1.

2.

Recording transactions The accountant updates the perpetual inventory records

daily for receipts and sales.

if the customer has a “paid” invoice received from the cashier.

Authorization The warehouse attendant can release a printer to a customer only

P2. Internal Control Procedures

Documents and records The principal documents are sales invoices and inventory

ployees less likely.

ventory records. These procedures are no guarantee, but they make theft by em-

Assets are often vulnerable to employee theft. In the case of Transco Printers, the

8-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

Third, Hazel hires bonded employees who are experienced. Fourth, Hazel provides train-

ing in procedures. These procedures are no guarantee, but they lessen the risk of loss of

cash in the cashier function.

Authorization Authorization for credit card sales is obtained by scanning the

P3. Internal Control Activities

8-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

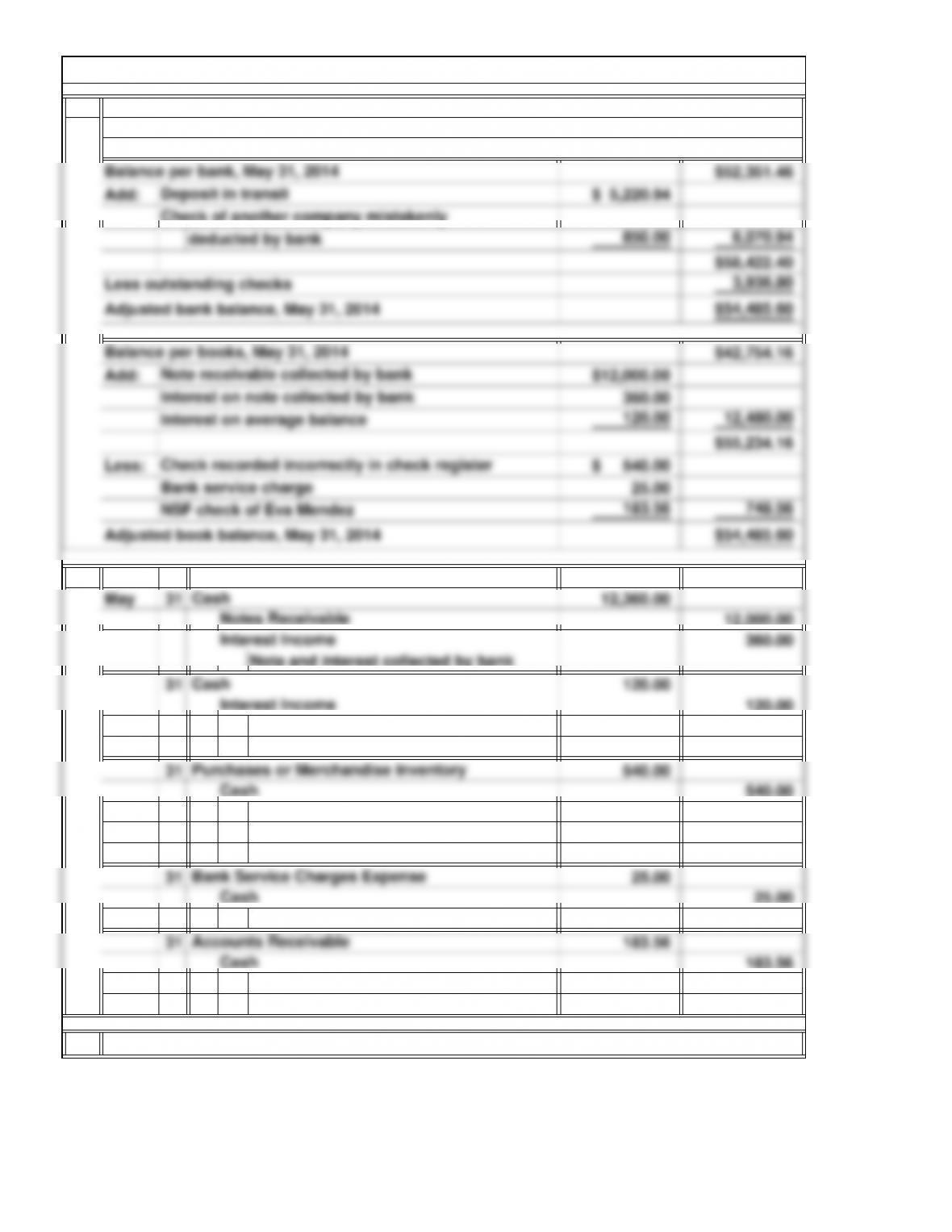

2. 2014

Note and interest collected by bank

Interest on average bank account

balance

To correct an incorrect entry for

purchase of merchandise

$1,920 – $1,380 = $540

Bank service charge for May

NSF check of Eva Mendez returned

by bank

3.

The adjusted cash balance of $54,485.60 should appear on the balance sheet.

May 31, 2014

Cash

Sedona, Inc.

Bank Reconciliation

P4. Bank Reconciliation

Cash

Cash

Interest Income

8-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

4.

A bank reconciliation is a necessary internal control because events and items such

P4. Bank Reconciliation (Concluded)

8-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

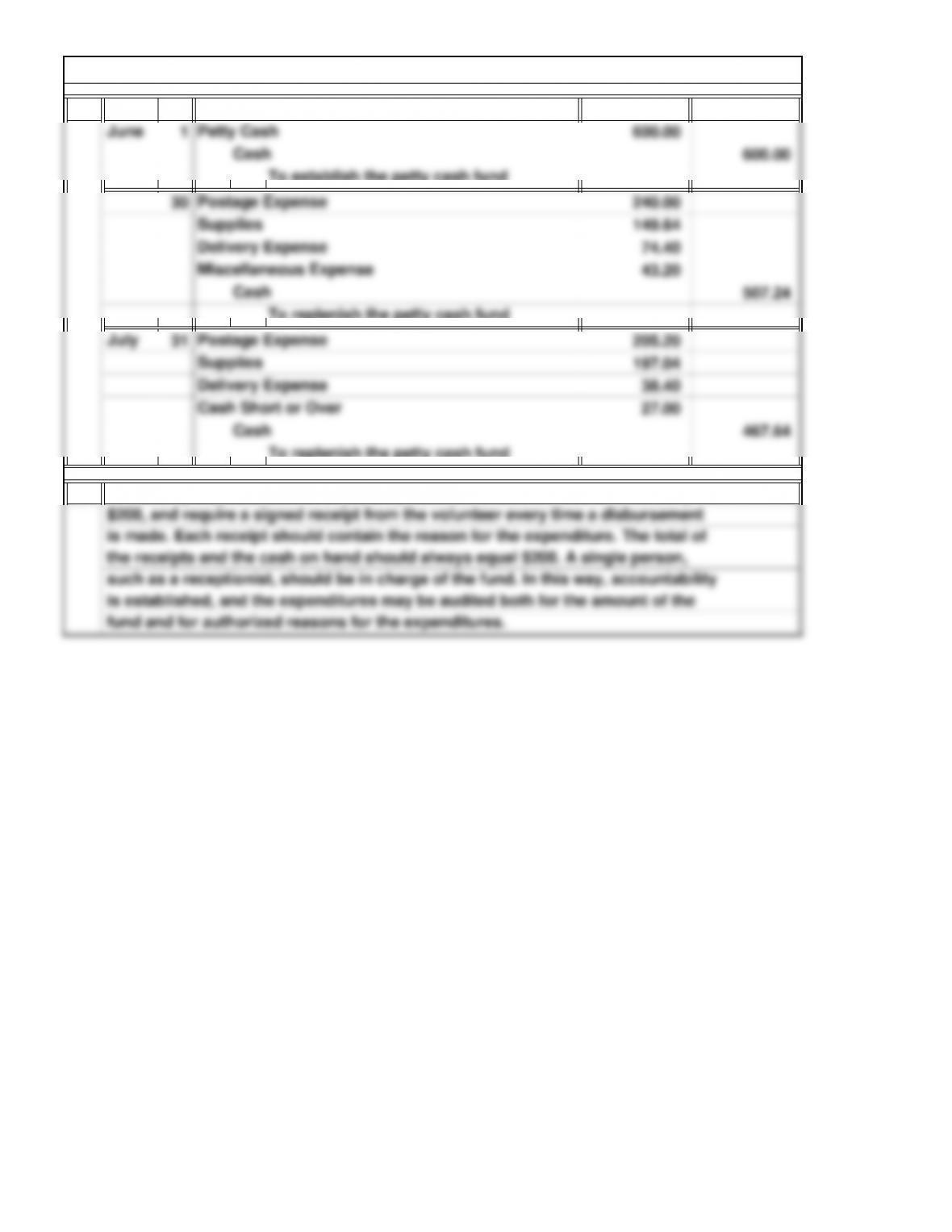

2.

To replenish the petty cash fund

2014

P5. Imprest (Petty Cash) Transaction

is established, and the expenditures may be audited both for the amount of the

fund and for authorized reasons for the expenditures.

$200, and require a signed receipt from the volunteer every time a disbursement

is made. Each receipt should contain the reason for the expenditure. The total of

the receipts and the cash on hand should always equal $200. A single person,

such as a receptionist, should be in charge of the fund. In this way, accountability

The charity may establish an imprest system with a fixed amount of funds, say

8-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

P6. Internal Control Components

Alternative Problems

ther, she can monitor compliance with the procedures.

8-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 1. 6.

2. 7.

3. 8.

c.

c

d

c, f

a

P7. Control Activities

a, f

b, c, f

Documents and records Several new documents and records were established by

is conducted by the warehouse supervisor.

8-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

g.

ployees’ understanding of and willingness to carry out their new roles. Some exam-

Sound personnel practices This is an area of apparent weakness in the new sys-

ples: The supplies clerk must be careful to release only the amount of supplies

authorized for each job. The warehouse manager must take the physical inventory

each month and do so accurately. The purchasing clerk must make a conscious

tem. Many employees have new duties with more rigorous procedures to follow and

more forms to complete than before. The case does not specify what steps, if any,

were taken to train the employees in the new procedures and to motivate them to

accept these procedures. The success of the new system will depend on the em-

P7. Control Activities (Concluded)

8-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.