If the present value of the net cash flows expected from a machine is less than its

purchase price, the investment should not be made.

Intangible assets are subject to a process called depreciation.

Freight-in is treated as an addition in the cost of goods sold section of the income

statement.

There is an impact on the income statement (gain or loss) of a partnership when a

partner withdraws from the business.

Expenses that have been paid for and recorded are called accrued expenses.

The operating cycle is the average days’ inventory on hand minus the average number

of days to collect credit sales.

When a withdrawing partner withdraws assets less than his or her capital balance, the

excess is treated as a bonus to the remaining partners.

One of the general rules of the double-entry system is that total debits must always be

equal to total credits.

An individual can be prosecuted by the SEC for insider trading whether or not that

individual is employed by the company involved.

Under a capital lease, the lessee records both an asset and a liability.

Merchandisers usually end their fiscal year during the peak season.

When all the bonds of an issue mature at the same time, they are called term bonds.

The equity method usually is the most appropriate method for accounting for

investments of more than a 20 percent interest of another company’s stock.

Accrued liabilities often arise as a result of the passage of time.

The Public Company Accounting Oversight Board (PCAOB) was created to determine

the standards that auditors must follow.

Bonding means insuring a company against loss due to employee theft.

A petty cash fund is established for small payments for which writing a check would be

impractical.

The cost of assets acquired for a lump sum should be allocated equally among the

acquired assets.

When the equity method is used to account for an investment in stock, the investor will

report its share of the investee’s annual earnings as income in proportion to how much

the investee distributes in the form of dividends.

Loans to company employees should be included with accounts receivable on the

balance sheet.

Reversing entries are all dated as of the first day of the new accounting period.

Criminal penalties can be imposed on those who prepare fraudulent financial

statements.

Declining profitability and liquidity ratios are indications that a company may not

survive.

The entire cost of developing computer software should be capitalized and amortized

over the software’s useful life.

Despite its advantages, the just-in-time operating environment produces increased

carrying costs for inventory.

A bond agreement is referred to as the bond indenture.

The Withdrawals account bypasses the Income Summary account when it is being

closed.

The lower the interest rate, the higher the present value factor.

Research and development costs normally are capitalized and amortized over the

estimated sales life of the product developed.

In a deferred payment arrangement, interest is charged only if it is stated.

When a loss is closed into the partners’ Capital accounts, Income Summary is debited.

Jeffrey Gray is paid $6 per hour, plus double-time for hours worked on weekends.

During the two-week period ending February 5, Jeffrey worked 70 hours on weekdays

and 8 hours on weekends. Social Security taxes are 6.2 percent, Medicare taxes are 1.45

percent, $65 is withheld for federal taxes, $18 is withheld for state income taxes, and

$24 is withheld for charities. In addition, Jeffrey’s employer must pay Social Security

taxes of 6.2 percent, Medicare taxes of 1.45 percent, federal unemployment taxes of 0.8

percent, and state unemployment taxes of 5.4 percent. Calculate (a) Jeffrey’s gross

earnings, (b) Jeffrey’s net pay, (c) the employer’s payroll taxes expense, and (d) the total

cost of employing Jeffrey for the two-week period. Round all amounts to the nearest

penny.

A retail store has beginning inventory of $30,000, purchases of $220,000, sales of

$200,000, and a normal gross margin of 25 percent. What is estimated inventory based

on these facts and the gross profit method?

A. $50,000

B. $150,000

C. $100,000

D. $200,000

IFRS are important to multinational companies because

A. if they can use IFRS for all their operations, it would simplify the process of

preparing financial statements.

B. it would lower their taxes in each country in which they do business.

C. it would enable them to achieve higher profitability due to the different reporting

standards under IFRS.

