DQ1.

DQ2.

DQ3.

DQ4.

DQ5.

DQ6.

current liabilities, the results could overwhelm the earnings and create negative

cash flows from operating activities.

statement.

cash flows are the details of the changes. For instance, cash flows from oper-

ating activities is a very important figure that cannot be seen on any other

The change in cash from year to year, while important, can easily be obtained

from the comparative balance sheets. What is important from the statement of

CHAPTER 15—Solutions

THE STATEMENT OF CASH FLOWS

Discussion Questions

to the goal of profitability, whereas the statement of cash flows is more closely

tied to the goal of liquidity.

Cash flows to sales and cash flows to assets would be less than profit margin

and return on assets, respectively, because a cash flow yield of 1.0 means that

cash flows from operations are less than net income. Both are numerators in

ratios that have the same denominators.

Gains and losses from operating activities are directly related to the cash flows

from the sale of assets reported in the investing activities section.

Both purchases of treasury stock and dividend payments represent payments

to stockholders. Each diverts cash from productive use in the business (as

assets), and thus each reduces free cash flow.

If a company has large gains, large increases in current assets, or decreases in

The statements are equally useful. The income statement relates most directly

15-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 4.

2. 5.

3. 6.

b

Schedule of Cash Flows from Operating Activities

c

Short Exercises

SE1. Classification of Cash Flow Transactions

c

a

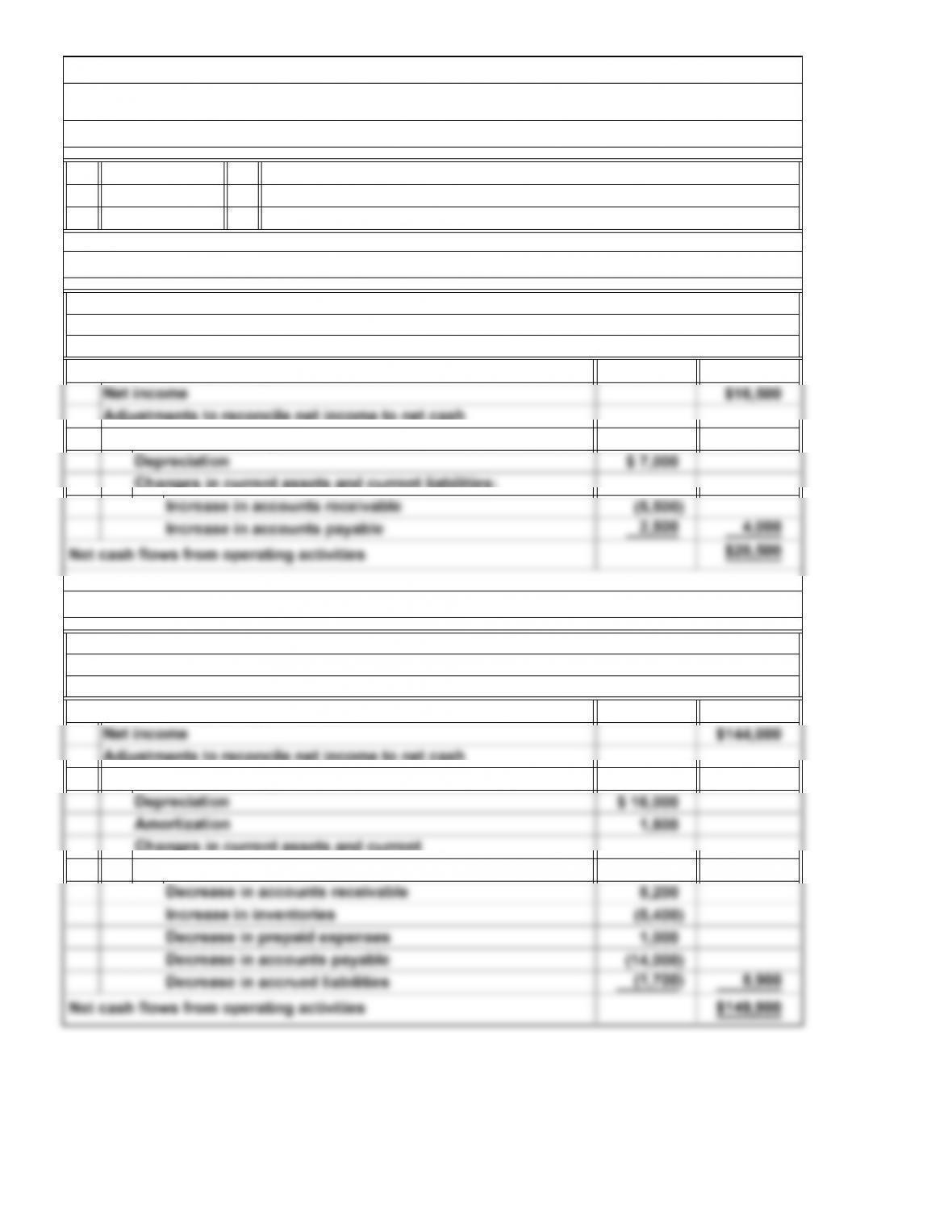

SE2. Computing Cash Flows from Operating Activities: Indirect Method

Stewart Construction Corporation

d

c

For the Year Ended December 31, 2014

Cash flows from operating activities:

15-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 5.

2. 6.

3. 7.

4. 8.

