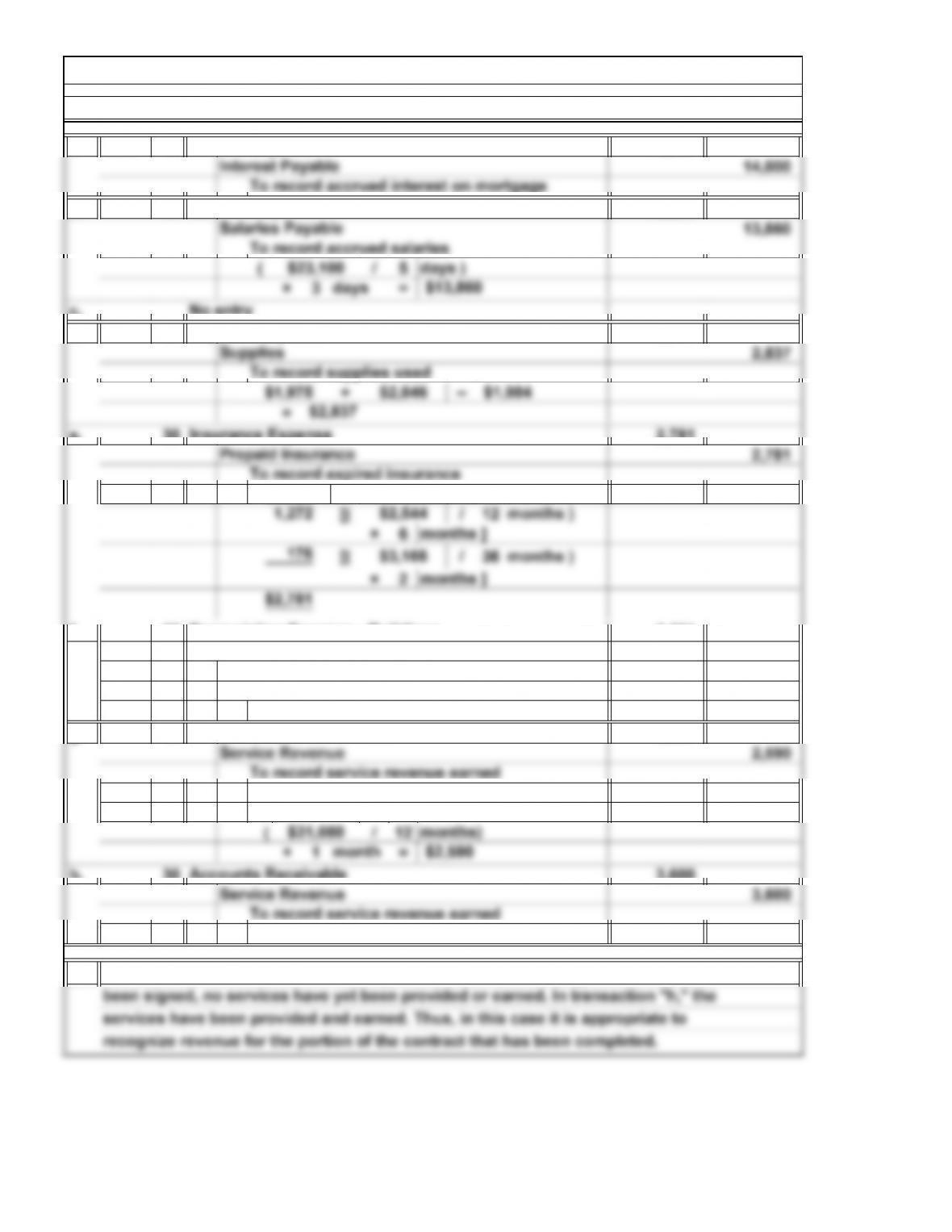

a. June 30 14,000

b. 30 13,860

h. 30 3,600

2.

In transaction “c,” no revenue is recognized because even though a contract has

Accounts Receivable

To record service revenue earned

on a contract to be billed in August

To record accrued interest on mortgage

Salaries Expense

Interest Expense

P15. Preparing Adjusting Entries

1.

