$ 32,500

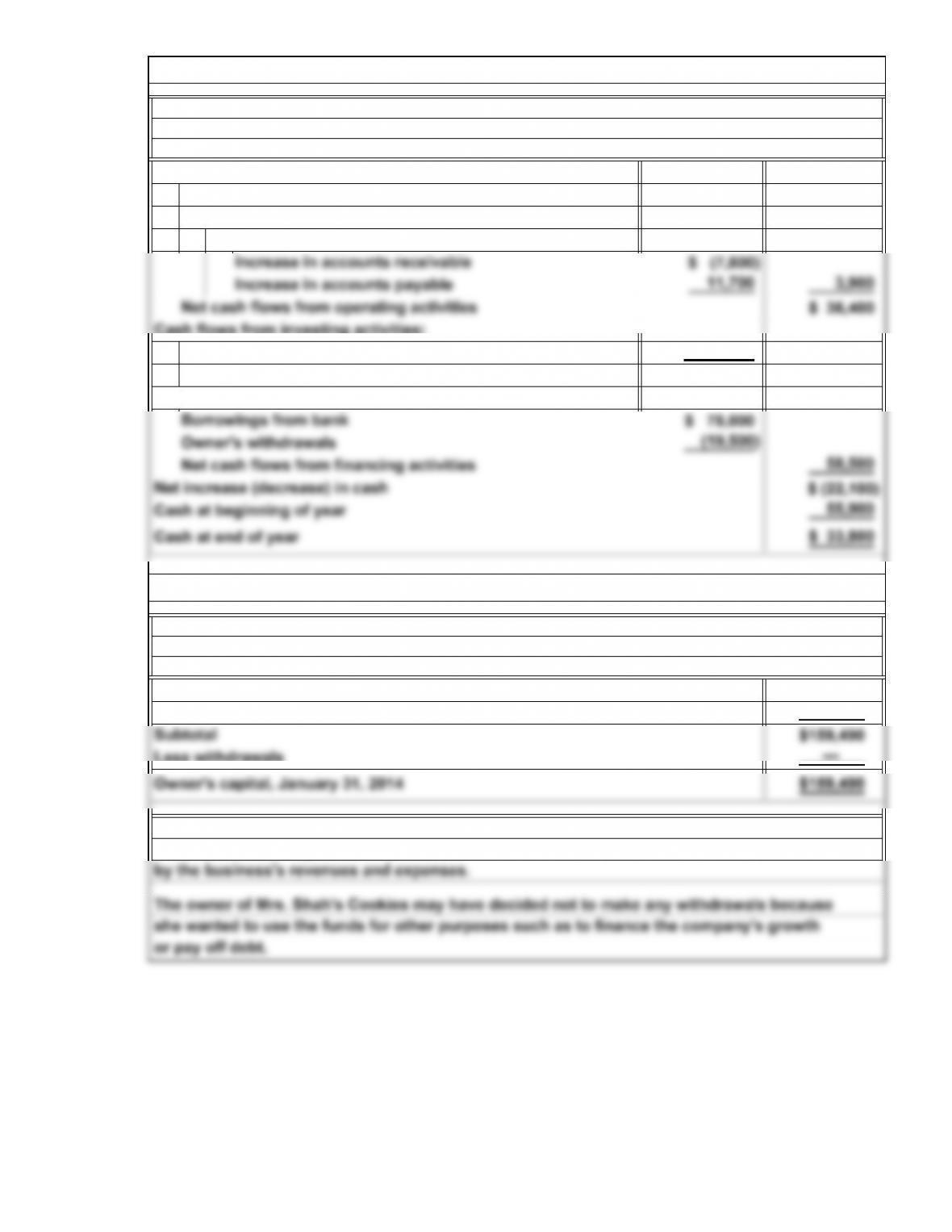

cash flows from operating activities:

$(117,000)

(117,000)

$102,403

57,087

—

Less withdrawals

Purchase of equipment

Cash flows from operating activities:

Statement of Owner’s Equity

For the Year Ended January 31, 2014

Adjustments to reconcile net income to net

Net income

For the Year Ended December 31, 2014

Cash flows from investing activities:

Cash flows from financing activities:

Net cash flows used by investing activities

Owner’s capital, January 31, 2013

Net income for the year

Mrs. Shah’s Cookies

E10A. Statement of Owner’s Equity

E9A. Statement of Cash Flows

Arlington Service Company

Statement of Cash Flows

1-9

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

●

●

●

●

●

●

●

●

1. b 5. l 9. c

2. k 6. f 10. d

3. g 7. a 11. e

4. i 8. j 12. h

Thus, start with (c), which must equal $3,000 (check: $29,000 + $3,000 – $2,000 = $30,000).

