DQ1.

DQ2.

CHAPTER 4—Solutions

COMPLETING THE ACCOUNTING CYCLE

Discussion Questions

It is so called because its steps are repeated each accounting period. Step 1 of

Since the Income Summary account is used to accumulate a balance that is sub-

one period follows step 6 of the prior period.

4-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 3.

5,200

500

2,200

800

Short Exercises

SE1. Concepts Underlying Closing Entries

a

b

SE2. Accounting Cycle

To close the Withdrawals account

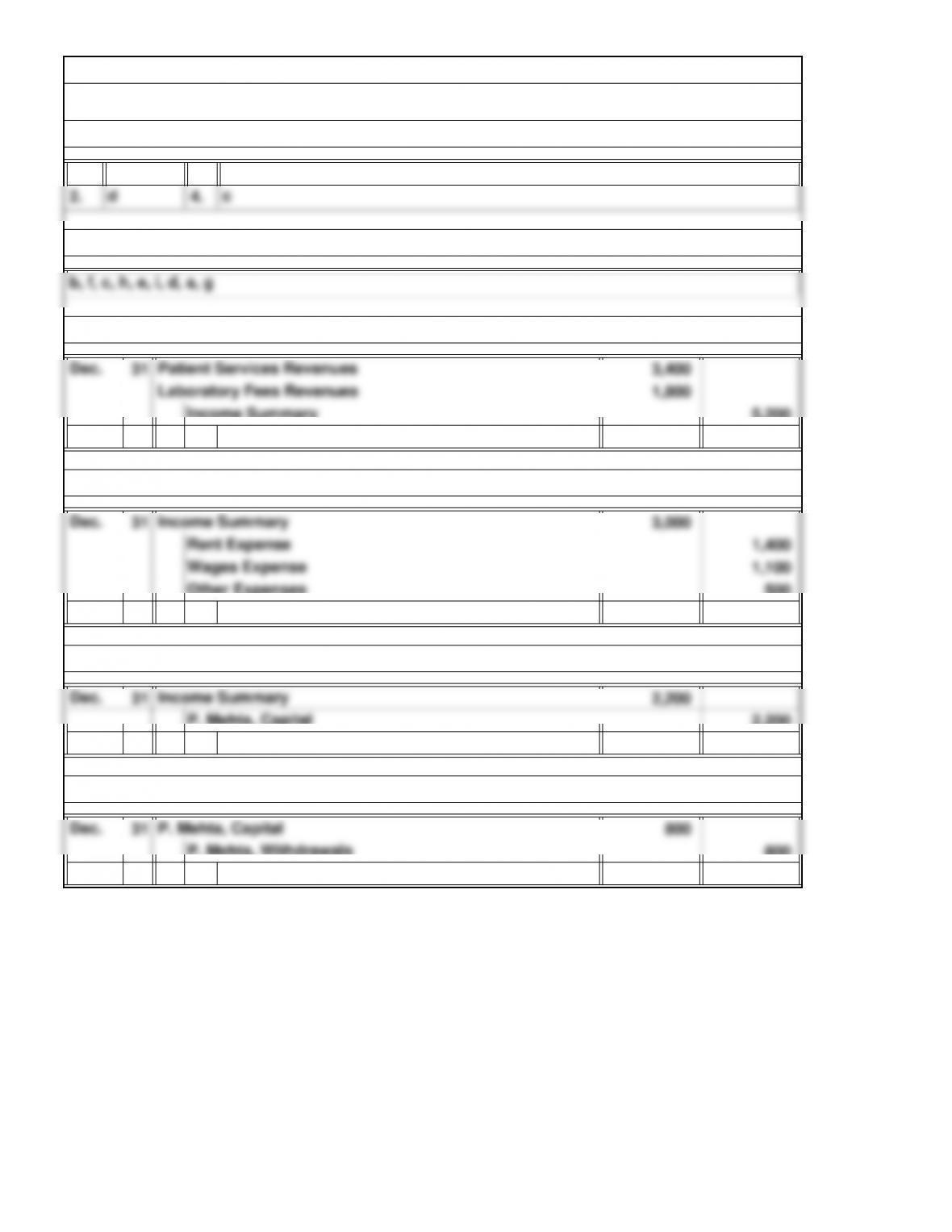

