×11 /×/=

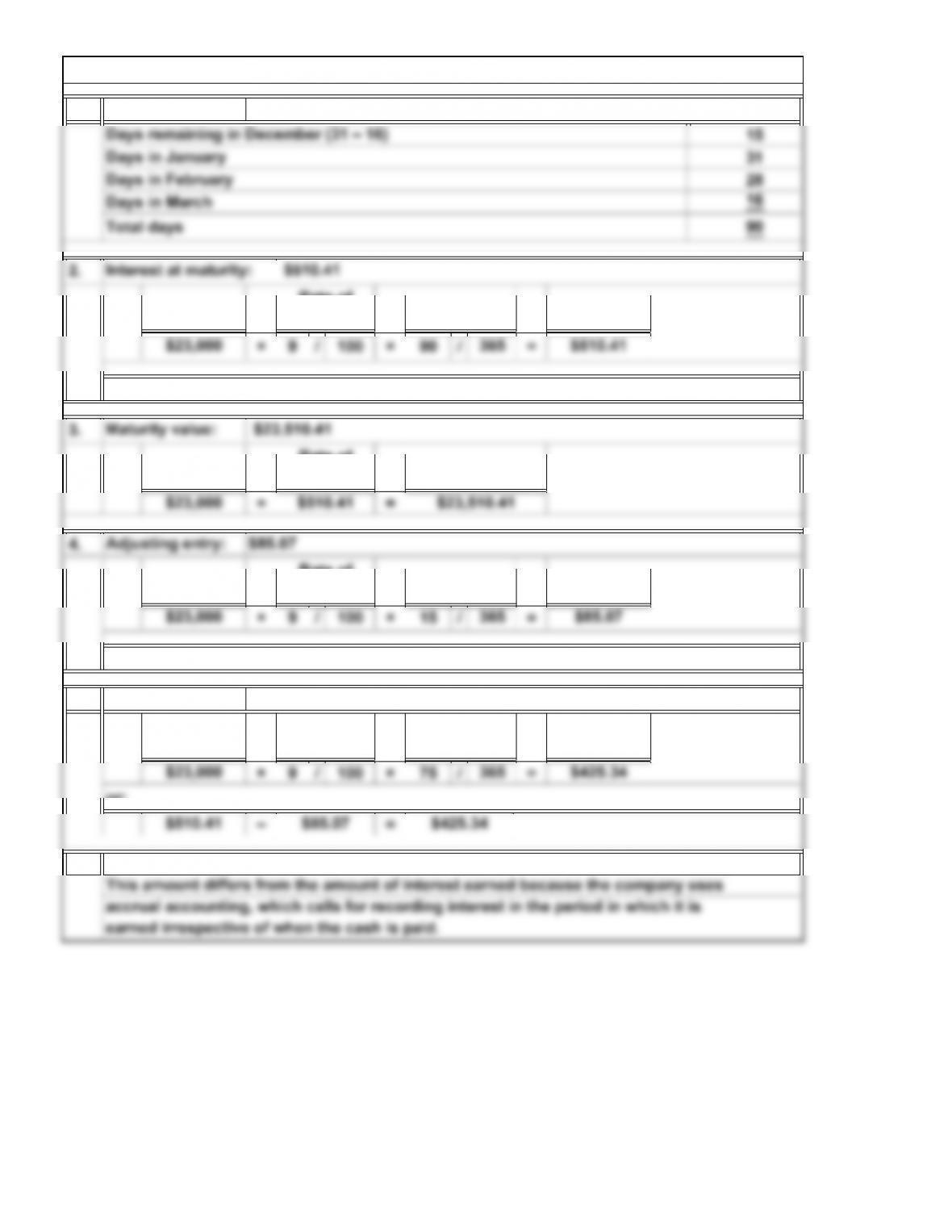

2.

3.

0

100

Days remaining in May (31 – 31)

Days in June

Principal

31

30

Days in July

Interest at maturity:

$3,856.44

Time =

Since interest income on these notes receivable will not be paid until maturity, the

cash flow impact on June 30 is zero.

Interest*

Rate of

Interest

Interest

*Rounded

Maturity value: $61,627.40

Maturity Value

Interest*

P3. Notes Receivable Calculations (Concluded)

Principal

$60,000

××

Rate of

Interest Time =

May 31, accepted $60,000, 90-day, 11% note receivable

Maturity date:

+

36590

August 29

×

×

$1,627.40

=

$1,627.40

Principal

*Rounded

Date of

Note

Accrued interest income as of June 30

9-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

Principal

×

P4. Notes Receivable Calculations

Maturity date: March 16

earned irrespective of when the cash is paid.

accrual accounting, which calls for recording interest in the period in which it is

Rate of

Interest ×Time

= Interest*

*Rounded

9-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2. a.

