1. c 6.

2. e 7.

3. c 8.

4. b 9.

5. a 10.

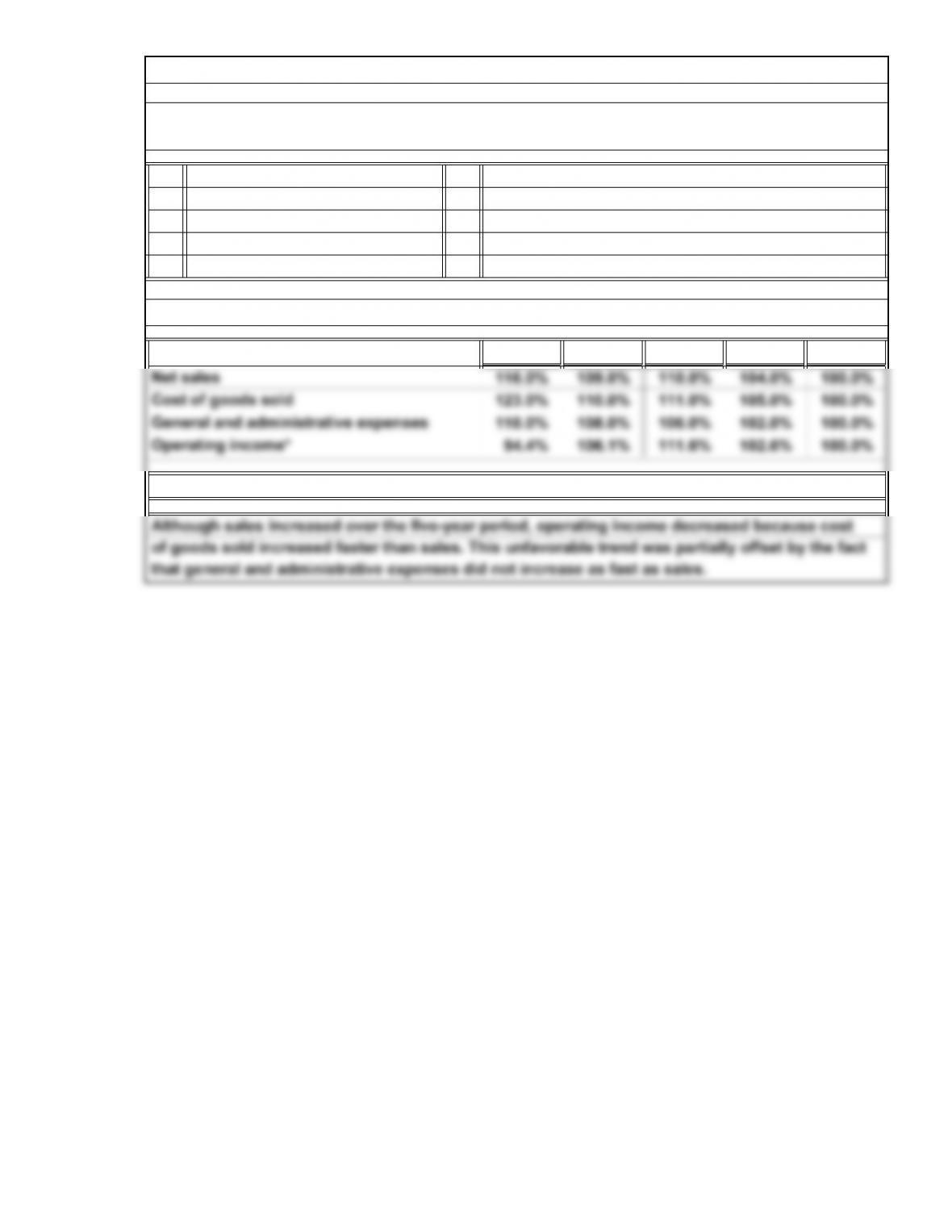

2014 2013 2012 2011 2010

*Rounded

Exercises: Set A

d

b

E2A. Trend Analysis

d

a

E1A. Issues in Financial Performance Evaluation: Objectives, Standards, Sources of Information,

