1.

*

**

××3/

Present value of 20 periodic payments at 8% (16% / 2) (from Table 2*):

$3,600,000 0.09

accrued interest

12

Sold bonds at 100 plus 3 months’

Sold bonds at 105 on interest

payment date

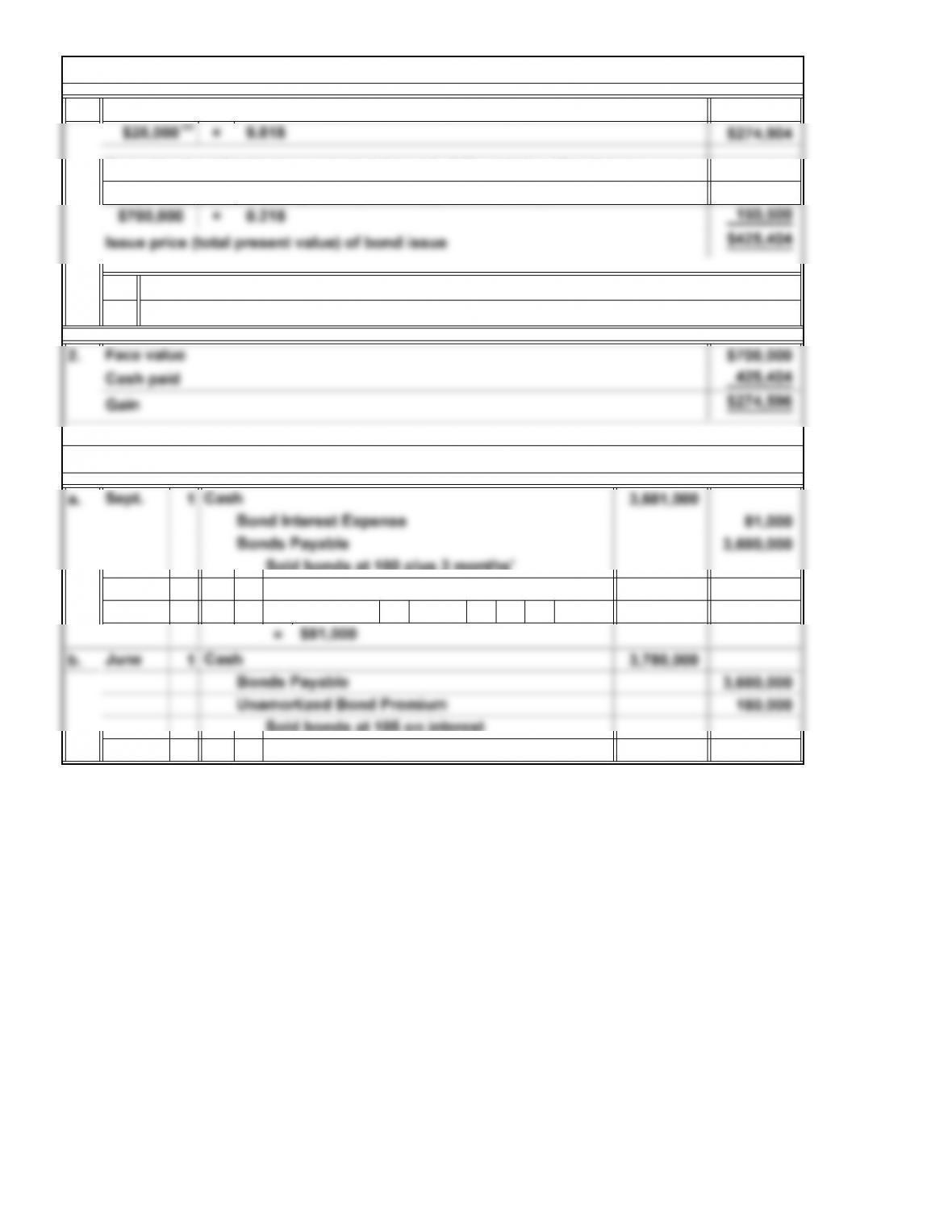

E13A. Time Value of Money and Early Extinguishment of Debt

From Appendix B

$700,000 × 8% × 6/12 = $28,000

14-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

××4/

××6/

2.