×

b.

‒

‒

4,300

Accounts Receivable

Bal.

= Net Credit Sales 1.6 percent

$231,748

Uncollectible Accounts Expense

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

Accounts Receivable, Net

Percentage of net sales method:

=

P5. Methods of Estimating Uncollectible Accounts and Receivables Analysis

$20,000

=

Alternate Problems

Accounts receivable aging method:

=

$20,000

= $4,300

$254,000

$15,700

$20,000

=

9-21

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3. –

4.

to estimate uncollectible accounts is to consider the portion of the accounts receiv-

Underlying the percentage of net sales method is the assumption that the best way

to estimate uncollectible accounts is to consider a portion of every sales dollar to

be an amount that will not be collected. This is known as an income statement

approach.

Underlying the accounts receivable aging method is the assumption that the best way

Because the percentage of net sales method and the accounts receivable aging

in this case has a credit balance.

able now existing that may not be collected. This is a balance sheet approach.

P5. Methods of Estimating Uncollectible Accounts and Receivables Analysis (Concluded)

Receivables Turnover =

***Rounded

$1,195,000

$73,000

9-22

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

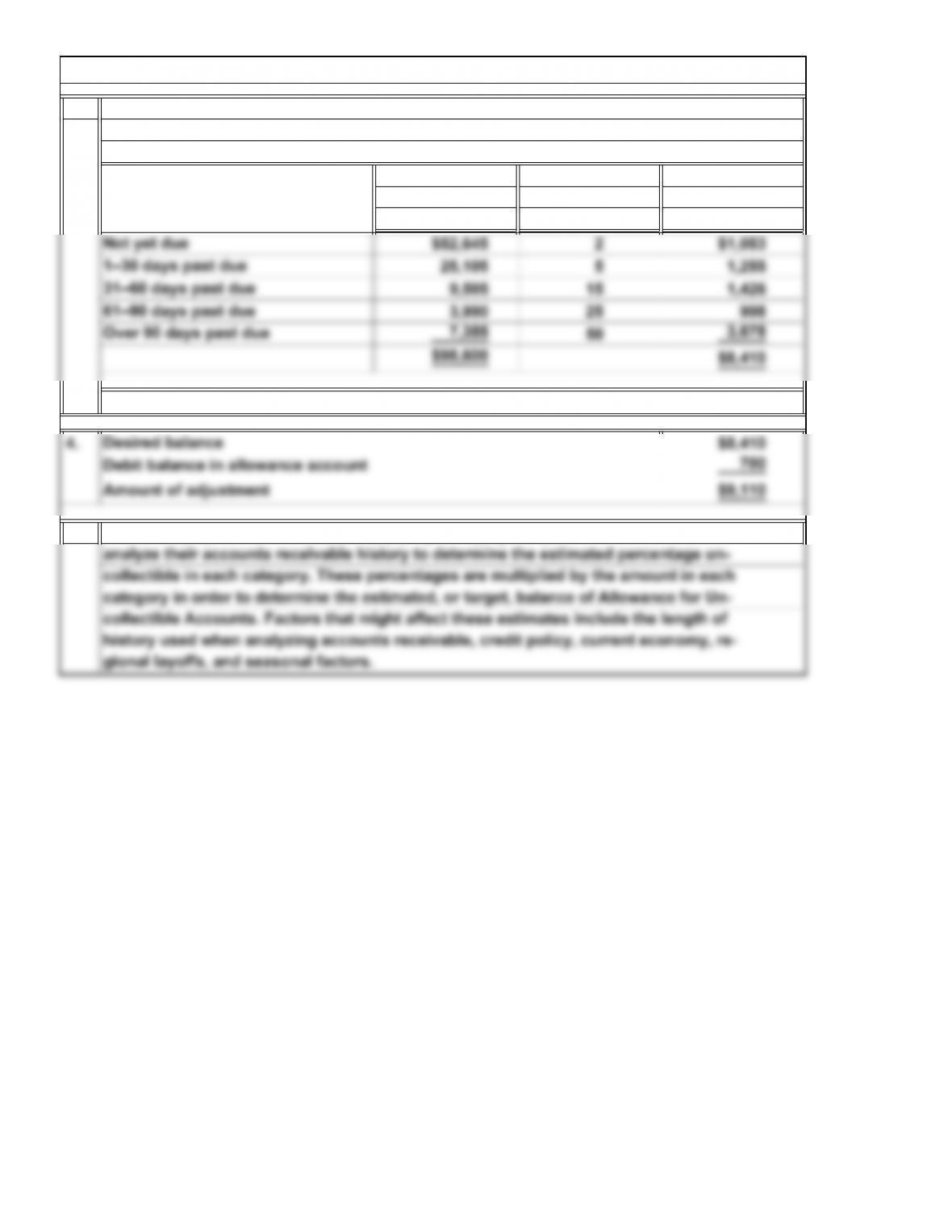

1.

