Investments with a maturity of less than ninety days are generally classified as cash

equivalents.

Callable preferred stock is preferred stock that may be redeemed or retired at the option

of the issuing corporation.

Under the perpetual inventory system, cost of goods sold is not recorded until the end

of the accounting period.

Most public companies issue interim financial statements to the public on a quarterly

basis.

Unrealized Loss (Gain) on Short-Term Investments is a contra-asset account that will

appear on the balance sheet.

When a company records the purchase of 1 month of prepaid expense the transaction

does not affect the totals of assets or liabilities and owner’s equity.

Bondholders are creditors of the issuing corporation.

Treasury stock is reported as an asset on the balance sheet because treasury shares may

be sold later.

The amount placed opposite the owner’s Capital account in the Balance Sheet columns

of the work sheet is the amount to be reflected for owner’s Capital on the balance sheet.

Depreciation Expense–Equipment is an example of a contra account.

Income and losses are divided equally among the partners unless the partnership

agreement specifies otherwise.

The first step in the accounting cycle is to post the journal entries to the ledger and

prepare a trial balance.

Under the partnership form of business, it may be difficult to raise large amounts of

capital.

Accountants consider money the common unit of measure for all business transactions.

In periods of falling prices, LIFO will result in a higher ending inventory valuation than

FIFO.

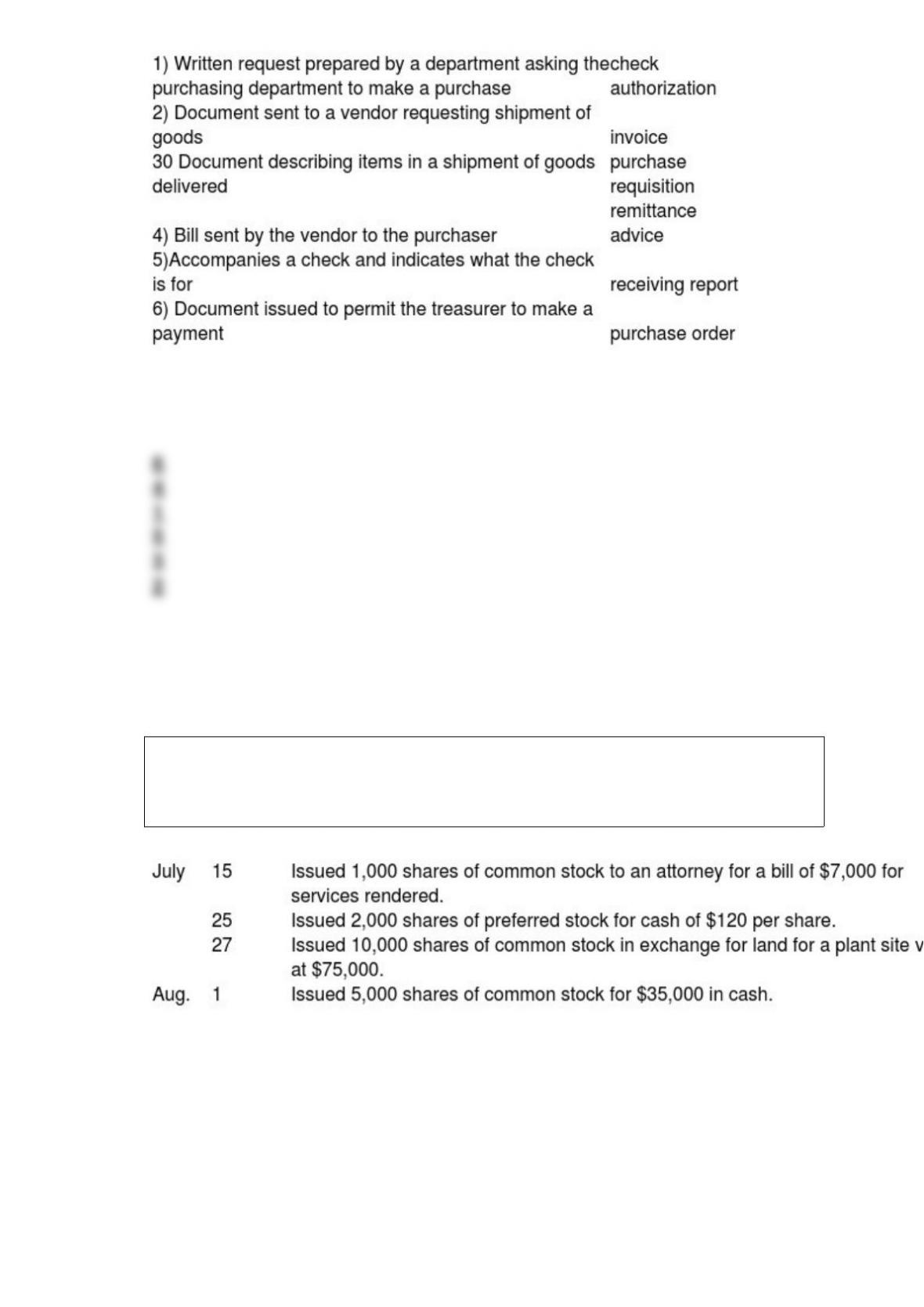

A remittance advice accompanies a check sent to a vendor or the vendor’s bank.

Determining the percentage change in an item from one year to the next is a type of

horizontal analysis.

When a business sells an item and collects a state sales tax on it, a current liability to

the state arises.

The use of salaries in the allocation of income or loss allows for the differences in the

services that partners provide the business.

Available-for-sale securities may only be classified as short-term investments.

No entry is required on the date of payment for a cash dividend.

Return on equity equals net income divided by average stockholders’ equity.