SE6. Identifying Components of the Statement of Cash Flows

ba

ca

ed

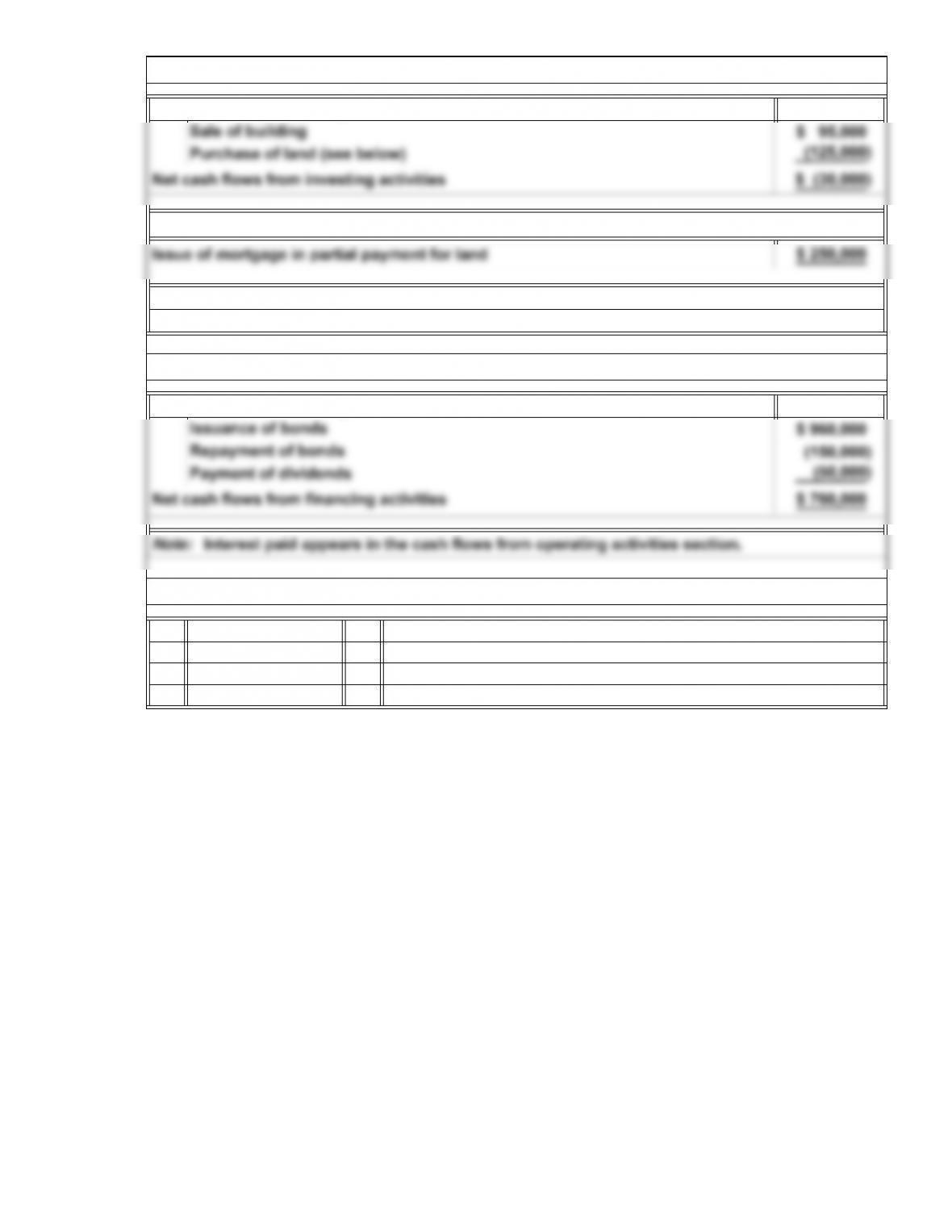

Cash flows from investing activities:

a

c

SE4. Cash Flows from Investing Activities and Noncash Transactions

15-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

( + ) / 2

‒‒+

place its depreciable assets, as indicated by a decline in the gross amount of equip-

ment, it did reduce liabilities by 25 percent. Overall the company improved its liquidity

and its ability to borrow for possible future expansion.

SE8. Cash-Generating Efficiency Ratios and Free Cash Flow

The cash flow yield is 0.7 times, which indicates that cash flows from operations are

that the company was able to finance its net expenditures for land and equipment from

its cash flows from operations after paying dividends. Although the company did not re-

to sales because the asset turnover is slightly more than 1. Because cash flow yield is

$240,000

*

$360,000 $40,000

22.8%

$80,000

Purchases of Plant Assets + Sales of Plant Assets

=

Net Cash Flows from Operating Activities ‒ Dividends ‒ Free Cash Flow =

Average Total Assets

$1,100,000 $1,000,000 =

$360,000

=$360,000 =

$1,580,000

Cash Flows to Sales = Net Cash Flows from Operating Activities

Sales

Cash Flow Yield = Net Cash Flows from Operating Activities

Net Income

SE7. Cash-Generating Efficiency Ratios and Free Cash Flow

*Rounded

Cash Flows to Assets = Net Cash Flows from Operating Activities

15-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. 6. 11.

2. 7. 12.

3. 8. 13.

4. 9.

5. 10.

