Closing entries are made

A. to clear revenue and expense accounts of their balances.

B. to clear withdrawals of its balance.

C. to summarize a period’s revenues and expenses.

D. All of these choices.

Assume a company uses the periodic inventory system and has a beginning

merchandise inventory balance of $10,000, purchases of $150,000, and sales of

$250,000. The company closes its records once a year on December 31. In the

accounting records, the merchandise inventory account would be expected to have a

balance on December 31 prior to adjusting and closing entries that was

A. indeterminate.

B. less than $5,000.

C. more than $5,000.

D. equal to $5,000.

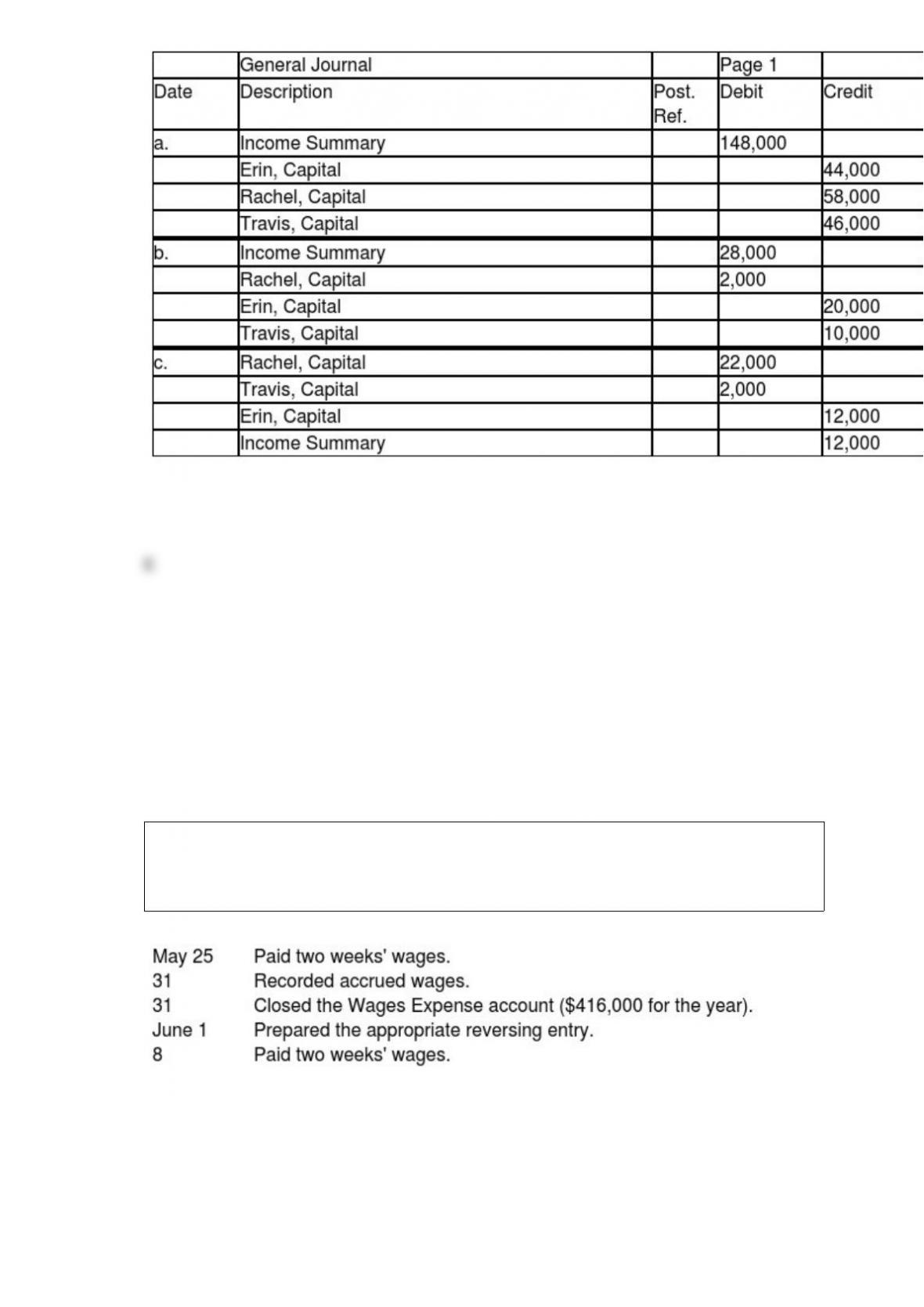

Erin, Rachel, and Travis are partners in ERT Company, with average capital balances

for the year of $60,000, $80,000, and $40,000, respectively. They share remaining

income and losses in a 2:5:3 ratio, respectively, after each receives a $30,000 salary and

10 percent interest on his or her average capital balance. In the journal provided,

prepare the entries without explanations to close income or loss into their Capital

accounts, assuming (a) net income of $148,000, (b) net income of $28,000, and (c) net

loss of $12,000.

