1.

7.

A company would spend millions of dollars on goodwill because the company anti-

CHAPTER 10—Solutions

LONG-TERM ASSETS

Discussion Questions

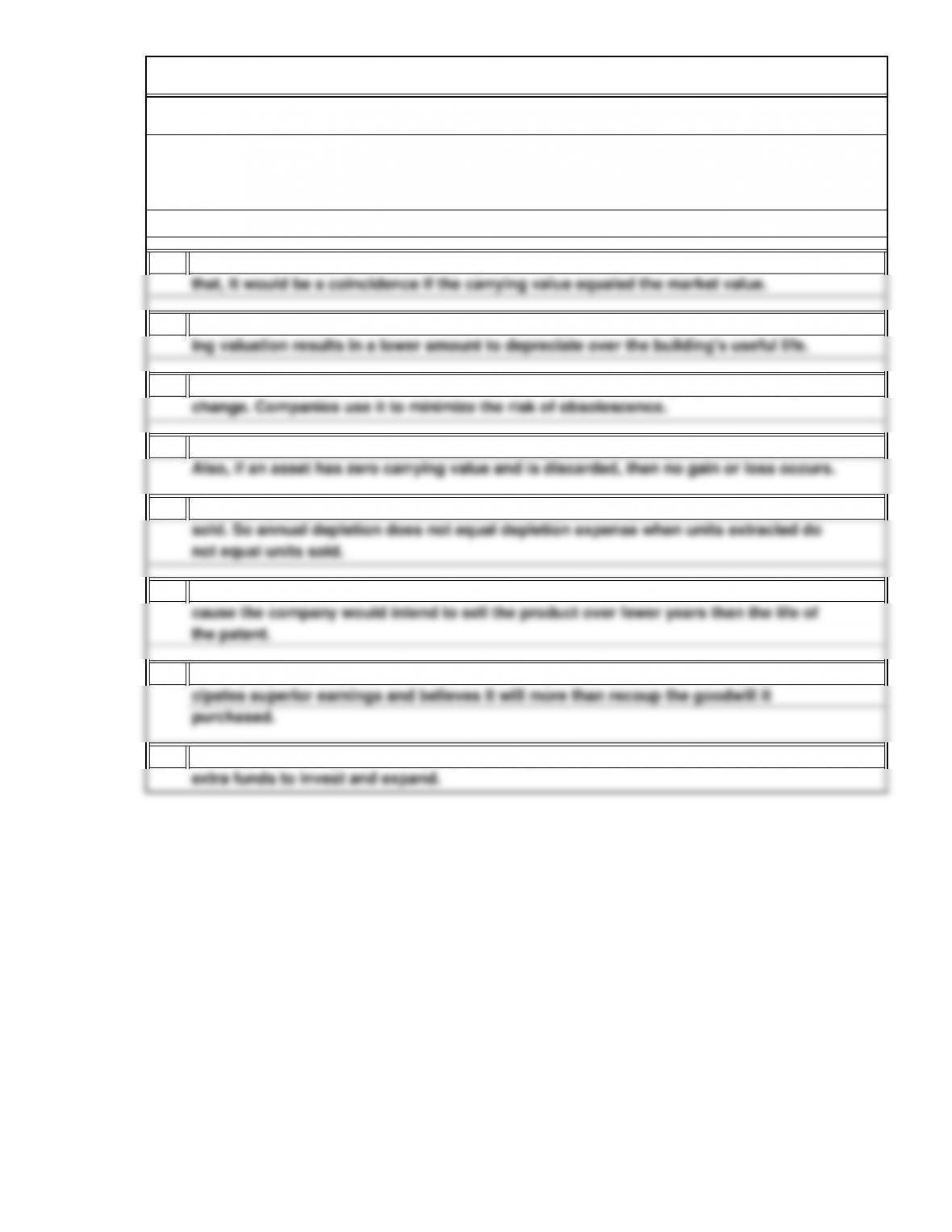

On the date of acquisition, the carrying value equals the current market value. After

10-1

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Apportionment*

*Rounded

Short Exercises

SE1. Classifying Cost of Long-Term Assets

SE2. Group Purchase

Percentage

Asset

Appraisal

$1,875

8,000 $2,250

– $750 2,200

) ×

– $750 2,000

=

$1,313( $8,250 – $750 1,400 =Year 4:

) ×

8,000

) ×

8,000

8,000

$2,063$8,250(

Year 2: $8,250(

Year 3: =

*

*

10-2

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1. =

=–

=

2. a.

=

=

b.

=

=

c.