Exercises: Set A

a

c

b

a

b

d

c

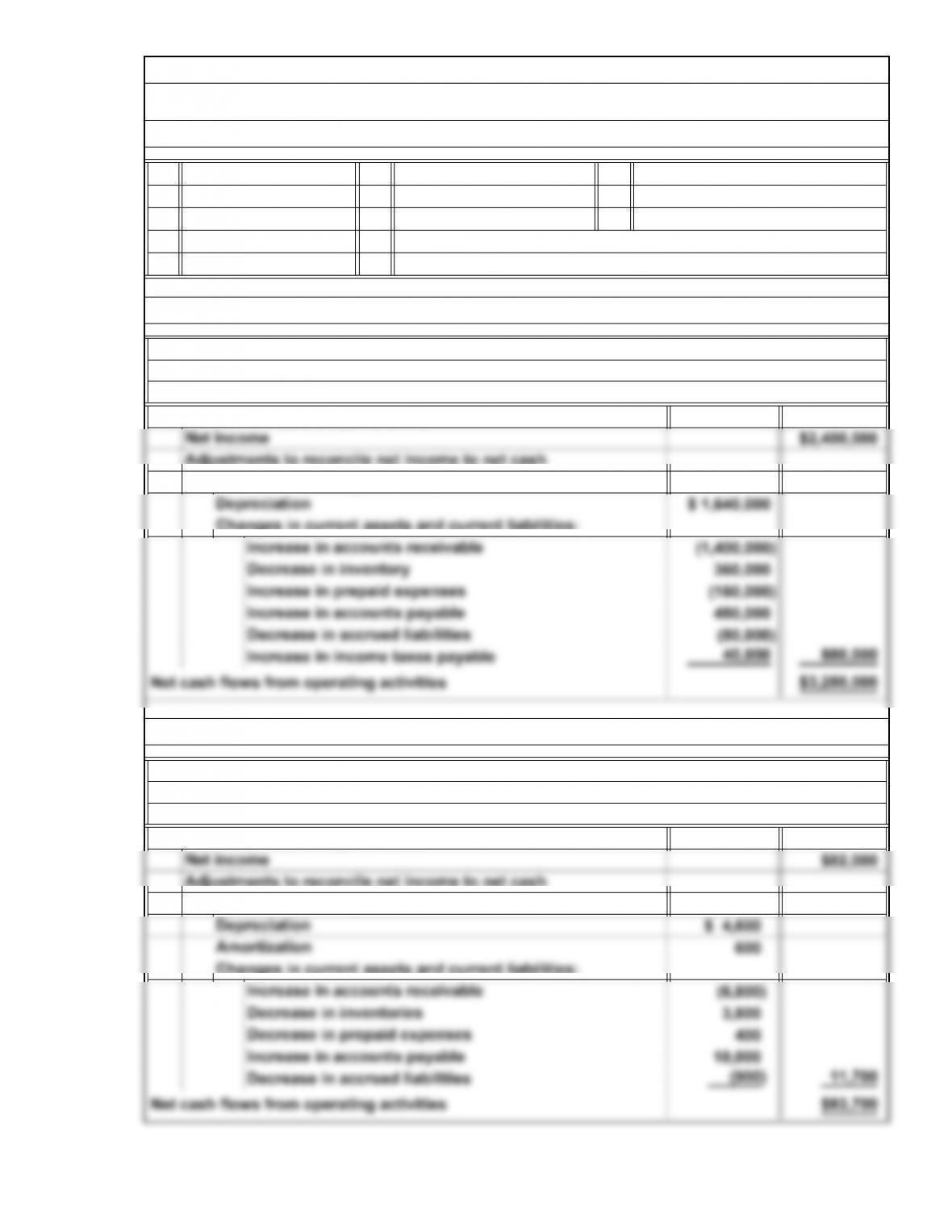

Cash flows from operating activities:

Conti Chemical Company

d

a

a b and a e

c

Schedule of Cash Flows from Operating Activities

For the Year Ended December 31, 2014

E1A. Classification of Cash Flow Transactions

E2A. Cash Flows from Operating Activities: Indirect Method

15-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

a.

b.