D. All of these choices.

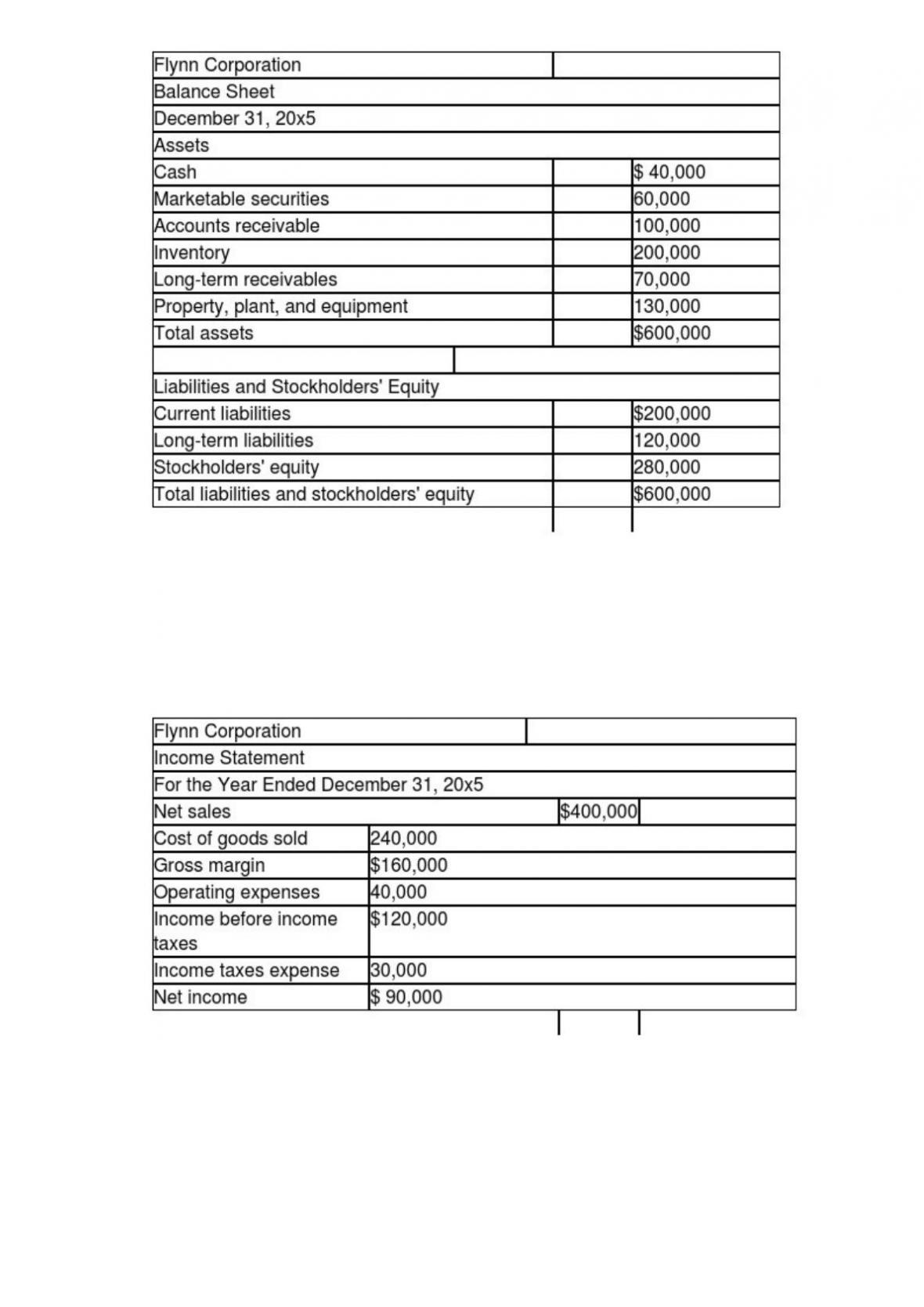

Following are the financial statements for Flynn Corporation for the year ended

December 31, 20×5. Assume that all balance sheet amounts represent both average and

ending figures.

What is the profit margin for this corporation? Round your answer to one decimal place.

