1.

(×)

(×)

= times*

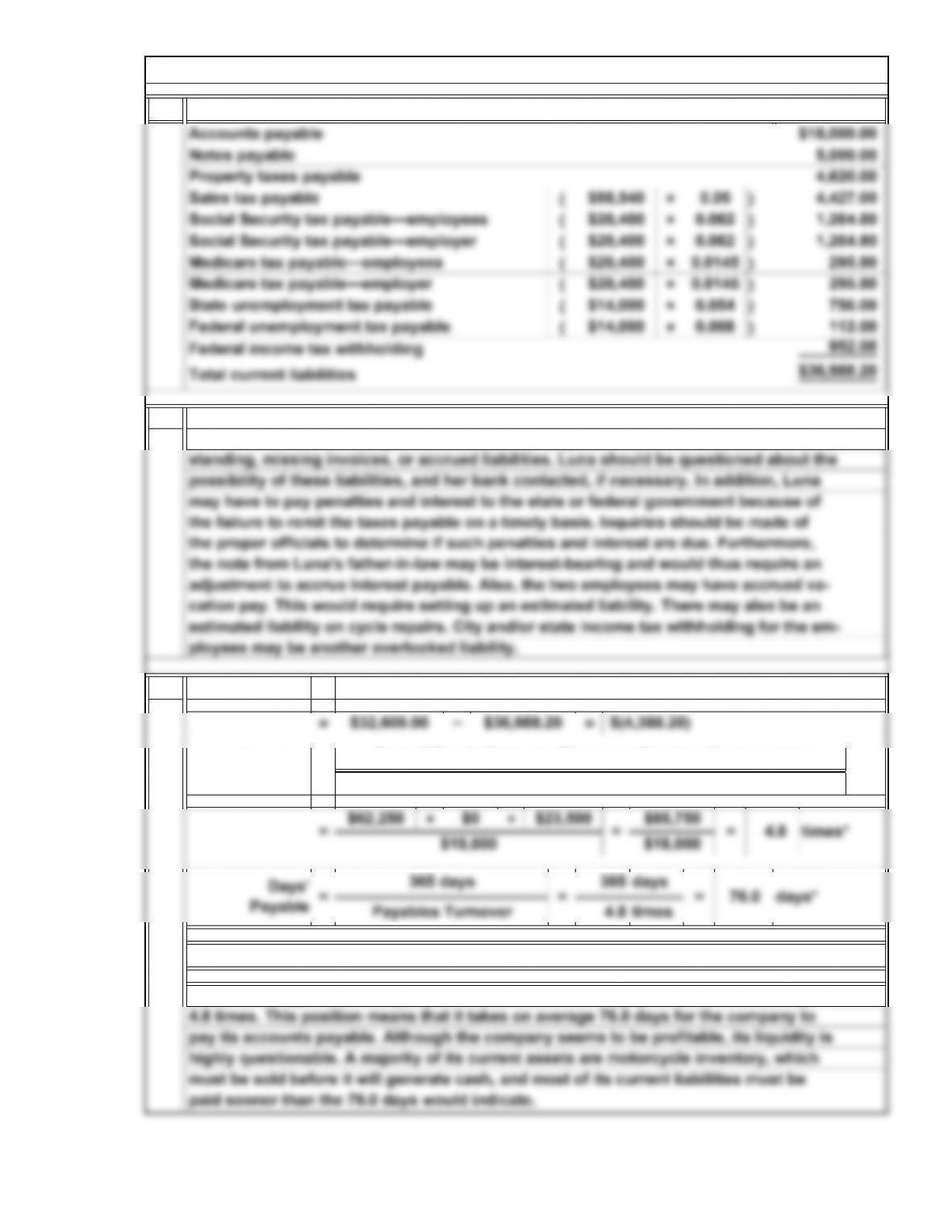

Sales tax payable

Social Security tax payable—employees

Accounts payable

Notes payable

Property taxes payable

= 4.8

$88,540

$20,400

0.05

$18,000.00

4,620.00

5,000.00

0.062

1,264.80

4,427.00

P9. Identification and Evaluation of Current Liabilities

The current liabilities of Luna Cycle Repair as of December 31, 2014, are as follows:

11-21

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. a.

2. The fundamental reason present value is a useful tool in making business decisions

is that it allows the decision maker to compare various alternatives in the present,

when business decisions are actually made.

Factor: 8%, 4 periods

P10. Applications of Present Value

Present value of a single payment (Table 1 in Appendix B)

11-22

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Cases

C1. Conceptual Understanding: Frequent Flyer Plan

If the expense and corresponding liability of frequent-flier programs are recognized, op-

erating income would be reduced and current liabilities would be increased. This is an

Another estimate of the cost would be a percentage of variable operating costs. (This cal-

culation assumes that idle capacity is used for these passengers, with additional aircraft

Finally, some students may argue that only the marginal costs of serving passengers who

are flying free should be expensed because these people would fill seats that would other-

and handle any disputed mileage credits. These costs have already been expensed as

incurred.

Many students will acknowledge the need for increased personnel to issue free tickets,

compute and record mileage credit earned, mail monthly statements to frequent fliers,

The above computations illustrate why airlines are reluctant to recognize frequent-flier

programs in their financial statements. Recognition may have a significantly negative ef-

11-23

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

C1. Conceptual Understanding: Frequent Flyer Plan (Concluded)

11-24

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Payables turnover and days’ payable computed and compared (in millions)

Payables Turnover

=Cost of Goods Sold +/‒ Change in Inventory

Accounts Payable

their industry peers.

Days’ Payable = Number of Days in a Year

Payable Turnover

365

year-end level of payables 18.9 times a year, or every 19.3 days, whereas Oracle pays its

*Rounded

Cisco Systems pays its accounts payable over 11 days faster than Oracle. Cisco pays its

C4. Interpreting Financial Reports: Comparison of Two Companies’ Ratios with Industry Ratios

11-25

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

The FASB has established two conditions for determining when a contingency should be

C5. Annual Report Case: Commitments and Contingencies

also discusses various legal matters in which it is involved and legal proceedings aris-

ing from its normal course of business. It follows to say that the management cannot

It is important to consider commitments and contingencies because if they are subse-

In its 2011 annual report, CVS talks about commitments and contingencies in note 13.

entered in the accounting records: (1) the liability must be probable, and (2) it must be

reasonably estimated.

a lease obligation or satisfies a court ruling on a lost lawsuit) they will increase the com-

pany’s current liabilities and impact its cash flows, so they need to be considered when

The note talks about lease guarantees on property leased by former CVS subsidiaries.

CVS disposed of many of its subsidiaries and the purchasers indemnified CVS of the

lease obligations, but if the purchaser or the subsidiary became insolvent, CVS would

cial condition, which is unlike the lease obligation guarantee situation.

guarantee that the results of these cases will not materially impact the company’s finan-

have to satisfy the lease obligations. As of December 31, 2011, CVS guaranteed approx-

imately 75 such store leases with maximum lease term extending up to 2022. The note

11-26

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

(+)/2

times

20.5

19.8

365 days

=

Days’ Payable =

$3,793 = times*

$75,207

2011 = $4,370 $4,026

$86,539 – $649

CVS:

Cost of Goods Sold +/‒ Change in Merchandise Inventory

Average Accounts Payable

C6. Comparison Case: Payables Analysis

Payables Turnover

Payables turnover and days’ payable computed (in millions)

=

Payables Turnover

Payables Turnover =

Walgreens:

Cost of Goods Sold +/‒ Change in Merchandise Inventory

Average Accounts Payable

C6. Comparison Case: Payables Analysis (Concluded)

11-28

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

C7. Ethical Dilemma: Known Legal Violations

The alternatives available to Swift are as follows:

Alternative 1 is the worst choice because it is unethical to be associated with an ille-

gal activity. Swift would be subjecting himself to possible criminal action, and, if the

maneuver were discovered, it would be difficult for Swift ever to get an accounting job

again.

Although Alternative 3 is probably the least confrontational action, it is also unethical

This case actually happened to one of the author’s students, who sought the author’s

Failure to withhold and remit income and payroll taxes is a serious criminal offense.

11-29

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

3.

4.

C8. Business Communication: Baseball Contract

Memorandum

Date: Today’s Date

Re: Management Contract Offer

Management’s offer does not accurately reflect the value to you because it does not

To: Devon Turner

From: Student

by using a table to calculate the present value of the offer:

Because the offer lies so far in the future, it is actually worth only about $6.0 million

If you refuse the new contract, you could have a few bad years or become in-

Other considerations in evaluating the offer are as follows:

The choice of interest rate should be considered. The bank prime rate may not

Whether or not the contract is guaranteed if you are injured or otherwise cannot

play will affect the amount of risk.

a present value of $10.5 million per year, you might propose a signing bonus of

$17,850,000 ($42,000,000 – $24,150,000). Since management is unlikely to agree to

this bonus, the range of the possible bonus is from zero or no bonus to $17,850,000.

Note to Instructor: Answers will vary depending on the company selected by the

C9. Continuing Case: Annual Report Project

students.

The new contract may not adequately reflect increases in salaries over the next

11-30

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.