If an asset costs $41,000, has a residual value of $3,000, and has a useful life of five

years, the entry to record depreciation in the second year, using the

double-declining-balance method, is

A. debit to Depreciation Expense, 9,430; credit to Cash, 9,430.

B. debit to Depreciation Expense, 9,840; credit to Accumulated Depreciation, 9,840

C. debit to Depreciation Expense, 10,250; credit to Accumulated Depreciation, 10,250

D. debit to Accumulated Depreciation, 10,660; credit to Depreciation Expense, 10,660

The primary difference between ordinary and extraordinary repairs is that extraordinary

repairs

A. are an expense of the current period.

B. are periodic in nature.

C. are necessary to maintain the asset in good operational condition.

D. extend the useful life or increase the residual value of the asset.

The direct method of preparing the statement of cash flows

A. results in more cash from operating activities, but less cash from investing activities,

and the same total cash flow as the indirect method.

B. converts each item on the income statement to its cash equivalent.

C. reports interest and dividends received in the investing activities section.

D. All of these choices.

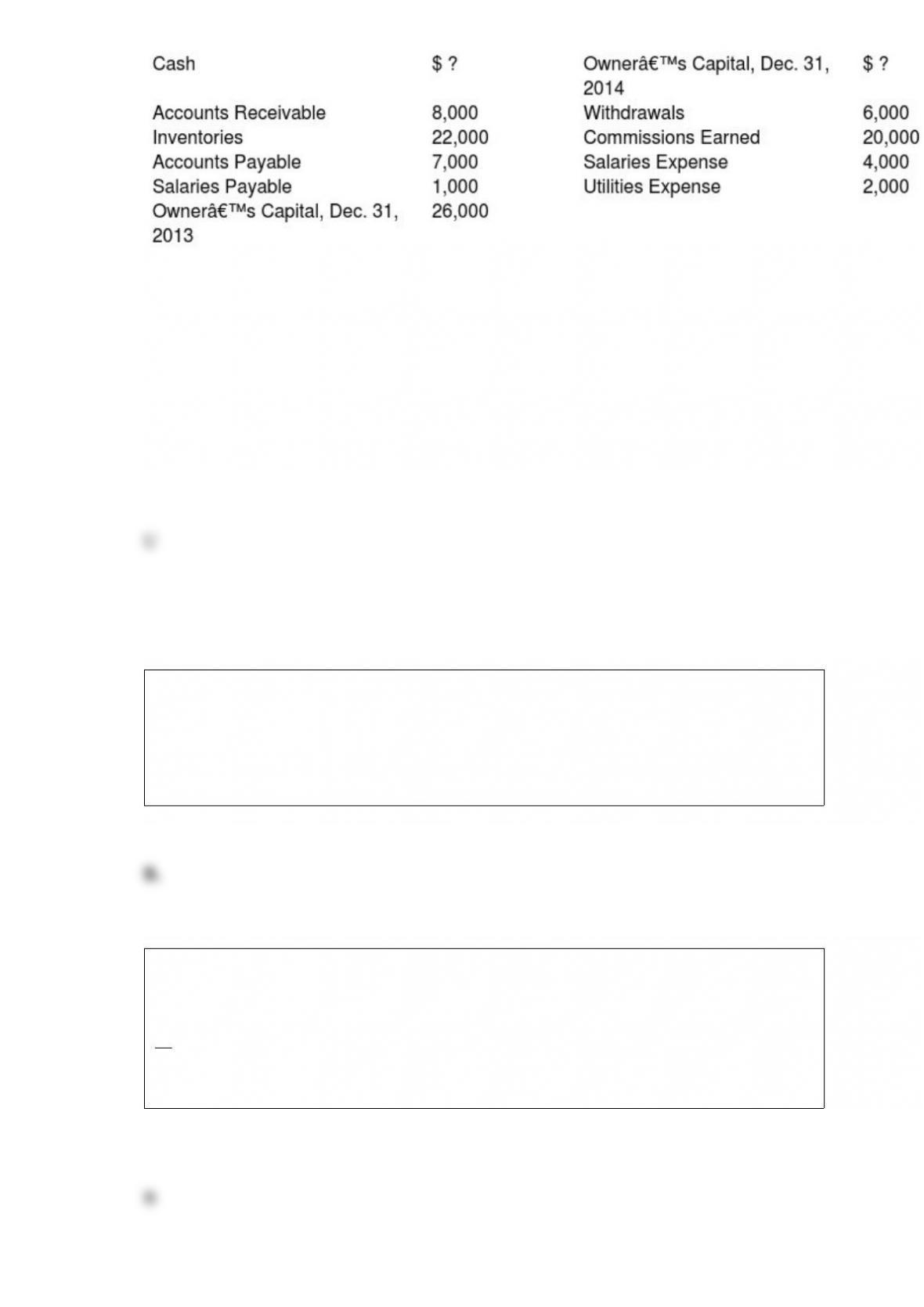

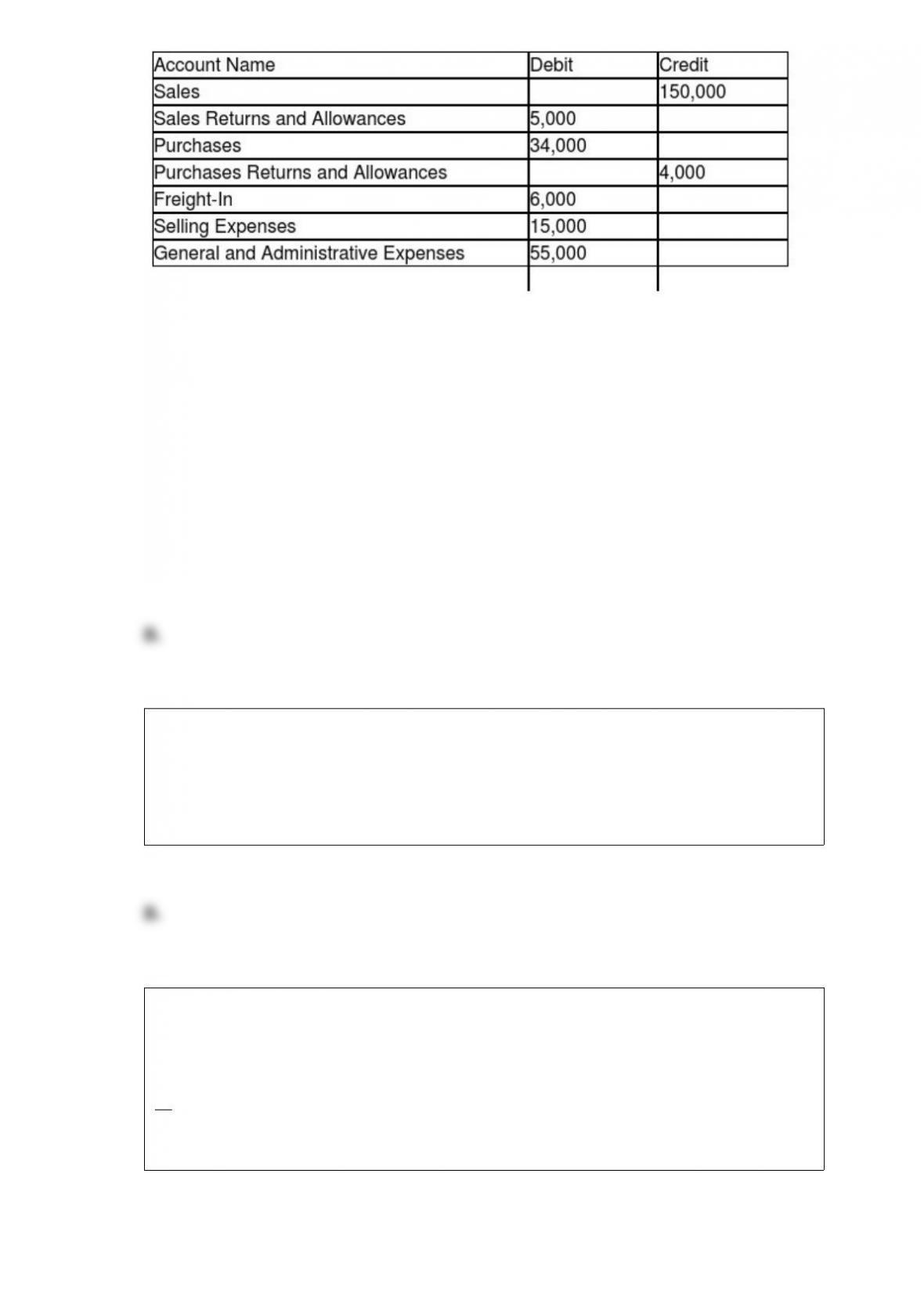

Use the following information to calculate at or for the year ended December 31, 2014:

(a) net income, (b) owner’s capital, (c) total assets, and (d) cash.

a. $20,000 – $4,000 – $2,000 = $14,000

b. $26,000 + $14,000 – $6,000 = $34,000

c. Total Assets = Total Liabilities and Owner’s Equity = $7,000 + $1,000 + $34,000 =

$42,000

d. $42,000 – $8,000 – $22,000 = $12,000

When bonds payable are converted into stock, the carrying value of the bonds should be

A. credited to Retained Earnings.

B. credited to contributed capital accounts.

C. debited to Retained Earnings.

D. debited to Loss on Conversion of Bonds.

A credit balance in the account Allowance to Adjust Long-Term Investments to Market

is disclosed in the financial statements as a

A. regular account in the stockholders’ equity section of the balance sheet.

B. contra account to Long-Term Investments.

C. note to the financial statements.

D. current asset.

On March 1, 20×5, King Corp. sold 102 of its 9 percent, $1,000 bonds for a price of 102

plus accrued interest. The accrued interest amounted to $800. If a balance sheet were to

be prepared at the end of the day, March 1, 20×5, the carrying value reported for the

bonds payable would be

A. $102,000.

B. $104,040.

C. $104,840.

D. $103,240.

The normal account balances for owner’s Capital and Withdrawals are

A. credit and debit, respectively.

B. debits.

C. credits.

D. debit and credit, respectively.

Discuss how each of the following would be recorded in the partner’s capital account

and why:

a. Trevor invests into the partnership land that he paid $40,000 for 3 years ago. Today,

the fair market value of the land is $65,000.

b. Marcela invests into the partnership a building that she paid $24,000 for 2 years ago.

The building has a $10,000 mortgage and its fair market value is $18,000. The

partnership assumes the mortgage.

c. Courtney invests into the partnership equipment she paid $12,000 for earlier in the

year by signing a note payable that the partnership is not assuming. The equipment has

a fair market value of $15,000.

a. Trevor’s capital account would be credited for $65,000 because that’s the fair market

value of the land.

b. Marcela’s capital account would be credited for $8,000 because that’s the difference

between the fair market value of the assets invested and the liabilities assumed.

The operating cycle for a merchandiser is

A. the period of time it takes to sell a unit of inventory.

B. the same for all companies.

C. most generally a year.

D. the time to buy, hold, sell, and collect payment for a sale.

When the effective interest method of amortization is used for a bond premium, the

amount of interest expense for an interest period is calculated by multiplying the

A. carrying value of the bonds at the beginning of the period by the face interest rate.

B. face value of the bonds at the beginning of the period by the effective interest rate.

C. carrying value of the bonds at the beginning of the period by the effective interest

rate.

D. face value of the bonds at the beginning of the period by the face interest rate.

Russell Company’s air-conditioning system has just completed the eighth year of an

estimated ten-year life. The system cost $60,000 and now has accumulated depreciation

of $48,000. At the beginning of the ninth year, the company expects to spend $16,000

on a complete renovation of the system and expects the total life of the system to be

fifteen years. Neither the capacity of the system nor the residual value was increased.

The company uses the straight-line method to determine depreciation. Determine the

following: (a) the account debited for the cost of renovation, (b) the carrying value of

the system after renovation, and (c) the depreciation expense for the ninth year.

a. Accumulated Depreciation

b. $28,000 ($60,000 – $48,000 + $16,000)

c. $4,000 [28,000 (15 – 8)]

Bonds that contain a provision that allows the holders to exchange the bonds for other

securities of the issuing corporation are called

A. debenture bonds.

B. secured bonds.

C. callable bonds.

D. convertible bonds.

A company with $75,000 in current assets, $37,500 in quick assets, and $45,000 in

current liabilities makes a payment of a $3,000 oncurrent debt. As a result of this

transaction, the current ratio and quick ratio will

A. both decrease.

B. increase and decrease, respectively.

C. both increase.

D. remain the same and decrease, respectively.

Which of the following accounts is increased with a debit?

