1.

(the receiving clerk) are separated from recordkeeping (the accounting

with the existing assets at reasonable intervals. The comparison of the cash regis-

compared with the invoices before payment is authorized. In addition, prior to pay-

ment, the invoice should be approved by the person who submitted the purchase

requisition to ensure that he or she actually received the quantity and quality of

goods requested. In this way, authorization (the purchasing agent) and custody

ter tape with the cash in the cash drawer at the end of each day accomplishes this

person who has custody of the assets. In this case, the sales clerk could misappro-

priate funds from the cash drawer and report the sales at less than actual.

Cash sales One objective of internal control is to compare the records of assets

objective. However, the comparison should be made by someone other than the

Purchases In this case, invoices are being paid before they are compared with the

purchase order and receiving report. An invoice could be paid for goods that have

department).

P8. Internal Control Activities

8-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

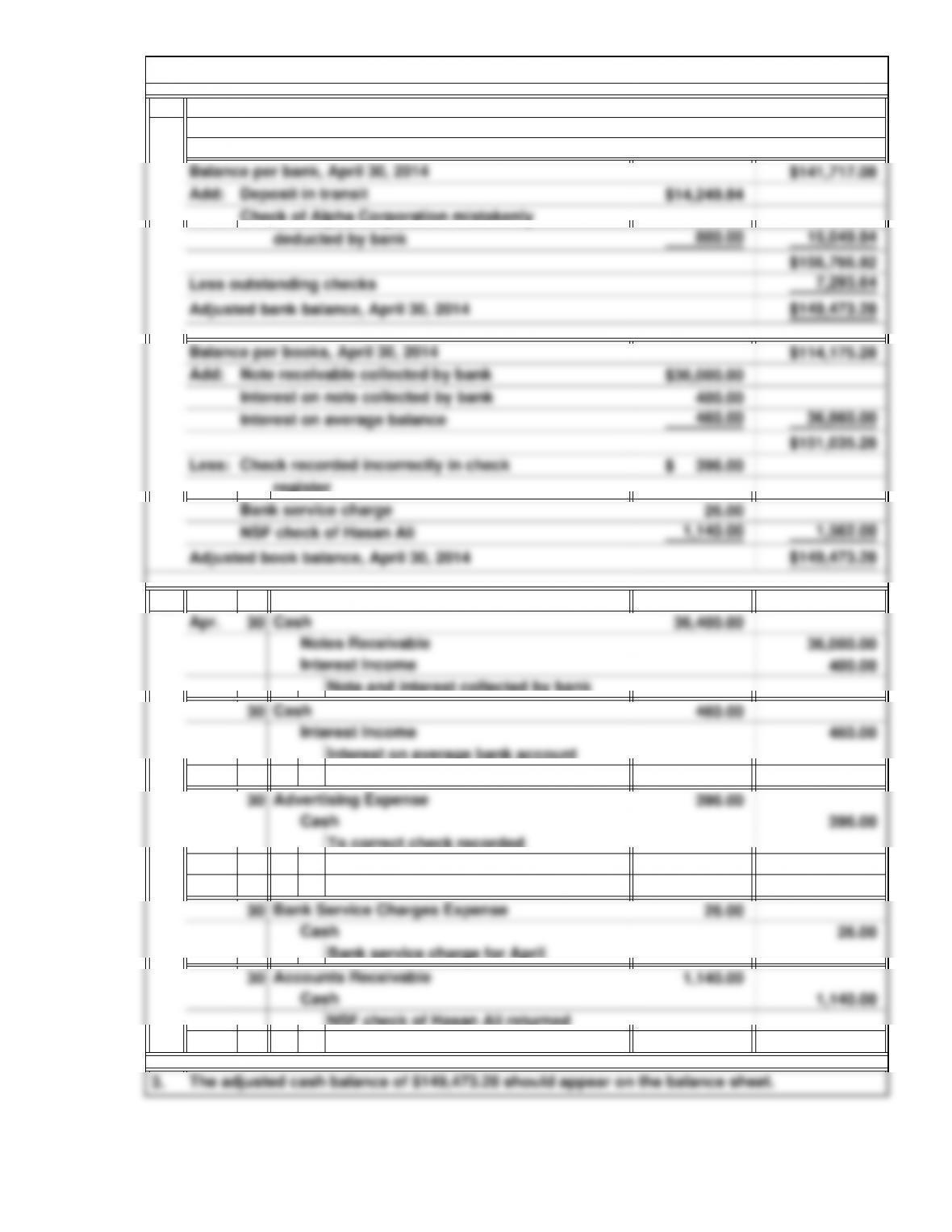

Note and interest collected by bank

Interest on average bank account

balance

To correct check recorded

incorrectly in check register

$2,420 – $2,024 = $396

Bank service charge for April

NSF check of Hasan Ali returned

by bank

April 30, 2014

2014

Delta Company

Bank Reconciliation

P9. Bank Reconciliation

8-17

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

4.

records of the company and proves that all cash transactions have been recorded.

as notes receivable collected by bank, interest income on notes, interest income,

overstatement of deposits, collection fees, NSF checks, and service charges, which

A bank reconciliation is a necessary internal control because events and items such

P9. Bank Reconciliation (Concluded)

8-18

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

To replenish the petty cash fund

A semiprofessional baseball team might use an imprest system as a fund for

2014

P10. Imprest (Petty Cash) Fund Transactions

8-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

Both the cashier and the ticket taker would be caught. At the end of the perform-

C1. Conceptual Understanding: Control Systems

Recording transactions Accountability is established at the point of receiving

Authorization Three key points of authorization have been put into the new sys-

Cases

8-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

a.

b.

c.

d.

1.

2.

3.

4.

C2. Interpreting Financial Reports: Internal Control Lapse

The control activities that were likely violated in this case are as follows.

Authorization: These expenditures were probably not authorized by a person who

No set solution. Note to Instructor: This case introduces students to the different types of

Periodic independent verification: There was apparently no independent verification

Separation of duties: It is likely that these expenditures were authorized by the em-

Sound personnel procedures: It is likely that sound personnel policies such as rotation

conceal the fraud.

of jobs, required vacations, and bonding were violated and enabled the employee to

C3. Conceptual Understanding: Internal Controls

C4. Annual Report Case: Internal Control Responsibilities

Management states, “We are responsible for establishing and maintaining adequate

The auditor states, “Because of its inherent limitations, internal control over financial

reporting may not prevent or detect misstatements. Also, projections of any evaluation

of effectiveness to future periods are subject to the risk that controls may become in-

control over financial reporting is effective and provides reasonable assurance that

2011, based on COSO criteria.”

assets are safeguarded and that the financial records are reliable for preparing finan-

cial statements as of December 31, 2011.”

The auditor states, “In our opinion, CVS Caremark Corporation maintained in all ma-

Management states, “Based on our assessment, we conclude our Company’s internal

terial respects effective internal control over financial reporting as of December 31,

the policies or procedures may deteriorate.”

internal control over financial reporting.”

8-21

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

quired for the customer to board the plane.

This case presents a situation that many students may be in a position to experience.

CVS and Southwest have different control risks. CVS is concerned that customers will

C5. Comparison Analysis: Contrasting Internal Control Needs

C6. Ethical Dilemma: Personal Responsibility for Mistakes

Note to Instructor: Answers will vary depending on the company selected by the

C7. Continuing Case: Annual Report Project

8-22

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.