=

=

$1,600

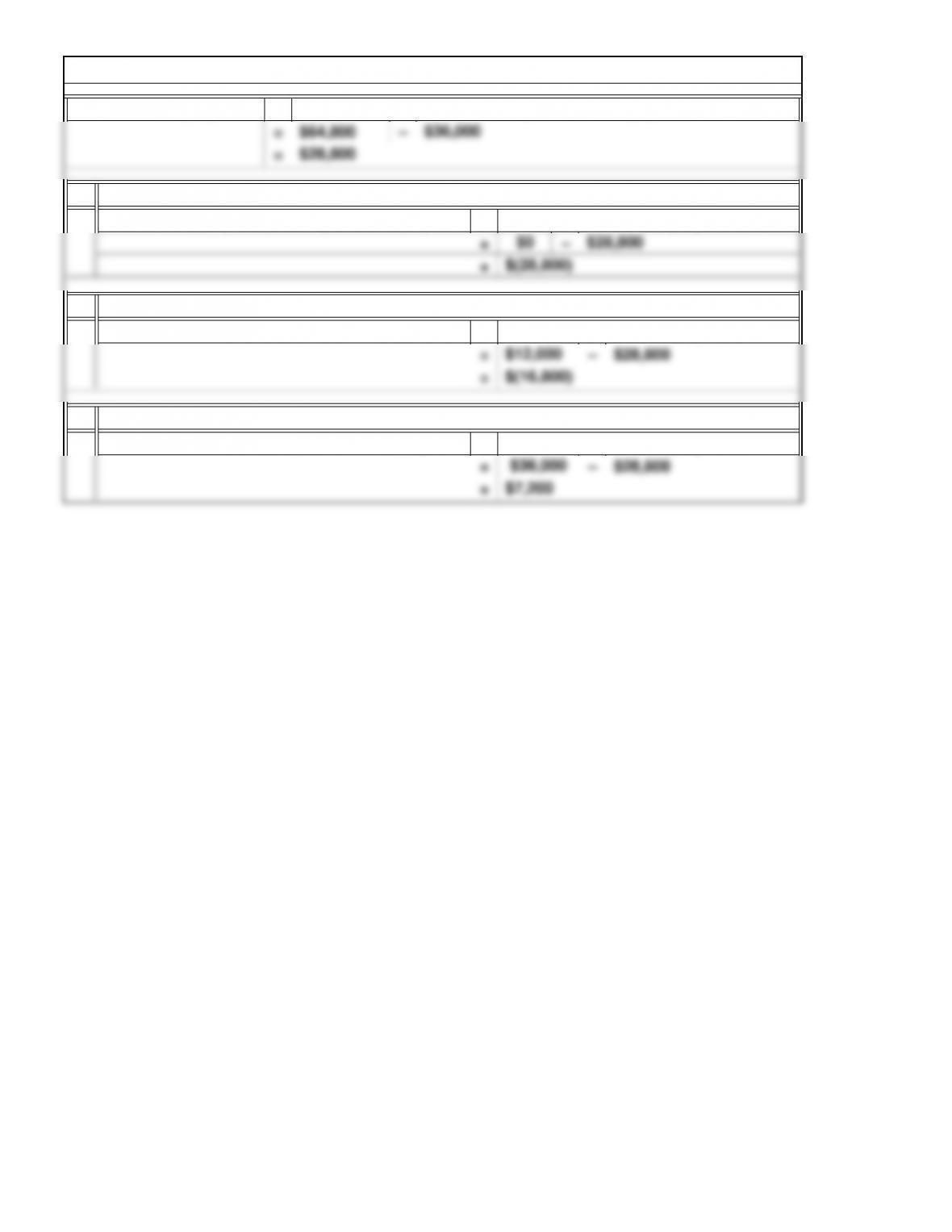

Gain (Loss) on Sale of Equipment

Cash Received – Carrying ValueGain (Loss) on Sale of Equipment

$14,400

$32,400 $18,000

SE5. Double-Declining-Balance Method

Depreciation for

SE6. Disposal of Plant Assets: No Trade-In

Asset sold for $6,000 cash

Asset sold for $16,000 cash

Cash Received – Carrying Value

Cash Received – Carrying ValueGain (Loss) on Disposal of Equipment

Asset discarded as having no value

$(14,400)

$(8,400)

Carrying Value Equipment – Accumulated Depreciation—Equipment

10-3

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

2. 5.

3. 6.

SE7. Natural Resources

SE8. Intangible Assets: Computer Software

c

c

b

a

The research and development costs are expensed as incurred. The costs after the work-

–

Free

Cash Flow =Net Cash Flows from

Operating Activities

SE10. Free Cash Flow

This amount of free cash is the amount of cash that Maki Corporation has available for

–

Purchases of

Plant Assets +

Dividends

other purposes, such as expansion or investment, after it deducts the funds it has com-

mitted to continue operations at the planned level.