Then, (b) equals (c), or $3,000. Thus, (a) must equal $8,100 (check: $11,100 – $8,100 =

$3,000). Because (e) equals $30,000 (ending balance from the statement of owner’s

E11A. Preparation and Integration of Financial Statements

that has been granted a charter from the state and is legally separate from its owners

Net income links the income statement and the statement of owner’s equity. The ending

balance of owner’s equity links the statement of owner’s equity and the balance sheet.

A partnership is a business that has two or more owners. A corporation is a business unit

Customers

Economic planners

Regulators

equal (f), or $46,000.

People who are interested in Avalon’s financial statements are the following:

Management

Investors (owners of the company)

ship of a partnership changes, the partnership must be dissolved and another one formed.

E13A. The Nature of Accounting

E12A. Users of Accounting Information and Forms of Business Organization

Tax authorities

Employees

Creditors

1-10

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

3.

AICPA:

IASB:

IRS:

PCAOB:

Note to Instructor: Solutions for Exercises: Set B are provided separately on the Instructor’s

Resource CD and website.

a

c

b

American Institute of Certified Public Accountants

Public Company Accounting Oversight Board

Internal Revenue Service

International Accounting Standards Board

CPA:

E14A. Accounting Abbreviations

Certified Public Accountant

E15A. Ethics and Accounting

1-11

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

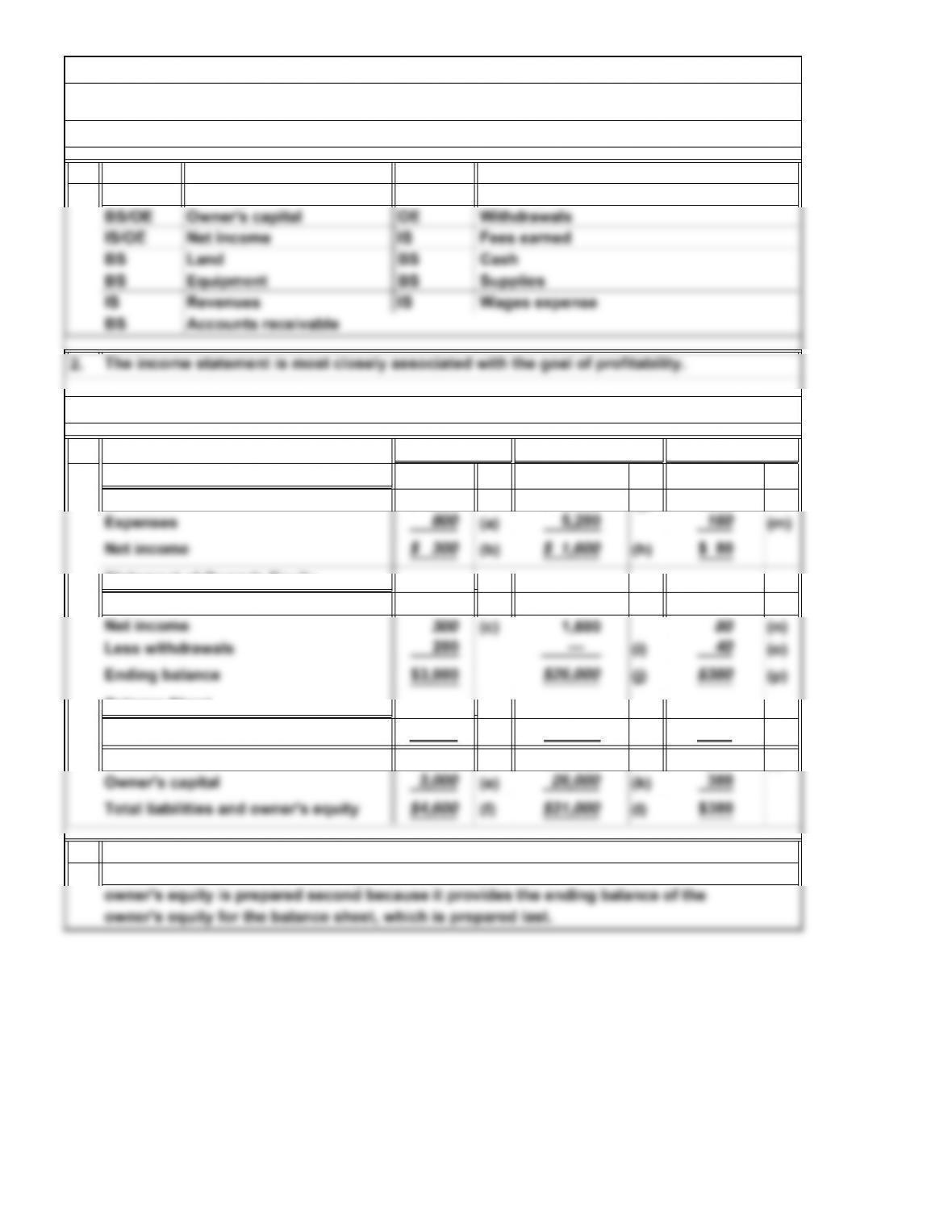

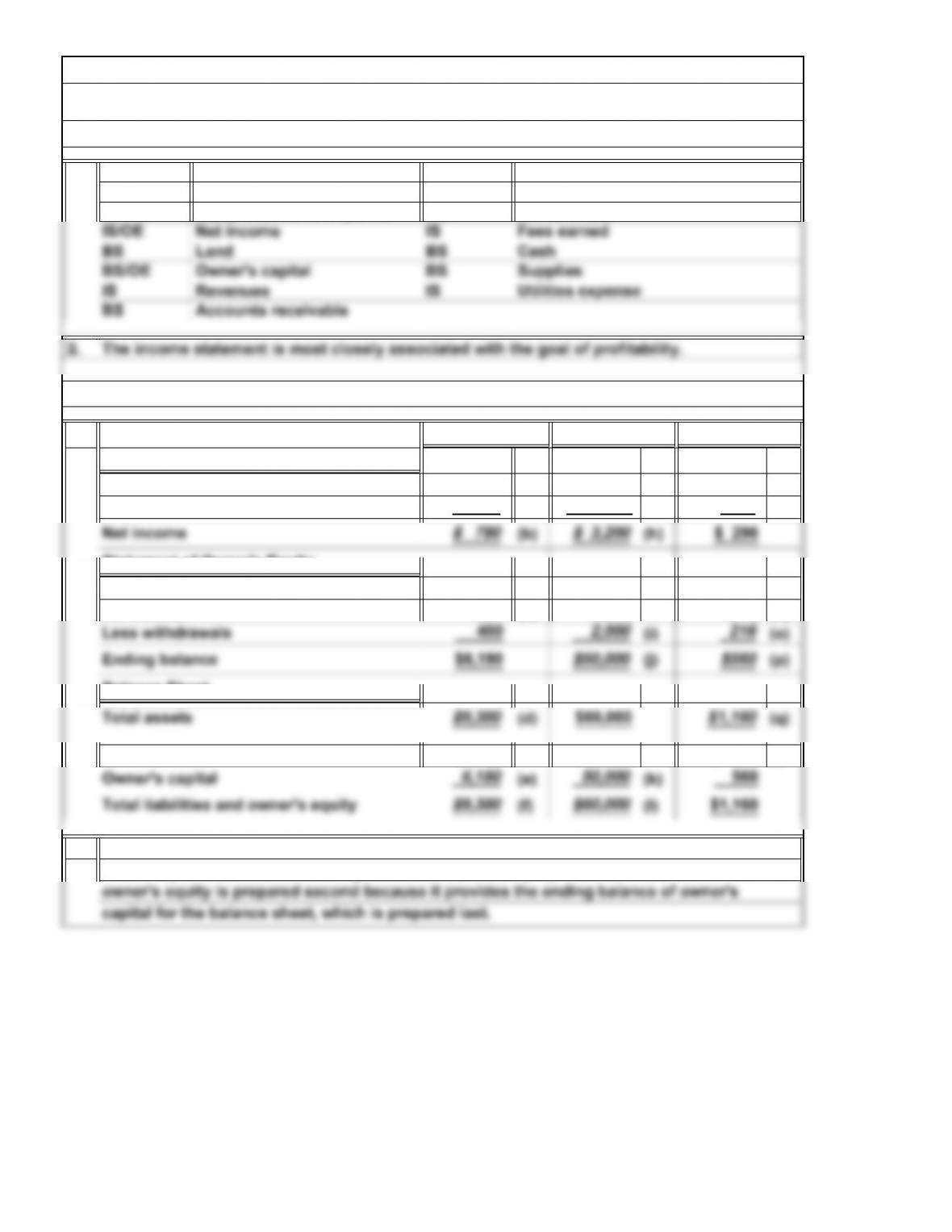

1. IS Utilities expense BS

BS Building IS

$1,100 $ 6,800 (g) $240

$2,900 $24,400 $340

$4,600 (d) $31,000 $380 (q)

$1,600 $ 5,000 $— (r)

2.

necessary to determine the ending balance of owner’s capital. The statement of

The income statement must be prepared first because the amount of net income is

P2. Integration of Financial Statements

Set A

Set B

Income Statement

Beginning balance

Statement of Owner’s Equity

Balance Sheet

Set C

1.

Problems

P1. Preparation and Interpretation of Financial Statements

Accounts payable

Rent expense

Total assets

Total liabilities

Revenue

1-12

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

$400,000

$225,000

20,100

$ 64,300

79,200

$ 71,700 Accounts payable $ 3,600

4,500 22,700

2.

Fuel Designs

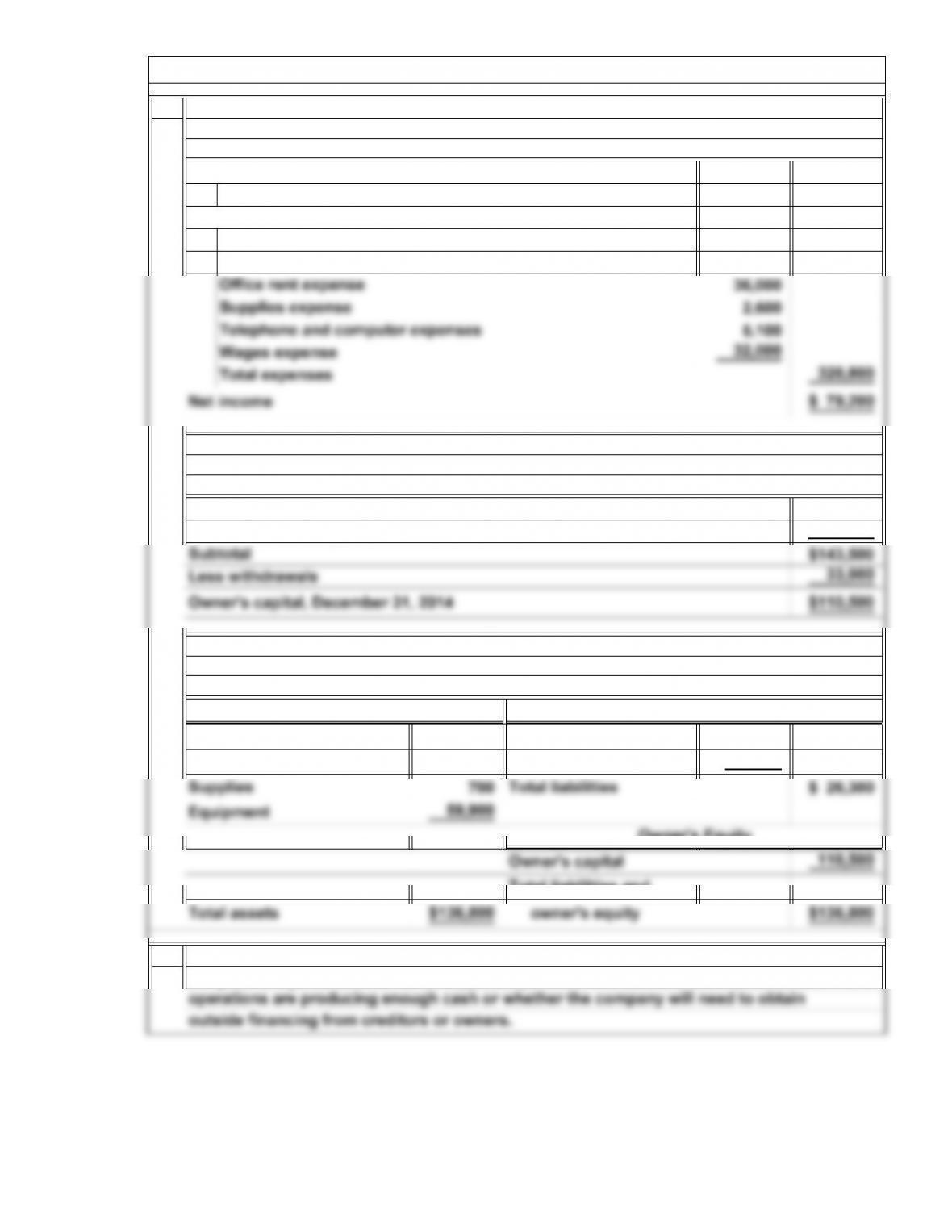

Revenues:

December 31, 2014

Net income for the year

Liabilities

Fuel Designs

Marketing expense

Owner’s capital, December 31, 2013

Statement of Owner’s Equity

For the Year Ended December 31, 2014

Assets

Balance Sheet

Income Statement

For the Year Ended December 31, 2014

Expenses:

Commission sales revenue

Commissions expense

Cash

Accounts receivable

The statement of cash flows is very useful in assessing whether a company’s operations

are generating sufficient funds to support expansion. The statement tells whether

Commissions payable

Fuel Designs

P3. Preparation and Interpretation of Financial Statements

1-13

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

$159,200

$37,200

$—

5,000

1,600

—

$ 1,800 $19,400

24,600 1,300

6,600

2.

low in that it has earned only $1,600 on revenues of $159,200. Liquidity is low because

Frequent Ad

Equipment rental expense

Revenues:

For the Year Ended January 31, 2014

Frequent Ad

Income Statement

Accounts receivable

Cash

Salaries payable

Frequent Ad

Liabilities

Assets

The company is challenged both in terms of profitability and liquidity. Profitability is

Accounts payable

Net income for the year

Balance Sheet

Owner’s Equity

A. Francis, capital

P4. Preparation and Interpretation of Financial Statements

January 31, 2014

A. Francis, capital, January 31, 2013

Investments by A. Francis

Less withdrawals

Statement of Owner’s Equity

Advertising service revenue

Expenses:

Total liabilities and

For the Year Ended January 31, 2014

1-14

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

3.

P5. Use and Interpretation of Financial Statements

The income statement shows net income of $3,775 earned by the company over a

month. The amount of net income is necessary for the preparation of the statement

of owner’s equity. The statement of owner’s equity shows an ending balance of

come on revenues of $6,100. The owner also withdrew money in the amount of

form to GAAP in all material respects.

The company appears to be very profitable because it has earned $3,775 of net in-

$2,400. However, the return on total assets (net income divided by total assets) is

pany might experience some challenges in its liquidity position in the future because

only 6.98 percent, or $0.0698 on each dollar of assets invested. Moreover, the com-

shown on the balance sheet.

cause it shows the earnings of the business. The cash flow statement is most closely

The income statement is most closely associated with the goal of profitability, be-

1-15

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Wages expense BS

Equipment IS

Equipment rental expense OE

$2,400 $13,200 (g) $ 480

1,620 (a) 10,000 184 (m)

$5,800 $48,800 $480

780 (c) 3,200 296 (n)

$3,200 $10,000 $ 600 (r)

2.

Revenues

Set A

Income Statement

Net income

Expenses

Statement of Owner’s Equity

Total liabilities

Beginning balance

P7. Integration of Financial Statements

necessary to determine the ending balance of owner’s equity. The statement of

1. Set CSet B

P6. Preparation and Interpretation of Financial Statements

Alternate Problems

The income statement must be prepared first because the amount of net income is

IS

BS

1.

IS

Accounts payable

Rent expense

Withdrawals

1-16

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.