A. 22.5 percent

B. 30.0 percent

C. 40.0 percent

D. 53.3 percent

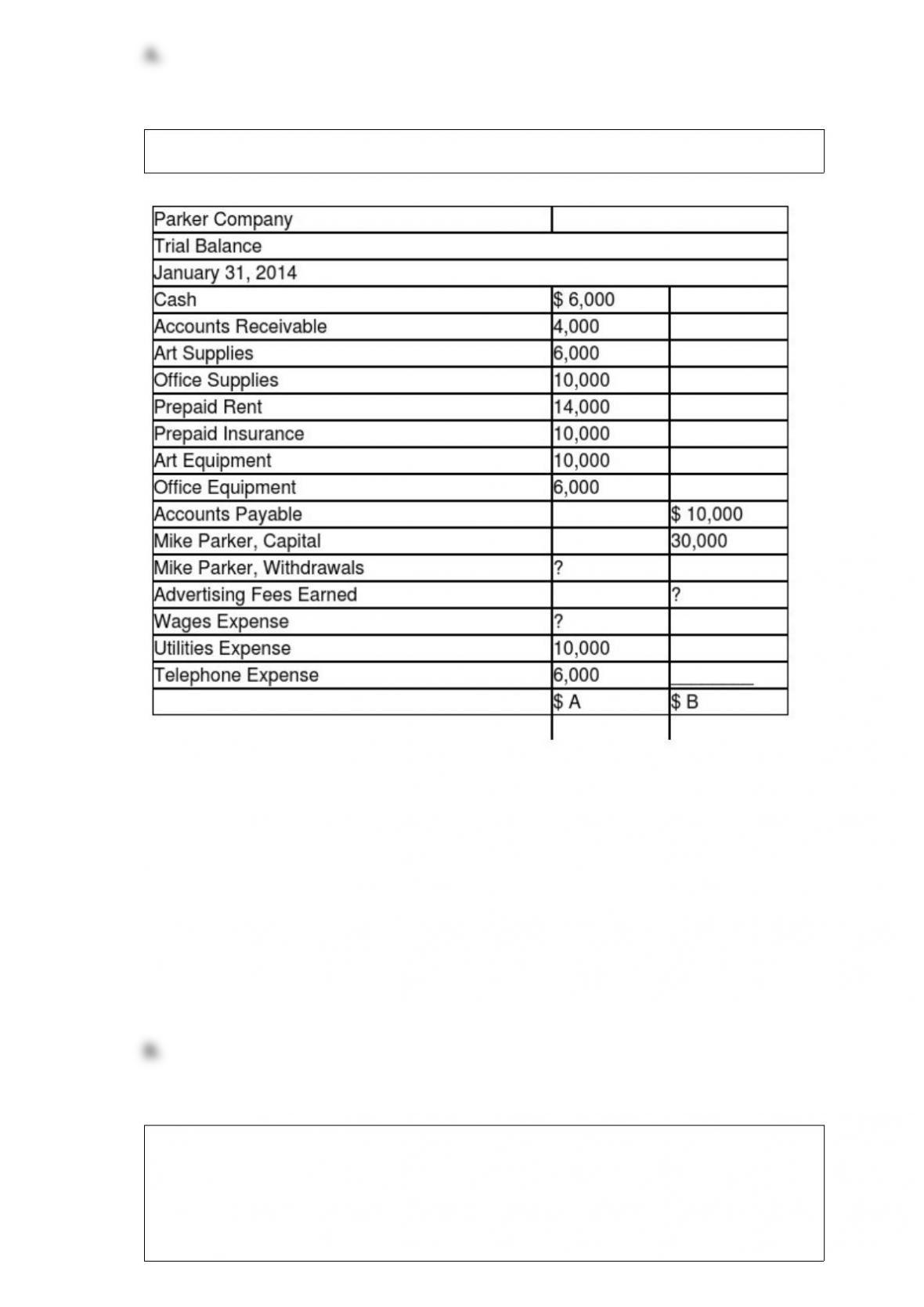

The trial balance for Parker Company is as follows:

If the trial balance showed a balance of $14,000 in the Mike Parker, Withdrawals account

and a balance of $30,000 in the Wages Expense account, what would be the amount of

Advertising Fees Earned for the period?

A. $106,000

B. $86,000

C. $116,000

D. $56,000

Cash flow yield is a

A. liquidity ratio.

B. profitability ratio.

C. long-term solvency ratio.

D. market strength ratio.

A bond issue of $50,000 with a carrying value of $49,000 is converted into $10 par

value common stock at the rate of fifty shares for each $1,000 bond. The entry to be

recorded on the conversion of bonds is:

A. Bonds Payable 50,000

Loss on Retirement of Bonds 1,000

Unamortized Bond Discount 1,000

Common Stock 51,000

B. Bonds Payable 50,000

Common Stock 25,000

Additional Paid-In Capital 25,000

C. Bonds Payable 50,000

Common Stock 25,000

Additional Paid-In Capital 24,000

Unamortized Bond Discount 1,000

D. Bonds Payable 49,000

Which of the following items will not be disclosed on a statement of stockholders’

equity?

A. Conversion of preferred stock into common stock

B. Results of discontinued operations

C. Purchase of treasury stock

D. Declaration of a stock dividend

Lassen Corporation issued ten-year term bonds on January 1, 20×5, with a face value of

$800,000. The face interest rate is 6 percent and interest is payable semi-annually on

June 30 and December 31. The bonds were issued for $690,960 to yield an effective

annual rate of 8 percent. The effective interest method of amortization is to be used. The

entry to be recorded on December 31, 20×5, for the payment of interest (rounded to the

nearest dollar) and the amortization of discount is:

A. Bond Interest Expense 3,638

Unamortized Bond

Discount 3,638

B. Bond Interest Expense 27,784

Unamortized Bond

Discount 3,784

Cash 24,000

C. Bond Interest Expense 27,784

Cash 27,784

D. Bond Interest Expense 24,000

To find the days’ payable,

A. divide 365 by the payables turnover.

B. multiply the payables turnover by 365.

C. divide the payables turnover by 365.

D. subtract 365 from the payables turnover.

A purchase order is sent from a company’s

A. purchasing department to the supplier.

B. requesting department to the supplier.

C. requesting department to its accounting department.

D. treasurer to the supplier.

A company purchases 600 shares of its $100 par value common stock at $110 per share.

It then reissues 100 shares at $114 per share. The entry upon reissue of the stock is

A. Cash 11,400

Treasury Stock-Common 11,000

Paid-in Capital, Treasury Stock 400

B. Cash 11,400

Treasury Stock-Common 11,400

C. Cash 11,400

Treasury Stock-Common 11,000

Gain on Sale of Treasury Stock 400

D. Cash 11,400

Interest on a note receivable may be calculated without knowledge of the

A. principal amount.

B. rate of interest.

C. note’s maturity date.

D. note’s duration.

Use this information pertaining to Tucson Company to answer the following question.

1) The corporation’s Supplies account showed a beginning debit balance of $400 and

supplies purchased of $1,600. There were $600 of supplies on hand at year end.

2)Depreciation on a building being depreciated over 5 years is estimated to be $10,000

per year. The building was purchased at the beginning of the prior year for $50,000.

3)A one-year insurance policy was purchased for $4,800. Five months have passed

since the purchase.

4)Accrued interest on a note receivable amounted to $200.

5)The company received a $3,600 advance payment during the year on services to be

performed. By the end of thE year, one-third of the services had been performed.

Which of the following statements is correct regarding the building?

A. The adjusting entry to record depreciation will include a credit to Accumulated

Depreciation – Building $10,000.

B. The book value of the building at the end of the current year is $30,000.

C. The Accumulated Depreciation – Building account will have a balance of $20,000 at

the end of the current year.