Sales of

Plant Assets

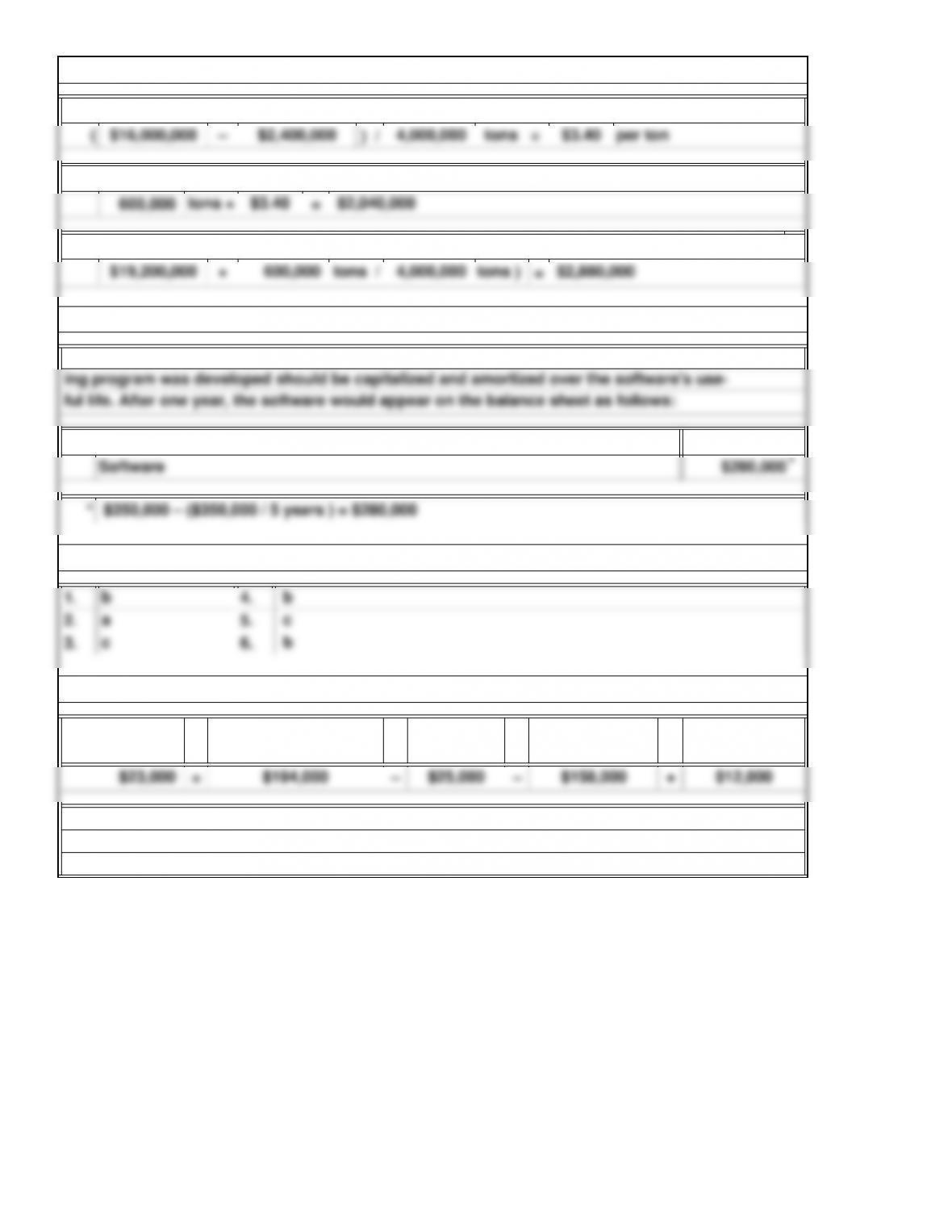

Depletion charge per ton:

10-4

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

3.

4.

5.

6.

Apportionment*

Cost of land:

A total of $338,400 should be debited to the Land account, and $78,400 should be debited

CE, N

CE, ER

RE, N

CE, A

E2A. Recognizing and Classifying the Cost of Long-Term Assets

Exercises: Set A

E1A. Recognition and Classification of Capital Expenditures

PercentageAppraisal

$240,000

Asset

E3A. Group Purchase

10-5

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

1.

2.