×=

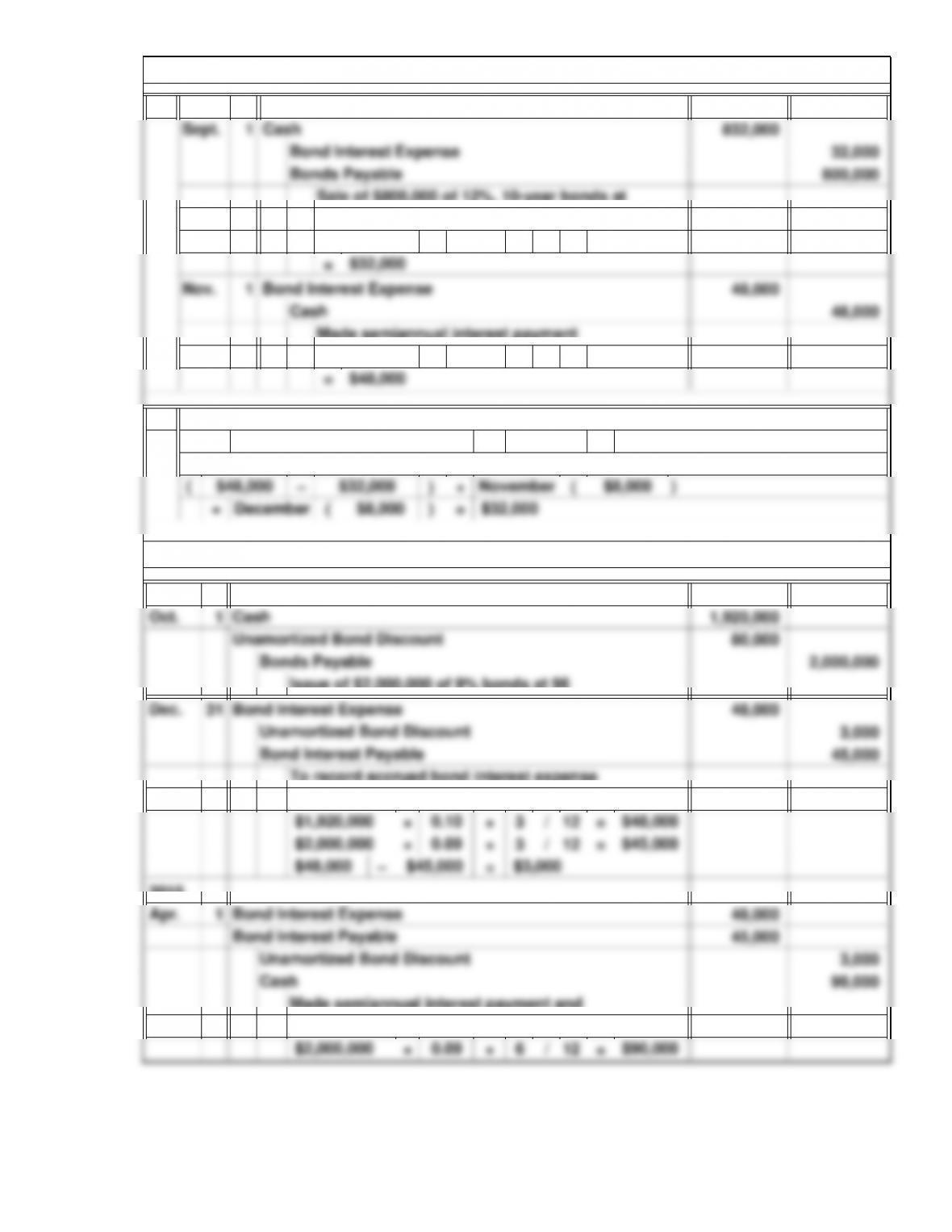

months (September–December) $32,000

2014

E15A. Bond Issue Between Interest Dates

$8,000

or

4

0.12

Made semiannual interest payment

Sale of $800,000 of 12%, 10-year bonds at

0.12

face value

$800,000 12

12

The bond interest expense for the year ended December 31, 2014, is $32,000:

$800,000

14-17

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

+

+

*Rounded

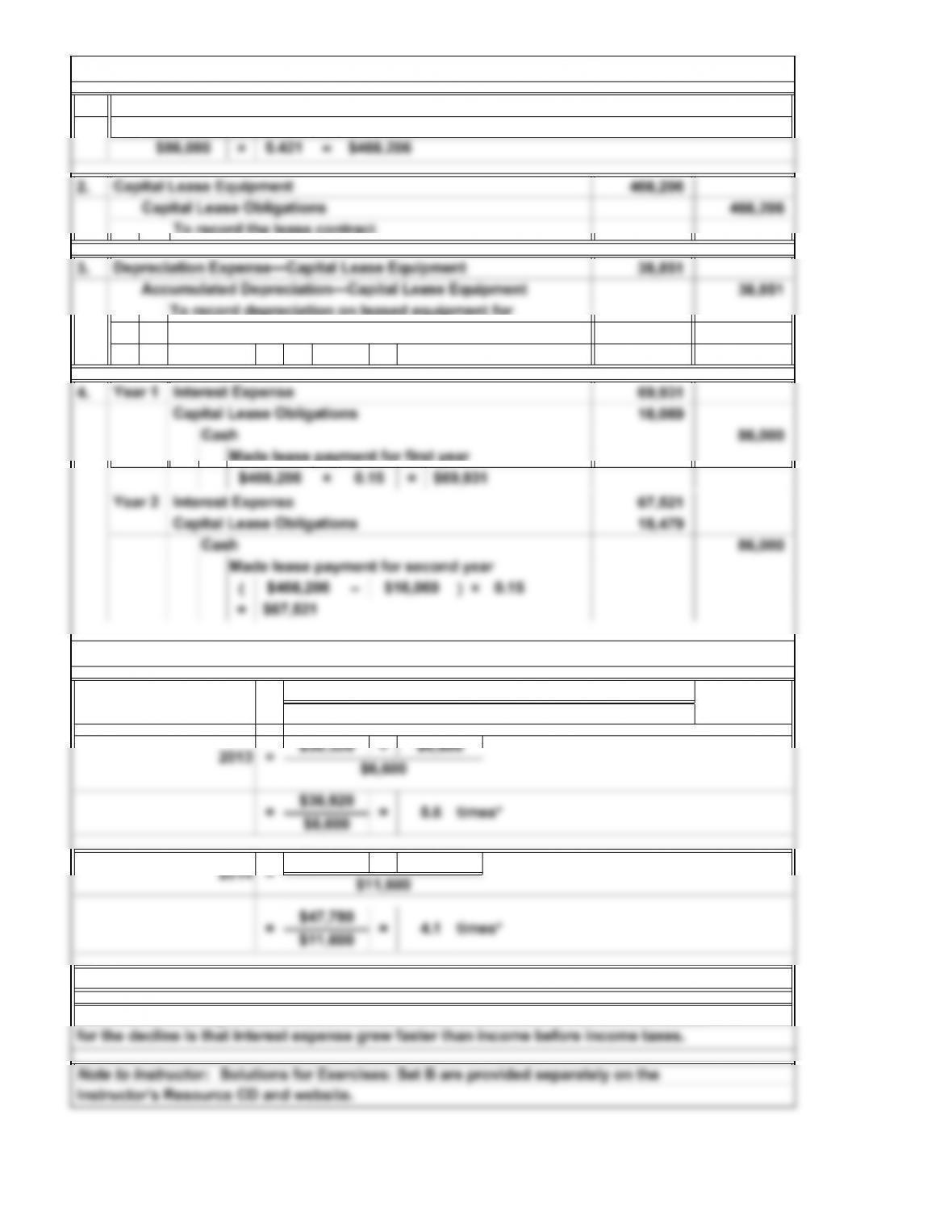

E17A. Recording Lease Obligations

Periodic Payment × Factor (Table 2 in Appendix B: 15%, 12 periods) = Present

Value of Lease

E18A. Interest Coverage Ratio

Interest

Coverage Ratio

Income Before Income Taxes + Interest Expense

Interest Expense

=

=$30,320 $6,600

$6,600

$36,920 = 5.6

2014 =

2013

=

$36,180 $11,600

$47,780 = 4.1

$11,600

$11,600

The interest coverage ratio declined from 2013 to 2014 from 5.6 to 4.1 times. The reason

times*

Instructor’s Resource CD and website.

14-18

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 1. 10.

2. 11.

3. 12.

4. 13.

5. 14.

6. 15.

7. 16.

8. 17.

9.

2.

P1. Bond Terminology

m

k

c

A decrease in the market interest rate will increase the price of the bond, therefore

Problems

n

l

o

i

h

dq

j

g

e

a

b

p

f

14-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

d.

(1)

(2)

(3)

2. a.

