Chapter 15

The Statement of Cash Flows

Learning Objectives

1. Describe the principal purposes and concepts underlying the statement of cash ows,

and identify its components and format.

2. Use the indirect method to determine cash ows from operating activities.

3. Determine cash ows from investing activities.

4. Determine cash ows from $nancing activities.

5. Analyze the statement of cash ows.

Section 1: Concepts

Concepts

Relevance

Classi$cation

Disclosure

Lecture Outline

I. The statement of cash ows shows how a company’s operating, investing, and

$nancing activities have a,ected cash during a period.

A. Cash is de$ned as including cash equivalents, which include:

1. Money market accounts.

2. Commercial paper.

3. U.S. Treasury bills.

B. The statement is relevant to:

1. Managers, who use it to:

a. Assess liquidity.

b. Determine dividend policy.

c. Evaluate the e,ects of policy decisions involving investments and

$nancing.

2. Investors and creditors, who use it to assess a company’s ability to:

a. Manage cash ows.

b. Generate positive future cash ows.

c. Pay its liabilities.

d. Pay dividends and interest.

e. Anticipate the need for additional $nancing.

C. The statement of cash ows has three major classi$cations.

1. Operating activities involve cash inows and outows from normal business

activities in generating net income

a. Cash inows include cash received from the sale of goods and services

and from the sale of trading securities.

b. Cash outows include cash payments for wages, inventory, expenses,

taxes, and the purchase of trading securities.

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 2

2. Investing activities involve:

a. The acquisition and sale of property, plant, and equipment; long-term

investments; and short-term marketable securities other than trading

securities.

b. The making and collecting of loans.

3. Financing activities involve obtaining resources from stockholders (owners)

and lenders (banks).

a. Cash inows include proceeds from stock issues and borrowing.

b. Cash outows include payments of dividends and repayments of loans

(excluding interest).

4. A reconciliation of the beginning and ending cash balances appears at the

bottom of the statement.

D. The disclosure of any signi$cant noncash investing and $nancing transactions

must be disclosed in a separate schedule.

E. There are two alternatives for presenting operating activities.

1. The direct method converts each item on the income statement from the

accrual basis to the cash basis.

2. The indirect method begins with net income and lists only items necessary to

convert net income to cash ows from operations.

Summary

The statement of cash ows is considered a major $nancial statement, along with the

income statement, balance sheet, and statement of stockholders’ equity. The statement of

cash ows, however, provides much information and answers certain questions that the

other three statements do not. It has replaced the statement of changes in $nancial position,

and its presentation is required whenever an income statement is prepared.

The statement of cash ows shows the e,ect on cash and cash equivalents of the

operating, investing, and $nancing activities of a company for an accounting period. Cash

equivalents are short-term, highly liquid investments such as money market accounts,

commercial paper (short-term notes), and U.S. Treasury bills. Short-term investments

(marketable securities) are not considered cash equivalents.

The principal purpose of the statement of cash ows is to provide information about a

company’s cash receipts and cash payments during an accounting period. The secondary

purpose of the statement of cash ows is to provide information about a company’s

operating, investing, and $nancing activities during the period.

Investors and creditors may use the statement of cash ows to assess such conditions as

the company’s ability to generate positive future cash ows, its ability to pay its liabilities,

its ability to pay dividends, and its need for additional $nancing. Management uses the

statement of cash ows (among other sources) to assess the business’s debt-paying ability,

determine its dividend policy, and plan its investing and $nancing needs.

The statement of cash ows categorizes cash receipts and cash payments as operating,

investing, and $nancing activities, as follows:

1. Operating activities include receiving cash from customers for the sale of goods and

services; receiving interest and dividends on loans and investments; receiving cash

from the sale of trading securities; and making cash payments for wages, goods and

services purchased, interest, taxes, and purchases of trading securities.

2. Investing activities include purchasing and selling long-term assets and marketable

securities (other than trading securities or cash equivalents) as well as making and

collecting on loans to other entities.

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 3

3. Financing activities include issuing and buying back capital stock as well as

borrowing and repaying loans on a short- or long-term basis (issuing bonds and notes).

Dividends paid are also included in this category, but the repayment of accounts

payable or accrued liabilities is not.