D. All of these choices.

Lease agreements are

A. estimates.

B. commitments.

C. liabilities.

D. contingencies.

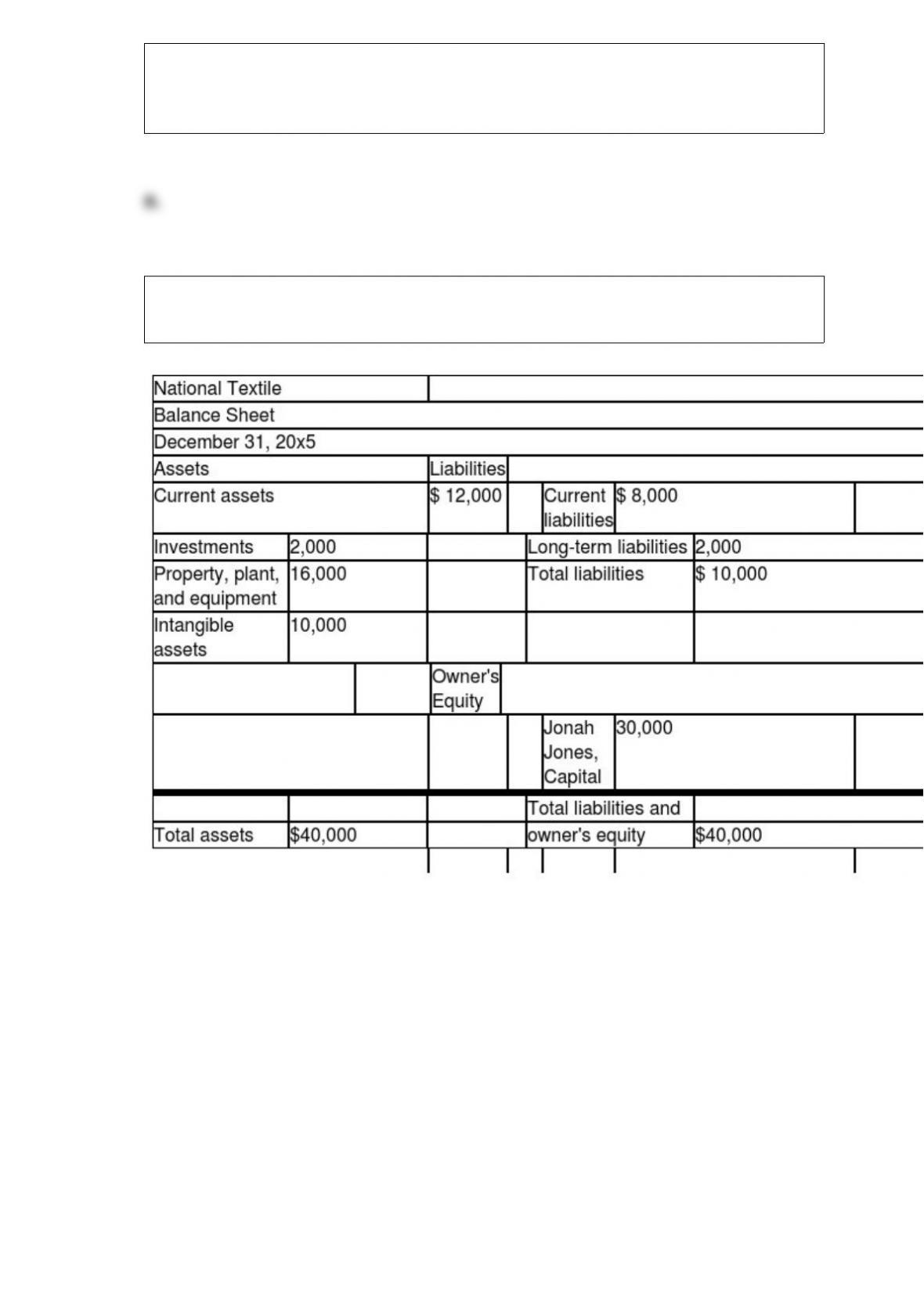

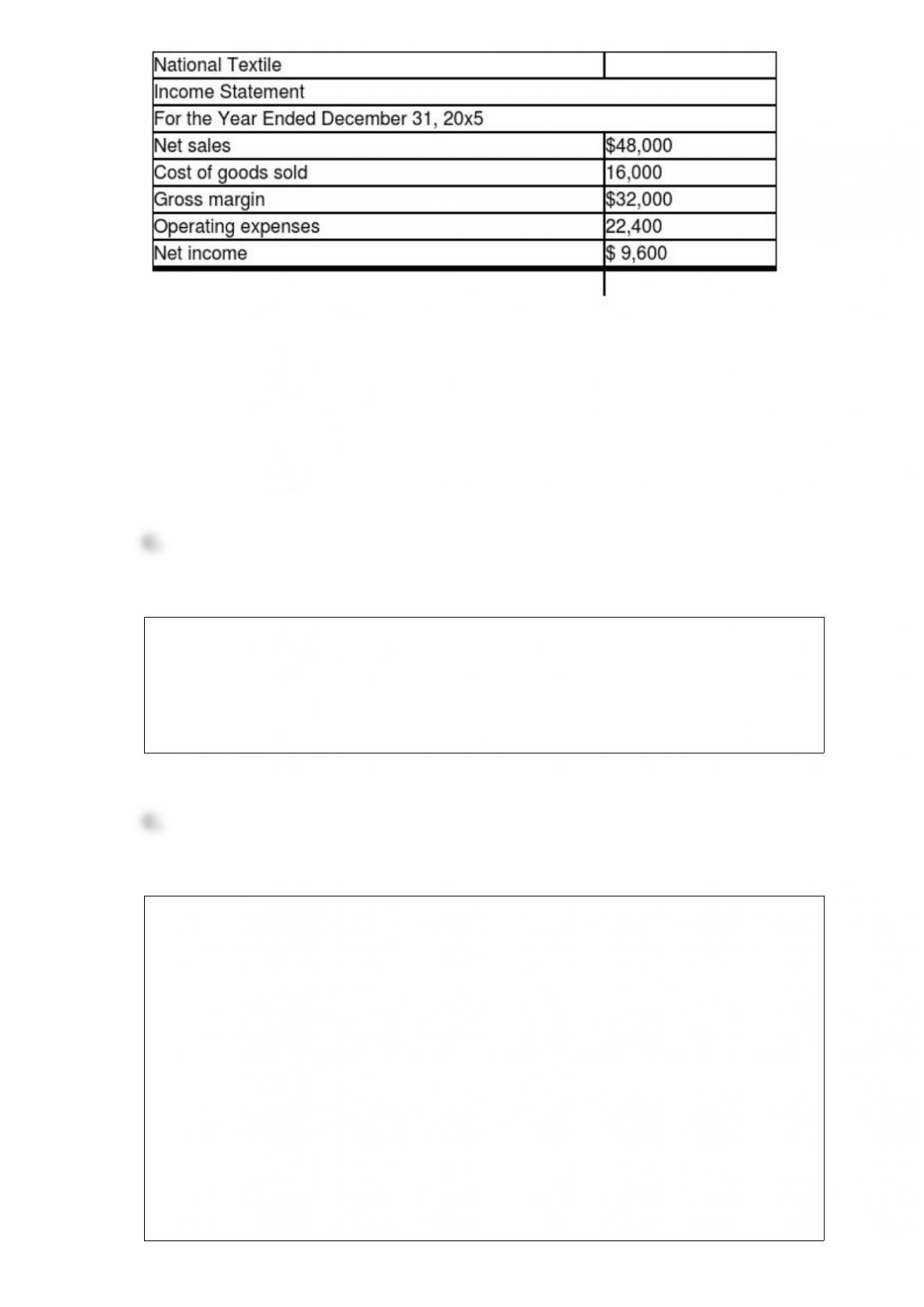

Use this balance sheet and income statement to answer the following question. Use

ending balances whenever average balances are required for computing ratios.

The profit margin for National Textile is

A. 60 percent.

B. 25 percent.

C. 20 percent.

D. 12 percent.

Failure to record depletion for a given accounting period will result in

A. understated total assets.

B. understated total liabilities.

C. overstated net income.

D. overstated total liabilities.

Use the following information to answer the question below.

When Langston Corporation was formed on January 1, 20×5, the corporate charter

provided for 50,000 shares of $20 par value common stock. The following transactions

were among those engaged in by the corporation during its first month of operation:

1) The corporation issued 200 shares of stock to its lawyer in full payment of the $5,000

bill for assisting the company in drawing up its articles of incorporation and filing the

proper papers with the state agency.

2) The company issued 8,000 shares of stock at a price of $25 per share.

3) The company issued 8,000 shares of stock in exchange for equipment that had a fair

market value of $160,000.

The entry to record transaction 3 is:

A. Equipment 160,000

Common Stock 160,000

B. Common Stock 160,000

Equipment 160,000

C. Additional Paid-in Capital 35,000

Equipment 125,000

Common Stock 160,000

D. Cash 160,000

Accelerated depreciation assumes all of the following except that

A. asset benefit increases with each year of use.

B. the asset provides more benefit in the early years.

C. obsolescence makes an asset less valuable in its later years.

D. repair expense is less in the early years than in the later years.

An asset was purchased for $100,000. It had an estimated residual value of $20,000 and

an estimated useful life of ten years. After four years of use, the estimated residual

value is revised to $14,000. Assuming straight-line depreciation, depreciation expense