(2)

(3)

Calculation of cash received:

Calculation of cash received:

Amortization computed:

Interest expense computed:

Amortization computed:

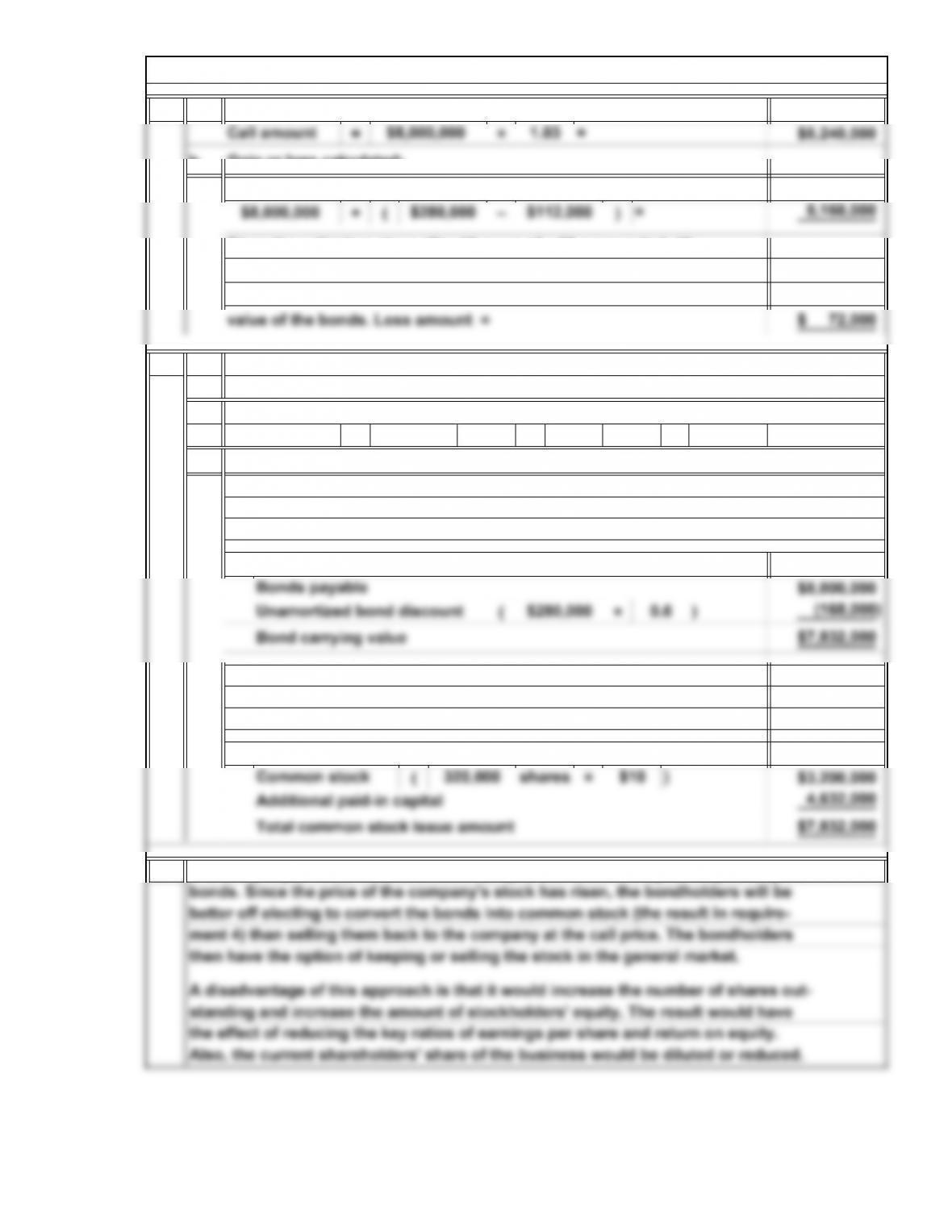

P2. Bond Basics—Straight-Line Method, Retirement, and Conversion

Cash paid in interest:

Interest components

Interest expense computed:

14-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3. a.

b.

4. a.

b.

/ × = shares

c.

5.

Gain or loss calculated:

Carrying value:

No gain or loss occurs in a bond conversion because the issued stock is re-

320,000

standing and increase the amount of stockholders’ equity. The result would have

the effect of reducing the key ratios of earnings per share and return on equity.

Also, the current shareholders’ share of the business would be diluted or reduced.

ment 4) than selling them back to the company at the call price. The bondholders

A disadvantage of this approach is that it would increase the number of shares out-

$8,000,000

shares

Decrease in liabilities:

Numbers of shares of common stock computed:

$1,000

then have the option of keeping or selling the stock in the general market.

better off electing to convert the bonds into common stock (the result in require-

The company can improve its debt to equity ratio without using cash by calling the

stockholders’ equity.