When the existing partners pay a bonus to a newly admitted partner, the existing

partners’ accounts are debited.

Under the perpetual inventory system, the return of goods from a customer is recorded

with a debit to Sales Returns and Allowances.

The timing of cash flows is critical to a company’s ability to maintain adequate liquidity

so that it can pay its bills on time.

When the estimates involved in earnings management begin moving outside a

reasonable range, the financial statements can become misleading.

Goods held on consignment should be included in the consignee’s ending inventory.

The purchase of land with cash would be disclosed on the statement of cash flows.

An advantage of the single-step income statement is that it is less complex than the

multistep form.

Under the allowance method, Uncollectible Accounts Expense is not recorded when an

individual customer defaults.

The cost of land would include the cost of a building purchased with the land and torn

down because it was not needed.

Financial position may be assessed by referring to a balance sheet.

Write-downs and restructurings increase current operating income and decrease future

income by shifting future costs to the future periods.

Annual reports of public companies will include statements from both management and

independent auditors regarding the adequacy of internal control.

Freight paid on goods shipped to customers is classified as a selling expense.

Asset turnover is most closely associated with a company’s liquidity position.

An informational tax return must be filed for a partnership.

Liquidity means not having enough funds on hand to pay debts when they fall due.

Corporations are subject to more government control and regulation than are other

forms of business.

The production method is an accelerated method of depreciation.

In preparing closing entries, which of the following columns of the work sheet are the

most helpful?

A. Adjusted Trial Balance columns

B. Income Statement columns

C. Adjustments columns

D. Balance Sheet columns

In the journal provided, prepare year-end adjustments for the following situations. Omit

explanations.

a. Accrued interest on notes receivable is $105.

b. Of the $12,000 received in advance of earning a service, two-thirds was still

unearned by year end.

c. Two years’ rent, totaling $36,000, was paid in advance at the beginning of the year.

d. Services totaling $5,300 had been performed, but not yet billed.

e. Depreciation on trucks totaled $3,400 for the year.

Positive operating income will result if gross margin exceeds

A. operating expenses.

B. purchases.

C. cost of goods sold.

D. cost of goods sold minus operating expenses.

All of the following are examples of internal control activities except

A. adequate supervision.

B. rotation of key personnel.

C. customer satisfaction surveys.

D. insistence that employees take earned vacations.

The responsibility for receiving the proper amount of interest falls on the bondholder

most heavily in the case of

A. term bonds.

B. serial bonds.

C. coupon bonds.

D. registered bonds.

Which of the following should be classified as a current asset?

A. Supplies

B. Trademark

C. Equipment

D. Land held for future use

The purchase and sale of debt and equity securities would appear in which section of

the statement of cash flows?

A. Operating activities

B. Investing activities

C. Financing activities

D. Noncash investing and financing activities

The Sarbanes-Oxley Act of 2002 applies to all except

A. quarterly statements

B. annual reports

C. internal management reports

D. none of these are exceptions

A good system of internal control is designed to achieve all of the following except

A. efficiency of operations.

B. reliability of financial reporting.

C. compliance with relevant laws and regulations.

D. attainment of target sales.

Which of the following would not be a valid reason for keeping currency on hand at a

place of business?