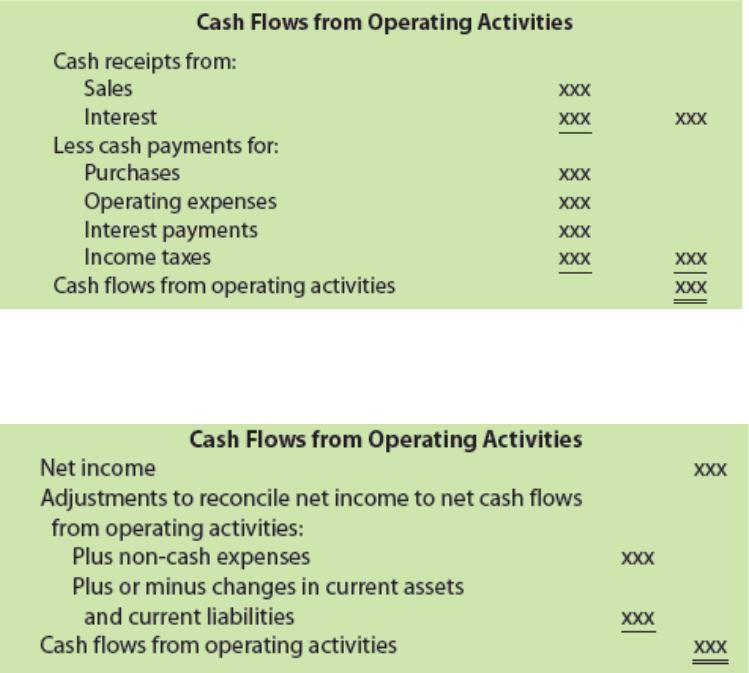

Statement of Cash Flows Direct Method and Indirect Method

There are two ways of presenting the operating activities section of the statement of cash

ows.

1. The direct method converts each item on the income statement from the accrual

basis to the cash basis. The operating activities section of the statement of cash

ows under the direct method follows in simpli$ed format.

2. The indirect method does not require the conversion of each item on the income

statement. It lists only the items necessary to convert net income to cash ows from

operating activities in the following format:

The statement of cash ows should be accompanied by a schedule disclosing any signi$cant

noncash investing and #nancing transactions involving long-term assets, long-term

liabilities, or stockholders’ equity. For example, the issuance of stock for land and the

conversion of bonds into stock represent simultaneous investing and $nancing activities that

do not, however, result in an inow or outow of cash. On the formal statement of cash

ows, individual cash inows and outows from investing and $nancing activities are shown

separately in their respective categories.

Relevant Examples and Exhibits

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 4

Exhibit 1 Consolidated Statement of Cash Flows

Exhibit 2 Classi$cation of Cash Inows and Cash Outows

Teaching Strategy

Distinguish between cash equivalents and short-term investments/marketable securities.

List the primary and secondary purposes of the statement of cash ows. Make a list or allow

students to suggest a list of management uses (such as determining the need for short-term

$nancing, determining available cash for dividends, and planning for long-term investing

and $nancing). Do the same for investors’ and creditors’ uses (determining the ability to

repay loans, pay dividends, and so on).

Operating Activities

Explain to students that transactions involving cash and current assets (except for

marketable securities and notes receivable) and transactions involving cash and current

liabilities (except for notes payable and dividends payable) are classi$ed as operating

activities.

Investing Activities

Explain that transactions involving cash and noncurrent assets, current marketable

securities, and current notes receivable are classi$ed as investing activities.

Financing Activities

Explain that transactions involving cash and the rest of the balance sheet accounts are

classi$ed as $nancing activities. These accounts are the noncurrent liabilities, current notes

payable, current dividends payable, and the equity accounts (except that net income’s e,ect

on retained earnings is part of operating activities).

Noncash Investing and Financing

Transactions involving any of the accounts listed as investing or $nancing activities that do

not involve cash are classi$ed as noncash investing or $nancing.

Refer students to Exhibit 2 for examples of operating, investing, and $nancing activities. Use

Short Exercise 1 and Exercise 1A as reinforcing class or group activities. Case 1 deals with

the real-world use of EBITDA.

Section 2: Accounting Applications

Accounting Applications

Determining cash ows from operating activities using the indirect method

Determining cash ows from investing activities

Determining cash ows from $nancing activities

Lecture Outline

I. Step one: Determine cash ows from operating activities.

A. Under the indirect method, cash ows from operating activities equal net

income adjusted by items that increase or decrease cash ow from operations.

B. Discuss the items to be added back to net income:

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 5

1. Depreciation expense, amortization expense, and depletion expense

2. Losses

3. Decreases in accounts receivable, inventory, and prepaid expenses

4. Increases in accounts payable, accrued liabilities, and income taxes payable

C. Discuss the items to be deducted from net income:

1. Gains

2. Increases in accounts receivable, inventory, and prepaid expenses

3. Decreases in accounts payable, accrued liabilities, and income taxes payable

D. The direct and indirect methods produce the same results, and both are GAAP.

II. Step two: Determine cash ows from investing activities.

A. Investing activities include the following:

1. Purchase and sale of long-term assets

2. Purchase and sale of short-term investments

B. Discuss the treatment of gains and losses under the indirect approach.

1. Gains (as part of full cash proceeds) are included in the investing activities

section.