1–30 31–60 61–90 Over

Not Yet Days Days Days 90 Days

Total Due Past Due Past Due Past Due Past Due

2.

Customer

P6. Accounts Receivable Aging Method

Account

Flossmoor Company

Aging Analysis of Accounts Receivable

December 31, 2014

Balance

Accounts Receivable

9-23

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

Percentage Allowance for

Considered Uncollectible

Amount Uncollectible Accounts*

5.

P6. Accounts Receivable Aging Method (Concluded)

Estimates play an important role in applying the aging analysis method. Businesses

Flossmoor Company

December 31, 2014

Estimated Uncollectible Accounts

9-24

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

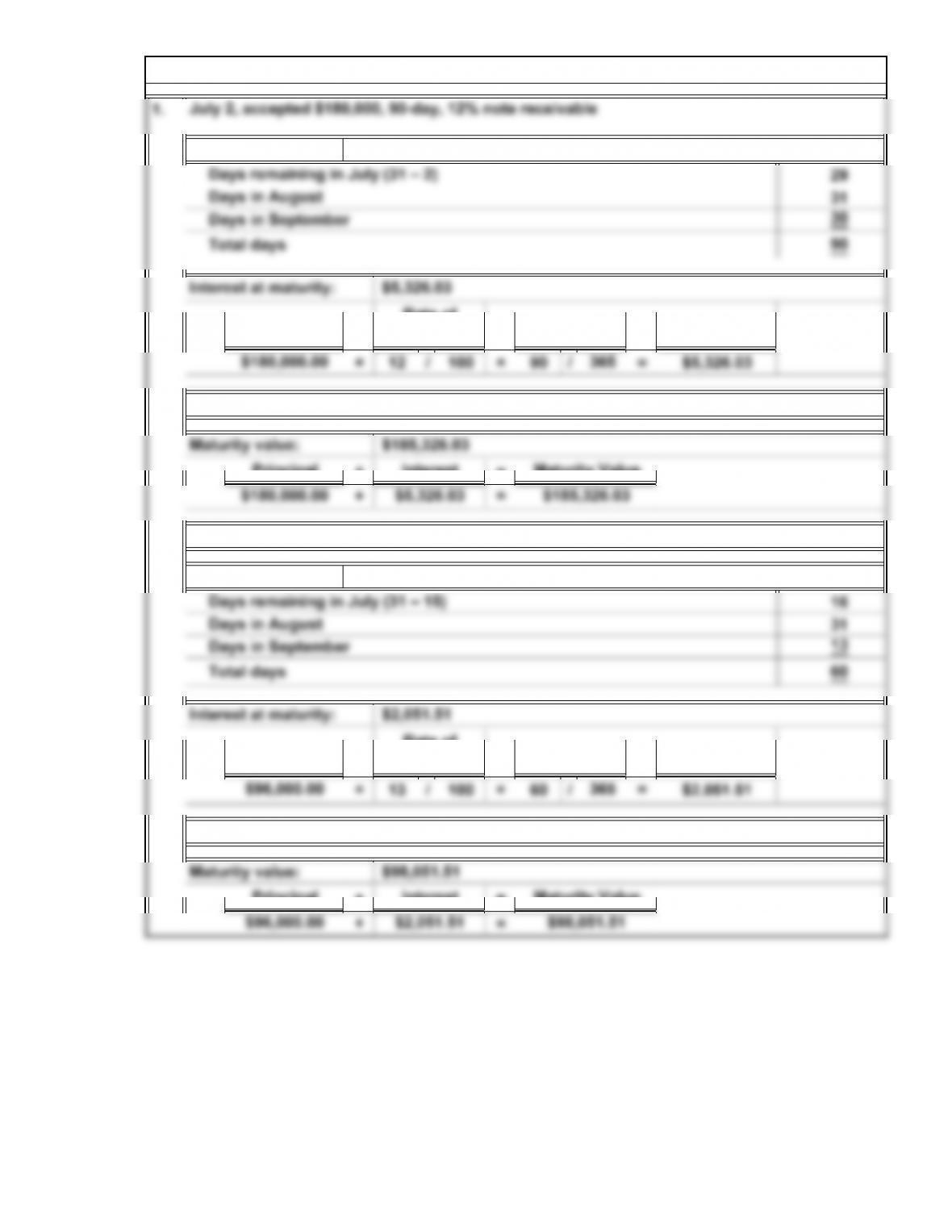

P7. Notes Receivable Calculations

Principal

=+

Maturity Value

Interest

September 30Maturity date:

9-25

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2.