A. To pay small, unforeseen expenses

B. To make up for any imbalance in the books

C. To advance money to sales reps for travel expenses

D. To provide money for cash registers

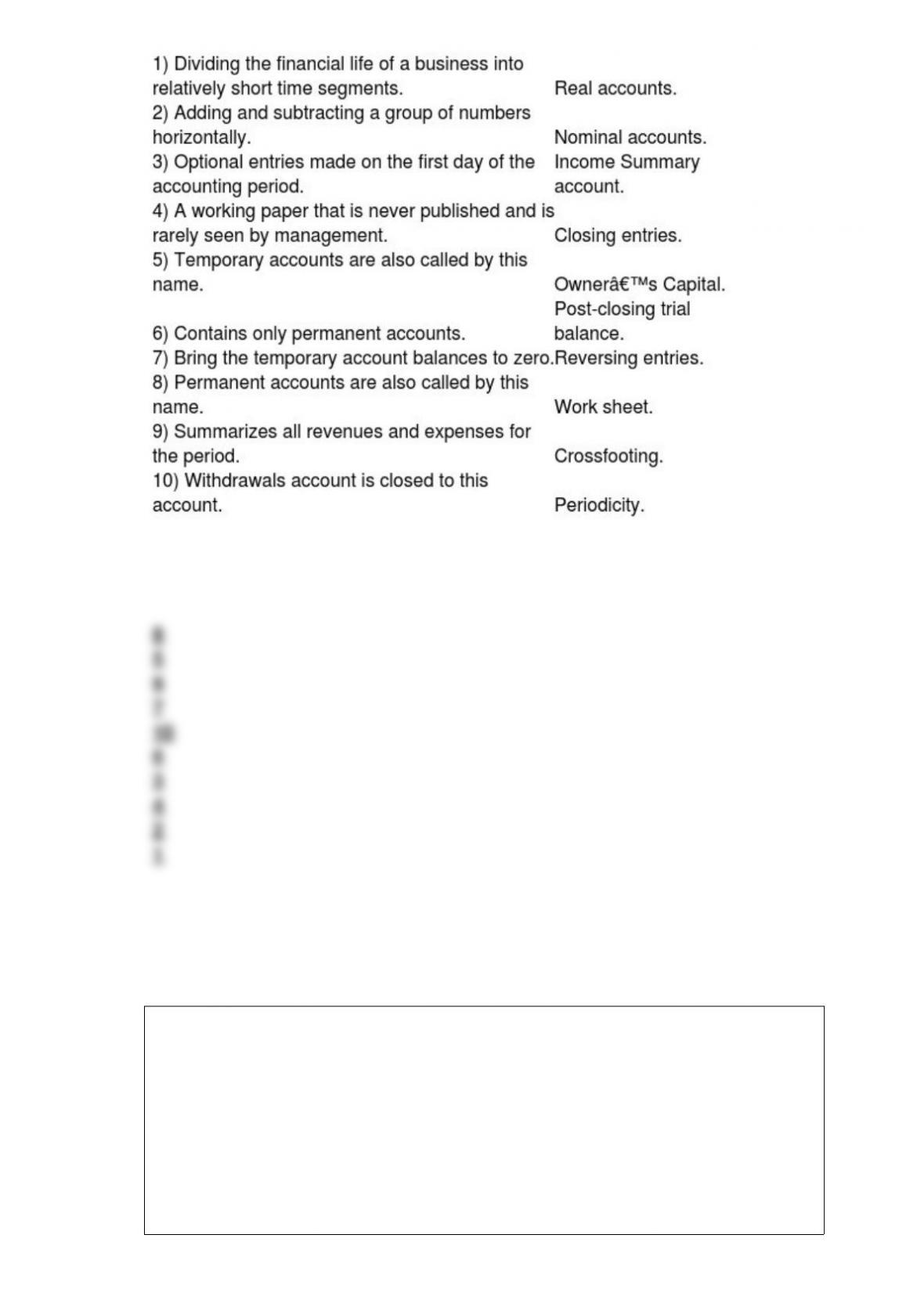

Match the itmes (a) – (q) to the appropriate description below.

On January 2, 20×5, Fresh Inc. issued 20-year bonds payable with a face value of

$1,000,000 and a face interest rate of 10 percent. The bonds were issued to yield a

market interest rate of 9 percent. Interest is payable semi-annually on January 1 and

July 1. In calculating the present value of the bond issue of January 2, 20×5, the factor

used to calculate the present value of the $1,000,000 is

A. 10%, 20 periods

B. 5%, 40 periods

C. 9%, 20 periods

D. 4.5%, 40 periods

Trading securities are valued on the balance sheet at

A. lower of cost or market.

B. cost.

C. market value.

D. cost, adjusted for the effects of interest.

The controller for Tires and More, Inc. has recorded the following transactions during

the month: the purchase of supplies on credit, $4,200; receipt of a bill for utilities for

the month which is due on the 15th of the next month, $1,200; and, partial payment on

the balance due for supplies, $800. What is the balance in the Accounts Payable account

at the end of the month assuming a beginning balance of $0, and is the balance a debit

or a credit?

A. $4,600 debit.

B. $4,600 credit.

C. $3,400 credit.

D. $5,400 credit.

An adjusting entry can include a debit to a(n)

A. expense and a credit to an asset.

B. cash and a credit to a revenue.

C. liability and a credit to cash.

D. liability and a credit to an asset.

The amount of cost of goods available for sale during the year depends on the amounts

of

A. beginning merchandise inventory, net cost of purchases, and ending merchandise

inventory.

B. beginning merchandise inventory and cost of goods sold.

C. beginning merchandise inventory, cost of goods sold, and ending merchandise

inventory.

