$40,000

$40,000

E7A. Admission of a New Partner: Recording a Bonus

Total bonus

*Distribution of bonus from original partners:

*Distribution of bonus to original partners:

Total bonus

12-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

*Distribution of bonus from remaining partners:

E8A. Withdrawal of a Partner

$80,000

Total bonus

12-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

Winner, Perry, Gain (or

Other Capital Capital Loss) from

$ 240,000 (320,000) $(80,000)

$ 240,000 —$ 20,000 $ 180,000 $ 120,000 $(80,000)

$ 220,000 —$ 180,000 $ 120,000 $(80,000)

(60,000) (20,000) 80,000

$ 220,000 $ 120,000 $ 100,000 —

— — —

* $80,000 × 0.75 )

$80,000 × 0.25 )

20,000

Winner (

Sale of Assets

E9A. Partnership Liquidation

Distribution of Gain (or Loss) from Realization

Explanation

Perry (

December 31, 2014

Distribution of Cash to Partners

Winner and Perry

Statement of Liquidation

Payment of Liabilities

Balance, December 31, 2014

*

12-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Sale of assets

Payment of liabilities

Distribution of the loss

Distribution of cash to the partners

E9A. Partnership Liquidation (Concluded)

12-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Abby, Anna, Anita, Gain (or

Other Capital Capital Capital Loss) from

$ 520,000 (960,000) $(440,000)

$ 520,000 —$ 320,000 $ 280,000 $ 80,000 $ 280,000 $(440,000)

$ 200,000 —$ 280,000 $ 80,000 $ 280,000 $(440,000)

(264,000) (88,000) (88,000) 440,000

$ 200,000 $ 16,000 $ (8,000) $ 192,000 —

(6,000) 8,000 (2,000)

$ 200,000 $ 10,000 —$ 190,000

Abby, Anna, and Anita

Statement of Liquidation

July 1, 2014

12-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2. a.

2013 2014

b.

c.

2013 2014

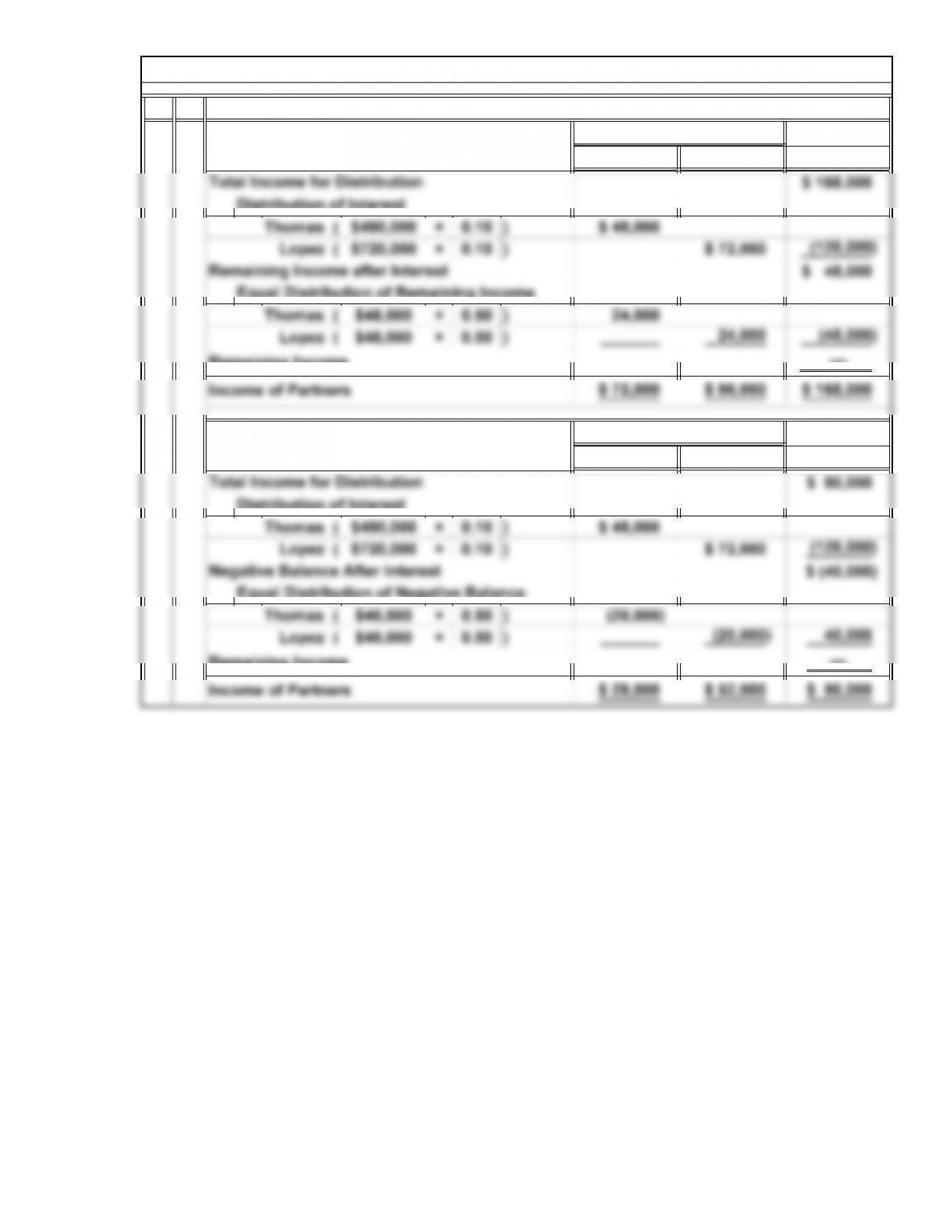

Thomas

be shared equally. This answer is identical to (a).