2. Gains are deducted from net income in the operating activities section.

3. With losses, full cash proceeds appear in the investing activities section.

4. Losses are added to net income in the investing activities section.

C. Upon a purchase, the full cash outows appear in the investing activities

section.

III. Step three: Determine cash ows from $nancing activities.

A. Financing activities include the following:

1. Short- and long-term borrowing (notes and bonds) and repayment

2. Issuance and repurchase of capital stock

B. Changes in retained earnings are explained through analyses of net income

(in operating activities section) and dividends paid (in $nancing activities section).

IV. Step four: Prepare the statement of cash ows

A. Exhibit 8 shows a completed statement of cash ows using the indirect

method.

B. The direct and indirect methods di,er only in the cash ows from operating

activities section of the statement of cash ows.

V. The statement of cash ows must be in agreement with other $nancial statements.

A. The beginning cash balance shown on the statement of cash ows must

match the cash amount reported on the previous balance sheet.

B. The ending cash balance shown on the statement of cash ows must match

the amount reported on the current balance sheet.

C. The statement of cash ows reconciles the di,erence between the two

amounts.

Summary

To determine cash ows from operating activities, it is necessary to convert the $gures on

the income statement from an accrual basis to a cash basis using either the direct method

or the more common indirect method. Under the direct method, each item in the income

statement is adjusted from the accrual basis to the cash basis. Under the indirect method,

net cash ows from operating activities are determined by taking net income and adding or

deducting items that do not a,ect cash ows from operations. Items to add include

depreciation expense, amortization expense, depletion expense, losses from investing

activities, decreases in certain current assets (accounts receivable, inventory, and prepaid

expenses), and increases in certain current liabilities (accounts payable, accrued liabilities,

and income taxes payable). Items to deduct include gains from investing activities, increases

in certain current assets, and decreases in certain current liabilities. The direct and indirect

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 6

methods produce the same results, and both are considered GAAP. The indirect method is

used more often, however, and is the focus of this section. It has the advantage of being

easier and less expensive to prepare than the direct method.

To determine cash ows from investing activities, it is necessary to examine each account

involving cash receipts and cash payments from investing activities. The objective is to

explain the change in the appropriate account balances from one year to the next. As

previously stated, investing activities concern the purchase and sale of long-term assets and

short-term investments. Under the indirect approach, gains and losses from the sale of these

assets should, respectively, be deducted from and added back to net income to arrive at net

cash ows from operating activities. Then, the full cash proceeds are entered into the cash

ows from investing activities section of the statement of cash ows.

Investing activities center on long-term assets shown on the balance sheet. They also

include transactions a,ecting short-term investments from the current assets section of the

balance sheet and investment gains and losses from the income statement.

Financing activities focus on certain liability and stockholders’ equity accounts. They include

short- and long-term borrowing (notes and bonds) and repayment, issuance and repurchase

of capital stock, and payment of dividends. Changes in the Retained Earnings account are

explained on the statement of cash ows, for the most part, through analyses of net income

and dividends paid.

Exhibit 8 illustrates a completed statement of cash ows using the indirect method. The

essence of the indirect approach is the conversion of net income to net cash ows from

operating activities.

Relevant Examples and Exhibits

Exhibit 3 Preparation of the Statement of Cash Flows

Exhibit 4 Income Statement

Exhibit 5 Comparative Balance Sheets Showing Changes in Accounts

Exhibit 6 Indirect Method of Determining Net Cash Flows from Operating Activities

Exhibit 7 Schedule of Cash Flows from Operating Activities: Indirect Method

Exhibit 8 Statement of Cash Flows: Indirect Method

Exhibit 9 Relationship of the Statement of Cash Flows to the Balance Sheet

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 7

Teaching Strategy

Point out that both the direct and indirect methods attempt to convert from the accrual basis

to the cash basis. Under the indirect method, however, net income is the starting point.

Students have diGculty understanding why items such as depreciation expense are “added

back,” whereas items such as “gain on sale” are deducted to arrive at cash ows from

operations. For the sale of plant assets, point out that it is the proceeds of the sale that

produce the cash ow, not the amount of the gain or loss (which must, in e,ect, be

eliminated).

Have students work Short Exercise 2 or 3 and Exercise 2A or 3A for practice.

Short Exercises 4 and 5, and Exercises 4A, 5A and 8A also apply to this section.

Point out that all of the items pertaining to $nancing activities relate to the right-hand side

of the balance sheet (stock, bonds, etc.) and that they appear in the $nancing activities

section whether they produce an inow or an outow of cash. Dividends paid are included

because they relate to retained earnings.