D. beginning merchandise inventory and net cost of purchases.

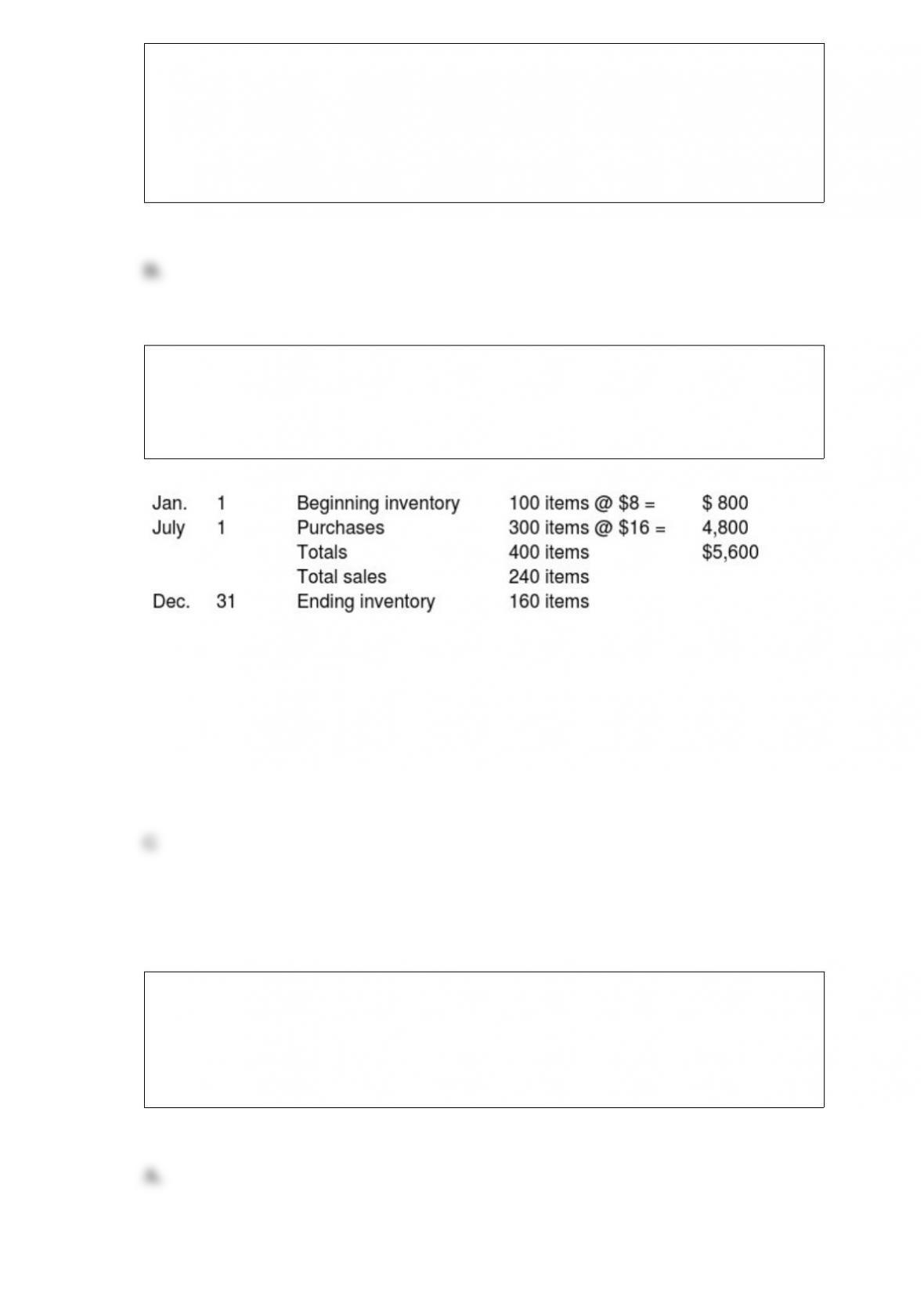

Given the following information about purchases and sales during the year, compute the

cost to be assigned to ending inventory under each of three methods: (a) average-cost,

(b) FIFO, and (c) LIFO. (Show your work.)

Assuming that a periodic inventory system is used

a. Average-cost: $2,240 ($5,600 400 160)

b. FIFO: $2,560 (160 $16)

c. LIFO: $1,760 [(100 $8) + (60 $16)]

Failure to record a liability probably will

A. result in an overstated net income.

B. result in overstated total liabilities and stockholders’ equity.

C. have no effect on net income.

D. result in overstated total assets.

Which of the following will not result in dissolution of a partnership?

A. Death of a partner

B. Withdrawal of a partner

C. Admission of a new partner

D. Sale of partnership assets

When the equity method is used to account for a long-term investment in the stock of