Thomas

Income shared on the basis of the partners’ original investments.

Because the partners failed to agree on an income-sharing arrangement, income must

Income shared equally

Initial investments of Edi Thomas and

George Lopez

P1. Partnership Formation and Distribution of Income

Problems

12-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

d.

Income of Partner

Thomas Lopez Distributed

—

Income of Partner

Thomas Lopez Distributed

—

2013 computation:

Interest on investments; remainder shared equally.

Remaining Income

2014 computation:

Remaining Income

Income

Income

P1. Partnership Formation and Distribution of Income (Continued)

12-17

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

e.

Thomas Lopez Distributed

—

Thomas Lopez Distributed

Equal Distribution of Negative Balance

—

Income

Income

Income of Partner

Income of Partner

P1. Partnership Formation and Distribution of Income (Continued)

Remaining Income

2013 computation:

2014 computation:

Salaries allowed; remainder shared equally.

Remaining Income

12-18

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

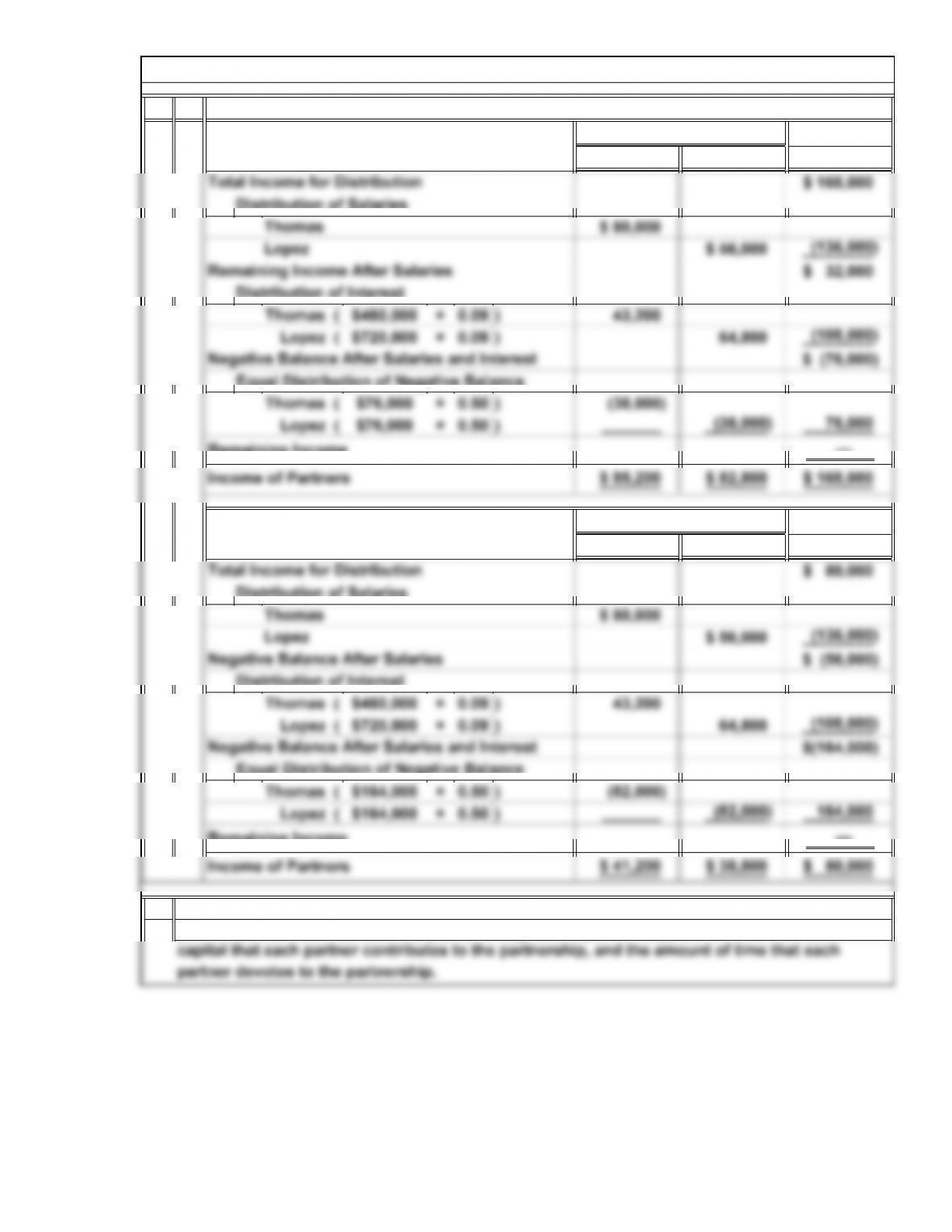

f.