3-44

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Bal. 1,660

Bal. 650 Bal. 3,200 Bal. 458

Advertising Expense

Rent Expense

Telephone Expense

Accounts Receivable Prepaid Insurance

Cash

Unearned Tax Fees S. Jacobs, Capital

P16. Determining Adjusting Entries and Tracing Their Effects to Financial Statements

1. and 2.

Accounts Payable

3-45

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

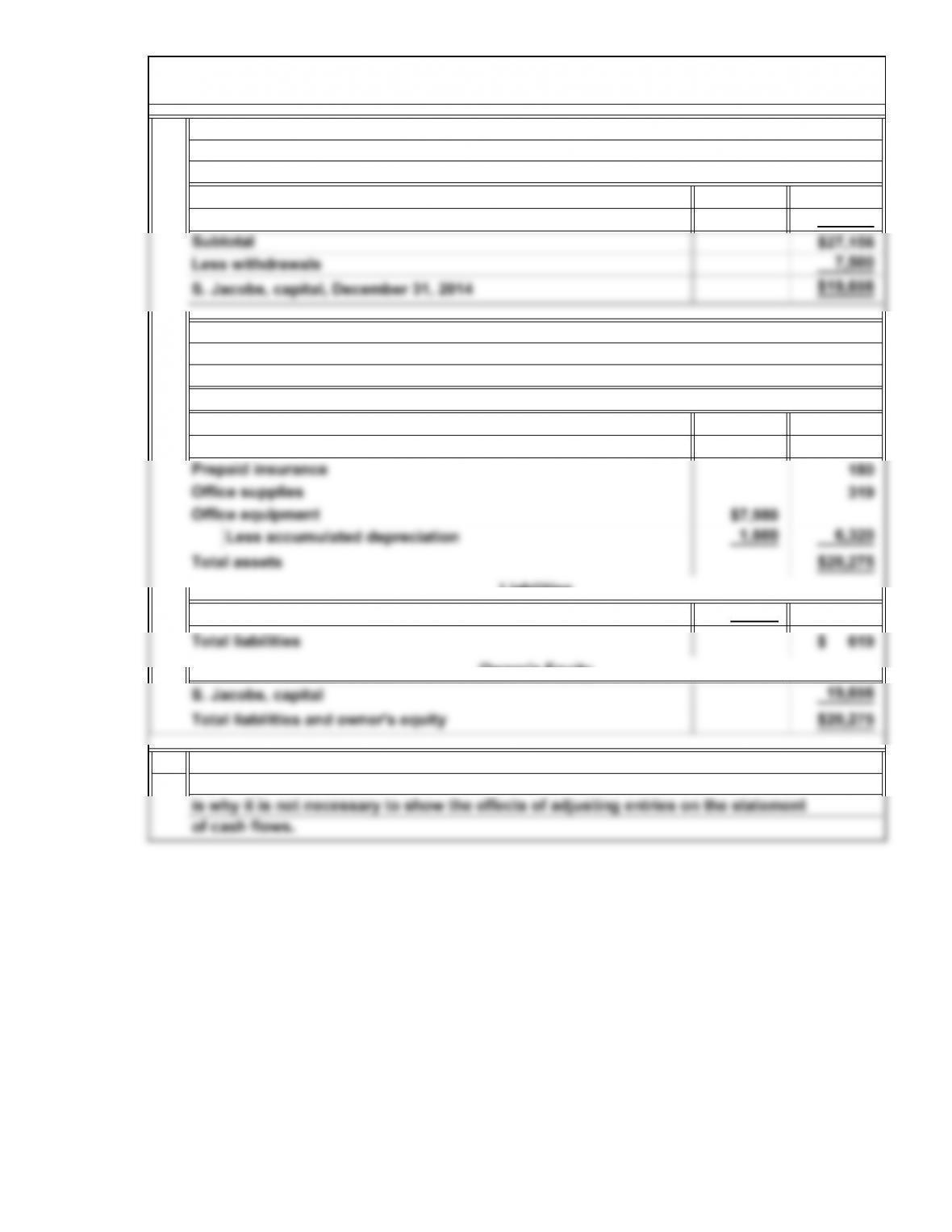

11,265

2,191

$37,445

$9,700

650

December 31, 2014

Cash

Accounts Receivable

P16. Determining Adjusting Entries and Tracing Their Effects to Financial Statements

(Continued)

Jacobs Financial Advisors Service

Adjusted Trial Balance

now has a zero balance.

Jacobs Financial Advisors Service

Income Statement

Note: Unearned Tax Fees does not appear on the adjusted trial balance because it

Tax fees revenue

Office salaries expense

Advertising expense

Expenses:

For the Year Ended December 31, 2014

Revenues:

3-46

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$ 5,474

21,682

$11,265

2,191

$ 619

4.

Net income

S. Jacobs, capital, December 31, 2013

adjusting entries never involve the cash account, they never affect cash flows. That

By definition, adjusting entries cannot include a debit or a credit to Cash. Because

Accounts payable

P16. Determining Adjusting Entries and Tracing Their Effects to Financial Statements

(Concluded)

Jacobs Financial Advisors Service

Balance Sheet

December 31, 2014

Assets

Liabilities

Cash

Accounts receivable

Jacobs Financial Advisors Service

Statement of Owner’s Equity

For the Year Ended December 31, 2014

3-47

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

a.

b.

c.

d.

Eclipsys recognized revenue, although it had not yet rendered the services. Therefore,

Xerox violated the guidelines for recognition by overstating revenues. It should re-

Eclipsys violated accrual accounting. Eclipsys shouldn’t have recorded any revenue

until it performed the services. If the company received some money up front, it

Lucent Technologies recognized revenue. However, collectibility was not reasonably

America Online (AOL) recognized advertising as an asset. However, advertising ser-

vices had already been used to produce revenue in that accounting period. Therefore,

assured. Therefore, Lucent Technologies violated accrual accounting. The company

AOL violated accrual accounting. AOL should have made the adjusting entry to recog-

should have had tighter credit terms and assessed the collectibility of its receivable

nize advertising expense and reduce the prepaid advertising asset account.

C1. Conceptual Understanding: Importance of Adjustments

pense undoubtedly led to poor management decisions and, eventually, to the company’s

bankruptcy.

in the period covered by the warranty. The failure to properly estimate the warranty ex-

that it was either charging too little for the rust-prevention service or being too generous

According to the concepts of accrual accounting, the accountant must estimate and record

(accrue) the expenses associated with a sale even though cash may not be paid out until

future years. This procedure enables management to tell whether a company is earning

Cases

C2. Conceptual Understanding: Earnings Management and Fraudulent Financial Reporting

3-48

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

erties that are specifically related to future productions. These costs are recorded as assets

C3. Interpreting Financial Reports: Application of Accrual Accounting

each year’s operations and to make year-to-year comparisons of operating results.

is taken into revenue through an adjusting entry in the year in which the production is per-

formed. These accounting policies apply accrual accounting to the preparation of finan-

cial statements. This enables Lyric Opera’s management to assess the financial success of

Deferred production costs result from expenditures for scenery, costumes, and stage prop-

C4. Interpreting Financial Reports: Analysis of an Asset Account

Film and television costs consist of the cost of producing films and television programs

3-49

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

3.

CVS states that its financial statements are prepared in accordance with generally

C5. Annual Report Case: Analysis of Balance Sheet and Adjusting Entries

term assets like property and equipment can require adjustments to allocate cost to

All current assets except cash can be affected by adjusting entries. Similarly, long-

3-50

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

It is not appropriate to record the cash received for the service contracts as revenues in

the current year because policy coverage does not begin until the second year of owner-

ship. This would overstate net income in the first year when cash is received. The ex-

practice is not followed, it would be unethical to accept management’s recommendation.

C6. Ethical Dilemma: Importance of Adjustments

penses associated with these receipts will be incurred for one year or more from the date

C7. Continuing Case: Annual Report Project

Note to Instructor: Answers will vary depending on the company selected by the

students.

3-51

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.