DQ1.

DQ8.

TRANSACTIONS

CHAPTER 2—Solutions

ANALYZING AND RECORDING BUSINESS

Discussion Questions

All equipment needs normal repairs. These are considered an ongoing cost of busi-

such as a major overhaul that is done every five years, the expenditure will benefit

ness and, thus, are expenses. However, it may be argued that if the repair is major,

ments (e.g., unused equipment), or get a loan from a bank.

To maintain liquidity it can seek more time from creditors, sell long-term invest-

2-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

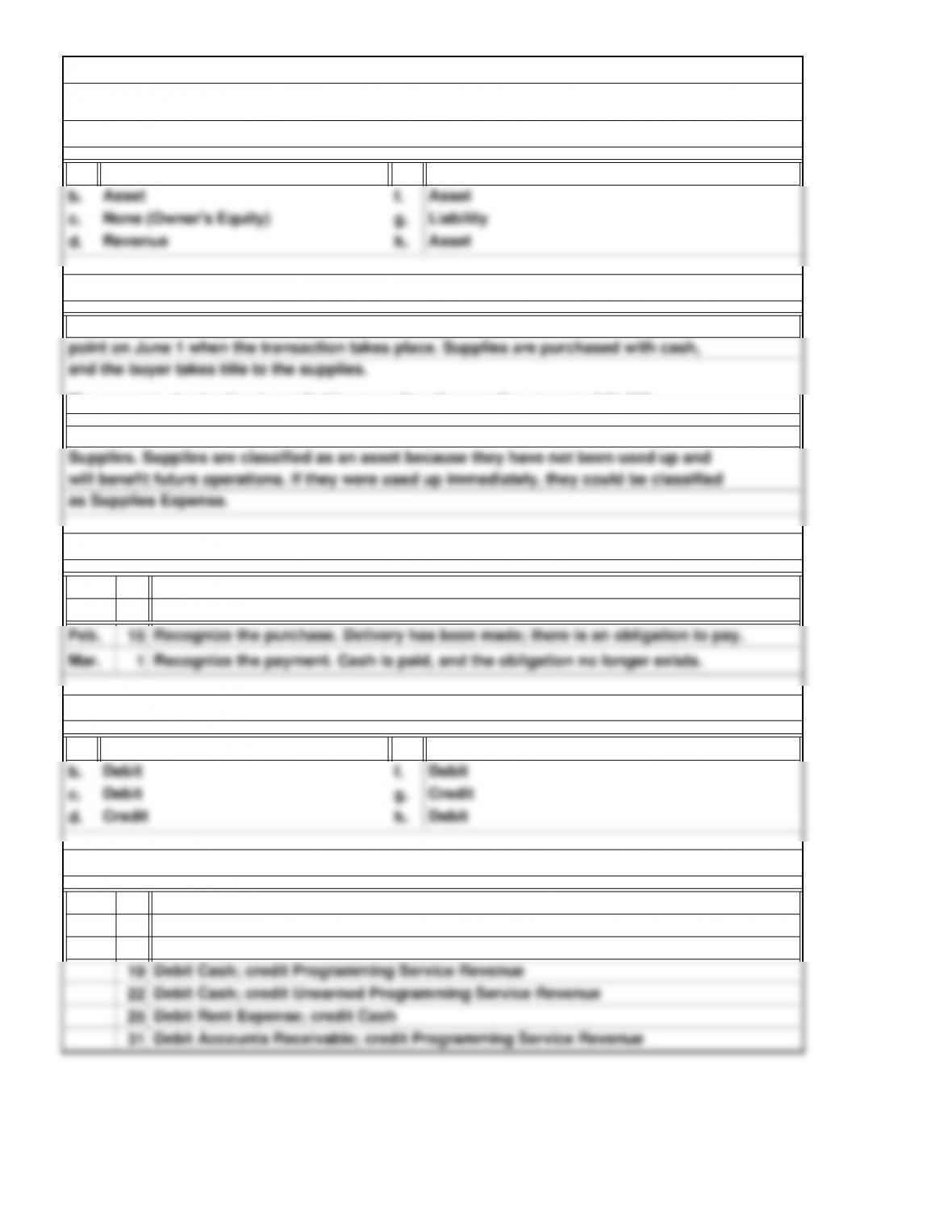

a. e.

b. f.

c. g.

d. h.

10

a. e.

2

5

7

Debit Cash; credit S. Michael, Capital

Debit Office Equipment; credit Cash

Debit Supplies; credit Accounts Payable

SE5. Transaction Analysis

May

The classification concept is applied by reducing the asset Cash and increasing the asset

The concept of valuation is applied by recording the supplies at cost of $1,000.

will benefit future operations. If they were used up immediately, they could be classified

as Supplies Expense.

Revenue

Asset

None (Owner’s Equity) Liability

Asset

Asset

point on June 1 when the transaction takes place. Supplies are purchased with cash,

and the buyer takes title to the supplies.

Expense

SE2. Recognition, Valuation, and Classification

Liability

The concept of recognition is applied by recording the transaction at the recognition

SE4. Normal Balances

Credit Debit

SE1. Classification of Accounts

Do not recognize because an order is not a complete transaction. There is no

Short Exercises

obligation on the part of either party at this point.

SE3. Recognition

Jan.

2-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

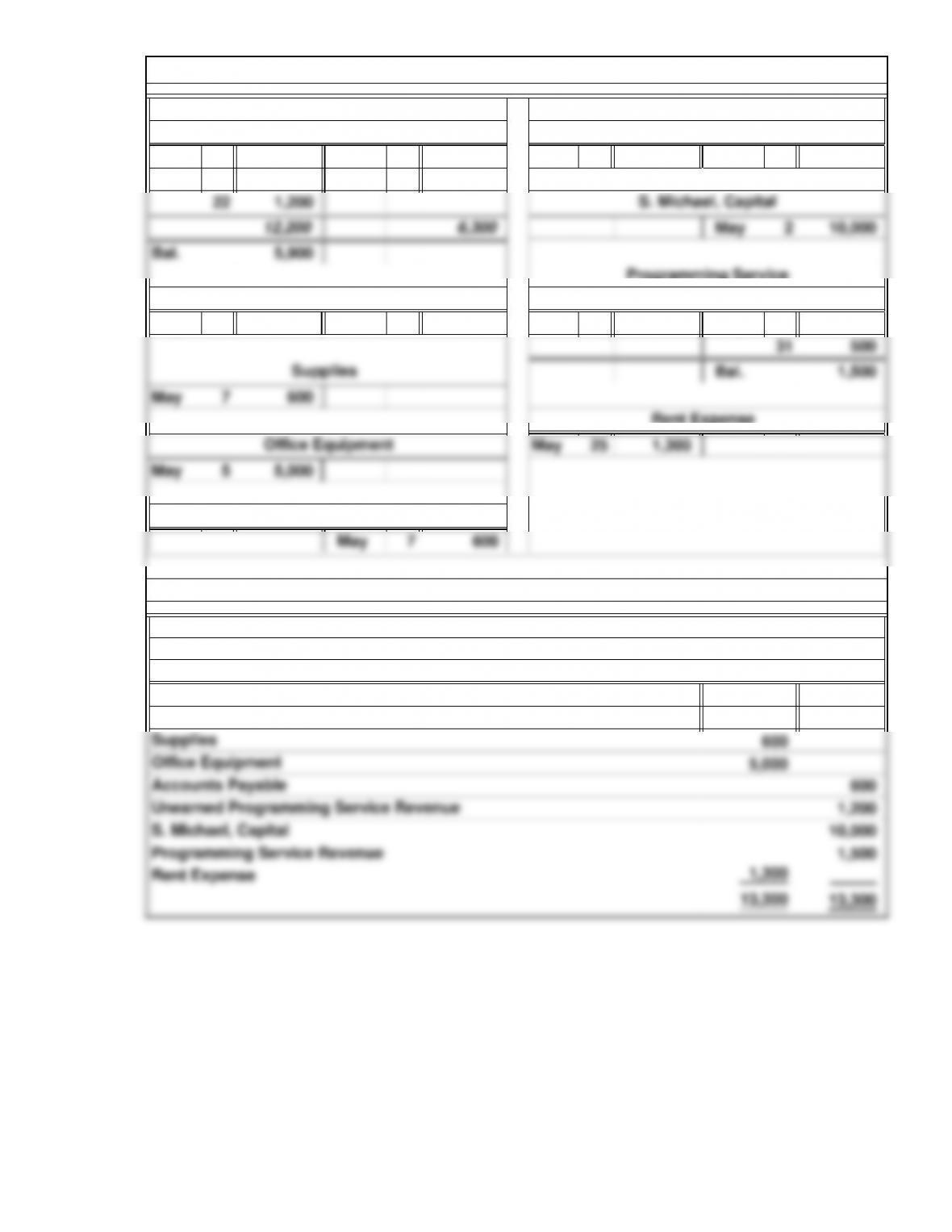

May 2 10,000 May 5 5,000 May 22 1,200

19 1,000 25 1,300

May 31 500 May 19 1,000

Cash

Accounts Receivable

Programming Service

SE6. Recording Transactions in T Accounts

Revenue

Service Revenue

Unearned Programming

2-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Page 4

Post.

Ref. Debit Credit

Sept. 6 3,800

3,800

Ref. Debit Debit Credit

Sept. 16 J4 1,800 1,800

Ref. Debit Debit Credit

Ref. Debit Debit Credit

Sept. 6 J4 3,800

$ 7,700

2,500

600

DescriptionDate

Credit

3,800

Accounts Receivable

Service Revenue

Billed customer for services performed

Credit

Accounts Receivable

SE9. Posting to the Ledger Accounts

SE8. Recording Transactions in the General Journal

Received cash on account from

customer billed on Sept. 6

General Journal

Michael’s Programming Service

Trial Balance

September 30, 2014

Cash

general journal in SE8.

Account No. 113

Account No. 411

Accounts Receivable

Supplies

Credit

Note: At this point, the account numbers would also be posted to the accounts in the

Cash Account No. 111

Balance

Item

Date

Post.

Date

Item

Balance

Post. Balance

Post.

Service Revenue

Date Item

2-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Post.