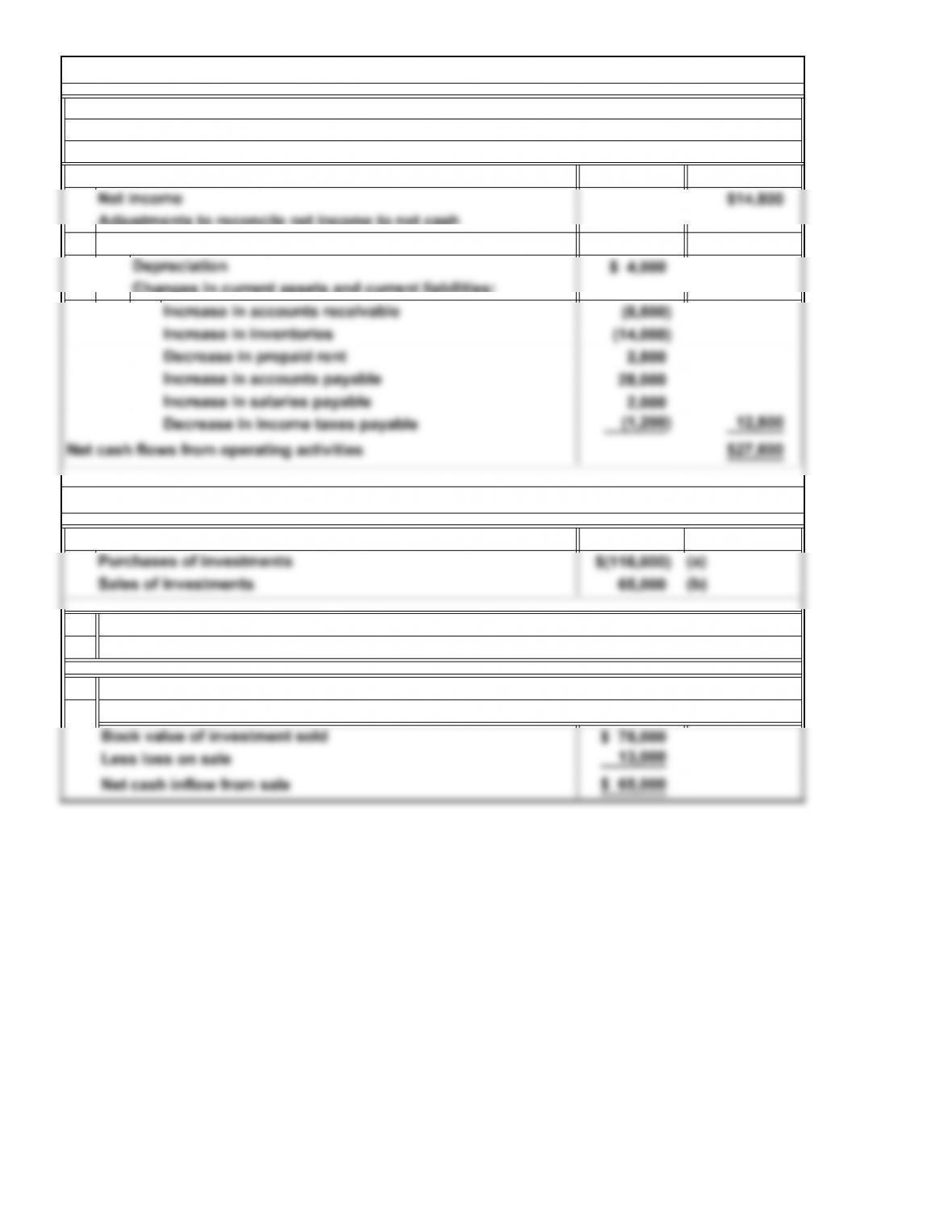

T account shows purchases of investments to be $116,000, which is an outflow

Flake Corporation

E4A. Preparing a Schedule of Cash Flows from Operating Activities: Indirect Method

Schedule of Cash Flows from Operating Activities

For the Year Ended June 30, 2014

T account shows $78,000 of investments sold. There was a $13,000 loss on the

of cash.

Cash flows from operating activities:

sale. The net cash flow from the sale is computed as follows:

15-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

a.

E6A. Computing Cash Flows from Investing Activities: Plant Assets

T account shows total purchases of plant assets of $67,200, which is an out-

Cash flows from investing activities:

flow of cash.