and Executive Compensation

d

16-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

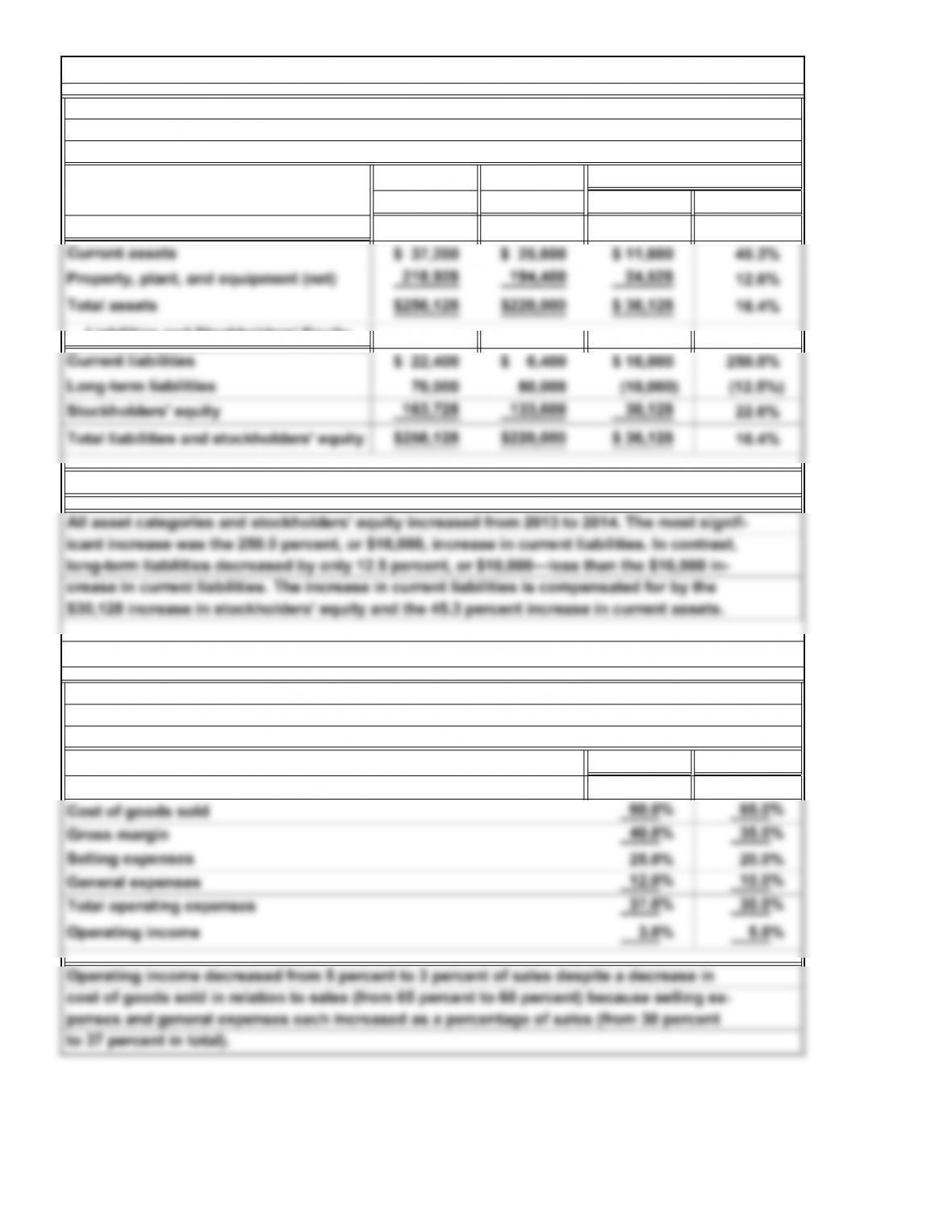

2014 2013 Amount Percentage*

2014 2013

100.0% 100.0%

crease in current liabilities. The increase in current liabilities is compensated for by the

All asset categories and stockholders’ equity increased from 2013 to 2014. The most signif-

icant increase was the 250.0 percent, or $16,000, increase in current liabilities. In contrast,

Comparative Balance Sheets

December 31, 2014 and 2013

Increase or Decrease

E3A. Horizontal Analysis

Rivera Company

*Rounded

Assets

Rivera Company

E4A. Vertical Analysis

For the Years Ended December 31, 2014 and 2013

Net sales

Common-Size Income Statements

16-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

++ ++

==

45.5=

times days*

$17,200

Quick ratio

times*

$40,000

$13,600

times=

$40,000 times

Receivables

turnover

2.2

$35,600

$28,200

1.6 times*

$7,200 $10,400

$28,200

3.0 4.0

76.2 days. This is a favorable development.

=

ratio (from 2.2 to 1.6). Also, its payables turnover and days’ payable were less favorable

6.58.0 56.2

in 2014 than in 2013. However, the operating cycle declined from 147.5 days (56.2 + 91.3)

orated, probably because of decreases in the current ratio (from 4.0 to 3.0) and the quick

Current ratio

2014

*Rounded

to 132.4 days (45.5 + 86.9). The required days of financing decreased from 94.6 days to

Although Posad Company’s receivables turnover, inventory turnover, days’ sales uncol-

lected, and days’ inventory on hand improved, its operating asset management deteri-

$44,800

2013

=

times days*

uncollected

E5A. Operating Asset Management Analysis

16-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

times=

times= –

times

profit margin (6.3 percent and 6.2 percent) because of an increase in asset turnover from

1.9 to 2.2 times.

E7A. Profitability and Total Asset Management Analysis

2013

2014

16-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

=

9.5

Price/earnings

(P/E) ratio

E8A. Financial Risk and Market Strength Ratios

Company B

However, in other respects Company A is more acceptable. For example, even though both

times) than Company A. Both of these measures indicate that investments in Company B,

Company B has a greater debt to equity ratio (1.2 versus 0.8) and a greater return on equity

*Rounded

B has a lower P/E ratio than Company A (9.5 compared to 12.5), and thus an investor in Com-

companies pay an $8 per share dividend, the dividend yield for Company A (10.0 percent) is

pany N obtains more underlying earnings per dollar invested than an investor in Company A.

=

better than that for Company B (8.4 percent) because the price of Company A’s stock ($80)

is less than that of Company B’s ($95). To reach a final decision, the investor must weigh

either bonds or stocks, may be more risky than similar investments in Company A. Company

ratio*

Return on

equity*

Company A

the relative risks and potential returns associated with each investment.

$106,920

= times

12.5 times $95.00

$10.00

$194,400

$6.40

$80

Interest

coverage ratio*

=

16-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(+) /2

=–– =

1.

( $47,500 – $45,000

2.

( $43,000 – $45,000

3.

4.

5.

E9A. Liquidity Analysis

=

$456,000

$456,000 15.2%

$352,000

$2,890,000

1.3

$456,000

$3,120,000

$456,000

=

=

$3,005,000

$298,000 $38,000$120,000

=

E10A. Effect of Alternative Accounting Methods

*Rounded

Cash flow yield

Cash flows to sales

Cash flows to assets

Free cash flow

$19,500

2,500

)

Net income under FIFO

$17,000Net income under average-cost method

Difference between FIFO and average-cost inventory

$15,000

(2,000)

Net income under LIFO

$17,000Net income under average-cost method

Difference between average-cost and LIFO inventory

)

Most accountants would consider the LIFO method the more conservative procedure

because it yields a lower asset value and a lower net income (in a period of rising

No, the choice of LIFO will not violate the consistency convention. Because this is

the company’s first year of operation, there has been no change in methods.

prices).

in the financial statements.

Yes, the full-disclosure convention requires disclosure of the inventory method used

= times*

$3,200,000

$456,000 14.3%*

*

16-17

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$3,800,000

2,100,000

$1,700,000

$ 100,000

80,000

180,000

$1,520,000

600,000

$ 920,000

(net of taxes, $60,000) $(100,000)

(70,000) (170,000)

$ 750,000

25,000

$ 775,000

Income taxes expense

Income from continuing operations

Cost of goods sold

Operating expenses:

Selling expenses

Stream Toy Corporation

Income from continuing operations before

Net sales

Total operating expenses

Income Statement

Discontinued operations:

E11A. Corporate Income Statement

Gross margin

Loss from operations of discontinued segment

For the Year Ended June 30, 2014

Administrative expenses

income taxes

Loss on disposal of segment (net of taxes, $26,000)

Income before extraordinary items

Extraordinary gain (net of taxes, $7,000)

Net income

16-18

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

$1,110,000

550,000

$ 560,000

(225,000)

(110,000)

$ 225,000

67,500

$ 157,500

(net of taxes, $48,000) $112,000

98,000 210,000

$ 367,500

50,400

$ 417,900

$0.79

1.05

$1.84

0.25

$2.09

Earnings per common share:*

Income from continuing operations

Discontinued operations (net of taxes)

Income before extraordinary items

Note to Instructor: Solutions for Exercises: Set B are provided separately on the Instructor’s

Extraordinary gain (net of taxes)

Net income

*Rounded

Gain on disposal of segment (net of taxes, $42,000)

Income before extraordinary items

Extraordinary gain on retirement of bonds (net of taxes,

$21,600)

Net Income

Income from continuing operations

Discontinued operations:

Income from operations of discontinued segment

Sales

Cost of goods sold

Gross margin

Operating expenses

Restructuring

Income from continuing operations before income taxes

Income taxes expense

Van Corporation

Income Statement

For the Year Ended December 31, 2014

Resource CD and website.

E12A. Corporate Income Statement

16-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2014 2013 Amount Percentage*

$3,276,800 $3,146,400 $130,400 4.1%

2,088,800 2,008,400 80,400 4.0%

$1,188,000 $1,138,000 $ 50,000 4.4%

Selling expenses $ 476,800 $ 518,000 $ (41,200) (8.0%)

Administrative expenses 447,200 423,200 24,000 5.7%

Total operating expenses $ 924,000 $ 941,200 $ (17,200) (1.8%)

$ 264,000 $ 196,800 $ 67,200 34.1%

65,600 39,200 26,400 67.3%

$ 198,400 $ 157,600 $ 40,800 25.9%

62,400 56,800 5,600 9.9%

$ 136,000 $ 100,800 $ 35,200 34.9%

$3.40 $2.52 $0.88 34.9%

Increase or Decrease

Cost of goods sold

Net income

Income from operations

Gross margin

Interest expense

Operating expenses:

Income before income taxes

Income taxes expense

For the Years Ended December 31, 2014 and 2013

Comparative Income Statements

Earnings per share

Problems

P1. Horizontal and Vertical Analysis

Obras Corporation

(in thousands of dollars)

*Rounded

Net sales

16-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.