Income of Partner

Thomas Lopez Distributed

Equal Distribution of Negative Balance

—

Income of Partner

Thomas Lopez Distributed

—

3.

Interest and salaries allowed; remainder shared equally.

2013 computation:

2014 computation:

Remaining Income

P1. Partnership Formation and Distribution of Income (Concluded)

Income

Income

Some factors that should be considered when developing a plan of income sharing among

partners are the talents that each partner brings to the partnership, the relative amounts of

Remaining Income

12-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

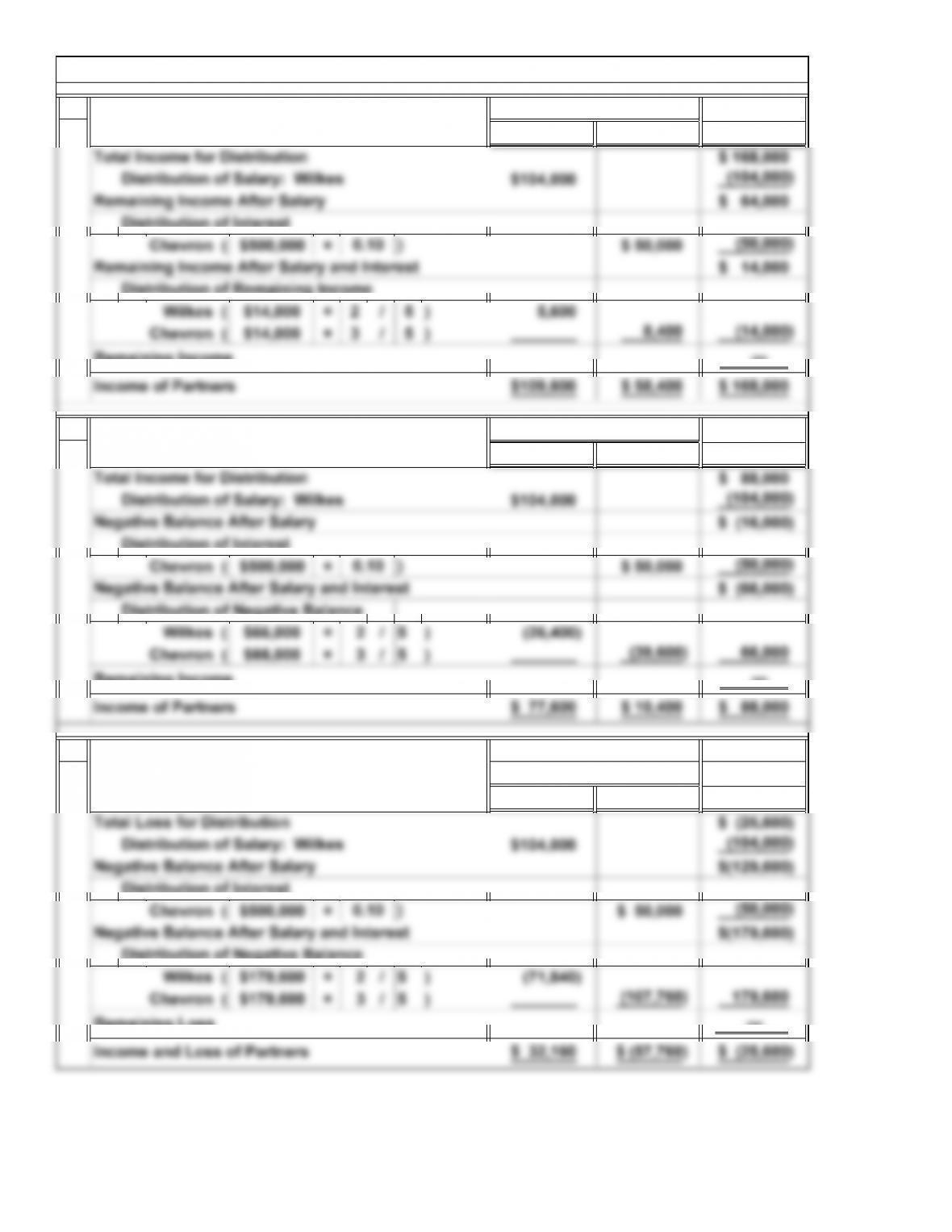

1.

Wilkes Chevron Distributed

—

2.

Wilkes Chevron Distributed

Distribution of Negative Balance

—

3.

Wilkes Chevron Distributed

—

of Partner Loss

Remaining Loss

Income (Loss)

Remaining Income

Income

Income of Partner

P2. Distribution of Income: Salaries and Interest

Income of Partner

Remaining Income

Income

12-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.