CD and website.

Note to Instructor: Solutions for Exercises: Set B are provided separately on the Instructor’s

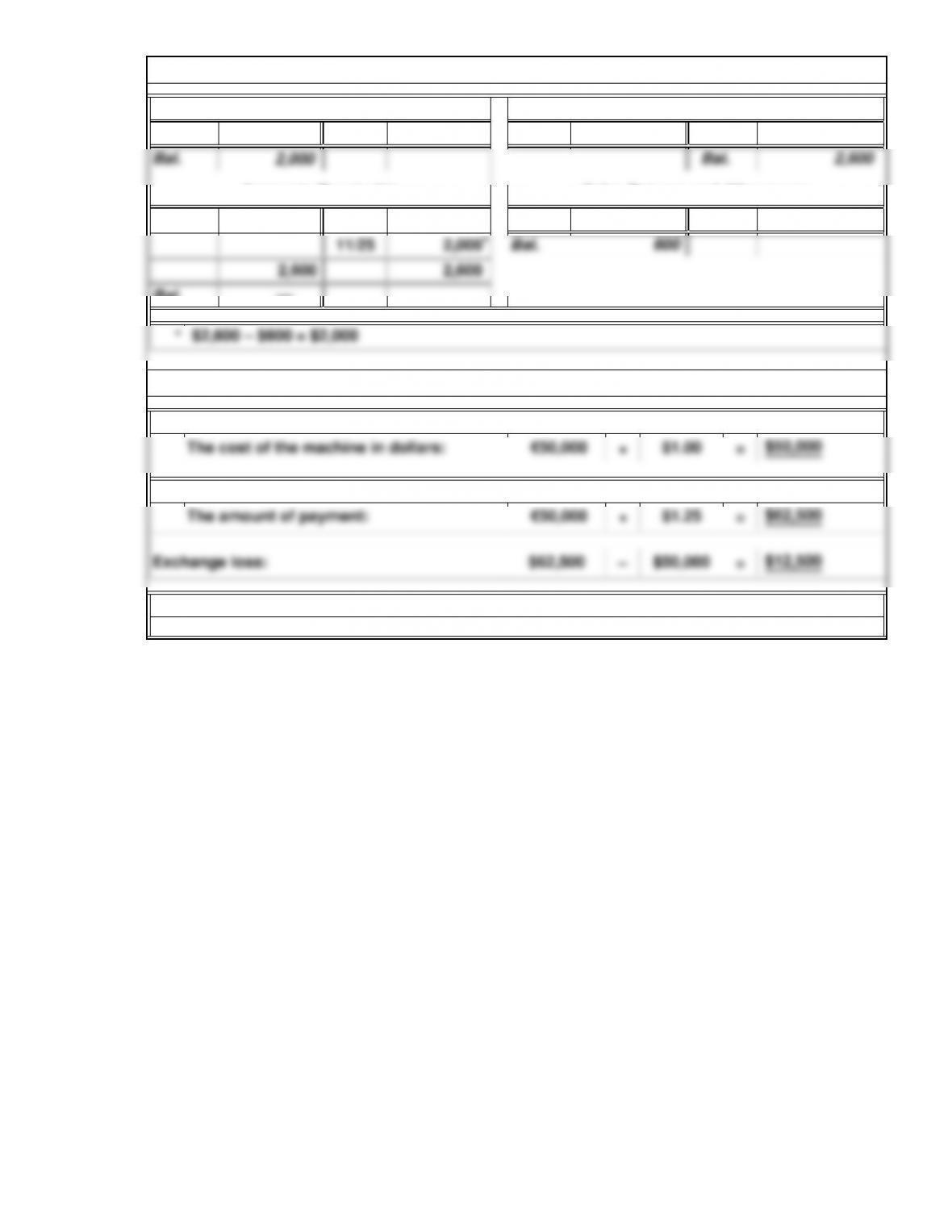

Date of purchase:

Date of payment:

E15A. Foreign Merchandising Transactions

11/15

Sales Returns and Allowances

11/15 600

11/202,600

E14A. Recording Sales: Periodic Inventory System

Sales

Accounts Receivable

600

11/25

Cash

6-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2014 %* 2013 %*

$525,932 100.0% $475,264 100.0%

2.

*Rounded

The primary reason for this increase was that general and administrative expenses

increased from 8.9 percent of net sales to 12.0 percent. Selling expenses actually

sold and the company’s overhead (general and administrative expenses).

P1. Forms of the Income Statement

Problems

Net sales

Matuska Tools Corporation

Income Statements

For the Years Ended July 31, 2014 and 2013

Income from operations decreased from 2013 to 2014 in absolute amount by $44,202

($110,628 – $66,426) and decreased in percentage from 23.3 percent to 12.6 percent

decreased as a percentage of net sales. Management must examine its cost of goods

6-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

$162,000

2,000

$32,625

$12,875

2,400

Net sales:

Sales

Less sales returns and allowances

Store salaries expense

P2. Merchandising Income Statement: Perpetual Inventory System

Operating expenses:

Selling expenses:

General and administrative expenses:

Office salaries expense

Rent expense

Murray’s Furniture Store

Income Statement

For the Year Ended June 30, 2014

6-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2.

the same industry, and covering the same period of time.

statement.

Fourth, when possible, an analysis would also include comparing the ratios above

Third, the net income can be compared with the total assets of the business to com-

Second, the components of gross margin and operating expenses can be examined.

The gross margin is $96,300 or 60.2 percent of net sales; the operating expenses are

$80,865, or 50.5 percent of net sales. Net income can be improved by increasing the

gross margin and/or by decreasing the operating expenses.

sales of $160,000. This is a profit margin of 9.6 percent.