Ref. Debit Credit

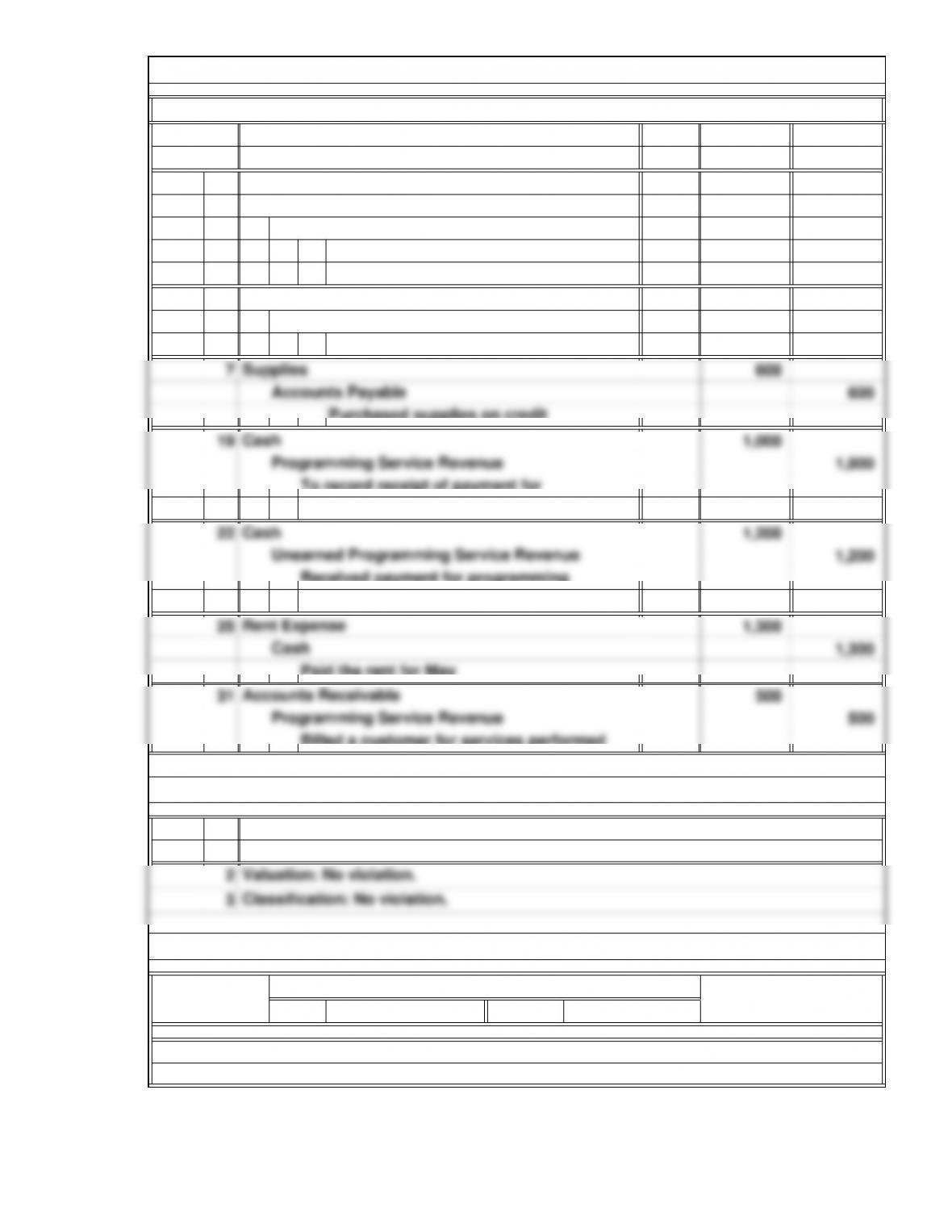

2014

May 2 10,000

10,000

5 5,000

5,000

1

1/4

SE12. Timing and Cash Flows

Recognition: A violation because the revenue from the service was earned in

the prior year.

business

Office Equipment

Cash

Purchased a computer for cash

Description

Cash

S. Michael Capital

1/2

2,400

Cash

1,400

actions of Jan. 8 and 9 will not impact cash until later when the cash is received or paid.

The transactions of Jan. 2 and 4 have an immediate impact on cash, whereas the trans-

SE11. Identifying Ethical Transactions

Billed a customer for services performed

SE10. Recording Transactions in the General Journal

Date

General Journal

Owner invested cash to start the

2-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Jan. 15

Feb. 2

Mar. 29

June 10

July 6

=+

=

E2A. T Accounts, Normal Balance, and the Accounting Equation

3,450

Exercises: Set A

E1A. Recognition

+–

+Owner’s Equity

Expenses

T. Captain,

Withdrawals

Cash Accounts

Payable

$2,250

T. Captain,

Withdrawals Service

Revenue Rent

Expense

LiabilitiesAssets

–

T. Captain,

Capital

=

Revenues

T. Captain,

Capital

2-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

D. Minimus, D. Minimus,

Item Asset Liability Capital Withdrawals Revenue Expense Debit Credit

a. x x

b. x x

c. x x

d. x x

e. x x

f. x x

g. x x

h. x x

i. x x

j. xx

k. x x

l. xx

m. x x

n. x x

o. x x

p. x x

q. x x

r. x x

s. x x

t. x x

u. x x

v. x x

w. x x

x. x x

Type of Account

E3A. Classification of Accounts

Owner’s Equity Normal Balance

2-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

a.

e.

Debit Credit

a. 51

b. 12

i.

Ordered equipment.

No entry

Paid for supplies purchased on credit last month.

Received cash from customers billed last month.

E4A. Transaction Analysis

The asset account Cash was increased. Increases in assets are recorded by debits.

The liability Accounts Payable was decreased. Decreases in liabilities are recorded

E5A. Transaction Analysis

2-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.