21,600

21,600

$90,000

57,600

$32,400

$36,000 + $21,600 = $57,600

First year’s depreciation:

100% / 5 = 20%; 20% × 2 = 40%

*

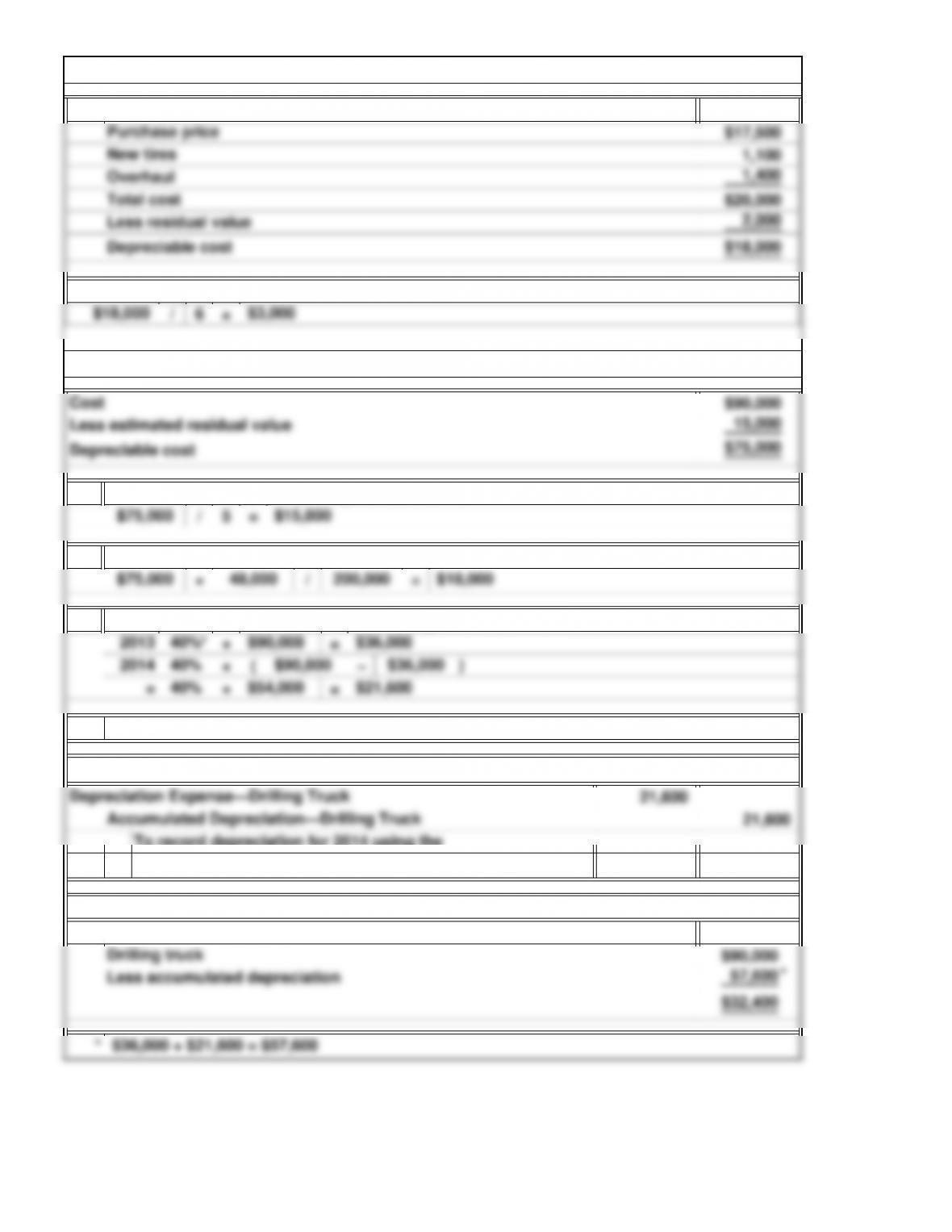

E4A. Cost of Long-Term Asset and Depreciation

Cost and depreciable cost of tractor:

Adjusting entry:

Drilling truck

double-declining-balance method

*

Balance sheet presentation:

Depreciation computed by straight-line method:

To record depreciation for 2014 using the

E5A. Depreciation Methods

Depreciation computed by production method:

Less accumulated depreciation

Property, plant, and equipment

Depreciation Expense—Drilling Truck

Accumulated Depreciation—Drilling Truck

*

10-6

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

Year 1 × =

Year 2 × ( – ) = ×

/10=

/10=

–2 =5

First-year depreciation:

$560,000 $ 56,000

Depreciation to date:

Second-year depreciation:

E7A. Revision of Depreciation Rates

years years years

56,000

$112,000

100% / 4 = 25%; 25% × 2 = 50%

50%

Remaining depreciable cost:

$560,000

$1,120

$1,120 $560

$560 50% = $280

E6A. Double-Declining-Balance Method

50%

$560

Remaining useful life:

7

Third-year depreciation:

*

*

*

10-7

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.

=

1.

=

2.

=

Cash Received – Carrying ValueGain (Loss) on Sale of Equipment

Asset sold for $12,000 cash

Cash Received – Carrying Value

E8A. Disposal of Plant Assets

Carrying Value

Gain (Loss) on Disposal of Equipment

Asset discarded as having no value

Equipment – Accumulated Depreciation—Equipment

10-8

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in whole or in part.