15-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

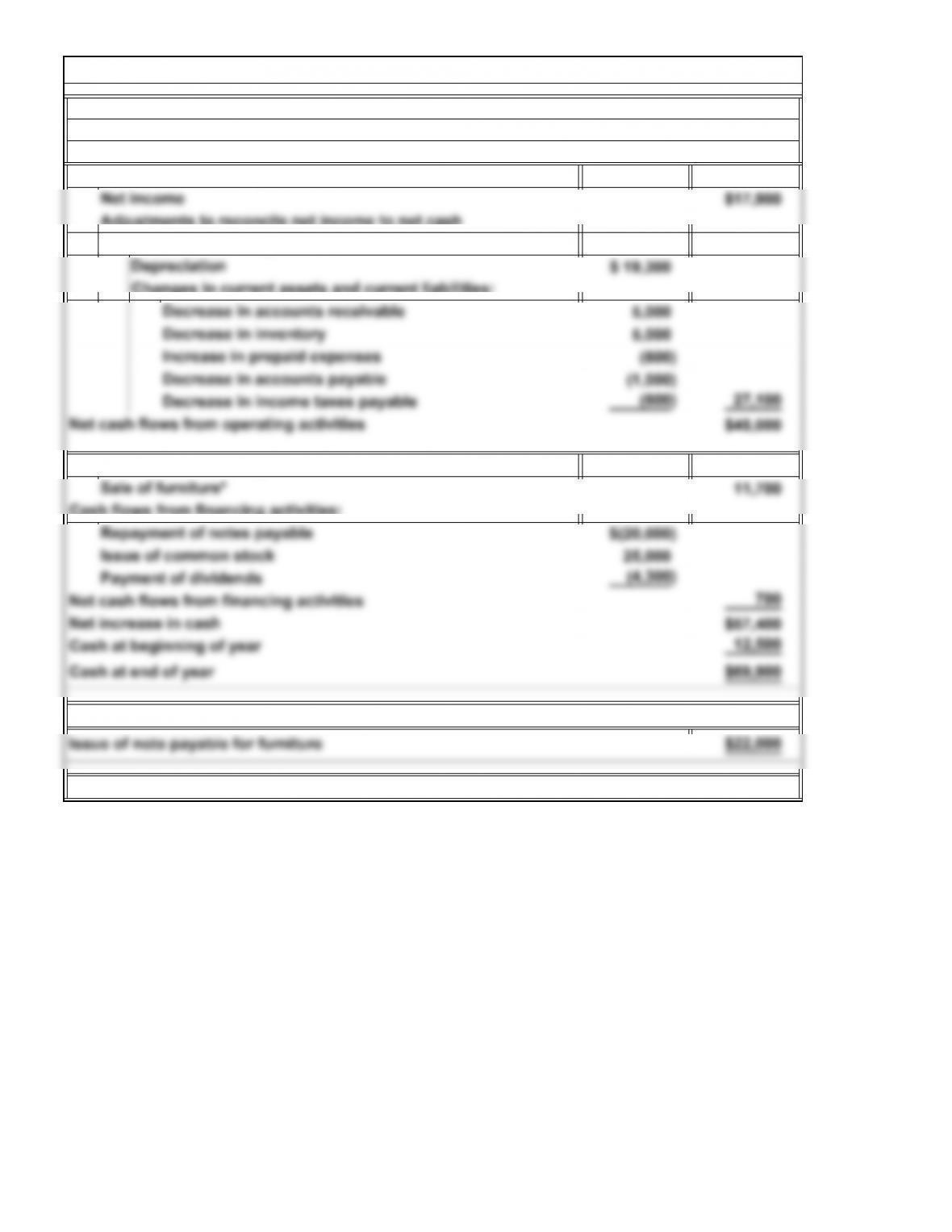

Keeper Corporation

E8A. Preparing the Statement of Cash Flows: Indirect Method

Statement of Cash Flows

For the Year Ended June 30, 2014

Cash flows from operating activities:

*$27,000 – $15,300 = $11,700

15-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.