3.

cause it is a good indicator of a company’s ability to pay its bills and to repay

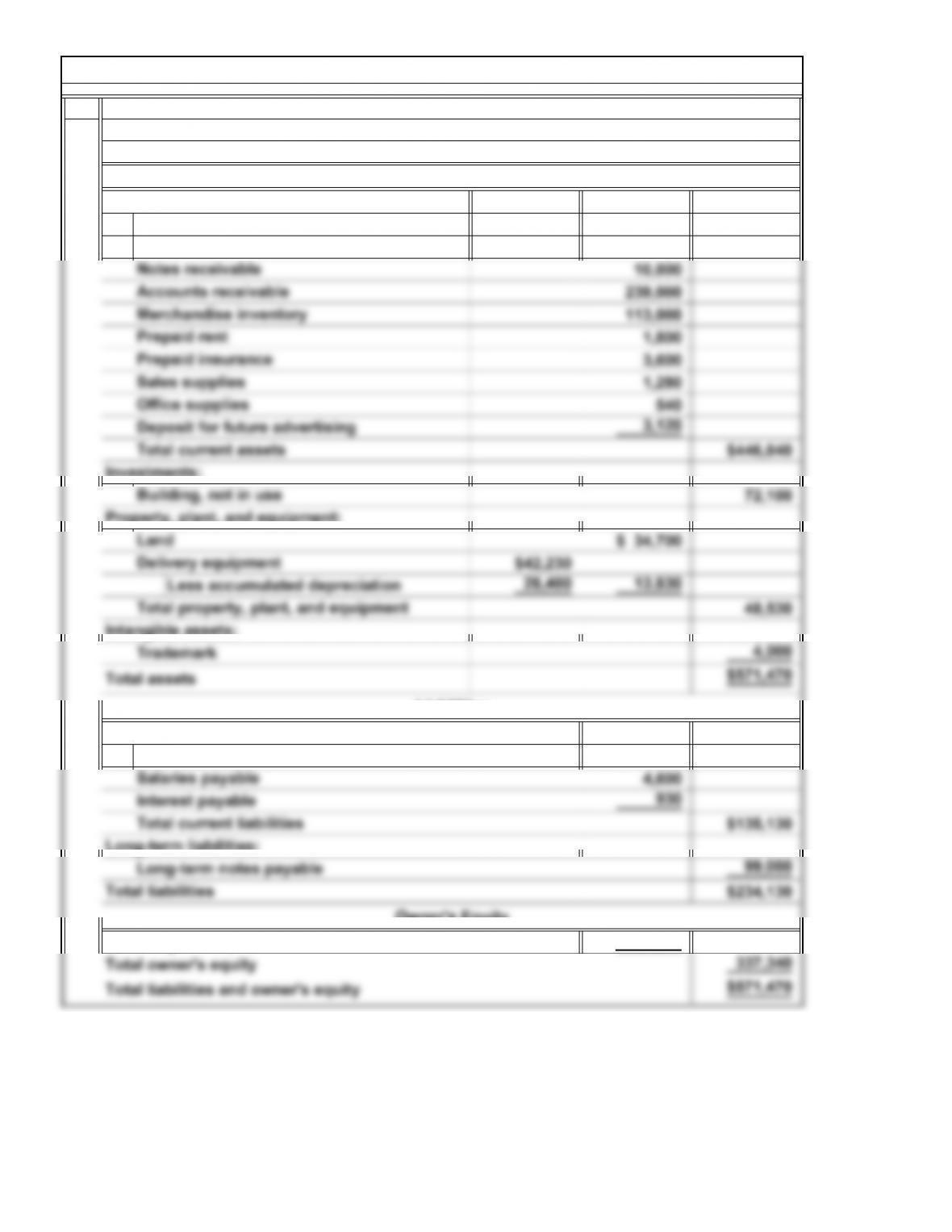

Current Assets

Owner’s Equity

a.

b.

A user of the classified balance sheet would want to know the current ratio be-

$133,140

Current Ratio

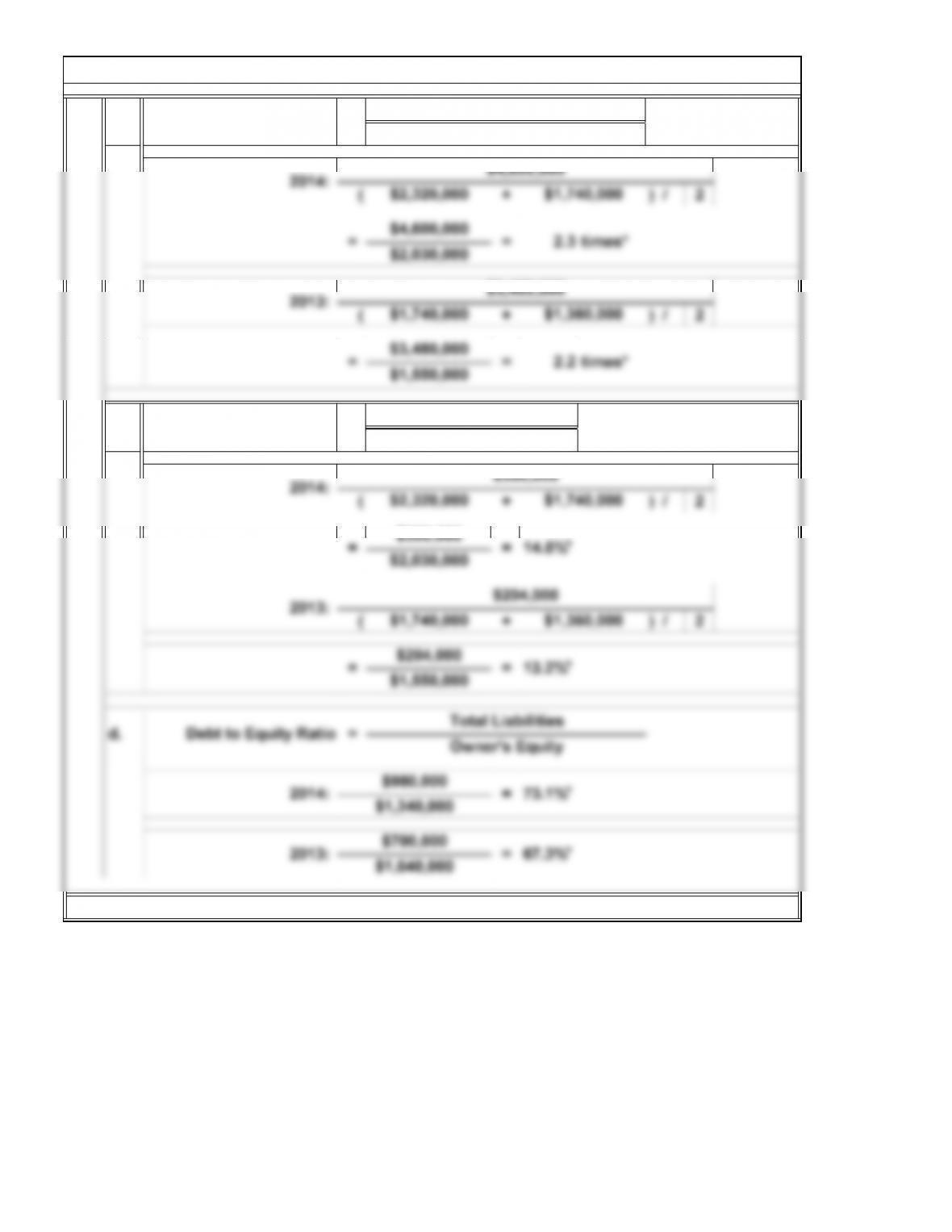

Debt to Equity

Ratio =Total Liabilities

=

P4. Classified Balance Sheet (Concluded)

2. Current Liabilities

*Rounded

5-19

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

4.

5.

6.

7.

8.

must disclose the change, the effect of the change on net income, and why the

the conservatism convention. This method of valuing inventory is less likely to over-

The change in the method of accounting for inventory is a violation of the consis-

determined that the benefits of the new reporting system outweigh the costs.

of it is important to users of the financial statements.

This is an acceptable application of the cost-benefit convention if management has

P5. Accounting Conventions

tency convention. If a company changes its method of accounting for inventory, it

Delays in issuing financial statements is a violation of the enhancing qualitative

Use of uncommon technical terms in the financial statements is a violation of the

enhancing qualitative characteristic of understandability.

characteristic of comparability.

Alternate Problems

Valuing inventory at lower of cost or market is a generally accepted application of

Producing financial statements that are not helpful in assessing future prospects is

ments so that the reader will be aware of the inconsistency. The change in the

newly adopted accounting principle is preferable in the notes to its financial state-

5-20

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

$ 31,000

33,000

$114,600

$394,960

Short-term investments

P6. Classified Balance Sheet

Assets

Matt’s Hardware Company

Balance Sheet

April 30, 2014

Current assets:

Cash

Accounts payable

Owner’s Equity

Liabilities

M. Shah, capital

Current liabilities:

5-21

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Current Ratio

a.

b.

P6. Classified Balance Sheet (Concluded)

2. Current Liabilities

=

Current Assets

Total Owner’s Equity

Total Liabilities

Debt to Equity

Ratio =

$506,800

$120,640 =

$200,640

5-22

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

Working Capital

P7. Liquidity and Profitability Ratios

$366,000 = 2.0

$180,000

Current Ratio =

$366,000

2014:

b.

Current Liabilities

*Rounded

2013

$310,000

Current Assets

Working Capital

2014

Current Assets

*

5-23

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

b.

2014: $4,600,000

2013: $700,000 = 67.3%

$1,040,000

P7. Liquidity and Profitability Ratios (Continued)

Asset Turnover = Net Sales

Average Total Assets

*Rounded

*

5-24

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

e.

2014: $300,000

Average Owner’s Equity

P7. Liquidity and Profitability Ratios (Concluded)

Return on Equity = Net Income

5-25

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

$ 31,000

43,500

$129,600

$337,340

Cash

Short-term investments

Current assets:

P8. Classified Balance Sheet

Owner’s Equity

Rodriguez’s Tools Company

Balance Sheet

April 30, 2014

Assets

C. Rodriguez, capital

Liabilities

Current liabilities:

Accounts payable

5-26

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

ure is very important to liquidity analysis because it is related to debt and its repay-

ment. It is also relevant to profitability analysis because the amount of debt affects

the amount of interest expense and the owner’s return on investment.

$337,340

Current Ratio

Debt to Equity

Ratio

a.

b.

A user of the classified balance sheet would want to know the current ratio because

it is a good indicator of a company’s ability to pay its bills and to repay outstanding

Total Owner’s Equity

=Total Liabilities

P8. Classified Balance Sheet (Concluded)

2. = Current Assets

Current Liabilities

*Rounded

5-27

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.