This question is meant to link the income statements in this chapter to the financial

P2. Merchandising Income Statement: Perpetual Inventory System (Concluded)

First, overall, the statement shows net income of $15,435, which was earned on net

6-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

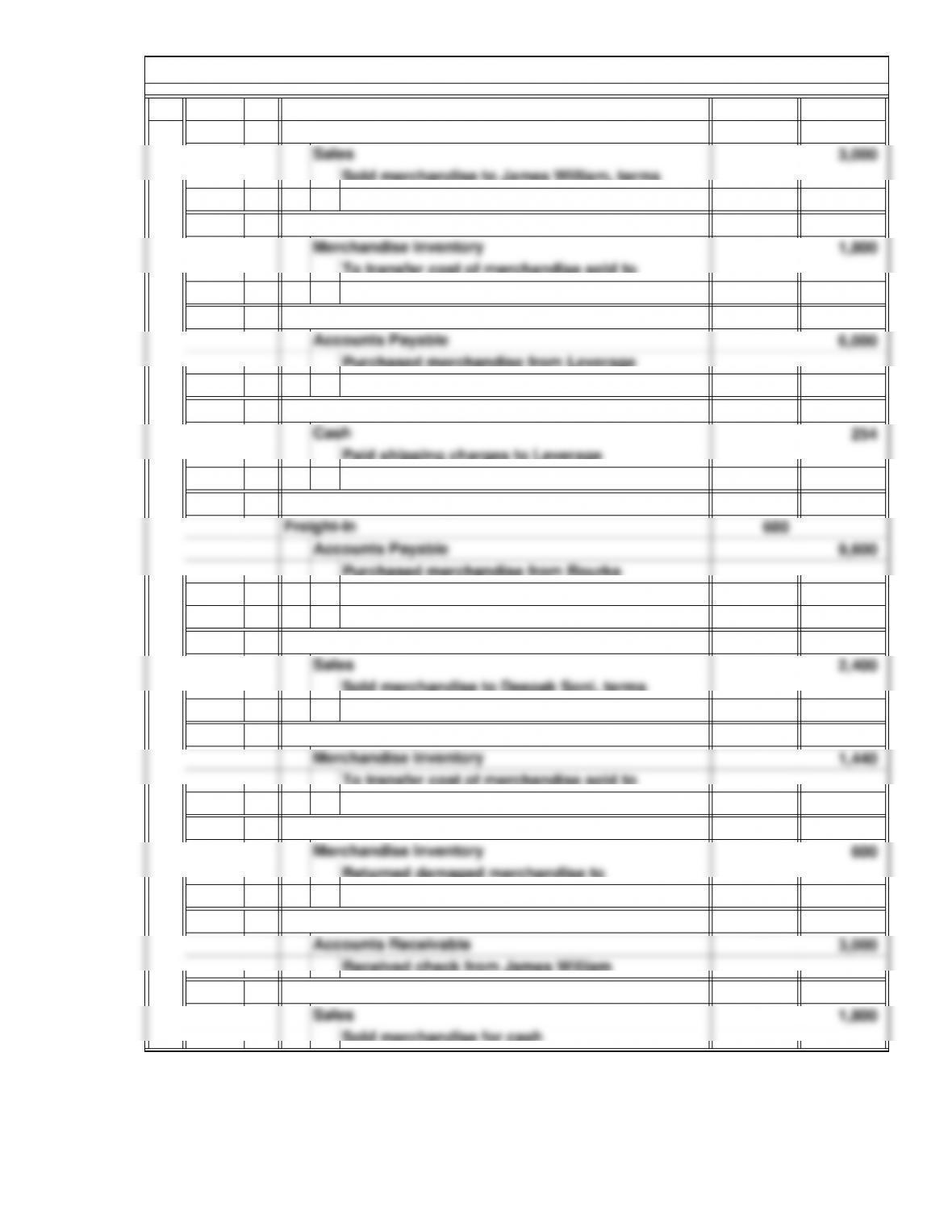

1.

7 3,000

7 1,800

8 6,000

9 254

10 9,000

14 2,400

14 1,440

14 600

17 3,000

19 1,800

Received check from James William

P3. Merchandising Transactions: Perpetual Inventory System

Cash

Company, terms n/30, FOB shipping point;

Purchased merchandise from Rourke

Cash

Sold merchandise for cash

n/30, FOB shipping point

Accounts Receivable

Accounts Payable

Returned damaged merchandise to

Rourke Company paid freight costs

Company, terms n/30, FOB shipping point

Freight-In

Paid shipping charges to Leverage

Company for March 8 purchase

Cost of Goods Sold

Mar.

2014

Accounts Receivable

n/30, FOB shipping point

Sold merchandise to James William, terms

Purchased merchandise from Leverage

Merchandise Inventory

Merchandise Inventory

To transfer cost of merchandise sold to

Cost of Goods Sold account

Sold merchandise to Deepak Soni, terms

Cost of Goods Sold account

Leverage Company for credit

To transfer cost of merchandise sold to

Cost of Goods Sold

6-17

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

19 1,080

20 9,600

21 5,400

24 200

24 120

2.

Cash rebates should not be recorded as revenue because doing so overstates reve-

nues. (Some companies have gotten into trouble for following this practice.) Cash

Mar.

$6,000 – $600 = $5,400

Accepted return from Deepak Soni

Accounts Payable

P3. Merchandising Transactions: Perpetual Inventory System (Concluded)

to Merchandise Inventory account

To transfer cost of merchandise returned

Company for purchase of March 8, net of

Made payment on account to Rourke

Made payment on account to Leverage

2014

Company for purchase of March 10

Merchandise Inventory

return on March 14

Sales Returns and Allowances

Cost of Goods Sold

Accounts Payable

Cost of Goods Sold account

To transfer cost of merchandise sold to

6-18

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.