Bonds payable and its accompanying unamortized discount will be reduced in

corded at the carrying value of the bonds that are converted.

P2. Bond Basics—Straight-Line Method, Retirement and Conversion (Concluded)

Effects of liabilities and stockholders’ equity shown:

the liabilities. Common stock and additional paid-in capital will be increased in

Cash to retire bonds:

bonds 40

14-21

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

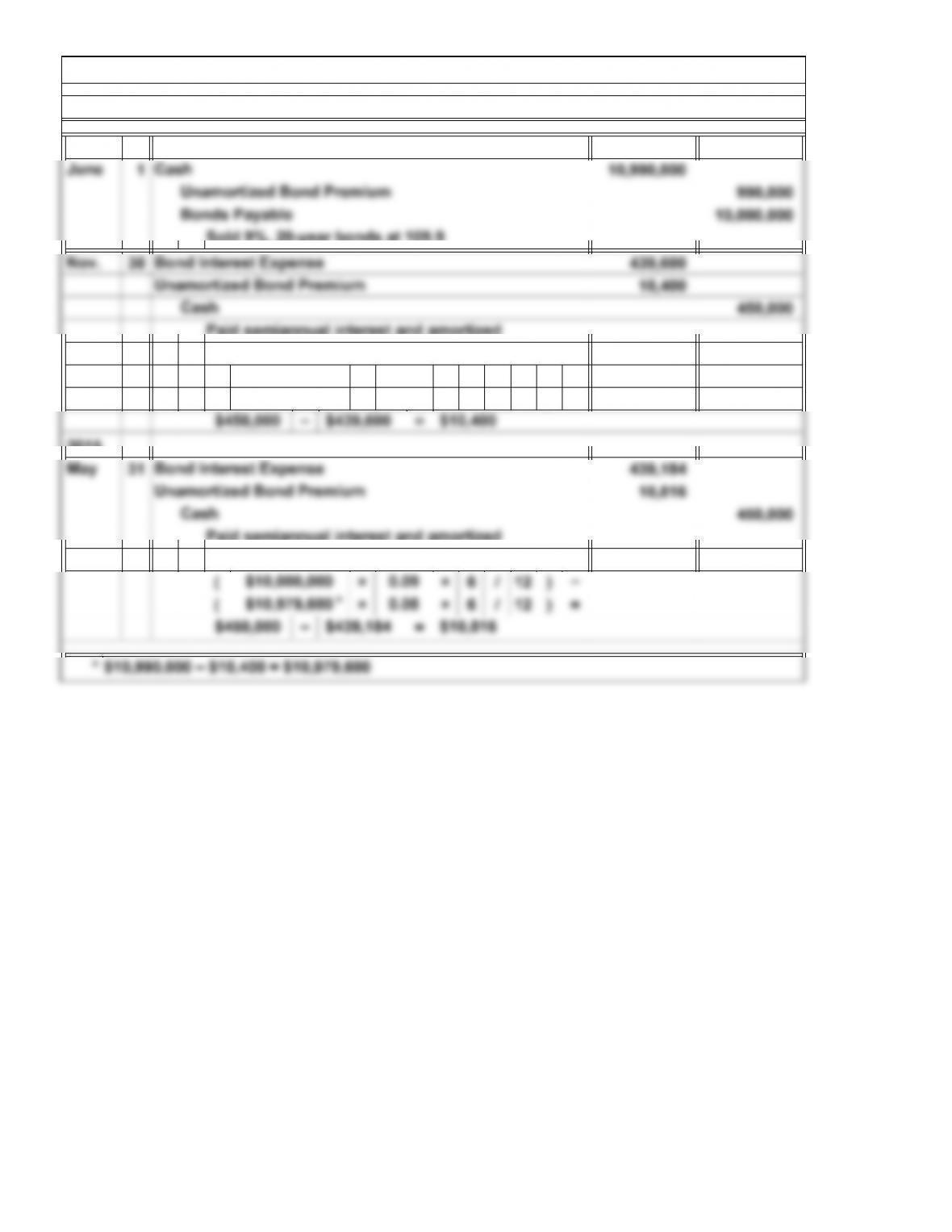

(××6/12)−

(××6/12)=

P3. Bond Transactions—Effective Interest Method

2014

0.08$10,990,000

1.

2015

Paid semiannual interest and amortized

the premium on 9%, 20-year bonds

0.09$10,000,000

14-22

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.