in year 5 of use would be

A. $7,667.

B. $8,572.

C. $9,000.

D. $14,334.

When an intangible asset becomes worthless,

A. it should remain on the books at its existing carrying value.

B. its remaining carrying value should be written off immediately as a loss.

C. prior years’ accounting records should be adjusted retroactively.

D. its remaining carrying value should be amortized over 20 years.

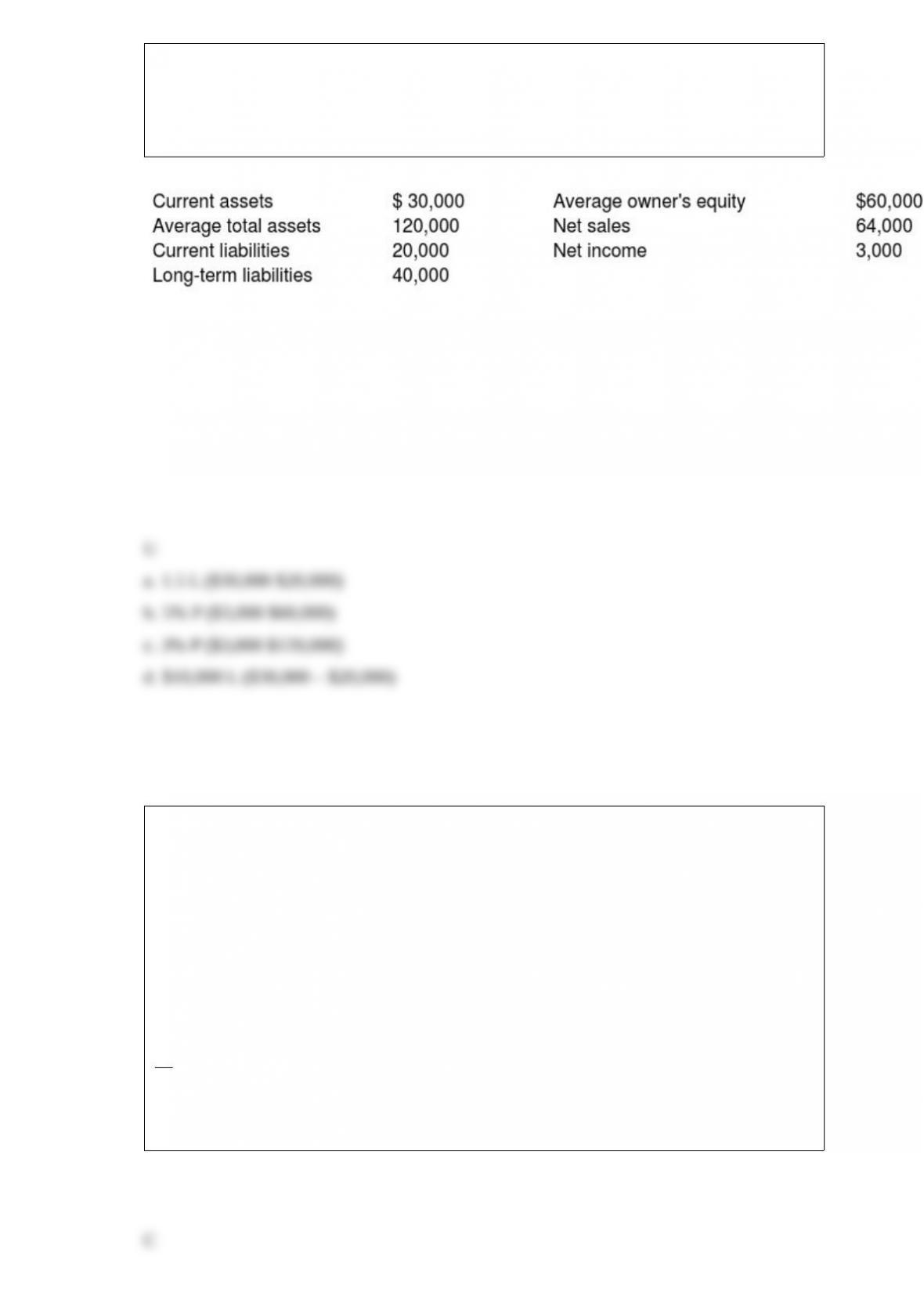

Using the following amounts taken from the balance sheet and income statement of a

business, compute the measures listed below. After each answer, write “L” if it is a

measure of liquidity or “P” if it is a measure of profitability. Round to two decimal

places.

a. Current ratio

b. Return on equity

c. Return on assets

d. Working capital

Sofranko Corporation purchased 8,000 shares of Bussey Corporation common stock for

$80 per share on January 1, 2014. Bussey reported net income of $240,000 for 2014

and paid dividends of $84,000 during 2014. As of December 31, 2014, the market value

of Bussey Corporation common stock was $80 per share. Assuming the shares owned

by Sofranko represent 10 percent of the total outstanding stock of Bussey, the entry to

record the receipt of dividend income in Sofranko Corporation’s books is:

A. Cash 16,000

Dividend Income 16,000

B. Cash 8,000

Dividend Income 8,000

C. Cash 8,400

Dividend Income 8,400

D. Cash 24,000

Dividend Income 24,000

Which of the following is not a component of the operating cycle?

A. Sales to customers

B. Collection of accounts receivable

C. Recognition of depreciation

D. Purchases from suppliers

When a list of customers or subscribers is purchased, its cost is

A. immediately expensed.

B. capitalized as an intangible asset.

C. amortized over a maximum of 5 years.

D. amortized as people on the list move away or pass on.

Which of the following statements is false about a journal entry?

A. All debits are always listed before any credits.

B. It may have more than one debit or credit entry.

C. Credits are always indented.

D. Accounts that are increased are always listed first.

According to generally accepted accounting principles, the proper accounting treatment

for the cost of a trademark that management feels will retain its value indefinitely is to

A. write the cost off immediately.

B. amortize the cost over a reasonable life.

C. amortize the cost over five years.

D. carry the cost as an asset as long as circumstances continue to support an indefinite

life.

Faithful representation is comprised of all of the following except

A. Verifiability

B. Completeness

C. Neutrality

D. Free from error

During the most recent month, Campbell Company began operations with a cash

balance of $0 and made made cash sales of $162,000. During this same time period, the

company paid $64,000 in cash expenses. Additionally, the company purchased supplies

on account, $68,000, made sales on account, $180,000, and paid cash on account

$12,000.

a. If cash at the end of the month totals $148,000, how much cash was received on

account?

b. What is the total amount still to be paid?

c. What is the total amount still to be received?