another company, the carrying value of the investment is affected by

A. declines in the market value of the stock.

B. the earnings and dividends of the investee.

C. an excess of market price over cost.

D. neither the earnings nor the dividends of the investee.

The Sarbanes-Oxley Act of 2002 does not apply to

A. public companies with assets over $300 million.

B. public companies with assets under $1 million.

C. privately owned companies.

D. companies established after 2002.

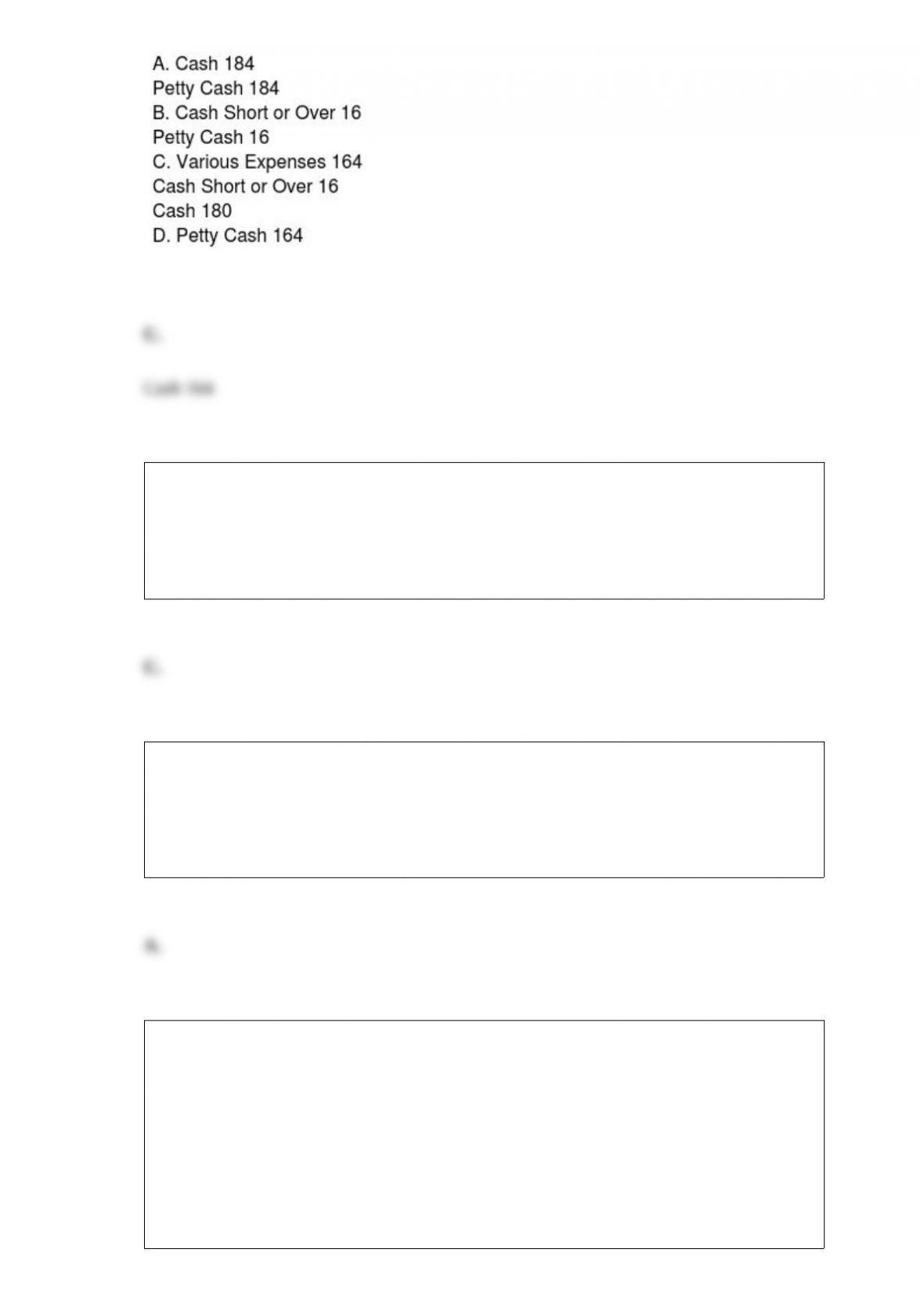

A $200 petty cash fund has cash of $20 and valid receipts of $164. The entry to

replenish the fund would be:

Which of the following is an illustration of the classification issue?

A. At what amount should land be shown on the balance sheet?

B. At what point should the payment of salaries to employees be recorded?

C. Should supplies be recorded as an asset or as an expense?

D. At what point should a bill be paid for the purchase of an item?

The number of days’ spayable uncollected is determined by dividing

A. the number of days in a year by the payables turnover.

B. the number of days in a year by average accounts payable.

C. cost of goods sold by average accounts payable.

D. inventory by average accounts payable.

You have just received notice that Agnes Fisher, a customer of yours with an Accounts

Receivable balance of $200, has gone bankrupt and will not be making any future

payments. Assuming you use the allowance method, the journal entry you make is to

A. debit Uncollectible Accounts Expense and credit Accounts Receivable.

B. debit Allowance for Uncollectible Accounts and credit Uncollectible Accounts

Expense.

C. debit Uncollectible Accounts Expense and credit Allowance for Uncollectible

Accounts.

D. debit Allowance for Uncollectible Accounts and credit Accounts Receivable.

A partnership agreement most likely will stipulate that assets be reappraised when

A. a new partner is admitted to the partnership

B. a partner leaves the partnership

C. profits and losses are being distributed

D. the partnership is liquidated

As the usefulness of a plant asset expires,

A. an amount is transferred from one asset account to another.

B. a related expense account is reduced.

C. a liability is created.

D. the cost of the asset is allocated to an expense account.

If an adjusting entry is not made at the end of an accounting period to remove the

earned revenue from the Unearned Revenue account,

A. assets would be understated.

B. owner’s equity would be overstated.

C. liabilities would be understated.

D. liabilities would be overstated.

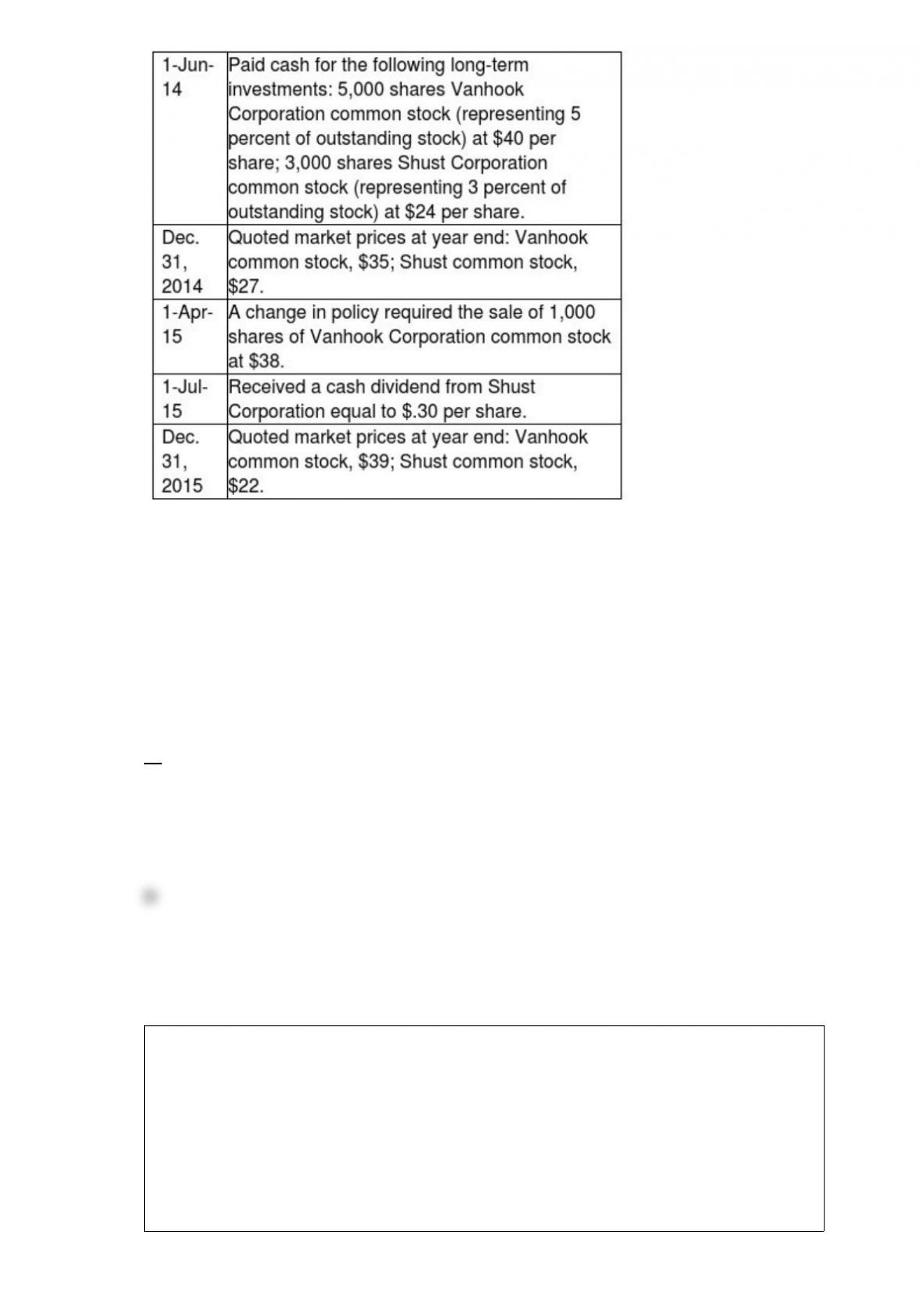

Use this information to answer the following question. These facts concern the

long-term stock investments of DeBord Corporation:

The entry to adjust the Allowance to Adjust Long-Term Investments to Market in 2015 is:

A. Unrealized Loss on Long-Term Investments 6,000

Allowance to Adjust Long-Term Investment to Market 6,000

B. Allowance to Adjust Long-Term Investment to Market 10,000

Unrealized Loss on Long-Term Investments 10,000

C. Unrealized Loss on Long-Term Investments 10,000

Allowance to Adjust Long-Term Investment to Market 10,000

D. Allowance to Adjust Long-Term Investment to Market 6,000

Unrealized Loss on Long-Term Investments 6,000

An adjusting entry was made on the last day of the previous fiscal year debiting

Accounts Receivable and crediting Service Revenue. If a reversing entry has been

made, then at the time of cash collection

A. the accountant needs to find out how much of the cash collection applies to the

current period and how much applies to the previous period.

B. the accountant will debit Accounts Receivable and credit Service Revenue.

C. the accountant will debit Cash and credit Service Revenue.

D. the accountant will debit Service Revenue and credit Cash.

Shares of treasury stock are

A. issued shares that have been bought back by the corporation and are being held by

the corporation.

B. shares held by the U.S. Treasury Department.

C. part of the total outstanding shares but not part of the total issued shares of a

corporation.

D. unissued shares that are held by the treasurer of the corporation.

List five possible users of a set of financial statements and state what each would be

interested in learning from its review.

Prepare journal entries for the following transactions involving notes payable for

Homer Company, whose fiscal year ends June 30. Omit explanations.

The following facts pertain to the stockholders’ equity section of the balance sheet of

Avenida Corporation:

During 20×5, Avenida declared and distributed a stock dividend. Also during 20×5,

Avenida declared and paid cash dividends of $17,000. There were no changes in the

number of shares of stock issued and outstanding during the period except for the change

caused by the stock dividend. Calculate the amount of net income reported by Avenida for

20×5.

Justin and Nicole are forming a partnership. What are some of the factors they should

consider in deciding how income might be divided?

How is it possible for a company to show a net loss for a given year, yet produce

positive net cash flows from operating activities?

Match each description with the document it is describing.

Marianna Corporation is authorized to issue 100,000 shares of $5 stated value common

stock and 2,000 shares of $100 par value, 6 percent preferred stock. Prepare entries in

journal form without explanations to record the following transactions:

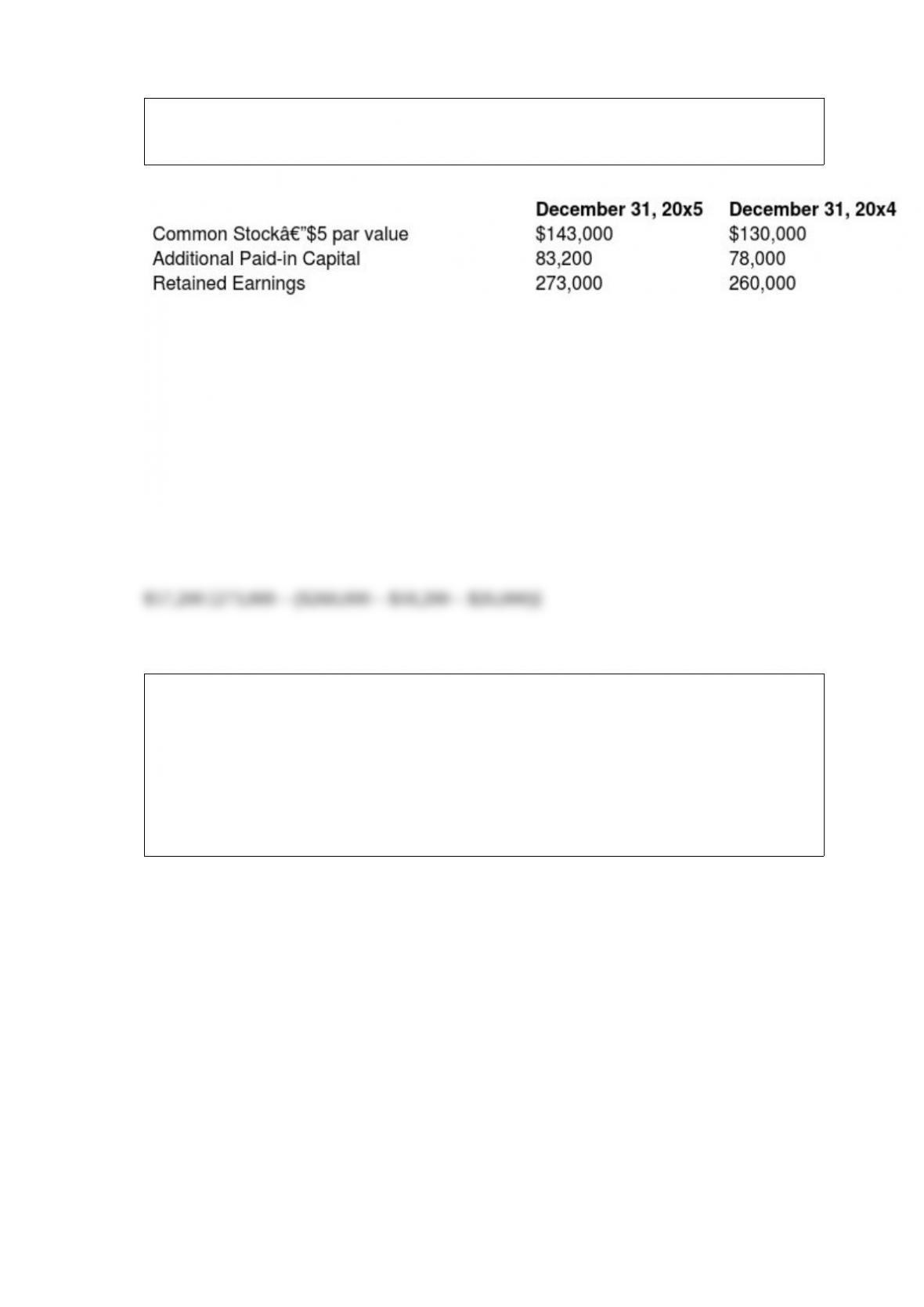

The following facts pertain to the stockholders’ equity section of the balance sheet of

Charlotte Corporation:

During 20×5, Charlotte declared and distributed a stock dividend. Also during 20×5,

Charlotte declared and paid cash dividends of $26,000. There were no changes in the

number of shares of stock issued and outstanding during the period except for the change

caused by the stock dividend. Calculate the amount of net income reported by Charlotte for

20×5.

On January 1, 20×5, Becky Bishop Fashion Company issued ten-year, 8 percent bonds

with a face value of $500,000. The semiannual interest dates are June 30 and December

31. The bonds were issued for $437,740 to yield an effective annual rate of 10 percent.

The accounting year ends on December 31. Prepare entries in journal form without

explanations to record the bond issue on January 1, 20×5, and the payments of interest

and amortization of discount on June 30 and December 31, 20×5. Use the effective

interest method of amortization. Round answers to the nearest dollar.

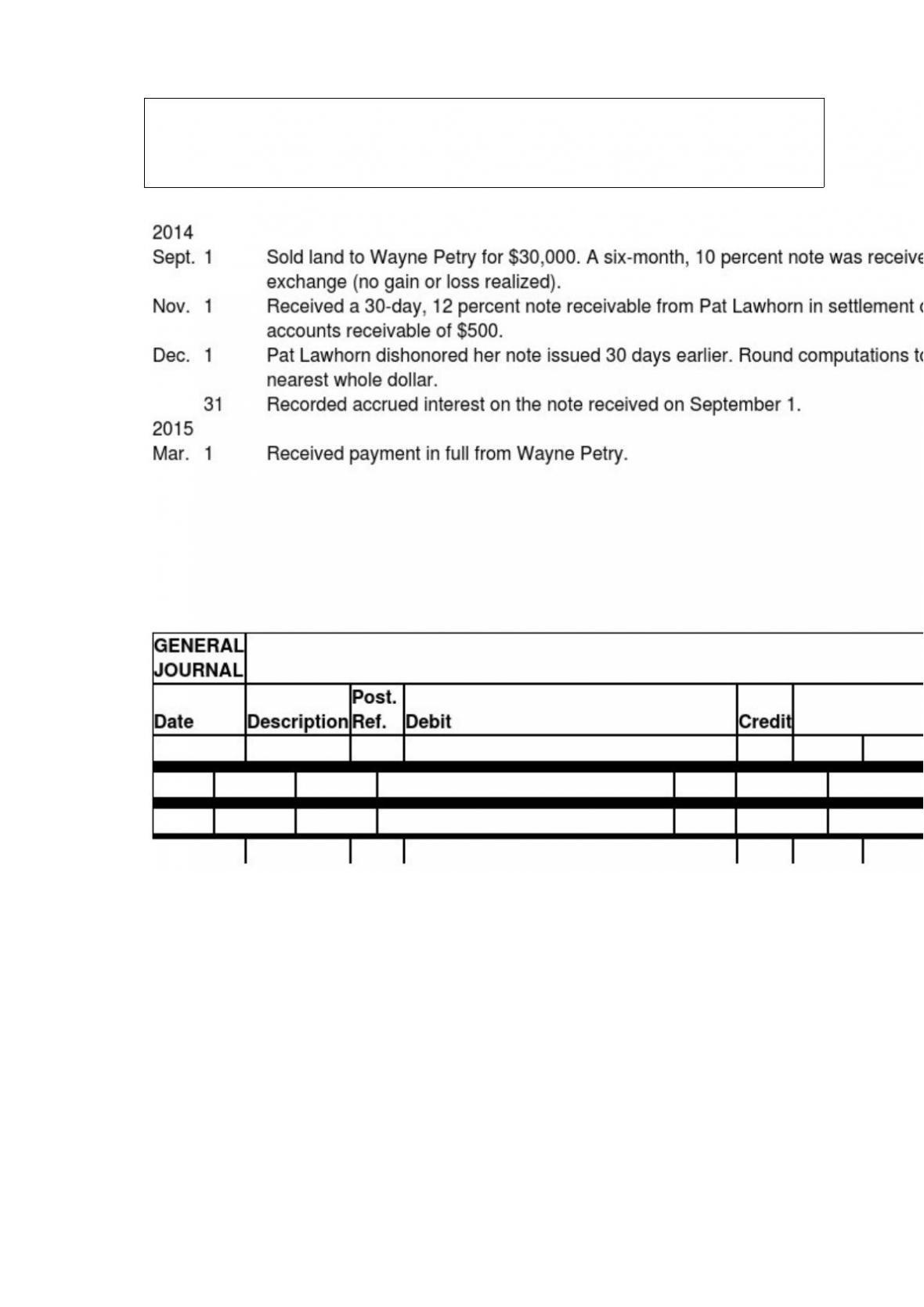

Brashear Corporation engaged in the following transactions involving promissory notes

in 2014 and 2015. Journalize these transactions in the journal provided. (Omit

explanations.) Round to nearest whole dollar.