K & K Enterprises pays wages of $16,000 every other Friday ($1,600 per weekday).

a. In the journal provided, prepare the following entries for the fiscal year ended May

31, 20×5 (omit explanations):

b. What would the June 8 entry be if no reversing entry was made?

In a common-size income statement for a retail store, the 100 percent amount is for

A. net revenues.

B. cost of goods sold.

C. gross profit.

D. net income.

Camp Corporation purchased 8,000 shares of Tent Corporation common stock for $80

per share on January 1, 2014. Tent reported net income of $220,000 for 2014 and paid

dividends of $90,000 during 2014. As of December 31, 2014, the market value of Tent

Corporation common stock was $80 per share. Assuming the shares owned by Camp

represent 30 percent of the total outstanding stock of Tent, the entry to record the

recognition of income by Camp Corporation is:

A. Cash 66,000

Dividend Income 66,000

B. Investment in Tent Corporation 220,000

Income, Tent Corporation Investment 220,000

C. Investment in Tent Corporation 66,000

Income, Tent Corporation Investment 66,000

D. Investment in Camp Corporation 66,000

The Equipment account would include all of the following costs except

A. installation costs.

B. maintenance costs.

C. equipment test runs.

D. freight charges.

An advantage of the corporate form of business is

A. separation of ownership and control.

B. tax treatment.

C. lack of mutual agency.

D. government regulation.

When a statement of cash flows is prepared using the direct method,

A. net income is the starting point in determining cash flows from operations.

B. cash paid for dividends is not included.

C. the increase in cash is different than when the indirect method is used.

D. the amount of cash collected from customers is calculated.

Manufacturing overhead would not include which of the following costs?

A. Plant utilities

B. Supervisory salaries

C. Depreciation of plant assets

D. Raw materials

McCloud Company purchased a machine for $15,500. The machine is expected to last

four years and has a residual value of $1,500. The entry to record depreciation expense

at the end of the first year using the straight-line method is:

A. Depreciation Expense—Machinery 3,500

Accumulated Depreciation—Machinery 3,500

B. Machinery 3,875

Depreciation 3,875

C. Depreciation Expense—Machinery 3,875

Machinery 3,875

D. Accumulated Depreciation—Machinery 1,500

A company with a current ratio of 2.4 times will see that ratio decrease when the

company

A. pays a large current liability.

B. declares a 10 percent stock dividend on its common stock.

C. borrows cash by issuing a short-term note payable.

D. converts a short-term liability to a long-term liability.

The recording of data falls under which stage of accounting?

A. measurement

B. processing

C. communication

D. decision making

Accounts Receivable was $1,500 at the end of November and $1,050 at the end of

December. Revenue totaled $8,400 for December. How much cash was received from

revenues during December?

A. $10,950

B. $8,850

C. $7,950

D. $5,950

Which of the following would be added to the balance per bank?

A. Outstanding checks

B. Bank service charges

C. Collection of a note receivable by the bank

D. Deposits in transit

The account most recently posted is determined most efficiently by referring to the

A. Post. Ref. column of the ledger.

B. balance column of the ledger.

C. date column of the general journal.

D. Post. Ref. column of the general journal.

Which of the following is not considered in computing net cost of purchases?

A. Freight-out expenses

B. Purchases

C. Freight paid on purchased goods

D. Purchases returns and allowances

Interest paid on debt would be entered on the multistep income statement in the

category called

A. selling expenses.

B. other revenues and expenses.

C. general and administrative expenses.

D. operating expenses.

All of the following items are associated with a purpose of the work sheet except

A. Recording adjusting entries.

B. Preparing financial statements.

C. Preparing budgets.

D. Recording closing entries.

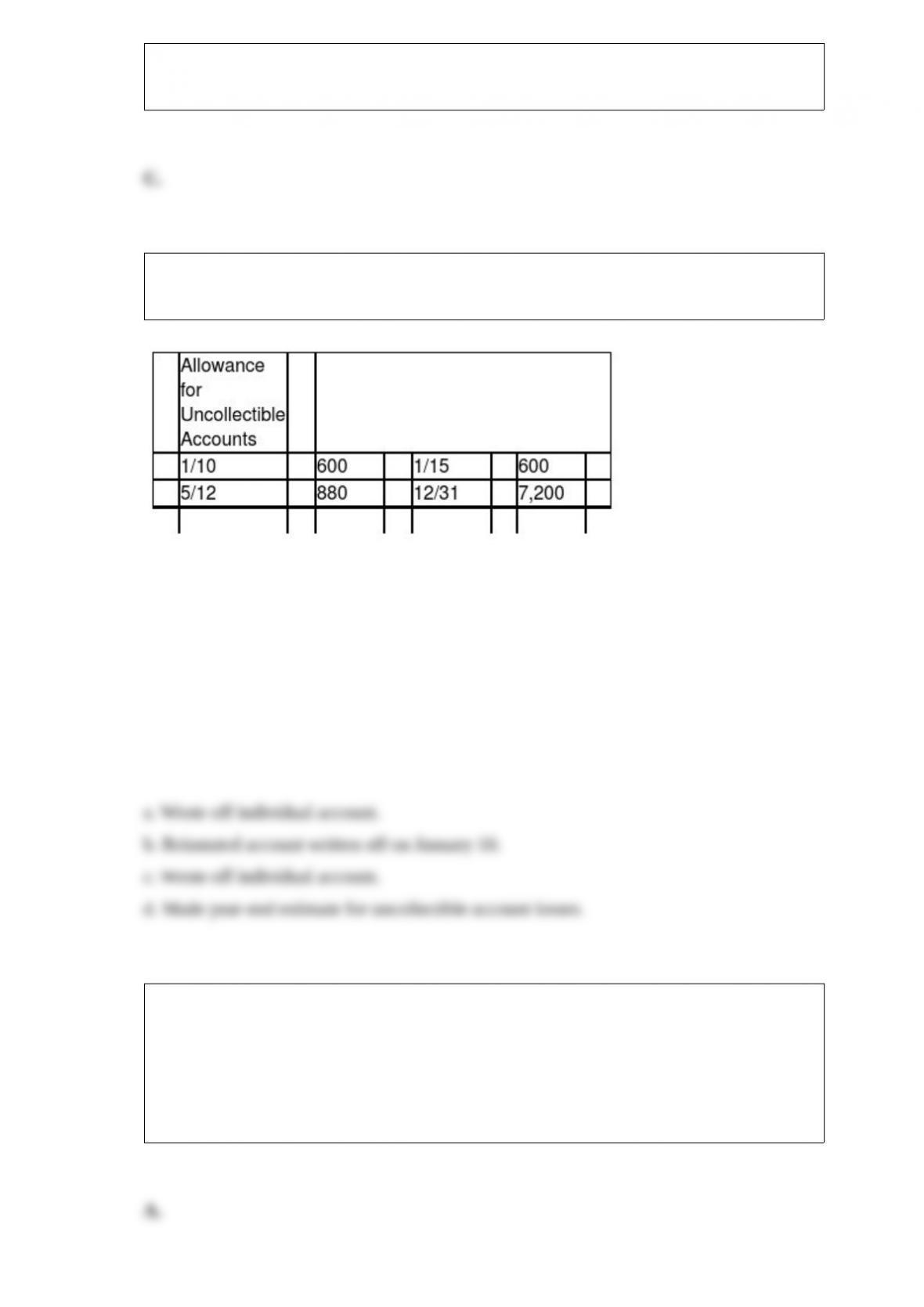

Use the following T account to answer the questions below (assume a calendar-year

accounting period).

What apparently occurred on:

a. January 10?

b. January 15?

c. May 12?

d. December 31?

Which of the following errors will not cause the debit and credit columns of the trial

balance to be unequal?

A. A debit entry was recorded in the wrong account.

B. A debit was entered in an account as a credit.

C. The account balance was carried to the wrong column of the trial balance.

D. The balance of an account was incorrectly computed.

Which of the following is a business event that is considered a recordable transaction?

A. A company hires a new employee.

B. A customer purchases merchandise.

C. A company orders a product from a supplier.

D. An employee sends a purchase requisition to the purchasing department.