SE6. Closing the Withdrawals Account

P. Mehta, Withdrawals

P. Mehta, Capital

To close the Income Summary account

SE5. Closing the Income Summary Account

Other Expenses

To close the expense accounts

To close the revenue accounts

SE4. Closing Expense Accounts

Income Summary

SE3. Closing Revenue Accounts

4-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

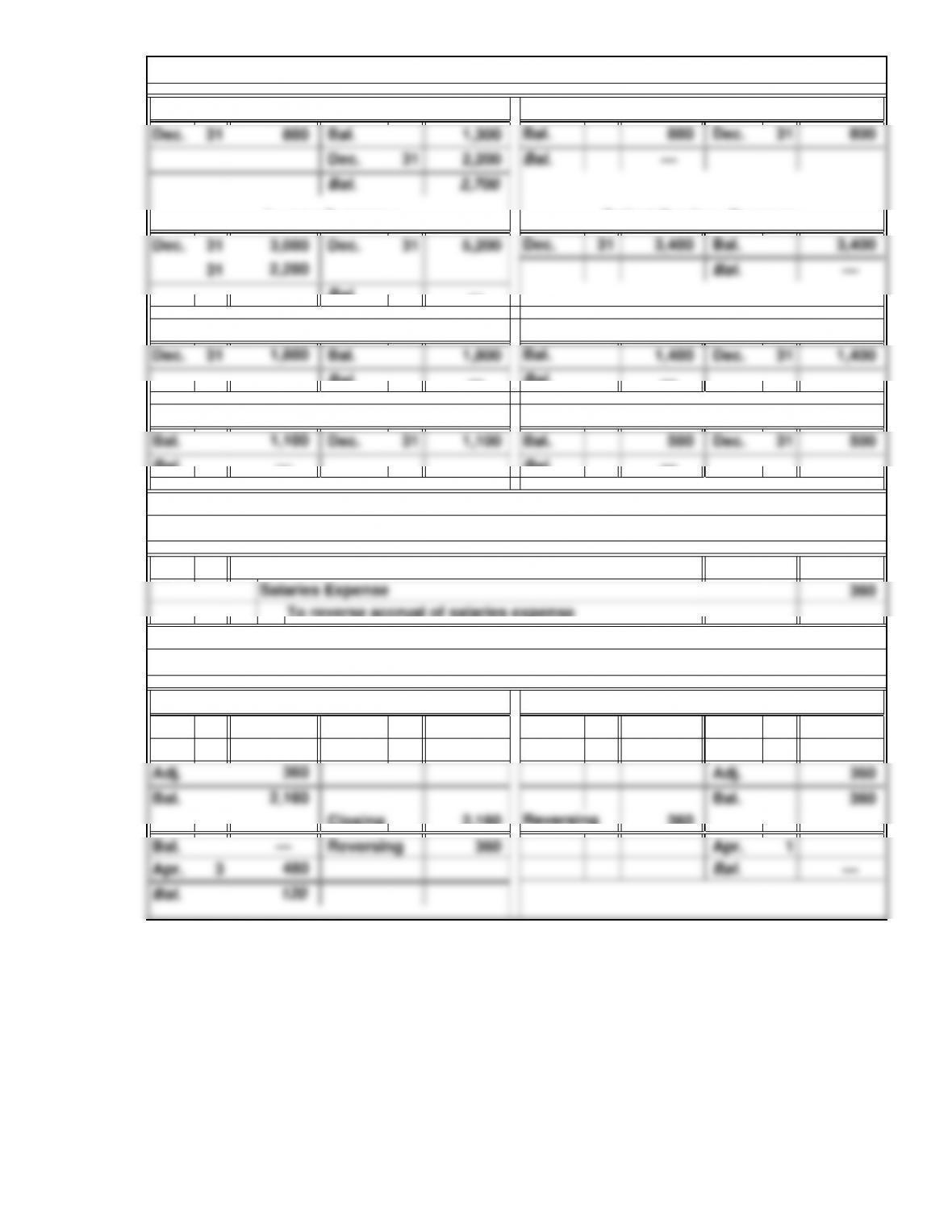

Bal. 800 Dec. 31 800

Bal. —

Bal. ——

Bal. Bal. —

Apr. 1

Mar. 31 Mar. 31

Bal. Bal. —

Bal.

SE9. Effects of Reversing Entries

Salaries Expense

1,800

To reverse accrual of salaries expense

Rent Expense

—

Wages Expense Other Expenses

31Dec. Bal.800

SE7. Posting Closing Entries

360

SE8. Preparation of Reversing Entries

Salaries Payable

P. Mehta, Capital P. Mehta, Withdrawals

1,300

Laboratory Fees Revenues

Salaries Payable

4-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Dec. 31 2,600

1,550

1,050

350

31 35,860

31 26,840

31 9,020

31 7,000

To close the Withdrawals account

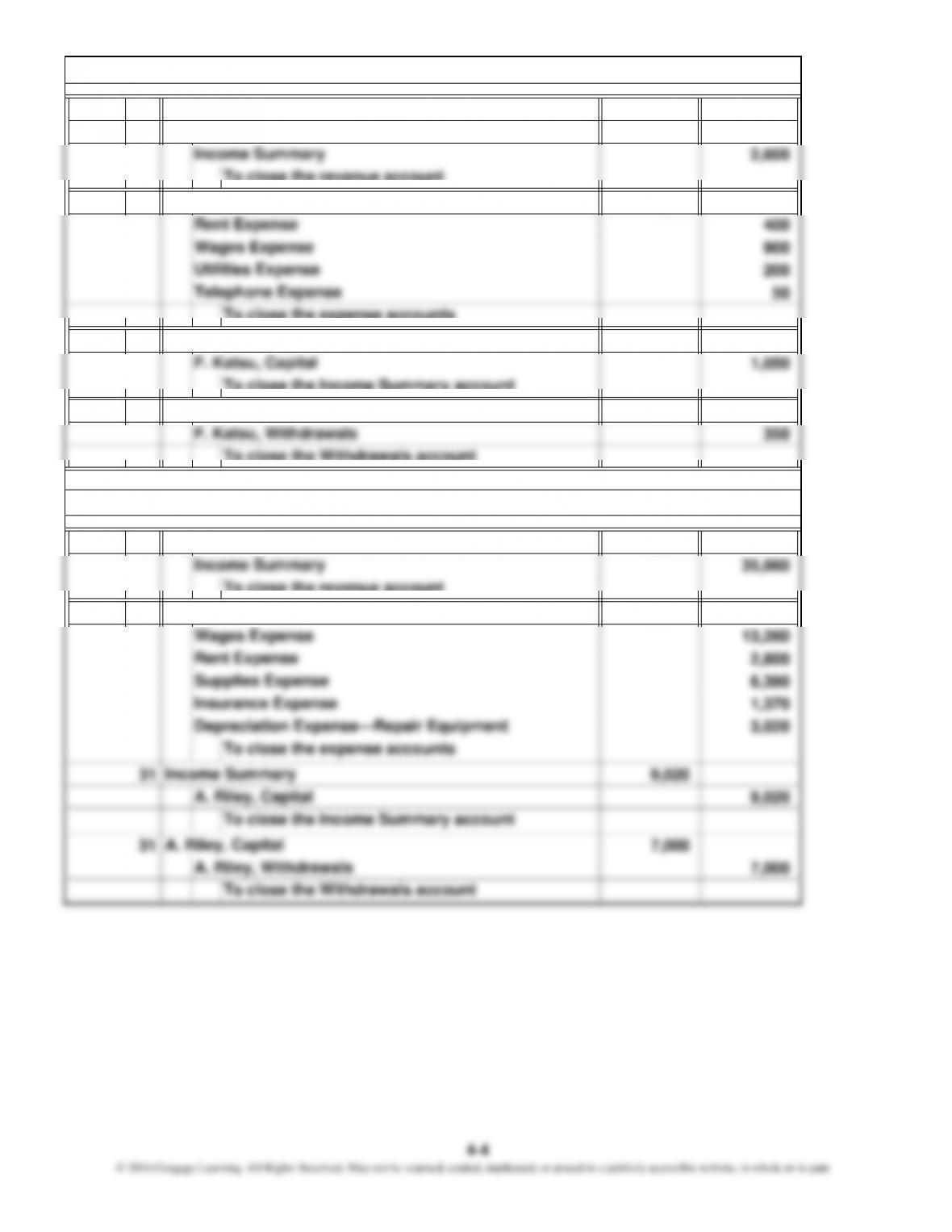

F. Katsu, Capital

Income Summary

To close the Income Summary account

SE10. Preparation of Closing Entries

To close the revenue account

To close the expense accounts

Income Summary

2014

Service Revenue

Income Summary

Income Summary

To close the Income Summary account

A. Riley, Capital

To close the expense accounts

To close the revenue account

Repair Revenue

To close the Withdrawals account

SE11. Preparation of Closing Entries from a Work Sheet

Dec.

4-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

31 25,620

31 15,830

31 9,790

1.

2. 1 1,280

3. 25 6,280

Exercises: Set A

Income Summary

E1A. Preparation of Closing Entries

Dec.

To close the Income Summary account

To close the expense accounts

Commission Revenue

Income Summary

To close the revenue account

in October, $1,280 was expensed in September. As a result of the reversing entry,

the Wages Expense account will show the correct balance, $5,000, after the entries

Oct.

payments applies to a previous period. The adjustment for supplies is a deferral; it

The amount that represents wages expense for October is $5,000. Of the $6,280 paid

accrued wages

Wages ExpenseOct.

Wages Payable

E2A. Reversing Entries

A reversing entry for the adjustment to establish Wages Payable would be helpful

because this accrual will be offset by a payment in the next accounting period. The

reversing entry makes it unnecessary to determine how much of the next period’s

To reverse the adjusting entry for

will not be offset by a subsequent transaction.

To record wages paid on October 25

are posted.

4-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

15,270

15,300

Ken’s Cleaners

Trial Balance

June 30, 2014

Cash

Accounts Receivable

E3A. Preparation of a Trial Balance

4-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Debit Credit Debit Credit Debit Credit Debit Credit

888

14 14 14

4 (a) 2 2 2

8 (d) 6 * 2 2

16 16 16

2 (b) 2 4 4

888

6 (e) 4 2 2

24 24 24

12 12 12

46 (e) 4 50 50

444

20 (c) 2 22 22

86 86

(a) 2 2 2

(b) 2 2 2

(c) 2 2 2

(d) 6 * 6 6

16 16 90 90 36 50 54 40

14 14

50 50 54 54

Trial Balance

Office Equipment

Work Sheet

Adjustments

Credit

SheetStatement

Trial Balance

Debit

Income Balance

Office Equipment

Adjusted

For the Month Ended March 31, 2014

4-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$26,000

19,000

1. 2014

(a) June 30 480

(b) 30 1,260

(c) 30 2,800

(d) 30 4,400

(e) 30 480

2.