At year end, Korkin Design Company has a $900 credit balance in Allowance for

Uncollectible Accounts. If an accounts receiving aging method analysis indicates that

an estimated $5,700 of year-end receivables are uncollectible, what will be the balance

in Allowance for Uncollectible Accounts after the appropriate adjusting entry for

uncollectible accounts has been made? Indicate if the balance is a debit or credit.

The following amounts are taken from the balance sheets of Baltic Company:

During 20×5, expenses related to accrued liabilities were $15,250, and expenses related to

prepaid expenses were $10,500.

If the purchase of machinery is treated incorrectly as a revenue expenditure, what will

be the effect on net income and total assets in the year of purchase and in the following

year, and why?

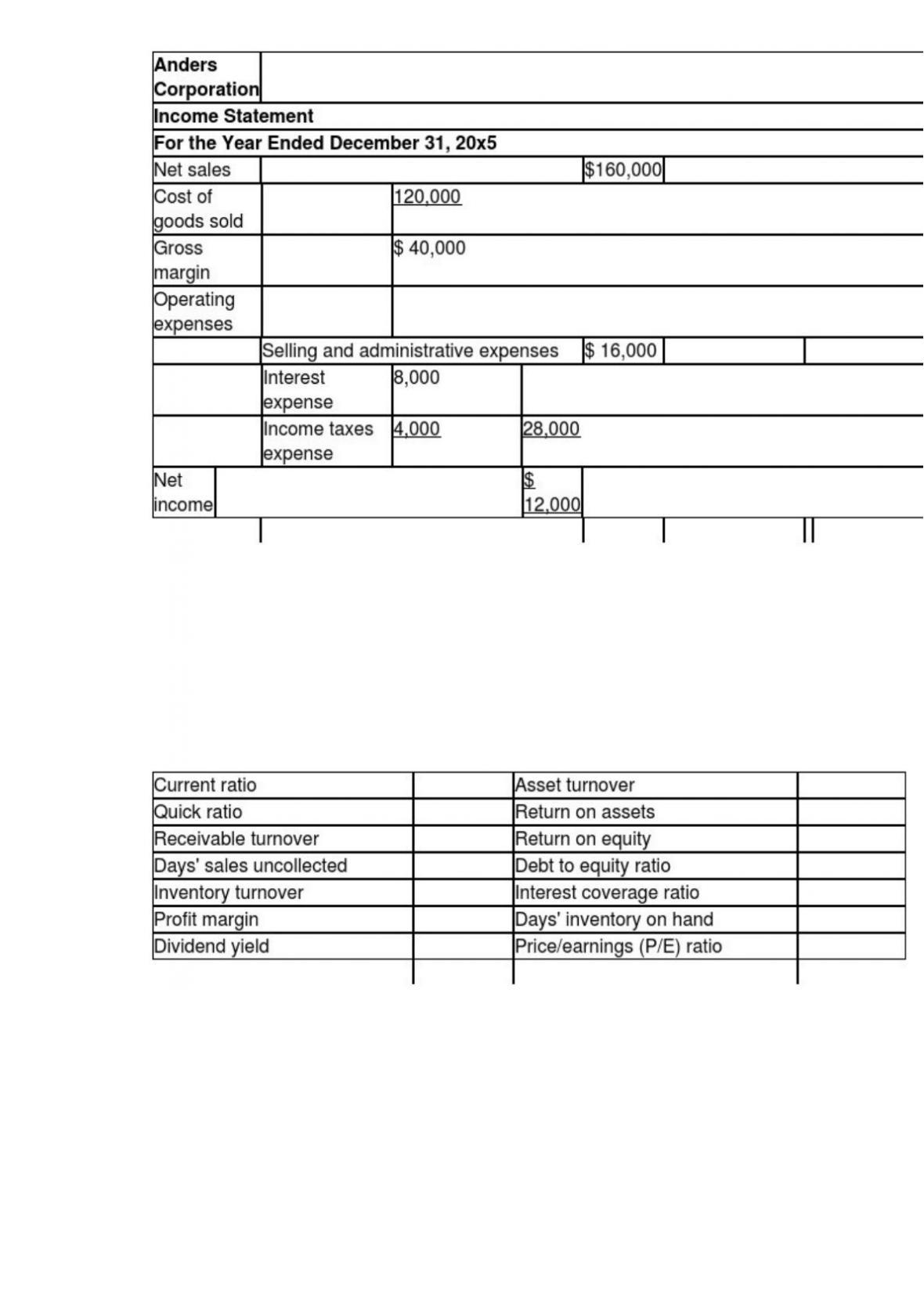

From the following information, compute the ratios indicated and place the proper

numbers in the spaces provided. Assume the average for the year is the same as the

ending balances for the balance sheet accounts. Round answers to one decimal place,

and show your work.

Anders had 4,000 shares of common stock issued and outstanding. The market price of

common stock at year end was $15.00 per share. Dividends paid in 20×5 were $0.60 per

share.

Prepare entries in journal form without explanations to record the following

transactions involving Wildflower Corporation’s $5 par value common stock: