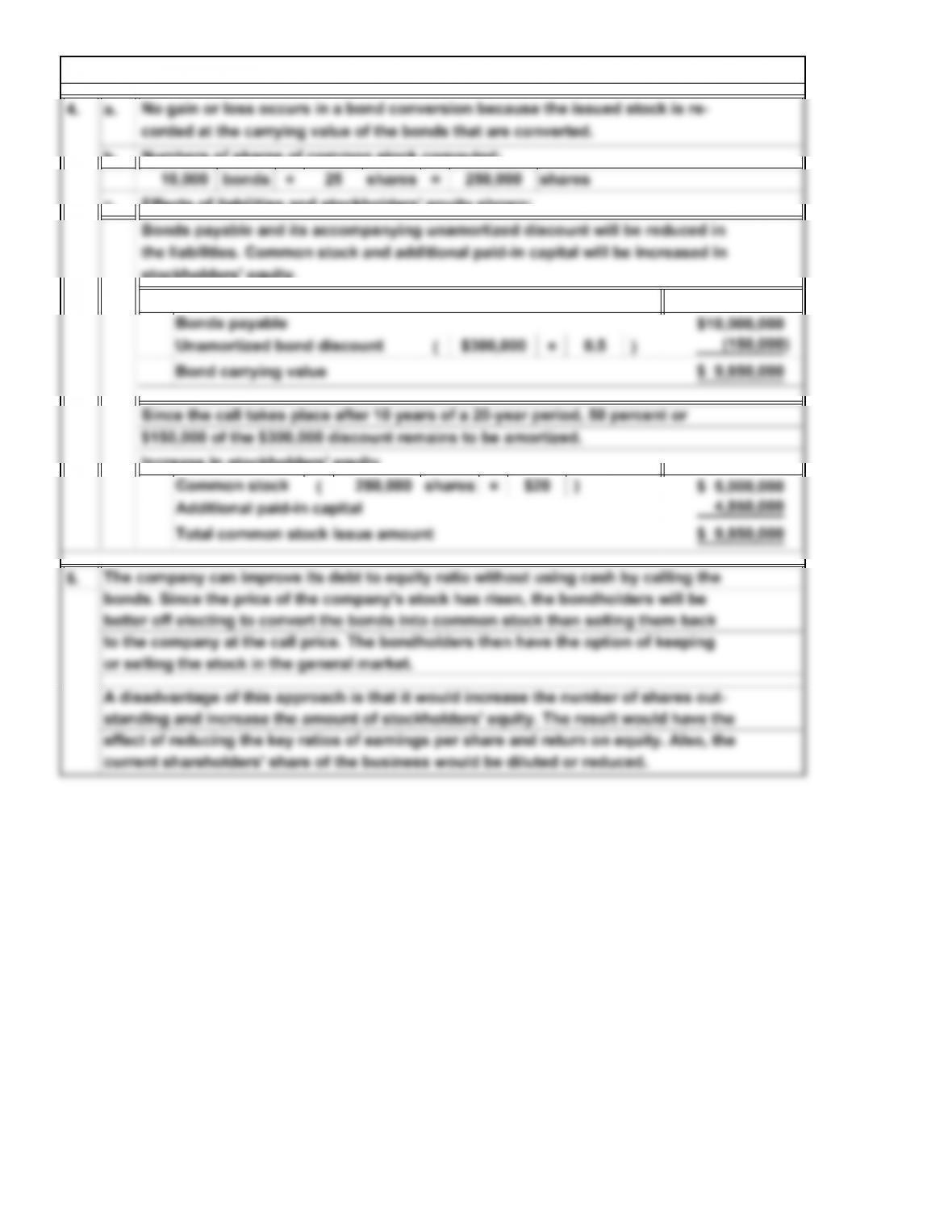

4. a.

b.

c.

current shareholders’ share of the business would be diluted or reduced.

A disadvantage of this approach is that it would increase the number of shares out-

standing and increase the amount of stockholders’ equity. The result would have the

effect of reducing the key ratios of earnings per share and return on equity. Also, the

No gain or loss occurs in a bond conversion because the issued stock is re-

P6. Bond Basics—Straight-Line Method, Retirement, and Conversion (Concluded)

Effects of liabilities and stockholders’ equity shown:

Decrease in liabilities

Numbers of shares of common stock computed:

stockholders’ equity.

14-30

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(××6/12)

– ( × × 6 / 12 )

(××6/12)

– ( × × 6 / 12 )

2015

2014

Paid semiannual interest and amortized

0.095

$8,200,000

$8,000,000

$8,197,200

0.095

0.092

the premium on 9.5%, 25-year bonds

0.092

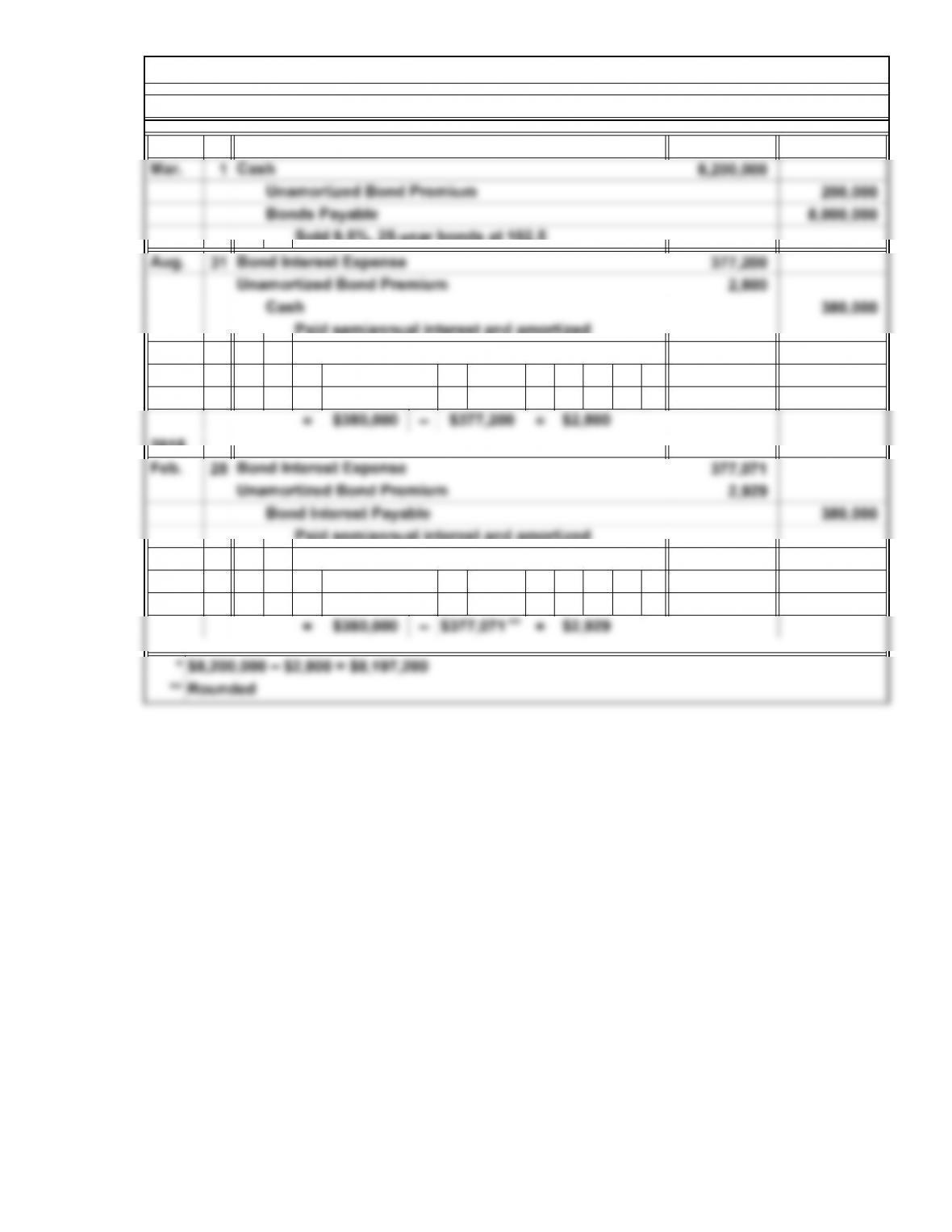

P7. Bond Transactions—Effective Interest Method

Paid semiannual interest and amortized

1.

$8,000,000

the premium on 9.5%, 25-year bonds

*

14-31

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(××6/12)

3.

example. When market rates are above the face interest rate, buyers are not willing

0.098

P7. Bond Transactions—Effective Interest Method (Concluded)

Paid semiannual interest and amortized

the discount on 9.5%, 25-year bonds

$7,800,000

2.

Market interest rates play a role in creating the premium and discount in the previous

2014

*

**

$7,800,000 + $2,200 = $7,802,200

Rounded

14-32

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(××6/12

(××6/12

=‒=

(××6/12

(××6/12

=‒=

(××6/12

(××6/12

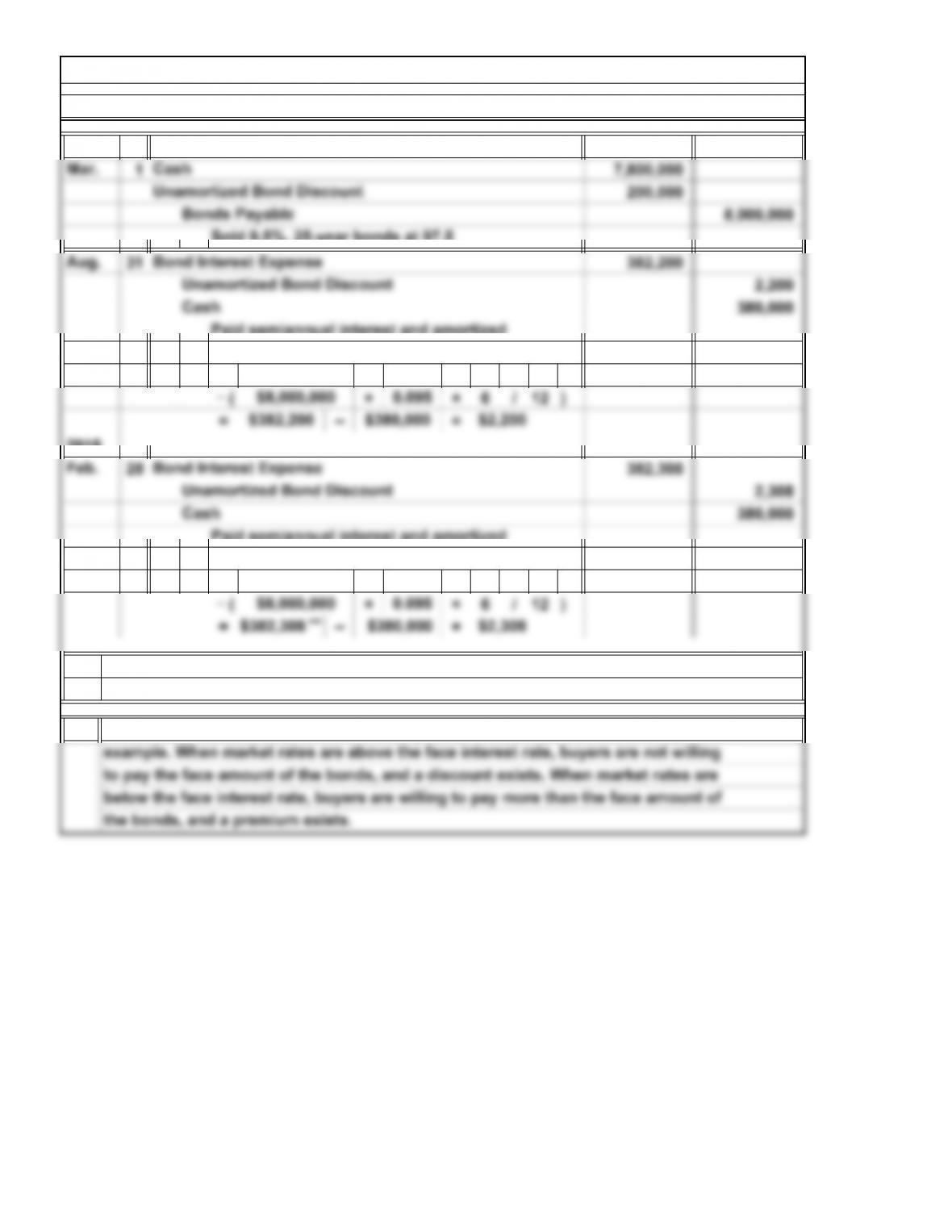

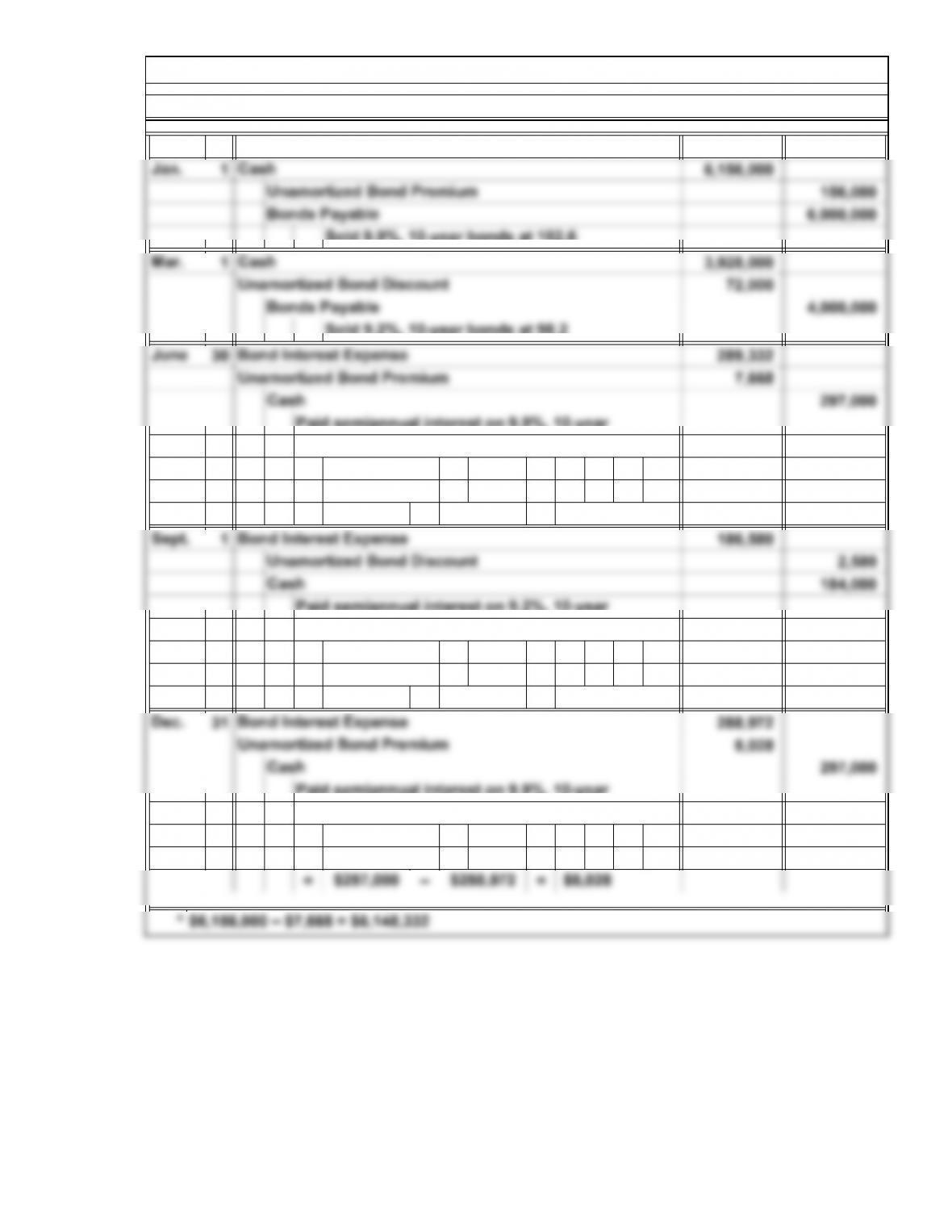

P8. Bonds Issued at a Discount and a Premium—Effective Interest Method

$6,000,000

1.

2014

Paid semiannual interest on 9.9%, 10-year

bonds and amortized the premium

0.095

0.092

$297,000 $289,332

$3,928,000

0.099

0.094

) –

$4,000,000

0.094

$7,668

)

$186,580 $184,000

$6,156,000 )

) –

Paid semiannual interest on 9.2%, 10-year

bonds and amortized the discount

$6,148,332

Paid semiannual interest on 9.9%, 10-year

$2,580

$6,000,000

) –

bonds and amortized the premium

0.099

)

*

14-33

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(××4/12

(××4/12

=–=

( × × 2 / 12 ) –

(××2/12

2.

30 $297,000

* Rounded

$3,930,580

$4,000,000

remainder of the interest period

expense and amortization of the discount

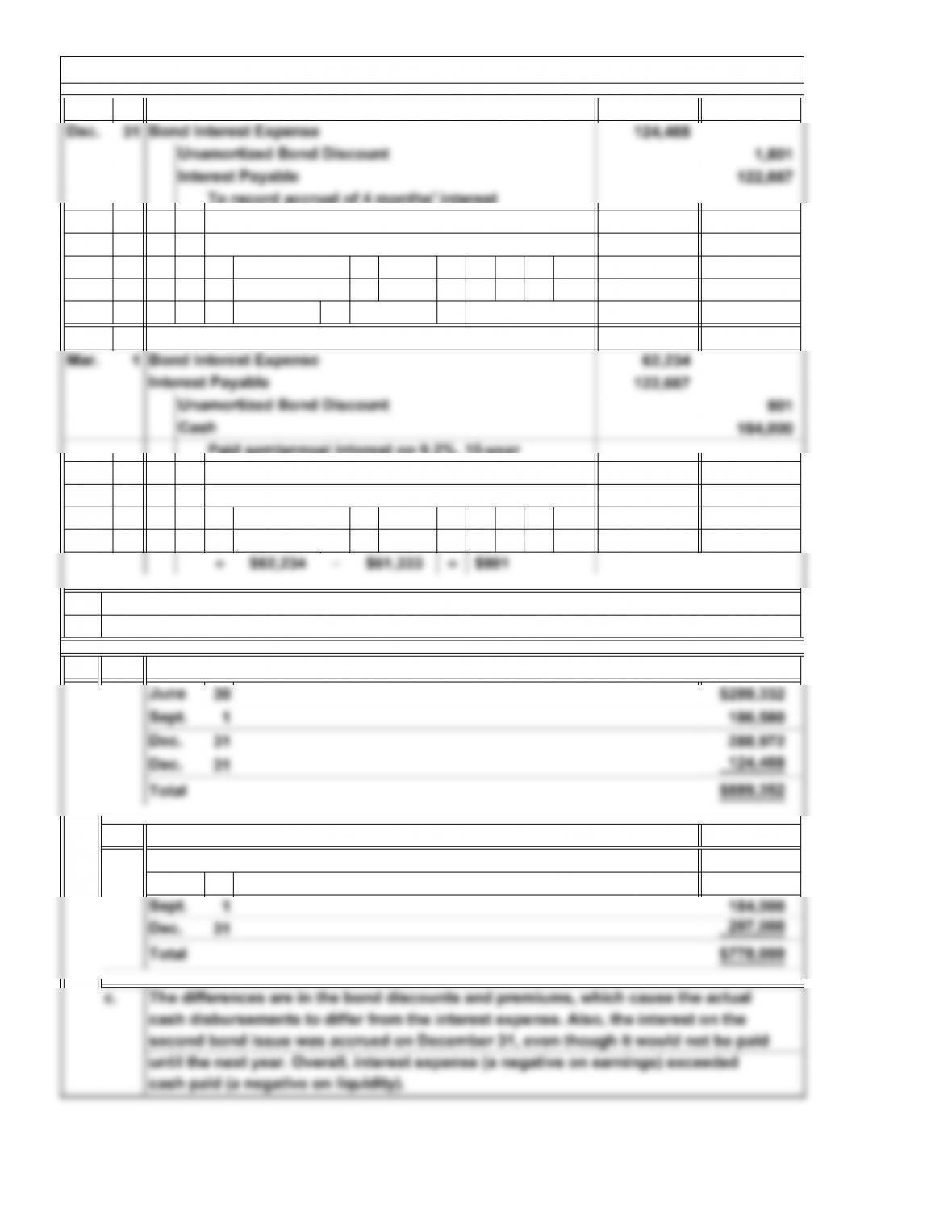

$122,667

2014

0.095

0.092

) –

)

P8. Bonds Issued at a Discount and a Premium—Effective Interest Method (Concluded)

2015

bonds and amortized the discount for the

Paid semiannual interest on 9.2%, 10-year

on 9.2%, 10-year bonds

June

$124,468

0.095

0.092

$4,000,000

$3,930,580

To record accrual of 4 months’ interest

a.

Bond interest expense in 2014:

b.

Cash paid for interest:

Total cash paid for 2014 bond issues:

$3,928,000 + $2,580 = $3,930,580

$1,801

)

**

**

**

14-34

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

/=

×=

2. a.

at End of Period

Reduction

in DebtUnpaid Balance

Present value calculated.

PaymentMonth

Unpaid Balance

Interest for 1

Month at 0.75% onMonthly

P9. Lease Versus Purchase

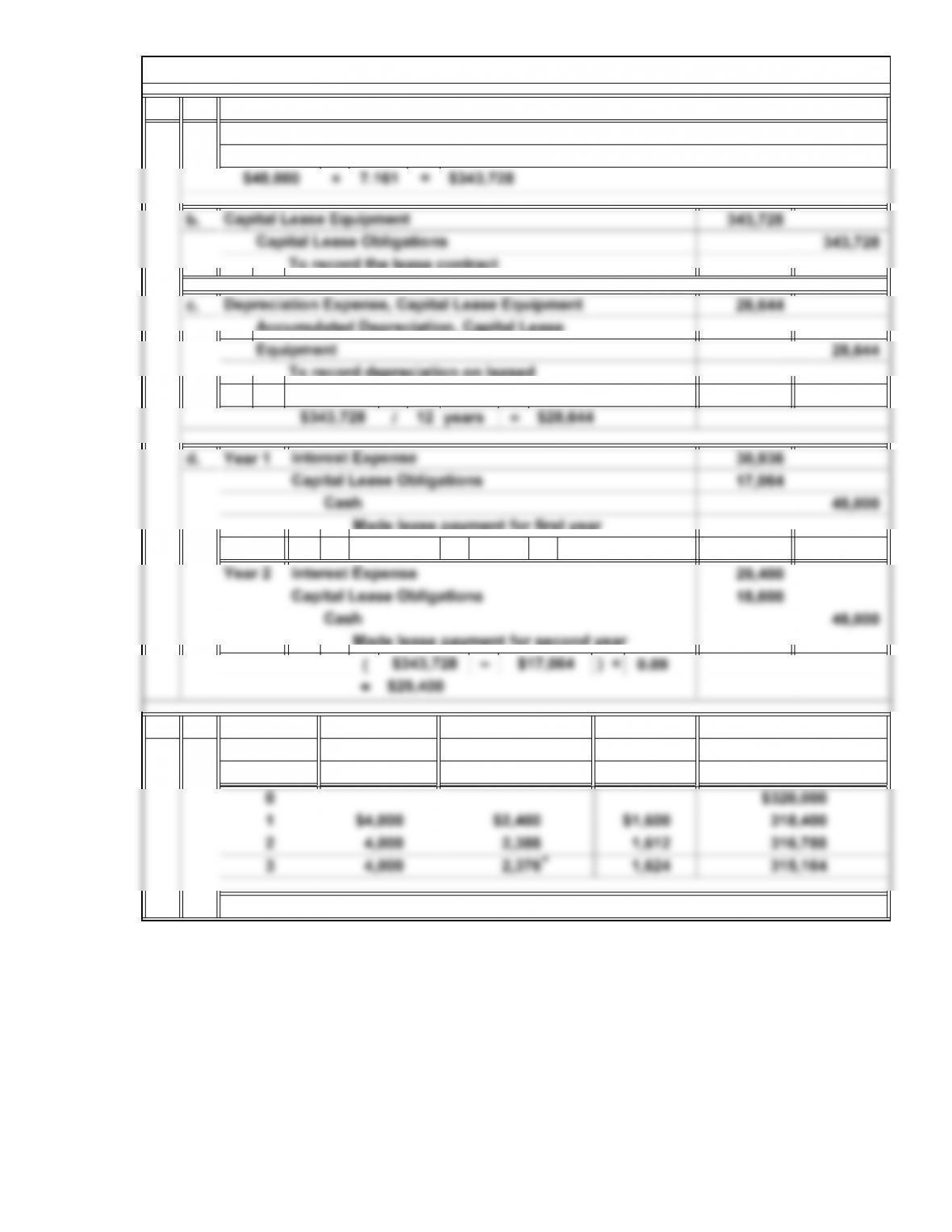

= Present Value of Lease

Periodic Payment × Factor (Table 2 in Appendix B: 9%, 12 periods)

To record depreciation on leased

equipment for first year

$343,728 12

0.09

Made lease payment for first year

$30,936$343,728

0

2

4,000

2,388

*Rounded

1,612

$320,000

316,788

years $28,644

14-35

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

financial considerations.

responsibilities of ownership, which can include repairs, taxes, and other costs.

In conclusion, the decision to lease or purchase depends both on financial and non-

parking facilities, which could be re-leasing the current facility, if it is still used. Also,

the owner of the facility may want to use the space for other purposes. An advantage

of purchasing the building is that Martha has control over the property and can reno-

vate, rebuild, or sell it, as the need arises. A disadvantage is that Martha assumes the

Based on the calculation, it appears that the purchase is best because the cost of

$320,000 is less than the net present value of the lease, which is $343,728. Both op-

mortgage

P9. Lease Versus Purchase (Concluded)

Made second monthly payment on

14-36

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.