Willow Corporation has retained earnings of $320,000. It has 5,000 shares of 6 percent,

$100 par value preferred stock outstanding that is callable at 102. The preferred stock is

cumulative, and one year of dividends is in arrears. It also has 10,000 shares of $50 par

value common stock outstanding. Assume all stock is issued at par. The book value of

each share of preferred stock is

A. $168.00.

B. $108.00

C. $163.20.

D. $176.00.

Given equal circumstances, which inventory method probably would be the most time

consuming?

A. Specific identification

B. FIFO

C. Average-cost

D. LIFO

Flint Company produces widgets that cost $30 each and have a 5 percent failure rate. If

500 widgets are sold, the entry to record the estimated product warranty expense would

be

A. Product Warranty Expense 150

Estimated Product Warranty Liability 150

B. Product Warranty Expense 750

Estimated Product Warranty Liability 750

C. Product Warranty Expense 75

Cash 75

D. Estimated Product Warranty Liability 150

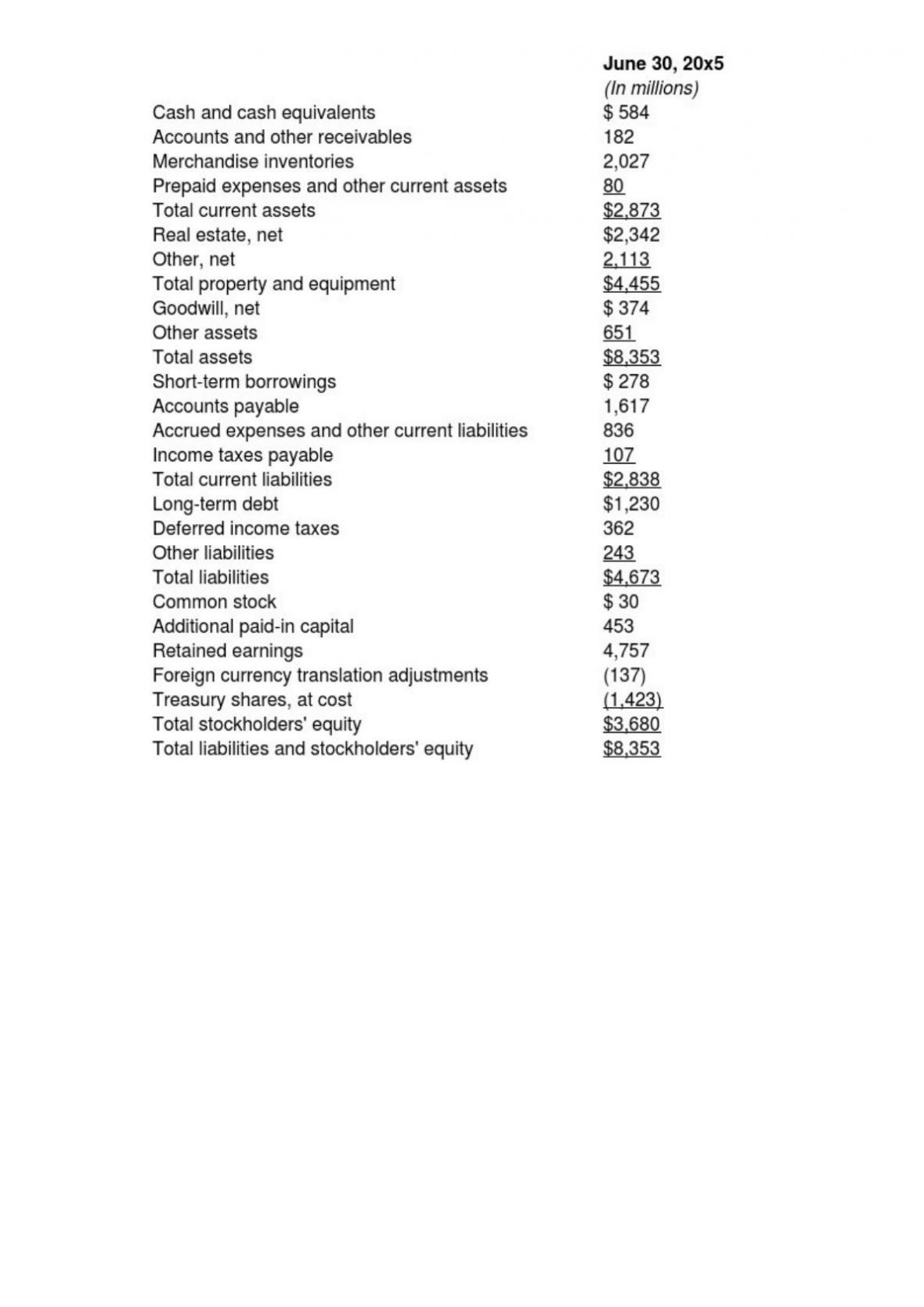

Using the following information from an annual report, prepare a vertical analysis of

the consolidated balance sheet at June 30, 20×5. (Round percentage answers to one

decimal place.)

How is the account Allowance for Uncollectible Accounts presented in the financial

statements, and what purpose does this presentation serve?

What is horizontal analysis, and why is it useful in performing financial performance

measurement?

A less-preferred term for “owner’s equity.