A. Jim Webb, Capital

B. Rent Payable

C. Service Revenue

D. Prepaid Insurance

A leasehold is a payment

A. for the right to use certain property.

B. for the right to sublease certain property.

C. to give up or to get out of a lease.

D. to improve leased property.

Piper Company issued ten-year, 8 percent bonds payable in 20×5 at a premium. During

20×5, the company’s accountant failed to amortize any of the bond premium. The

omission of the premium amortization will

A. cause net income for 20×5 to be overstated.

B. not affect net income reported for 20×5.

C. cause net income for 20×5 to be understated.

D. cause retained earnings at the end of 20×5 to be overstated.

Holiday Corporation provided these figures for the year ended December 31, 20×5:

Cost of goods sold, $516,117; change in inventory, $67,483 decrease; average accounts

payable, $58,209.

What is the company’s payables turnover? Round your answer to one decimal place.

A. 8.3 times

B. 7.7 times

C. 10.1 times

D. 7.2 times

The board of directors of Lark Corporation declared a cash dividend of $3.50 per share

on 57,000 shares of common stock on June 14, 20×5. The dividend is to be paid on July

15, 20×5, to shareholders of record on July 1, 20×5. The proper entry to be recorded on

July 15, 20×5 is,

A. Cash 199,500

Dividends Payable 199,500

B. Dividends Payable 199,500

Cash 199,500

C. Cash 199,500

Dividends 199,500

D. Dividends 199,500

Use this information to answer the following question.

Panadora Company has the following information for the pay period of January 1-15,

2014. Payment occurs on January 20.

The entry to record the payroll taxes expense would include a credit to

A. Salaries Payable.

B. Federal Income Taxes Payable.

C. Social Security Tax Payable.

D. Cash.

Which of the following is not a permanent account?

A. Supplies

B. Accounts Receivable

C. Withdrawals

D. Unearned Revenue

Which of the following is an agency of the U.S. government?

A. IASB

B. SEC

C. FASB

D. AICPA

The Income Summary account is credited in the entry that closes

A. the Withdrawals account.

B. expense accounts.

C. net income.

D. revenue accounts.

An unsecured bond is the same as a

A. term bond.

B. zero coupon bond.

C. debenture bond.

D. bond indenture.

Given the following information about purchases and sales during the year, compute the

cost to be assigned to ending inventory under each of three methods: (a) average-cost,

(b) FIFO, and (c) LIFO. (Show your work.)

Which of the following accounts should be debited in a journal entry?

A. Accounts Receivable, when it has been decreased.

B. Withdrawals, when it has been increased.

C. Wages Payable, when it has been increased.

D. All of these choices.

Use this information to answer the following question.

In addition, beginning merchandise inventory was $11,000 and ending merchandise

inventory was $7,000.

If beginning and ending merchandise inventories were ignored in computing net income,

then net income would be

A. understated by $11,000.

B. overstated by $4,000.

C. understated by $7,000.

D. understated by $4,000.

If bonds are issued at a premium, the face interest rate is

A. lower than the market rate of interest.

B. higher than the market rate of interest.

C. too low to attract investors.

D. adjusted to a higher effective rate of interest.

Stock categorized as trading securities is purchased for $52,000. At year end, when the

market value of the stock is $61,000, the balance of the Short-Term Investments

account appearing on the balance sheet will be

A. $9,000

B. $52,000

C. $61,000

D. none of these

An important purpose of closing entries is to

A. set nominal account balances to zero to begin the next period.

B. adjust the accounts in the ledger.

C. help in preparing financial statements.

D. set real account balances to zero to begin the next period.

The qualitative characteristic of faithful representation includes

A. materiality

B. confirmative value.

C. timeliness.

D. neutral information.

All of the following are estimated liabilities except

A. liability for vacation pay.

B. payroll liabilities.

C. product warranty liability.

D. property tax liability.

The excess of the issuance price over the stated value of a no-par common stock should

be credited to the

A. Common Stock account.

B. Retained Earnings account.

C. Additional Paid-in Capital.

D. Treasury Stock.

Which of the following is a reason for not using the specific identification method?

A. It is impractical to keep track of the purchase and sale of individual items.

B. Deciding which of many identical items sold would be arbitrary.

C. Deciding whether lower or higher-priced identical items sold could be a means of

manipulating income.

D. All of these are reasons for not using the specific identification method.

The going concern assumption helps solve the

A. matching issue.

B. accounting period issue.

C. revenue recognition issue.

D. continuity issue.