Section 3: Business Applications

Business Applications

Evaluate a company’s cash-generating eGciency

oCash ow yield

oCash ow to sales

oCash ow to assets

oFree cash ow

Ethics

Lecture Outline

I. An analysis of cash inows and outows from operating activities can reveal signi$cant

relationships.

A. Cash-generating eGciency is the ability of a company to generate cash from

operations.

B. Cash ow yield is the quotient of net cash ows from operating activities

divided by net income.

1. It is calculated as:

Cash Flow Yield = Net Cash Flows from Operating Activities

Net Income

2. It shows whether a company is generating suGcient cash ow in relation to its

net income.

3. For most companies, the cash ow yield should exceed 1.0.

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 8

C. Cash ows to sales is the quotient of net cash ows from operating activities

divided by net sales:

1. It is calculated as:

Cash Flows to Sales = Net Cash Flows from Operating Activities

Sales

2. This ratio is closely related to pro$t margin and varies from it by the cash ow

yield.

D. Cash ows to assets is the quotient of net cash ows from operating activities

divided by average total assets:

1. It is calculated as:

Cash Flows to Assets = Net Cash Flows from Operating Activities

Average Total Assets

2. This ratio is related to return on assets and varies from it by the cash ow

yield.

E. Free cash ow is the amount of cash that remains after deducting the funds a

company must commit to continue operating at its planned level.

1. It is calculated as:

Net Cash Flows from Operating Activities

− Dividends

− Purchases of Plant Assets

+ Sales of Plant Assets

= Free Cash Flow

2. The free cash ow is the best predictor of future increases in stock price.

3. A positive free cash ow means the company has cash available to reduce

debt or expand operations.

4. A negative cash ow means that the company will need to sell investments,

borrow money, or issue stock in the short term to continue operating at its

planned level.

F. When interpreting the statement of cash ows, it pays to know the right questions

to ask:

1. What are the primary reasons cash ows from operating activities di,ered

from net income?

2. What were the most important investing activities other than capital

expenditures?

3. How did the company manage its $nancing activities?

4. What has been the trend in cash ows over several years?

Summary

The components of the statement of cash ows show how management is spending cash.

Interpreting the statement of cash ows includes examining fundamental relationships such

as cash-generating eGciency and free cash ow. Cash-generating e*ciency, which

focuses on net cash ows from operating activities, is the ability of a company to generate

cash from operations. Three measures of cash-generating eGciency are cash ow yield, cash

ows to sales, and cash ows to assets:

1. Cash ow yield is the ratio of net cash ows from operating activities to net income.

For most companies, this ratio should exceed 1.0.

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.

Chapter 15: The Statement of Cash Flows Instructor’s Manual, p. 9

2. Cash ows to sales is the ratio of net cash ows from operating activities to net sales.

3. Cash ows to assets is the ratio of net cash ows from operating activities to average

total assets.

Free cash ow is the cash remaining after the company has met current operating

commitments, such as those for operations, interest, income taxes, dividends, and net

capital expenditures. A positive free cash ow means that the company has met its cash

commitments and has cash remaining to reduce debt or expand operations. A negative free

cash ow means that the company will have to sell investments, borrow money, or issue

stock in order to continue operating at its planned level.

As is true with all $nancial statement ratios, it is necessary to consider trends in order to

obtain an accurate picture. The trends in the cash-generating eGciency and free cash ow

over several years should be examined to analyze a company’s cash ows.

Because cash ows from operations are a widely used measure of performance, companies

have been known to overstate cash ows through questionable accounting practices. While

these practices may not be illegal, they are considered unethical because they misrepresent

actual performance.

Relevant Examples and Exhibits

Ratio: Cash Flow Yield

Ratio: Cash Flows to Sales

Ratio: Cash Flows to Assets

Example: Free Cash Flow Computation

Teaching Strategy

This objective is best taught by illustration. Use Short Exercise 8 and Exercise 9A for

classroom illustration. Case 3 considers ethics and cash ow classi$cations; Case 2 on

Enron’s statement of cash ows is always of high interest to students.

Student Engagement Tactics

1 . Assign Case 3 to small groups in class. Use previously established groups or assign

groups randomly. Each group should select a representative to speak for the group.

2. Be clear on the expected output of the learning activity. Identify questions to address

and determine whether written answers are necessary. For example, ask one person

from each group to present one alternative and explain why that alternative would be

best.

3. Elicit as many alternatives as possible for the class to consider. After each group has

presented one alternative, if time permits, ask if any other alternatives might be

available.

4. Allow groups one or two minutes to consider which alternative they prefer and why. Poll

the class as to their preferred response.

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated,

or posted to a publicly accessible website, in whole or in part.