3.

Date of

Note

Since interest income on these notes receivable will not be received until maturity,

Interest*

P7. Notes Receivable Calculations (Concluded)

Accrued interest income as of August 31

Rate of

Interest TimePrincipal ×=

October 28Maturity date:

July 30, accepted $90,000, 90-day, 11% note receivable

*Rounded

*Rounded

×

9-26

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

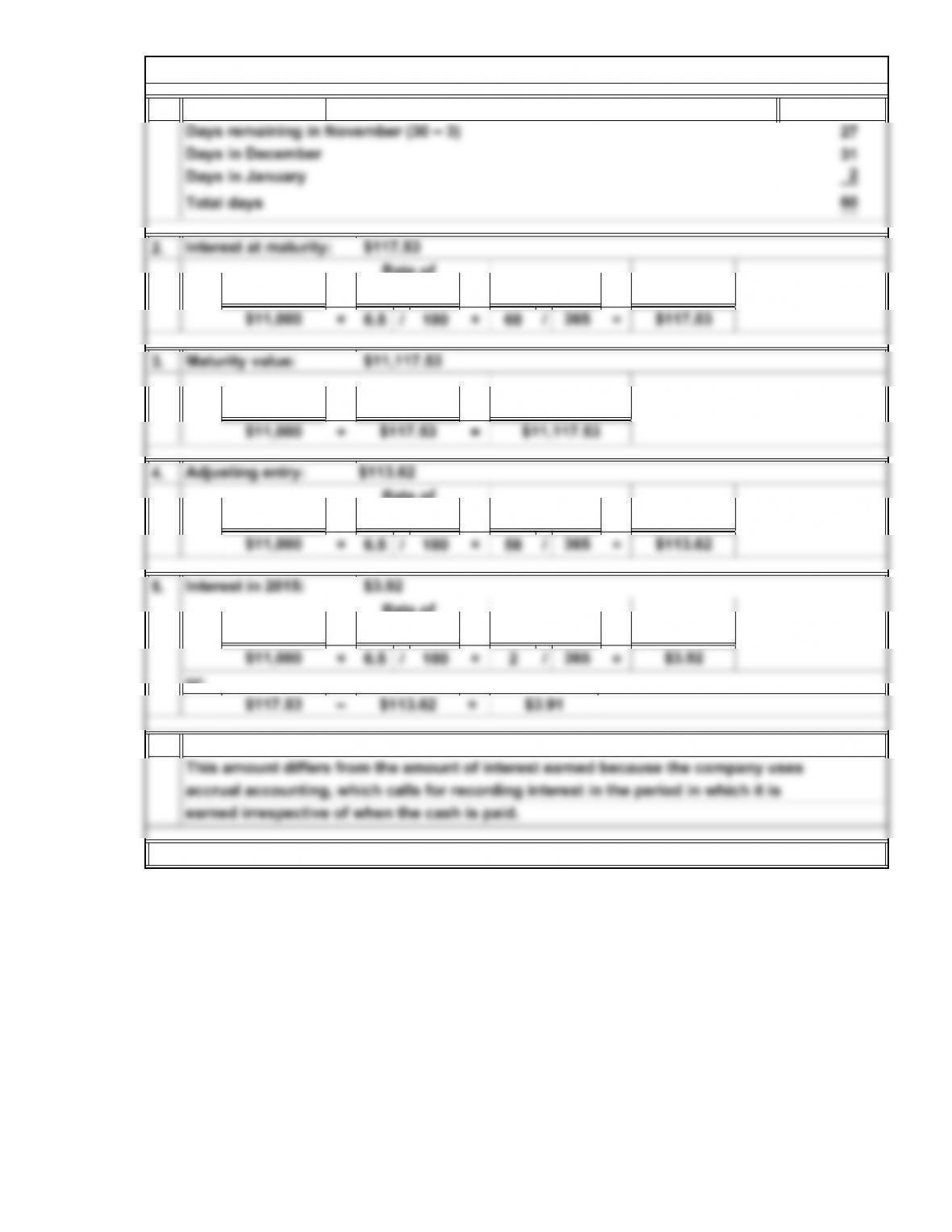

1.

2.

4.

–=

6.

Interest at maturity: $117.53

Adjusting entry: $113.62

Zero cash will be received in 2014 because the interest is due at the date of maturity.

*Differences in calculations due to rounding.

P8. Notes Receivable Calculations

January 2Maturity date:

Rate of

Interest

×TimePrincipal ×

=Interest*

Rate of

Interest

Principal ×

Interest*

×Time =

$117.53 $113.62 $3.91

or:

9-27

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.