2014

(e) July 1 1,440

To reverse the adjusting entry for

accrued salaries from the previous

period

Salaries Payable

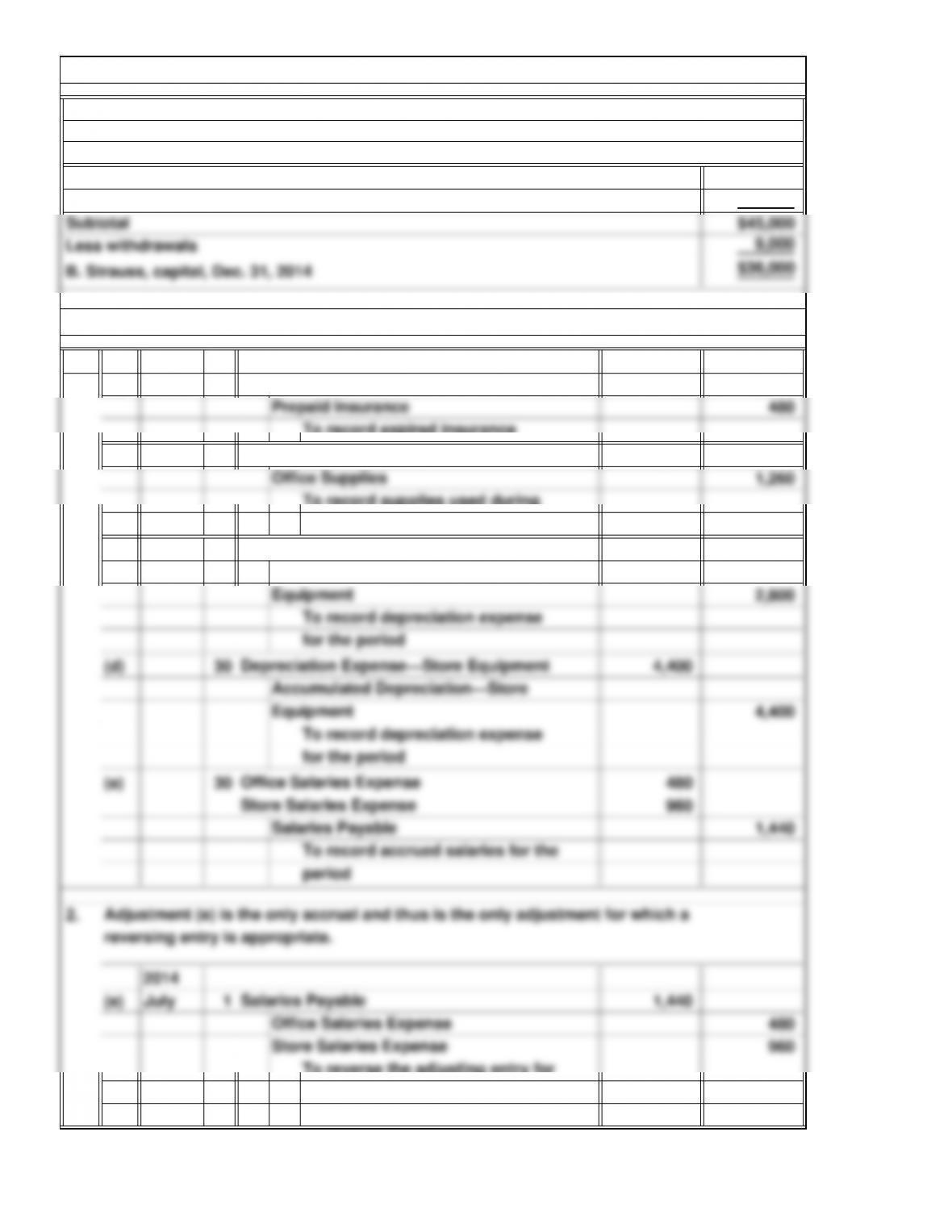

E6A. Preparation of Adjusting and Reversing Entries from Work Sheet Columns

Depreciation Expense—Store Equipment

Accumulated Depreciation—Office

To record depreciation expense

Insurance Expense

To record expired insurance

Depreciation Expense—Office Equipment

Accumulated Depreciation—Store

for the period

Office Supplies Expense

To record supplies used during

the period

period

Office Salaries Expense

for the period

To record accrued salaries for the

To record depreciation expense

Adjustment (e) is the only accrual and thus is the only adjustment for which a

reversing entry is appropriate.

Strauss’s Hair Salon

Statement of Owner’s Equity

For the Year Ended December 31, 2014

B. Strauss, capital, Dec. 31, 2013

Net income

E5A. Preparation of Statement of Owner’s Equity

4-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.