Draw two distinctions between accounting for a stock split and accounting for a stock

dividend.

Include assets, usually long-term, that are not used in normal business operations and

that management does not plan to convert to cash within the next year.

At the beginning of the year, Pullman Company’s assets were $270,000 and its owner’s

equity was $201,000. During the year, assets decreased by $35,000 and liabilities

increased by $10,000. What was owner’s equity at the end of the year?

The balance of the Wages Expense account of Ryan Company, prior to adjustment, was

$95,000.

Novack Company has current assets of $100,000, total assets of $300,000, current

liabilities of $75,000 of which accounts payable are $35,000, and total liabilities of

$150,000.

Use the following accounts and information to prepare, in good form, an income

statement, statement of owner’s equity, and balance sheet for McCollum Enterprises for

the year ended December 31, 2014.

The following information relates to the number of common shares of the Jackson

Corporation:

60,000 Authorized shares 25,000 Unissued shares 3,500 Treasury shares

Calculate the number of outstanding shares from the information given.

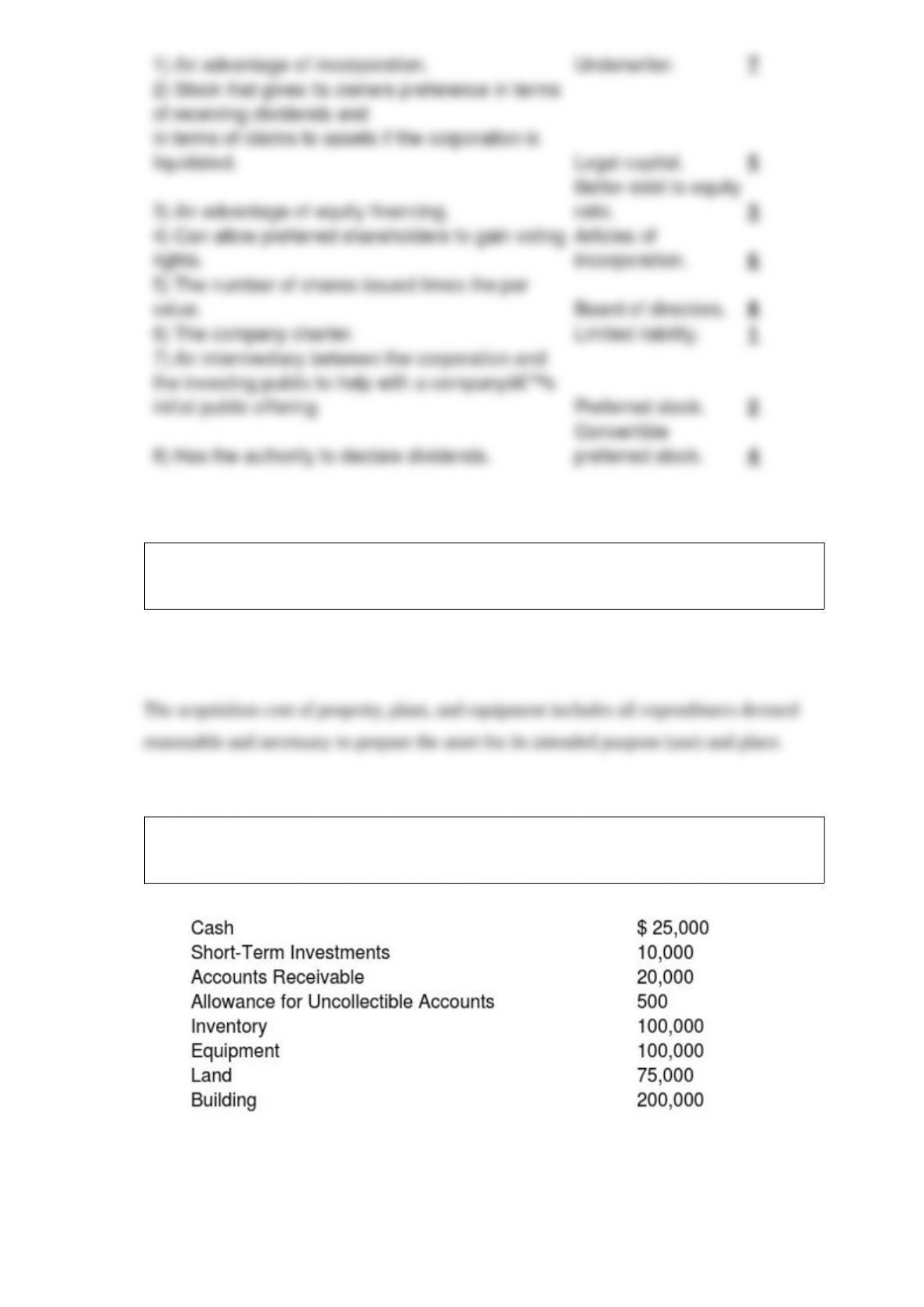

In general, how does one determine whether or not an expenditure should be included

in the acquisition cost of property, plant, and equipment?

A company has the following listed asset accounts. Determine the amount that should

appear on the balance sheet as the total current assets.

How does the statement of owner’s equity relate to the income statement and the

balance sheet?

The following amounts are taken from the balance sheets of Candy Cane Enterprises:

How is it possible for a corporation to have more shares issued than it has outstanding?